© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 10 11

The Foundational 15 (continued)

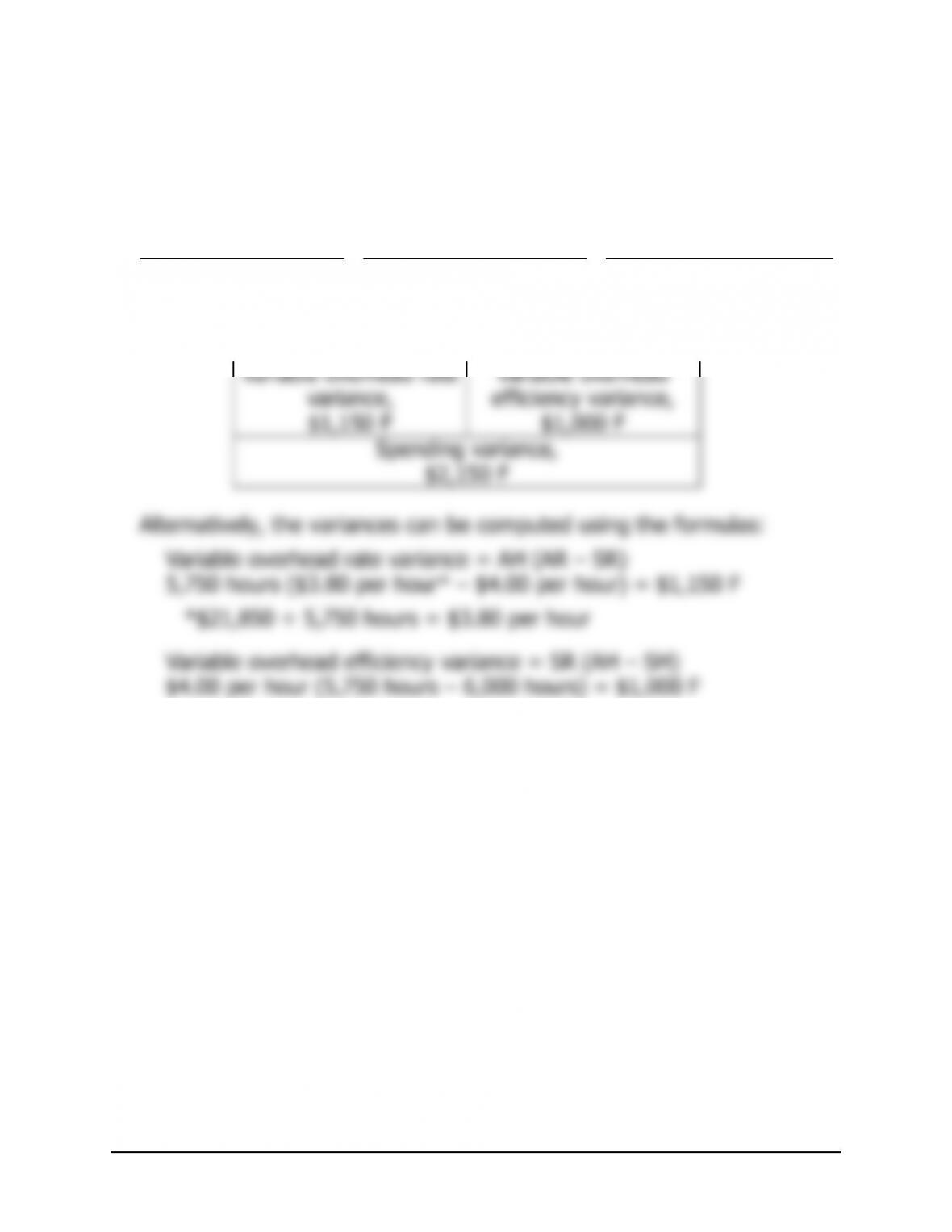

12. The variable manufacturing overhead cost included in the planning

13, 14, and 15.

