© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 10A 61

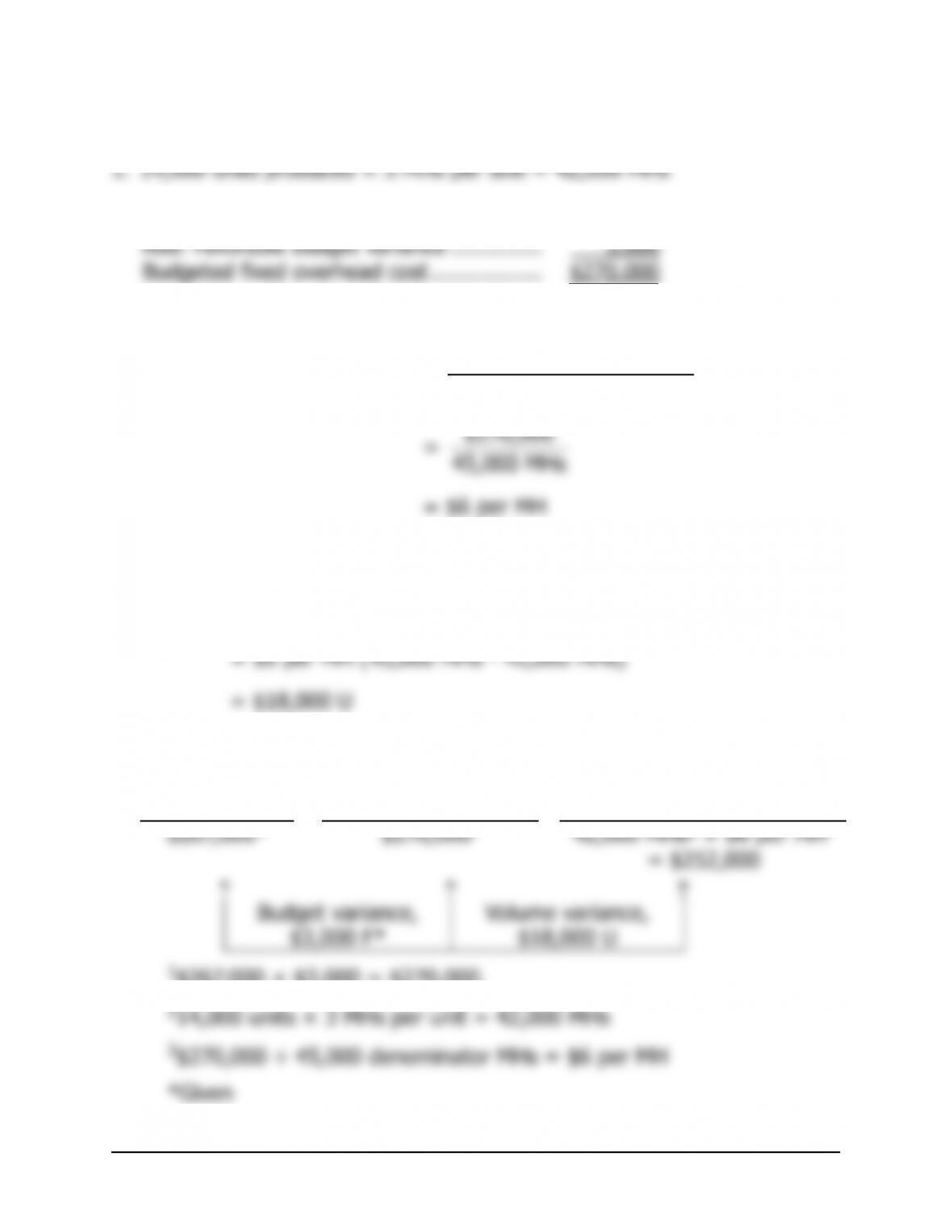

Exercise 10A-7 (15 minutes)

2.

A

ctual fixed overhead incurred……………. $267,000

A

g

3.

