Chapter 08 – The Efficient Market Hypothesis

CHAPTER EIGHT

THE EFFICIENT MARKET HYPOTHESIS

CHAPTER OVERVIEW

This chapter examines the concept of market efficiency. We are asking whether securities are,

on average, fairly priced according to the benefits they give an investor. If they are then one

cannot expect to consistently earn more than one should for the risk level you are taking. In other

words you cannot consistently beat the market’s risk-adjusted return. There are two aspects of

efficiency, although the text does not explicitly separate the two. In an informationally-efficient

market, price changes are unpredictable. It is this aspect of efficiency with which the text is

concerned. However we may also ask a related question, “Are the markets efficient allocators of

LEARNING OBJECTIVES

After studying this chapter, the student should thoroughly understand the concept of

informational market efficiency and how to make rational investment decisions based upon the

existence of market efficiency. The student also should have a working knowledge of some tests

of market efficiency, the forms of market efficiency, and observed market anomalies. Market

efficiency is akin to the perfect competition model to which it is related. Like perfect

competition, it should be interpreted as an ideal that markets move toward but will probably

never completely and consistently achieve. Nevertheless the financial markets are highly

competitive and it is likely that markets will closely approach efficiency, the occasional bubbles

notwithstanding. Bubbles remind us that math and models of cash flows, etc., do not drive

Chapter 08 – The Efficient Market Hypothesis

CHAPTER OUTLINE

1. Random Walks and the Efficient Market Hypothesis

PPT 8-2 through PPT 8-6

Definitions of informational and allocational efficiency are provided. Implications of efficiency

are then discussed and the idea of random walk is introduced and illustrated. Note that we

actually expect there to be a positive trend in stock prices albeit with random movements around

those positive trends. The reason that we would expect to see price changes that are random is

related to efficiency. If information that has importance for stock values arrives or occurs in a

random fashion, price changes will occur randomly. If the market is efficient in its analysis, the

change in prices will reflect that information in a timely basis.

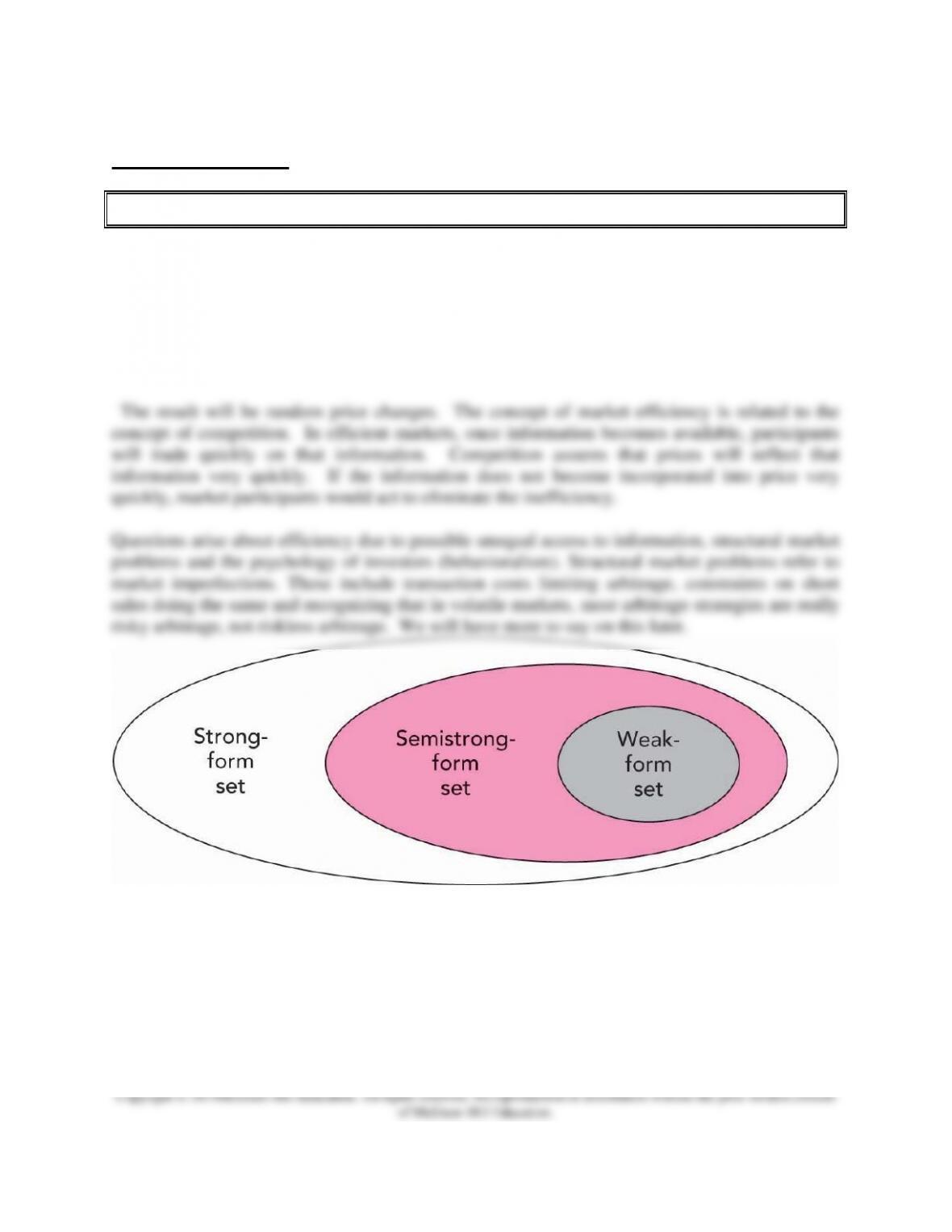

The forms of the efficient market are presented. In a weak-form efficient market, prices will

reflect all information that can be derived from trading data such as prices and volumes. In a

semi-strong form, market prices will reflect all publicly available information regarding the

firm’s prospects. In a strong-form market, prices would reflect all information relevant to the

firms’ prospects, even inside information. It is important that students understand the following

Venn diagram.