The variable overhead cost included in the flexible budget (SH × SR =

$300,000), the variable overhead rate variance ($5,500 U), and the

variable overhead efficiency variance ($25,000 F) can be computed using

the general model for cost variances as follows:

Actual Hours of Input,

at Actual Rate

(AH × AR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Standard Hours

A

llowed

for Actual Output,

at Standard Rate

(SH × SR)

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance = AH (AR* – SR)

Variable overhead efficiency variance = SR (AH – SH)

Exercise 10-1 (20 minutes)

1. Number of helmets produced (a) ……………………. 35,000

Standard kilo

g

rams of plastic per helmet (b)……… 0.6

Standard quantity of kilo

g

rams allowed (a) × (b) .. 21,000

2. Standard quantity of kilo

g

rams allowed (a)……….. 21,000

Standard cost per kilo

g

ram (b) ………………………. $8

Standard cost allowed for actual output (a) × (b).. $168,000

3.

A

ctual cost incurred (

g

iven) (a) ……………………… $171,000

T

–

4.

A

ctual Quantity

of Input, at

Actual Price

Actual Quantity of Input,

at Standard Price

Standard Quantity

Allowed for Output, at

Standard Price

(AQ ×

A

P) (AQ × SP) (SQ × SP)

v

Exercise 10-2 (20 minutes)

1. Number of meals prepared (a)……………. 4,000

2. Standard labor-hours allowed (a) …….…. 1,000

3.

A

ctual cost incurred (a) …………………… $19,200

–

4.

A

ctual Hours of

Input, at the

Actual Rate

A

ctual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH×

A

R) (AH

×

SR) (SH×SR)

960 hours ×

960 hours ×

1,000 hours ×

v

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

14 Managerial Accounting, 16th Edition

Exercise 10-3 (20 minutes)

1. Number of items shipped (a) …………………………. 120,000

2. Standard quantity of labor-hours allowed (a) …….. 2,400

3.

A

ctual variable overhead cost incurred (a) ………… $7,360

V

–

4.

A

ctual Hours of

Input, at the

Actual Rate

A

ctual Hours of Input,

at the Standard Rate

Standard Hours

A

llowed for Output, at

the Standard Rate

(AH×

A

R) (AH

×

SR) (SH×SR)

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance:

Exercise 10-4 (30 minutes)