Budgeted fixed overhead

Fixed element of the =

predetermined overhead rate Denominator activity

4. Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

overhead rate allowed

æö

÷

ç

÷

ç

÷

ç

÷

ç

÷

ç

èø

Alternative solution to parts 1-3:

A

ctual Fixed

Overhead

Bud

g

eted Fixed

Overhead

Fixed Overhead Applied

to Work in Process

g

v

v

1

3

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

62 Managerial Accounting, 16th Edition

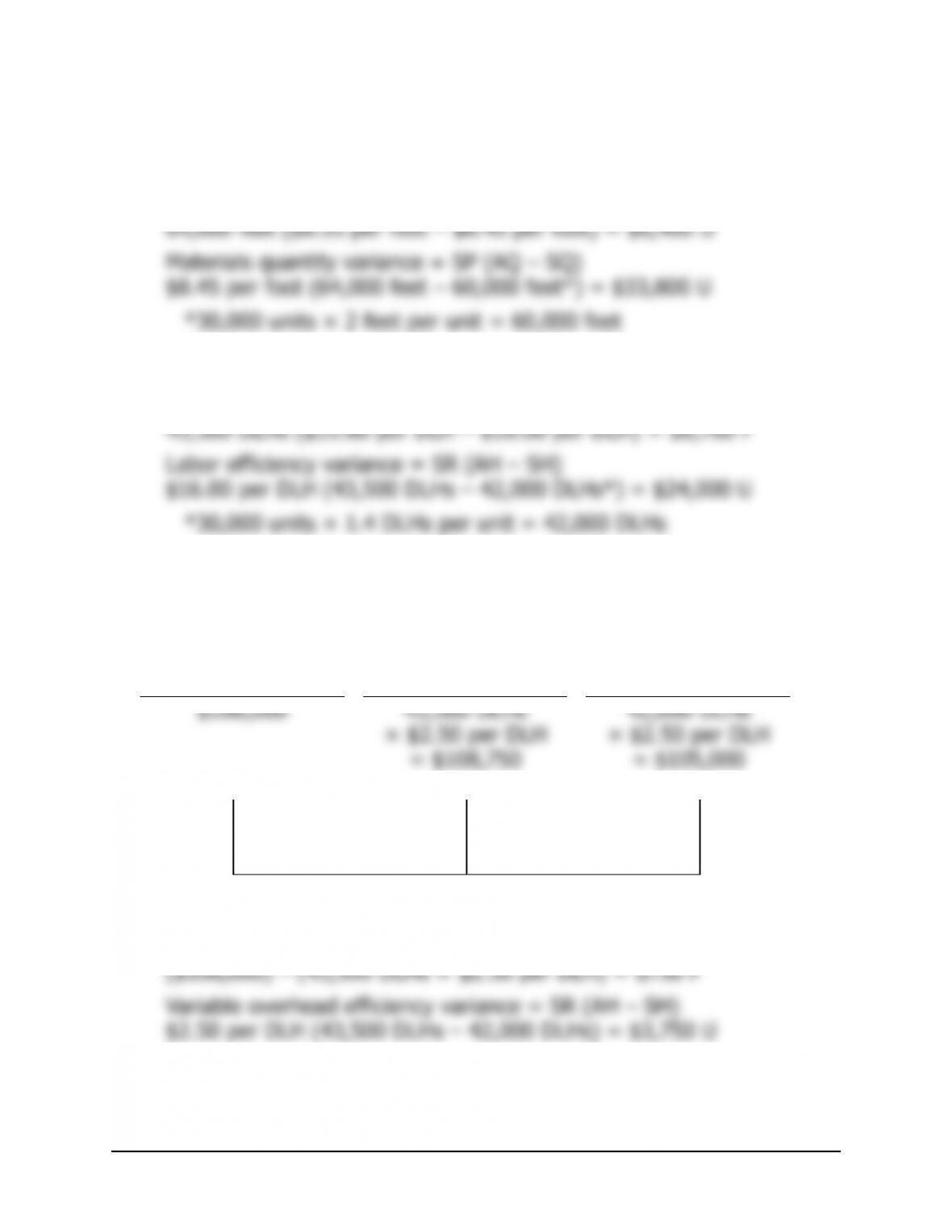

Problem 10A-8 (45 minutes)

1. $600,000

T

otal rate: = $10 per DLH

60,000 DLHs

2. Direct materials: 3 pounds at $7 per pound ………. $21

Direct labor: 1.5 DLHs at $12 per DLH……………… 18

V

b. Manufacturin

g

Overhead

A

A

4. Variable overhead variances:

A

ctual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH ×

A

R) (AH × SR) (SH × SR)

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 10A 63

Problem 10A-8 (continued)

Alternative solution:

Variable overhead rate variance = (AH × AR) – (AH × SR)

Fixed overhead variances:

