© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 11 21

Exercise 11-7 (continued)

4. Each office’s individual performance should be based on the scorecard

measures only if the measures are controllable by those employed at

the branch offices. In other words, it would not make sense to attempt

to hold branch office managers responsible for measures such as the

percent of job offers accepted or the amount of compensation paid

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

22 Managerial Accounting, 16th Edition

Exercise 11-8 (15 minutes)

1. ROI computations:

Net operating income Sales

ROI = ×

Sales Avera

g

e operatin

g

assets

Queensland Division:

2. The manager of the New South Wales Division seems to be doing the

better job. Although the New South Wales Division’s margin is three

percentage points lower than the margin of the Queensland Division, its

Notice that if you look at margin alone, then the Queensland Division

appears to be the stronger division. This fact underscores the

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 11 23

Exercise 11-9 (15 minutes)

Company A Company B Company C

Sales (a)…………………………….. $9,000,000 * $7,000,000 * $4,500,000 *

Net operatin

g

income (b) ……….. $540,000 $280,000 * $360,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

24 Managerial Accounting, 16th Edition

Exercise 11-10 (20 minutes)

1.

(b) (c)

Net Average

(a) Operating Operating ROI

Sales Income* Assets (b) ÷ (c)

$2,500,000 $475,000 $1,000,000 47.5%

$2,600,000 $500,000 $1,000,000 50.0%

$2,700,000 $525,000 $1,000,000 52.5%

2. The ROI increases by 2.5% for each $100,000 increase in sales. This

happens because each $100,000 increase in sales brings in an additional

profit of $25,000. When this additional profit is divided by the average

operating assets of $1,000,000, the result is an increase in the

company’s ROI of 2.5%.

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 11 25

Exercise 11-11 (30 minutes)

