© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 1 21

Exercise 1-8 (continued)

3. Direct materials ………………………………….. $ 7.00

Direct labor ……………………………………….. 4.00

V

ariable manufacturin

g

overhead ……………. 1.50

V

ariable manufacturin

g

cost per unit ……….. $12.50

T

T

4. Sales commissions ………………………………. $1.00

V

ariable administrative expense ……………… 0.50

V

ariable sellin

g

and administrative per unit .. $1.50

V

g

T

T

T

V

g

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

22 Managerial Accounting, 16th edition

Exercise 1-9 (20 minutes)

1. Direct materials ……………………………….. $ 7.00

Direct labor …………………………………….. 4.00

V

ariable manufacturin

g

overhead …………. 1.50

V

2. Direct materials ………………………………..

$ 7.00

Direct labor …………………………………….. 4.00

V

ariable manufacturin

g

overhead …………. 1.50

V

V

3.

V

ariable cost per unit sold (a) ………………

$14.00

T

4.

V

ariable cost per unit sold (a) ………………

$14.00

T

Note: The key to answering questions 5 through 8 is to calculate the total

fixed manufacturing overhead costs as follows:

A

vera

g

e fixed manufacturin

g

overhead

T

Note: The average fixed manufacturing overhead cost per unit of $5.00 is

V

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 1 23

Exercise 1-9 (continued)

5. The average fixed manufacturing overhead per unit is:

T

otal fixed manufacturin

g

overhead (a)….. $100,000

A

6. The average fixed manufacturing overhead per unit is:

T

otal fixed manufacturin

g

overhead (a)….. $100,000

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

24 Managerial Accounting, 16th edition

Exercise 1-10 (10 minutes)

1. Direct materials ……………………………….. $ 7.00

Direct labor …………………………………….. 4.00

2. Direct materials ……………………………….. $ 7.00

Direct labor …………………………………….. 4.00

V

ariable manufacturin

g

overhead …………. 1.50

V

V

3. Because the 200 units to be sold to the new customer have already

been produced, the incremental manufacturing cost per unit is zero.

4. Sales commission ………………………………

$1.00

V

V

V

g

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 1 25

Exercise 1-11 (20 minutes)

1. The company’s variable cost per unit is:

$180,000 =$6 per unit.

30,000 units

The completed schedule is as follows:

Units produced and sold

30,000 40,000 50,000

T

otal costs:

T

T

2. The company’s contribution format income statement is:

Sales (45,000 units × $16 per unit)…………………… $720,000

V

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

26 Managerial Accounting, 16th edition

Exercise 1-12 (10 minutes)

1. The computations for parts 1a through 1e are as follows:

a. The cost of batteries in Raw Materials:

Be

g

innin

g

raw materials inventory…………. 0

Plus: Battery purchases ………………………. 8,000

Batteries available ……………………………… 8,000

b. The cost of batteries in Work in Process:

Be

g

innin

g

work in process inventory ……… 0

Plus: Batteries withdrawn for production…. 7,500

c. The cost of batteries in Finished Goods:

Be

g

innin

g

finished

g

oods inventory ……….. 0

Plus: Batteries transferred in from work in

process (see requirement b) ………….….. 6,750

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 1 27

Exercise 1-12 (continued)

d. The cost of batteries in Cost of Goods Sold:

Number of batteries (see requirement c)

e. The cost of batteries included in selling expense:

2. Raw Materials, Work in Process and Finished Goods would appear on

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

28 Managerial Accounting, 16th edition

Exercise 1-13 (30 minutes)

1. True. The variable manufacturing cost per unit will remain the same

2. False. The total fixed manufacturing cost will remain the same within

3. True. The total variable manufacturing cost will increase, so the total

4. True. The average fixed manufacturing cost per unit will decrease as

5. False. The total variable manufacturing cost will increase (rather than

6. False. The variable manufacturing cost per unit will remain the same,

7. True. The variable manufacturing cost per unit of $28 will stay

constant within the relevant range. The $28 figure is computed as

follows:

T

g

V

V

8. False. The total fixed manufacturing cost of $420,000 does not change

within the relevant range. The $420,000 figure is computed as follows:

T

otal manufacturin

g

cost per unit (a) …….. $70.00

V

A

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 1 29

Exercise 1-13 (continued)

9. True. The underlying computations are as follows:

V

ariable manufacturin

g

cost per unit (see

requirement 7) (a) …………………………...