A

ctual Fixed

Overhead

Bud

g

eted Fixed

Overhead

Fixed Overhead

Applied to Work in Process

g

v

v

Alternative solution:

Budget variance:

Bud

g

et Actual fixed Bud

g

eted fixed

= –

variance overhead overhead

Volume variance:

æ

ö

÷

ç

÷

ç

÷

ç

÷

ç

÷

÷

ç

è

ø

Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

overhead rate allowed

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

64 Managerial Accounting, 16th Edition

Problem 10A-8 (continued)

The company’s overhead variances can be summarized as follows:

V

ariable overhead:

5. Only the volume variance would have changed. It would have been

unfavorable because the standard DLHs allowed for the year’s

—

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 10A 65

Problem 10A-9 (45 minutes)

1. $297,500

T

otal rate: = $8.50 per hour

35,000 hours

3. Variable overhead variances:

A

ctual Hours of

Input, at the

Actual Rate

A

ctual Hours of Input,

at the Standard Rate

Standard Hours

A

llowed for Output, at

the Standard Rate

(AH ×

A

R) (AH × SR) (SH × SR)

Alternative solution:

Variable overhead rate variance = (AH × AR) – (AH × SR)

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

66 Managerial Accounting, 16th Edition

Problem 10A-9 (continued)

Fixed overhead variances:

A

ctual Fixed

Overhead

Bud

g

eted Fixed

Overhead

Fixed Overhead Applied to

Work in Process

Alternative solution:

Budget variance:

Bud

g

et Actual fixed Bud

g

eted fixed

= –

variance overhead overhead

Volume variance:

Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

overhead rate allowed

æö

÷

ç÷

ç÷

ç÷

ç÷

÷

ç

èø

V

erification:

Variable overhead rate variance …….. $ 3,000 U

Variable overhead efficiency variance 5,000 F

g

v

v

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 10A 67

Problem 10A-9 (continued)

4. Variable overhead

Rate variance:

This variance includes both price and quantity elements.

The overhead spending variance reflects differences between actual and

standard prices for variable overhead items. It also reflects differences

Efficiency variance:

The term “variable overhead efficiency variance” is a

misnomer, because the variance does not measure efficiency in the use

of overhead items. It measures the indirect effect on variable overhead

of the efficiency or inefficiency with which the activity base is utilized. In

Fixed overhead

Budget variance:

This variance is simply the difference between the

budgeted fixed cost and the actual fixed cost. In this case, the variance

Volume variance:

This variance occurs as a result of actual activity being

different from the denominator activity in the predetermined overhead

rate. In this case, the variance is unfavorable, so actual activity was less

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

68 Managerial Accounting, 16th Edition

Problem 10A-10 (45 minutes)

1. Direct materials price and quantity variances:

Materials price variance = AQ (AP – SP)

2. Direct labor rate and efficiency variances:

Labor rate variance = AH (AR – SR)

3. a. Variable overhead spending and efficiency variances:

A

ctual Hours of

Input, at the

Actual Rate

A

ctual Hours of

Input, at the

Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH ×

A

R) (AH × SR) (SH × SR)

Variable overhead

r

ate

variance,

$750 F

Variable overhead

efficiency variance,

$3,750 U

Alternative solution:

Variable overhead rate variance = (AH × AR) – (AH × SR)

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 10A 69

Problem 10A-10 (continued)

b. Fixed overhead budget and volume variances:

A

ctual Fixed

Overhead

Bud

g

eted Fixed

Overhead

Fixed Overhead Applied to

Work in Process

Alternative solution:

Budget variance:

Bud

g

et Actual fixed Bud

g

eted fixed

= –

variance overhead overhead

Volume variance:

æö

÷

ç÷

ç÷

ç÷

ç÷

Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

g

v

v

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

70 Managerial Accounting, 16th Edition

Problem 10A-10 (continued)

4. The total of the variances would be:

Direct materials variances:

Direct labor variances:

V

ariable manufacturin

g

overhead variances:

Fixed manufacturin

g

overhead variances:

Bud

g

et variance ………………………………….. 1,800 U

T

Note that the total of the variances agrees with the $18,300 variance

mentioned by the president.

It appears that not everyone should be given a bonus for good cost

The company’s large unfavorable variances (for materials quantity and

labor efficiency) do not show up more clearly because they are offset by

the favorable volume variance. This favorable volume variance is a result

of the company operating at an activity level that is well above the

denominator activity level used to set predetermined overhead rates.