1. Net operating income

Margin = Sales

Sales

Turnover =

A

vera

g

e operatin

g

assets

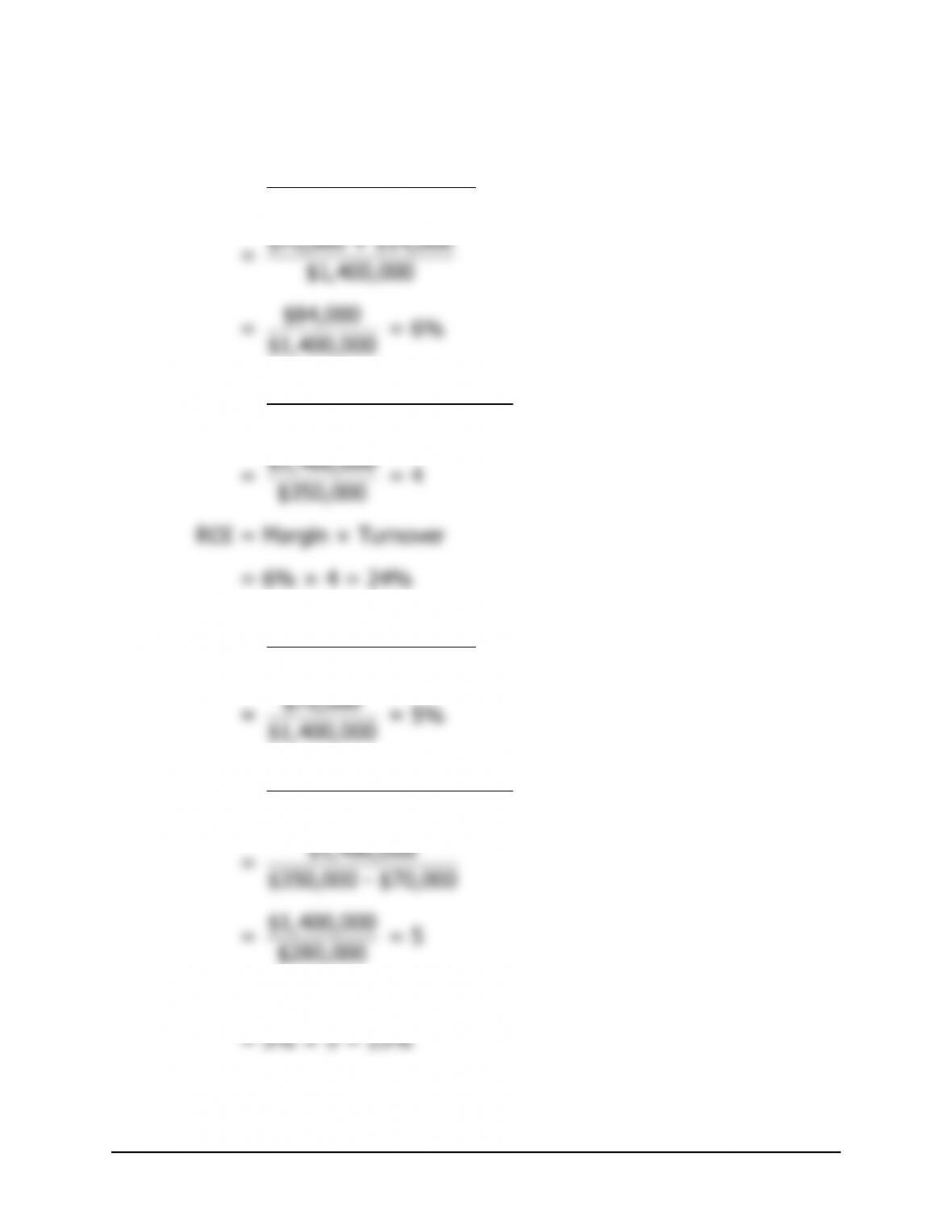

ROI = Margin × Turnover

2. Net operating income

Margin = Sales

Sales

Turnover =

A

vera

g

e operatin

g

assets

$1,400,000 + $70,000

= $350,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

26 Managerial Accounting, 16th Edition

Exercise 11-11 (continued)

3. Net operatin

g

income

Margin = Sales

Sales

Turnover =

A

vera

g

e operatin

g

assets

4. Net operatin

g

income

Mar

g

in =

Sales

Sales

Turnover =

A

vera

g

e operatin

g

assets

ROI = Margin × Turnover

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 11 27

Exercise 11-12 (30 minutes)

1. ROI computations:

Net operating income Sales

ROI = ×

Sales Avera

g

e operatin

g

assets

Division A:

Division B:

Division C:

2.

Division A Division B Division C

A

vera

g

e operatin

g

assets ……… $3,000,000 $7,000,000 $5,000,000

Required rate of return ………… × 14% × 10% × 16%

Minimum required return ……… $ 420,000 $ 700,000 $ 800,000

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

28 Managerial Accounting, 16th Edition

Exercise 11-12 (continued)

3. a. and b.

Division A Division B Division C

Return on investment (ROI)……….. 20% 8% 16%

T

herefore, if the division is

presented with an investment

opportunity yielding 15%, it

probably would ……………..……… Reject Accept Reject

Minimum required return for

If performance is being measured by ROI, both Division A and Division C

probably would reject the 15% investment opportunity. These divisions’

ROIs currently exceed 15%; accepting a new investment with a 15%

If performance is measured by residual income, both Division A and

Division B probably would accept the 15% investment opportunity. The

15% rate of return promised by the new investment is greater than their

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 11 29

Exercise 11-13 (15 minutes)

1. Net operating income

Margin = Sales

Sales

Turnover =

A

vera

g

e operatin

g

assets

ROI = Margin × Turnover

2. Net operatin

g

income

Margin = Sales

Sales

Turnover =

A

vera

g

e operatin

g

assets

$3,000,000(1.00 + 0.50)

= $750,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

30 Managerial Accounting, 16th Edition

Exercise 11-13 (continued)

3. Net operating income

Margin = Sales

Sales

Turnover =

A

vera

g

e operatin

g

assets

ROI = Margin × Turnover