© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 10B 81

Exercise 10B-3 (continued)

4. The Work in Process will increase by $388,800 computed as follows:

5. The Finished Goods will increase by $903,960 computed as follows:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

82 Managerial Accounting, 16th Edition

Exercise 10B-4 (30 minutes)

1a. The Raw Materials will increase by $720,000 computed as follows:

1b. The Cash will decrease by $660,000 computed as follows:

1c. The materials price variance is computed as follows:

Materials price variance = AQ(AP – SP)

2a. The Raw Materials will decrease by $720,000 computed as follows:

2b. The Work in Process will increase by $672,000 computed as follows:

Standard quantity allowed (28,000 units

2c. The materials quantity variance is computed as follows:

Materials quantity variance = SP (AQ – SQ)

3a. The Work in Process will increase by $630,000 computed as follows:

Standard hours allowed (28,000 units

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 10B 83

Exercise 10B-4 (continued)

3b. The Cash decrease by $600,000 computed as follows:

3c. The labor rate variance is zero because the actual rate (see

requirement 3b) and the standard rate are both $15.00 per hour. The

labor efficiency variance is computed as follows:

4a. The Work in Process will increase by $1,680,000 computed as follows:

Standard hours allowed (28,000 units

4b. The fixed overhead budget and volume variances are computed as

follows:

Budget variance = Actual fixed overhead – Budgeted fixed overhead

Volume variance = Budgeted fixed overhead – Fixed overhead applied

5. The Finished Goods will increase by $2,982,000 computed as follows:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

84 Managerial Accounting, 16th Edition

Problem 10B-5 (60 minutes)

1. The manufacturing cost variances are computed as follows:

Materials price variance = AQ(AP – SP)

*95,000 units × 2 pounds per unit = 190,000 pounds

Labor rate variance = AH(AR – SR)

Budget variance = Actual fixed overhead – Budgeted fixed overhead

Budget variance = $2,740,000 – $2,880,000 = $140,000 F

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 10B 85

Problem 10B-5 (continued)