$28.00

Number of units produced (b) …….………… 10,050

T

T

g

T

10. True. The underlying computations are as follows:

T

otal fixed manufacturin

g

cost (see requirement 8)

A

11. False. The total variable manufacturing cost will equal $281,400,

computed as follows:

V

ariable manufacturin

g

cost per unit (see

T

12. True. The underlying computations are as follows:

V

ariable manufacturin

g

cost per unit (see

A

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

30 Managerial Accounting, 16th edition

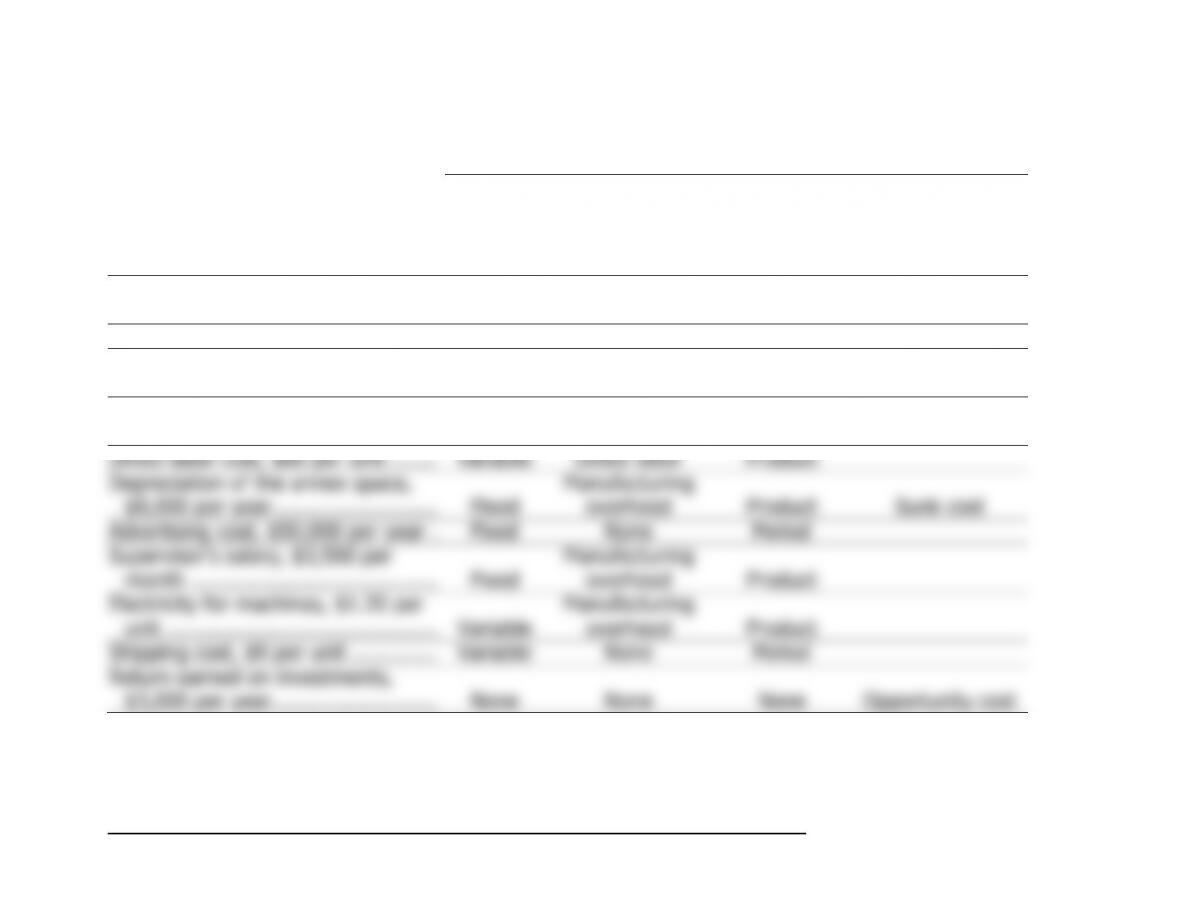

Exercise 1-14 (30 minutes)

Cost Classifications for:

Name of the Cost

(1)

Predictin

g

Cost

behavior

(2)

Manufacturers

(3)

Preparing

Financial

Statements

(4)

Decision

Making

Rental revenue for

g

one, $30,000

per year ………………………………. None None None Opportunity cost

Direct materials cost, $80 per unit .. Variable Direct materials Product

Rental cost of warehouse, $500

per month ……………………………. Fixed None Period

Rental cost of equipment, $4,000

per month ……………………………. Fixed

Manufacturin

g

overhead Product

g

g

g