Many students struggle with this concept so it is worth taking the time to point out the

relationships among the different forms of efficiency.

Chapter 08 – The Efficient Market Hypothesis

2. Implications of the EMH (for Security Analysis)

PPT 8-7 through PPT 8-10

Technical and fundamental analyses are defined in this section as well as the implications of the

different forms of market efficiency with respect to security analysis. If markets are weak-form

efficient, technical analysis, such as charting, should not result in superior profits. If markets are

semi-strong form efficient, fundamental analysis should not result in consistent superior profits.

Fundamental analysis involves using information on the economy as well as information such as

earning trends and profit trends to find undervalued securities. If markets are at least semi-strong

efficient, investors would tend to employ passive strategies such as buying indexed funds or

employing a diversified buy-and-hold strategy. Active management such as security analysis or

attempting to time the market would not result in consistently superior profits if markets are

efficient.

3. Are Markets Efficient?

PPT 8-11 through PPT 8-22

Over time stock prices tend to follow a submartingale. This has nothing to do with efficiency,

per se. It does however have serious implications for tests of efficiency. This implies that a

randomly chosen portfolio of stocks can be expected to have a positive return. In practice this

means that when trying to figure out if some portfolio manager is earning abnormal returns we

must compare their performance to the performance of a randomly chosen portfolio. That is,

they must outperform the random portfolio or, in practice, they must beat some benchmark rate

of return. The magnitude, selection bias and lucky-event issues are covered, as well as possible

model misspecification. Because a model of expected return is needed to assess whether an

investor or an investment rule earns excess return, tests of market efficiency are joint tests of the

model used to estimate expected returns and market efficiency. Therefore, even when an

anomaly is discovered, we have to be careful in interpreting the results. Some apparent

anomalies are discussed including the Fama-French results, the Keim and Stambaugh findings

and the Campbell and Shiller work. Note that each of these results may also be consistent with

changing risk premiums and may have nothing to say about market efficiency. Some anomalies

do not have staying power after being reported.

Chapter 08 – The Efficient Market Hypothesis

Periodically, stock prices appear to undergo a ‘speculative bubble.’ A speculative bubble is said

to occur if prices do not equal the intrinsic value of the security. Does this imply that markets

are not efficient? There is no definitive answer to this question. However we can make some

observations:

• It is very difficult to predict if you are in a bubble and when the bubble will burst. Stock

prices are estimates of future economic performance of the firm and these estimates can

change rapidly.

• Risk premiums can change rapidly and dramatically.

Nevertheless, with hindsight there appear to be times when stock prices decouple from intrinsic

or fundamental value, sometimes for years. What does this imply?

• Prices eventually conform once more to intrinsic value. Many who don’t believe in

efficient markets anyway have jumped on this result to pronounce the death of market

efficiency. However, the bubbles bring into question the allocational efficiency of the

markets more than the informational efficiency. Very few people will be able to

consistently predict the extent and duration of a bubble.

• Some claim the bubbles imply that investors are irrational. Perhaps, but think about what

determines the price of gold. Is it irrational to buy an asset for more than its fundamental

value if you believe that you can sell it for more than you paid for it? It is indeed risky to

engage in this type of transaction, but is it irrational?

Chapter 08 – The Efficient Market Hypothesis

Copyright © 2019McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Some of the major types of tests that researchers have done on market efficiency are described. If

markets are inefficient, then professionals who spend considerable resources in investment

should secure superior performance. The tests are broken down in terms tests of the forms of

efficiency. Tests have uncovered some inefficiency in pricing but many possible interpretations

of results are possible. Tests of weak-form efficiency show small magnitudes of positive

correlation for very short term tests; hence prices do not strictly conform to a random walk.

Studies of returns for periods of 3 to 12 months offer evidence of positive momentum. Longer

horizon tests have uncovered some pronounced negative correlation. Tests do document

tendencies for long term reversals in results. This may be because of information flow in

competitive markets. People rush to buy recent winners and in so doing drive up the price

enough so that future returns are not abnormal. This does not imply inefficiency unless the same

investors can consistently do this. Attempting to interpret the results of efficiency tests has led to

various explanations ranging from model misspecification to data mining.

4. Mutual Fund and Analyst Performance

PPT 8-23 through PPT 8-30

Some recent studies on mutual funds have documented some persistence in positive and negative

performance. Some researchers question whether the performance is abnormal or whether the

studies have measurement errors or model biases. The overall test results are mixed at best but

the evidence shows that some superstars exist. Note that Warren Buffet’s portfolio, (Buffet is

one of the postulated superstars) took quite a beating in the financial crisis of 2008. Although

the evidence is not conclusive, it appears safe to state that the ability to consistently earn

abnormal returns, greater than one should for the risk level undertaken, is very rare.

Chapter 08 – The Efficient Market Hypothesis

Chapter 08 – The Efficient Market Hypothesis