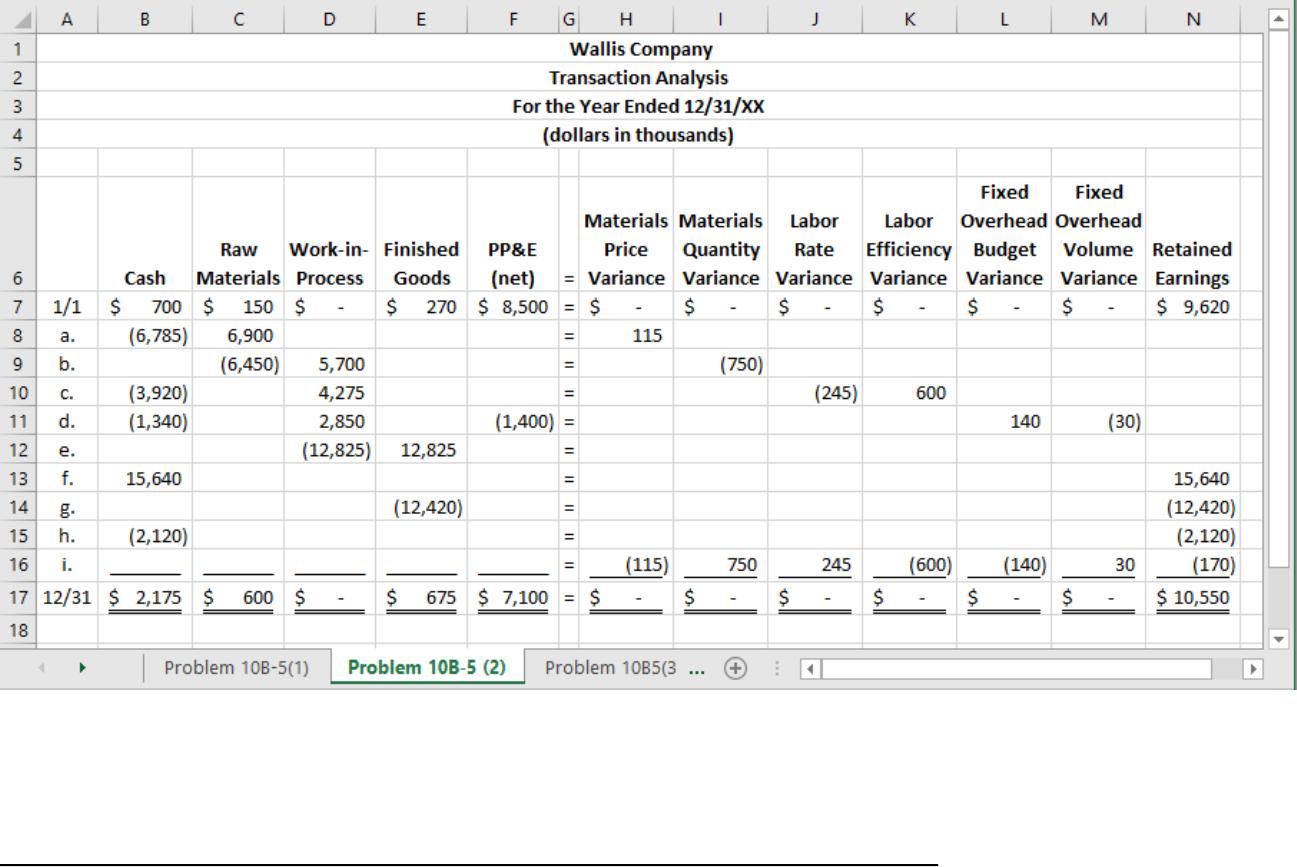

2 and 3: The transactions (including the ending balances) are recorded as follows:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

86 Managerial Accounting, 16th Edition

Problem 10B-5 (continued)

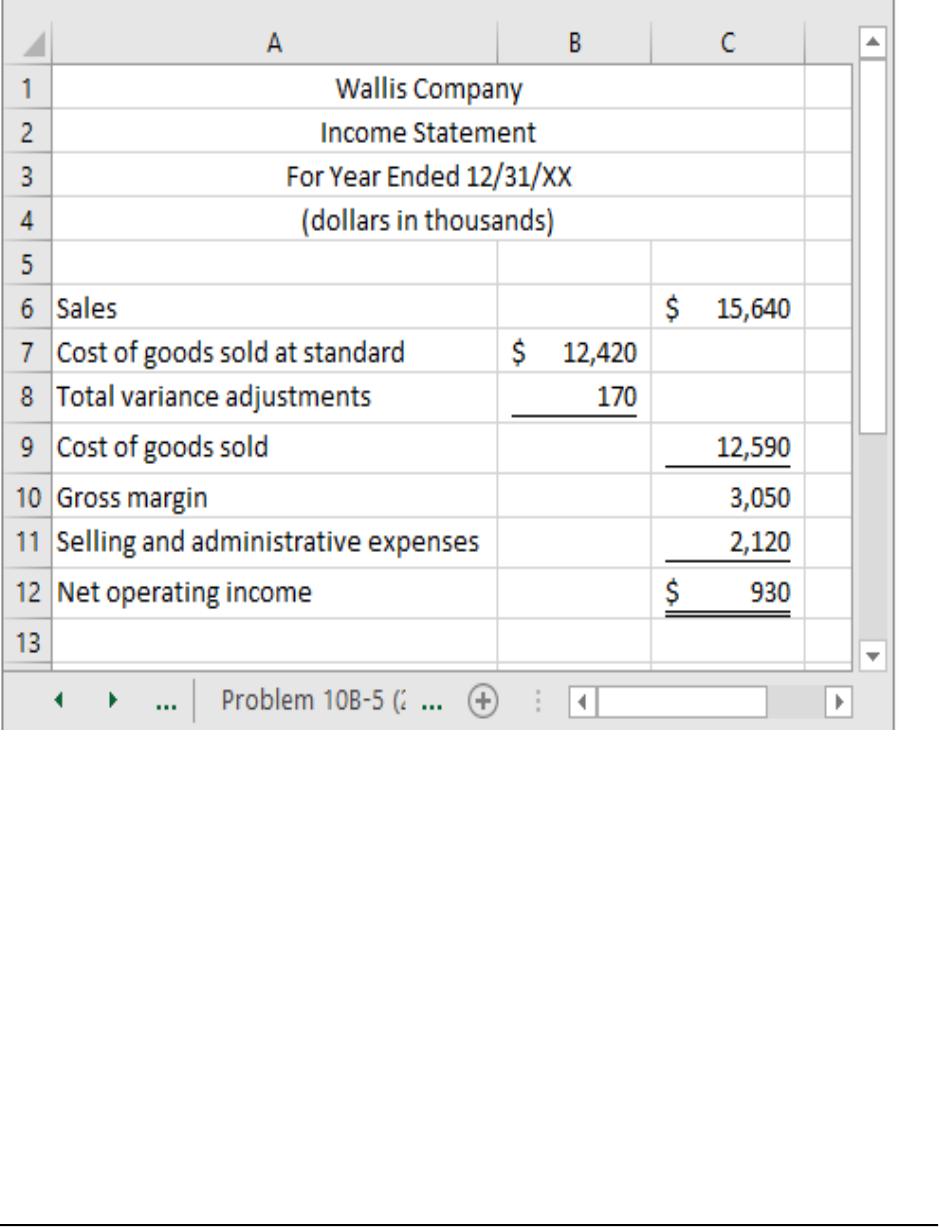

4. The income statement is computed as follows:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 10B 87

Problem 10B-6 (60 minutes)