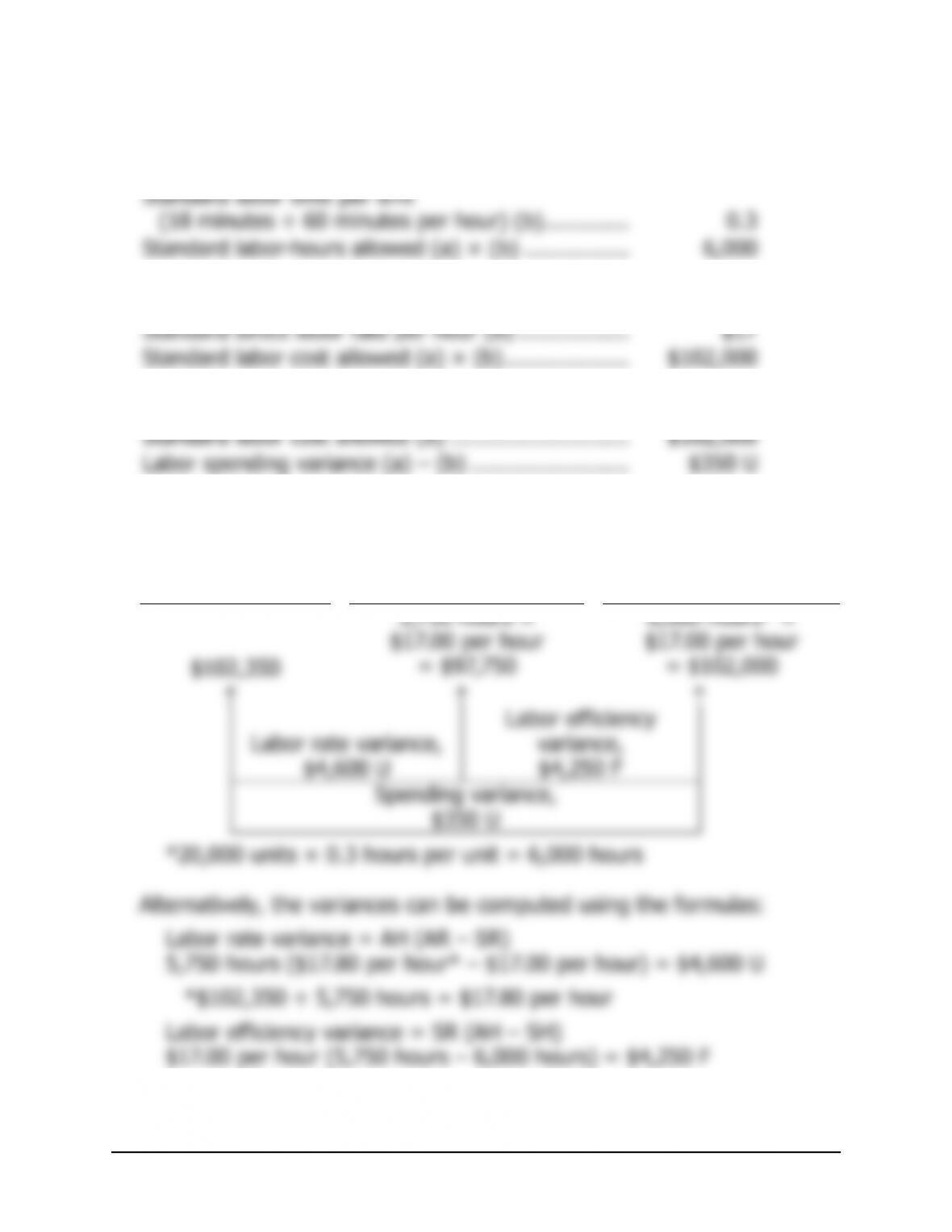

1. Number of units manufactured (a) ………………….. 20,000

2. Standard labor-hours allowed (a) 6,000

3.

A

ctual direct labor cost (a) ……………………………. $102,350

–

4.

A

ctual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours Allowed

for Output, at the

Standard Rate

(AH × AR) (AH × SR) (SH × SR)

v

Exercise 10-4 (continued)

5.

A

ctual Hours of

Input, at the

Actual Rate

A

ctual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR) (AH × SR) (SH × SR)

5,750 hours ×

$4.00 per hour

6,000 hours ×

$4.00 per hour

$21,850 = $23,000 = $24,000

v

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 10 17

Exercise 10-5 (20 minutes)

1. If the labor spending variance is $200 unfavorable, and the labor rate

variance is $150 favorable, then the labor efficiency variance must be

$350 unfavorable, because the labor rate and labor efficiency variances

taken together always equal the spending variance. Knowing that the

labor efficiency variance is $350 unfavorable, one approach to the

solution would be:

2. Labor rate variance = AH (AR – SR)

139 hours (AR – $25.00 per hour) = $150 F

139 hours × AR – $3,475 = –$150*

Exercise 10-5 (continued)

An alternative approach would be to work from known to unknown data

in the columnar model for variance analysis:

Actual Hours of Input,

at the Actual Rate

A

ctual Hours of Input,

at the Standard Rate

Standard Hours

A

llowed for Output, at

the Standard Rate

(AH × AR) (AH × SR) (SH × SR)

139 hours ×

139 hours ×

125 hours§×

v

Exercise 10-6 (20 minutes)

1.

A

ctual Quantity

of Input, at

Actual Price

A

ctual Quantity

of Input, at

Standard Price

Standard Quantity

A

llowed for Output,

at Standard Price

(AQ ×

A

P) (AQ × SP) (SQ × SP)

v

Exercise 10-6 (continued)

2.

A

ctual Hours of

Input, at the

Actual Rate

A

ctual Hours of Input,

at the Standard Rate

Standard Hours

A

llowed for Output, at

the Standard Rate

(AH ×

A

R) (AH × SR) (SH × SR)

750 hours ×

800 hours* ×

v