1. The manufacturing cost variances are computed as follows:

Materials price variance = AQ(AP – SP)

Labor rate variance = AH(AR – SR)

265,000 hours ($15.00 per hour – $16.00 per hour) = $265,000 F

Labor efficiency variance = SR(AH – SH)

$16.00 per hour (265,000 hours – 250,000 hours) = $240,000 U

Variable overhead efficiency variance = SR(AH – SH)

$2.00 per hour (265,000 hours – 250,000 hours) = $30,000 U

Budget variance = Actual fixed overhead – Budgeted fixed overhead

Note: The budgeted fixed overhead of $2,400,000 is computed as

follows:

T

otal bud

g

eted overhead (a) ……………………………. $2,880,000

V

ariable portion of the bud

g

et (240,000 DLH ×$2.00

T

g

–

Note: The fixed overhead applied of $2,500,000 is computed as follows:

Standard labor-hours allowed (a) ………………………. 250,000

Fixed portion of the predetermined overhead rate

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

88 Managerial Accounting, 16th Edition

Problem 10B-6 (continued)

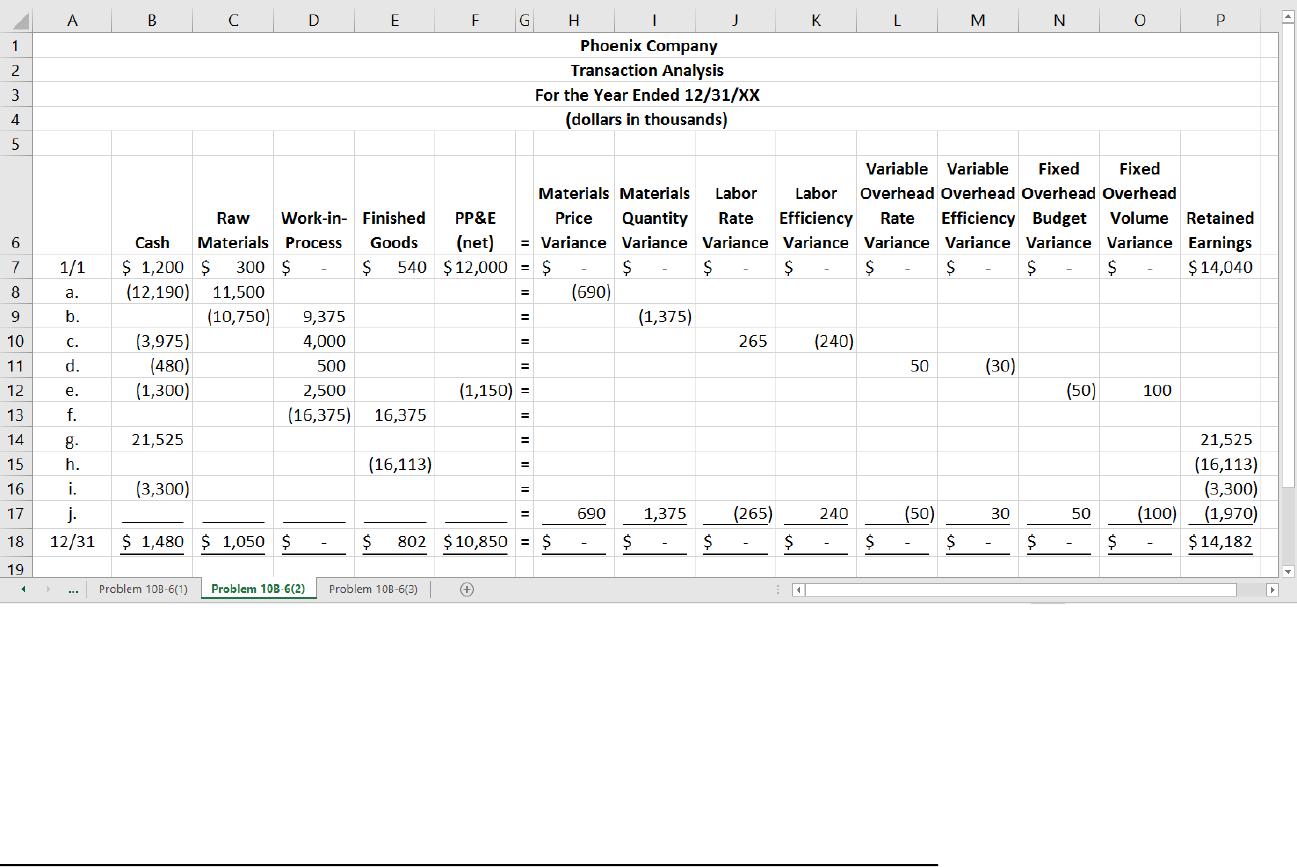

2 and 3. The transactions (including the ending balances) are recorded as follows:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 10B 89

Problem 10B-6 (continued)

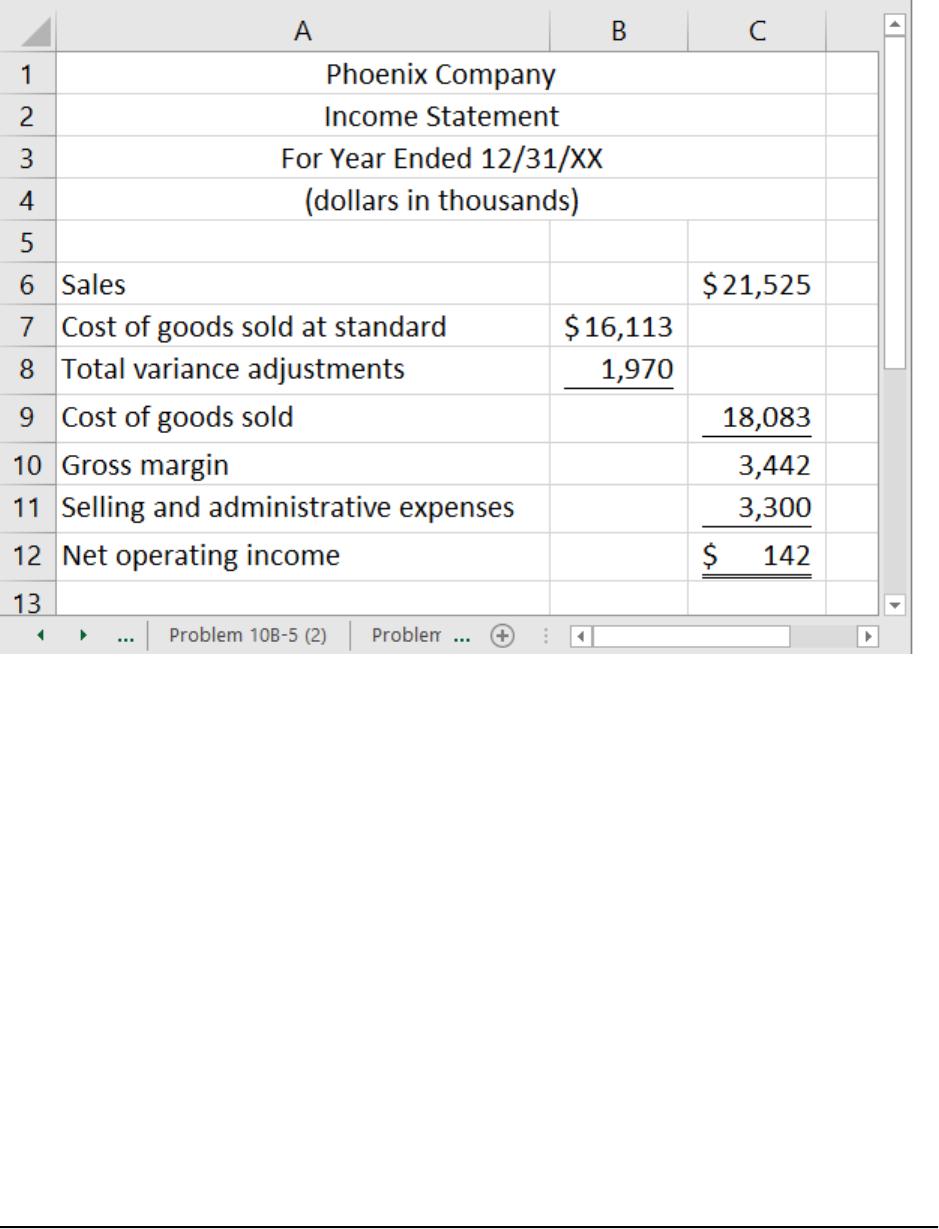

4. The income statement is computed as follows: