Chapter 06 – Efficient Diversification

CHAPTER 06

EFFICIENT DIVERSIFICATION

1. So long as the correlation coefficient is below 1.0, the portfolio will benefit from

3. a and b will have the same impact of increasing the Sharpe ratio from .40 to .45.

4. The expected return of the portfolio will be impacted if the asset allocation is changed.

5. Total variance = Systematic variance + Residual variance = β2 Var(rM) + Var(e)

When β = 1.5 and σ(e) = .3, variance = 1.52 × .22 + .32 = .18. In the other scenarios:

sMs(e) b

TOTAL

Variance

Corr Coeff

0.2 0.3 1.65 0.1989 0.7399

0.2 0.33 1.5 0.1989 0.6727

a. Both will have the same impact. Total variance will increase from .18 to .1989.

Thus, there appears to be a higher variance, yet the mean is probably the same

since the spread is equally large on both the high and low side. The mean return,

however, should be higher since there is higher probability given to the higher

returns.

Chapter 06 – Efficient Diversification

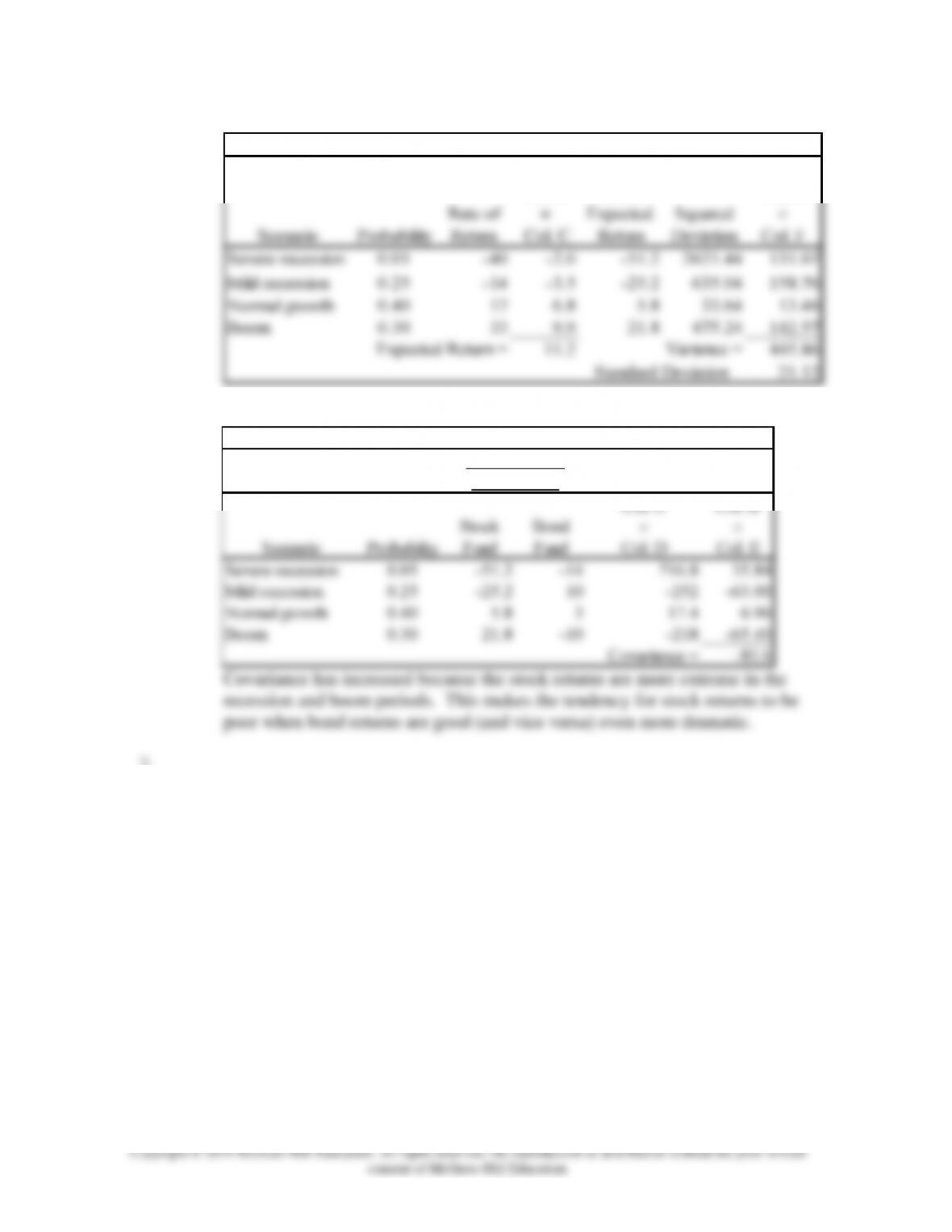

b. Calculation of mean return and variance for the stock fund:

(A) (B) (C) (D) (E) (F) (G)

Col. B

Col. B

×

Col. C

Col. F

Severe recession 0.05 –40 –2.0 –51.2 2621.44 131.07

Mild recession 0.25 –14 –3.5 –25.2 635.04 158.76

Normal growth 0.40 17 6.8 5.8 33.64 13.46

Boom 0.30 33 9.9 21.8 475.24 142.57

11.2 445.86

21.12

Scenario

Deviation

from

Expected

Return

Squared

Deviation

Expected Return =

Variance =

Standard Deviation =

Rate of

Return

Probability

c. Calculation of covariance:

(A) (B) (C) (D) (E) (F)

Col. C Col. B

Stock Bond

Fund Fund Col. D Col. E

Severe recession 0.05 –51.2 –14 716.8 35.84

Mild recession 0.25 –25.2 10 –252 –63.00

Normal growth 0.40 5.8 3 17.4 6.96

Boom 0.30 21.8 –10 –218 –65.40

Covariance = –85.6

Deviation from

Mean Return

Scenario

Probability

Covariance has increased because the stock returns are more extreme in the

recession and boom periods. This makes the tendency for stock returns to be

poor when bond returns are good (and vice versa) even more dramatic.

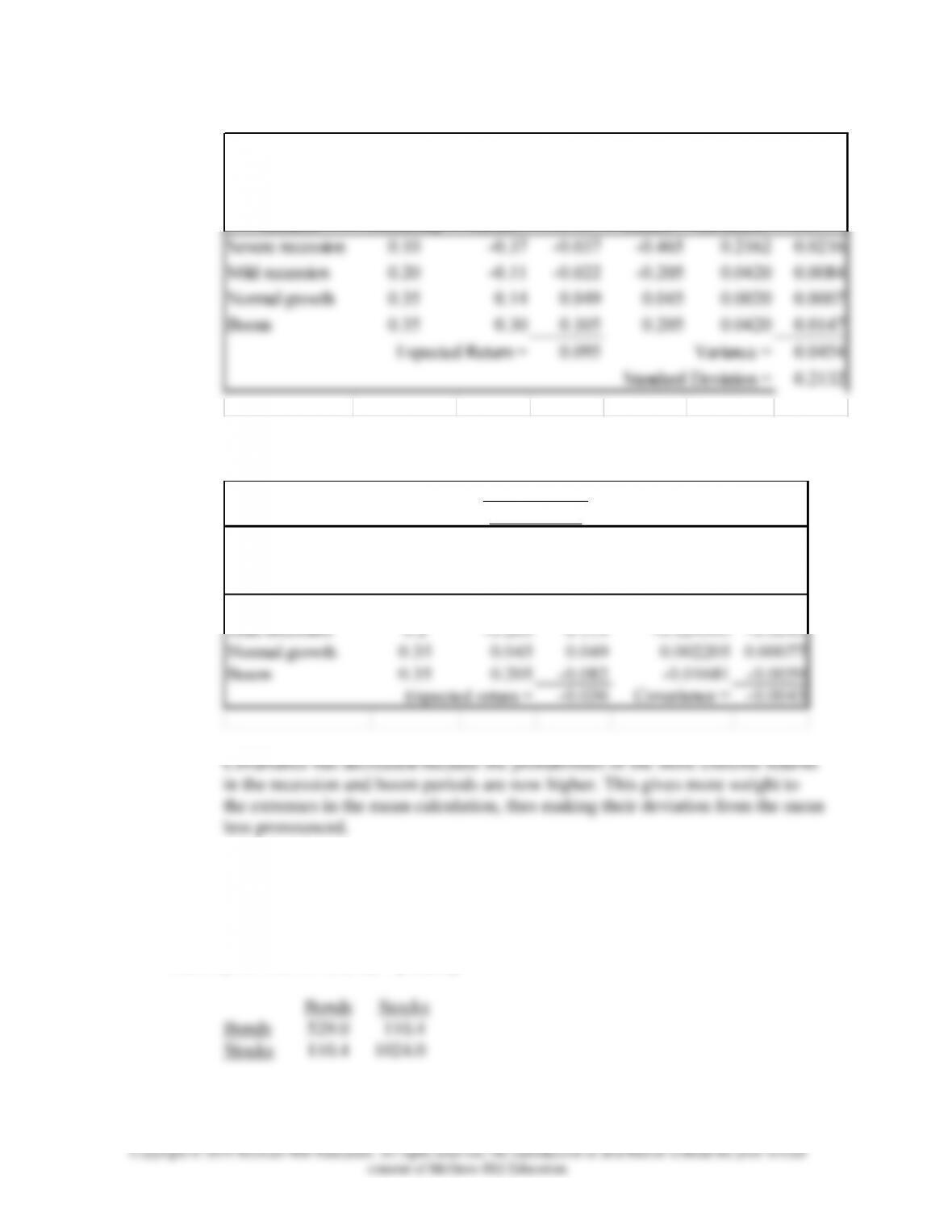

7. a. One would expect variance to increase because the probabilities of the extreme

outcomes are now higher.

Chapter 06 – Efficient Diversification

b. Calculation of mean return and variance for the stock fund:

Col. B Col. B

Col. C Col. F

Severe recession 0.10 –0.37 –0.037 –0.465 0.2162 0.0216

Mild recession 0.20 –0.11 –0.022 –0.205 0.0420 0.0084

Normal growth 0.35 0.14 0.049 0.045 0.0020 0.0007

Boom 0.35 0.30 0.105 0.205 0.0420 0.0147

0.095 0.0454

0.2132

Expected Return =

Variance =

Standard Deviation =

Scenario

Probability

Stock

Rate of

Return

Deviation

from

Expected

Return

Squared

Deviation

c. Calculation of covariance

Col. C Col. B

Stock Bond

Fund Fund Col. D Col. E

Severe recession 0.1 –0.465 –0.122 0.05673 0.00567

Mild recession 0.2 –0.205 0.119 –0.024395 –0.0049

Normal growth 0.35 0.045 0.049 0.002205 0.00077

Boom 0.35 0.205 –0.082 –0.01681 –0.0059

–0.036 Covariance = –0.0043

Deviation from

Mean Return

Scenario

Probability

Expected return =

8. The parameters of the opportunity set are:

E(rS) = 15%, E(rB) = 9%, S = 32%, B = 23%, = 0.15, rf = 5.5%

From the standard deviations and the correlation coefficient we generate the covariance

matrix [note that Cov(rS, rB) = SB]:

The minimum-variance portfolio proportions are:

Chapter 06 – Efficient Diversification

wMin(S) = B2 - Cov(rS, rB)

S2 + B2 - 2Cov(rS, rB) = 529 - 110.4

1,024 + 529 - (2 ×110.4) = .3142

wMin(B) = 1 – .3142 = .6858

The mean and standard deviation of the minimum variance portfolio are:

E(rMin) = ( .3142 15%) + ( .6858 9%) = 10.89%

Min = [wS

2S

2 + wB

2B

2 + 2 wS wB Cov(rS, rB)]1/2

= [( .31422 1024) + ( .68582 529) + (2 .3142 .6858 110.4)]1/2

= 19.94%

% in stocks % in bonds Exp. Return Std dev.

Sharpe Ratio

0.00 1.00 0.09 0.23 0.15

0.20 0.80 0.10 0.20 0.23

0.3142 0.6858 0.1089 0.1994 0.2701 Minimum Variance Portfolio

0.40 0.60 0.11 0.20 0.29

0.60 0.40 0.13 0.23 0.3155

0.6466 0.3534 0.1288 0.233382 0.3162 Tangency Portfolio

0.80 0.20 0.14 0.27 0.31

1.00 0.00 0.15 0.32 0.30

0

5

10

15

20

010 20 30 40

Expected Return (%)

Standard Deviation (%)

Investment Opportunity Set

Chapter 06 – Efficient Diversification

The graph approximates the points:

E(r)

Minimum variance portfolio

10.89%

19.94%

Tangency portfolio

12.88%

23.3382%

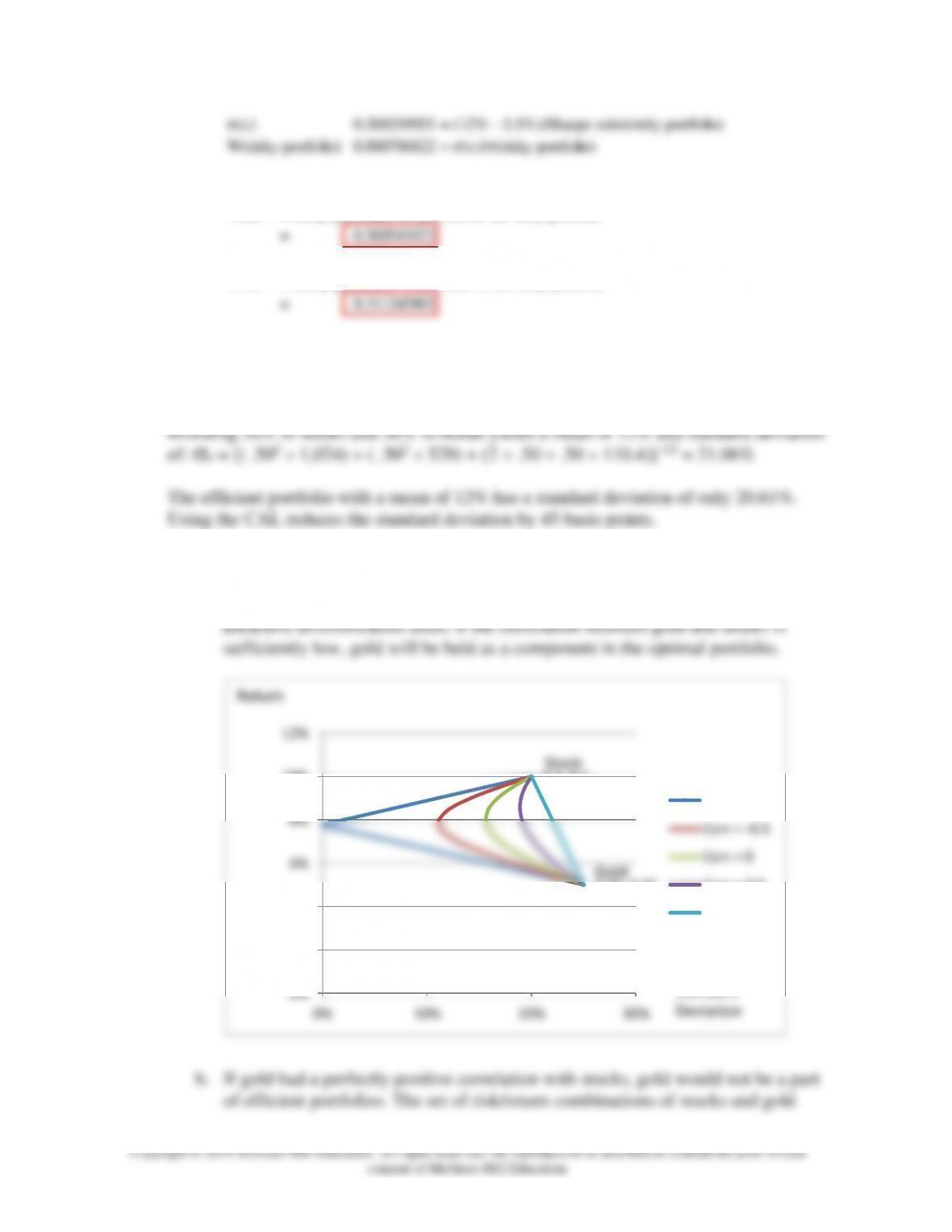

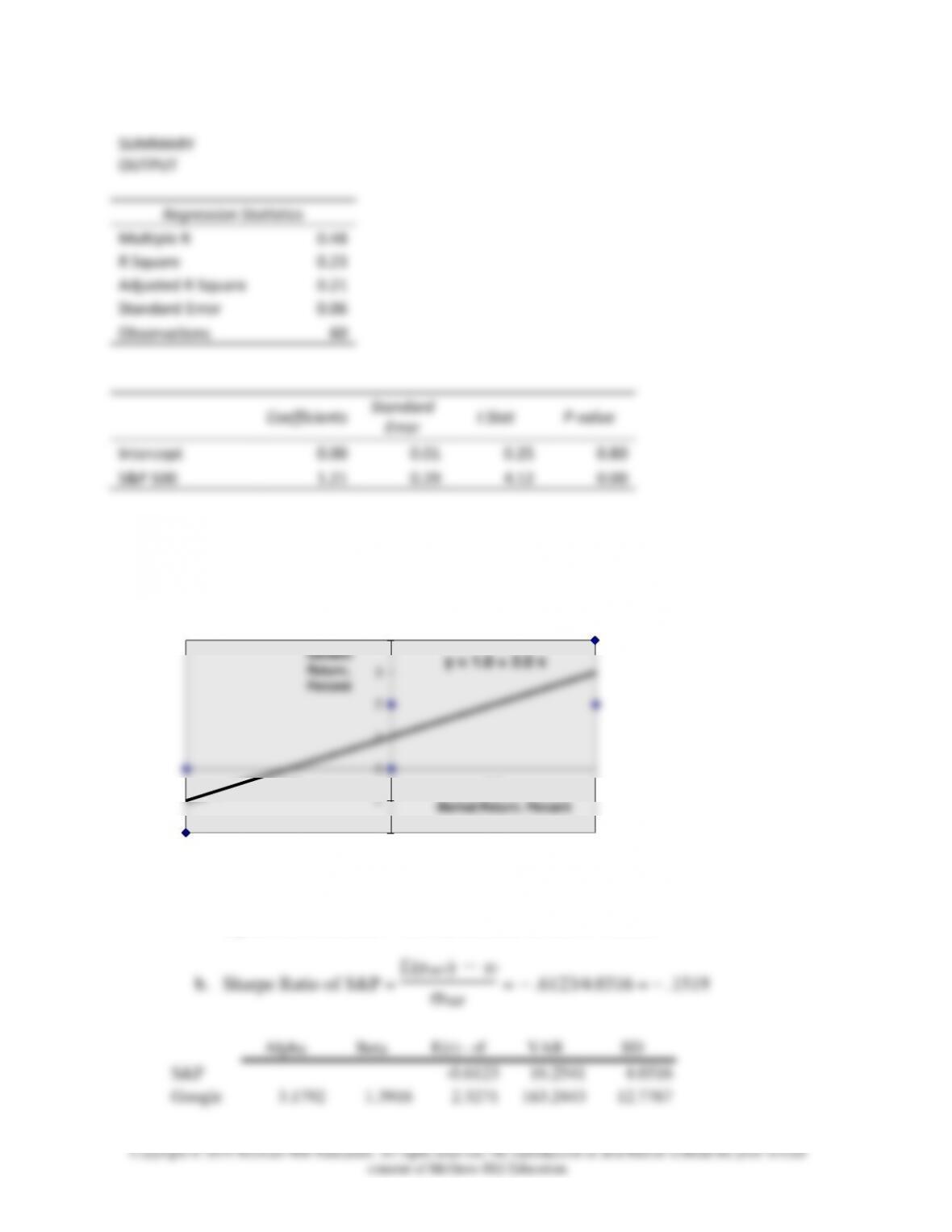

10. The Sharpe ratio of the optimal CAL is:

P

23.34 = .3162

11.

a. The equation for the CAL is:

E(rC) = rf + E(rP) - rf

P

C = 5.5 + .3162C

complete portfolio:

0

2

4

6

8

10

12

14

16

18

20

010 20 30 40

Expected Return (%)

Standard Deviation (%)

Investment Opportunity Set

Chapter 06 – Efficient Diversification

(c) 0.205559955 = (12% – 5.5%)/Sharpe ratio(risky portfolio)

W(risky portfolio) 0.880786822

= (c)/(risky portfolio)

Proportion of stocks in complete portfolio

W(s) = W(risky portfolio)*% in stock of the risky portfolio

= 0.569541021

Proportion of bonds in complete portfolio

W(b) = W(risky portfolio)*% in bonds of the risky portfolio

= 0.311245801

12. Using only the stock and bond funds to achieve a mean of 12%, we solve:

12 = 15wS + 9(1 −wS ) = 9 + 6wS wS = .5

13.

a. Although it appears that gold is dominated by stocks, gold can still be an

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

14. Since Stock A and Stock B are perfectly negatively correlated, a risk-free portfolio can

be created and the rate of return for this portfolio in equilibrium will always be the risk-

free rate. To find the proportions of this portfolio [with wA invested in Stock A and wB

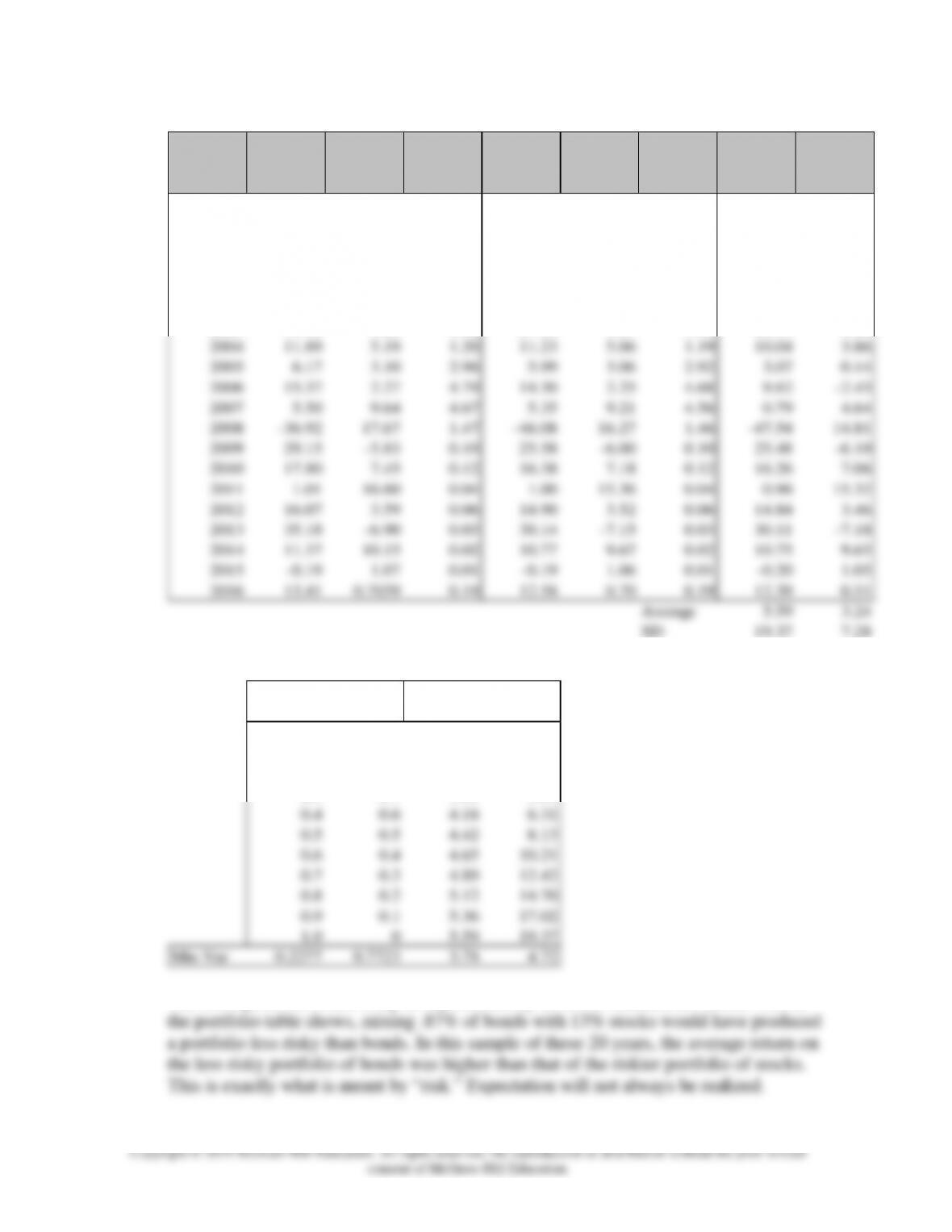

15. Since these are annual rates and the risk-free rate was quite variable during the sample

period of the recent 20 years, the analysis has to be conducted with continuously

Chapter 06 – Efficient Diversification

Annual returns from Table 2 Continuously compounded rates Excess returns

Year

Large

Stock

Long-

Term T-

Bonds

T-Bills

Large

Stock

Long-

Term T-

Bonds

T-Bills

Large

Stock

Long-

Term T-

Bonds

1997 31.33 11.31 5.26 27.25 10.72 5.13 22.13 5.59

1998 24.27 13.09 4.86 21.73 12.30 4.75 16.98 7.56

1999 24.89 –8.47 4.68 22.23 –8.85 4.57 17.65 –13.43

2000 –10.82 14.49 5.89 –11.45 13.53 5.72 –17.17 7.81

2001 –11.00 4.03 3.78 –11.65 3.95 3.71 –15.36 0.24

2002 –21.28 14.66 1.63 –23.93 13.68 1.62 –25.54 12.07

2003 31.76 1.28 1.02 27.58 1.27 1.01 26.57 0.25

2004 11.89 5.19 1.20 11.23 5.06 1.19 10.04 3.86

2005 6.17 3.10 2.96 5.99 3.06 2.92 3.07 0.14

2006 15.37 2.27 4.79 14.30 2.25 4.68 9.62 –2.43

2007 5.50 9.64 4.67 5.35 9.21 4.56 0.79 4.64

2008 –36.92 17.67 1.47 –46.08 16.27 1.46 –47.54 14.81

2009 29.15 –5.83 0.10 25.58 –6.00 0.10 25.48 –6.10

2010 17.80 7.45 0.12 16.38 7.18 0.12 16.26 7.06

2011 1.01 16.60 0.04 1.00 15.36 0.04 0.96 15.32

2012 16.07 3.59 0.06 14.90 3.52 0.06 14.84 3.46

2013 35.18 –6.90 0.03 30.14 –7.15 0.03 30.11 –7.18

2014 11.37 10.15 0.02 10.77 9.67 0.02 10.75 9.65

2015 –0.19 1.07 0.01 –0.19 1.06 0.01 –0.20 1.05

2016 13.41 0.7039 0.19 12.58 0.70 0.19 12.39 0.51

0.9 0.1 5.36 17.02

1.0 05.59 19.37

Min–Var 0.2277 0.7723 3.78 4.72

The bond portfolio is less risky as represented by its lower standard deviation. Yet, as

16. If the lending and borrowing rates are equal and there are no other constraints on

portfolio choice, then the optimal risky portfolios of all investors will be identical.

were 1.0, the frontier would be a straight line connecting A and B.

18. In the special case that all assets are perfectly positively correlated, the portfolio

standard deviation is equal to the weighted average of the component-asset standard

Probability

Rate of Return

.7

100%

.3

-50%

Expected return = ( .7 1) + .3 (− .5) = 0.55 or 55%

Variance = [ .7 (1 − 0.55)2] + [ .3 (−50 − 0.55)2] = 0.4725

Standard Deviation =√0.4725 = 0.6874 or 68.74%

20. The expected rate of return on the stock will change by beta times the unanticipated

change in the market return: 1.2 ( .08 – .10) = –2.4%

Therefore, the expected rate of return on the stock should be revised to:

21.

a. The risk of the diversified portfolio consists primarily of systematic risk. Beta

measures systematic risk, which is the slope of the security characteristic line (SCL).

22. Using “Regression” command from Excel’s Data Analysis menu, we can run a

regression of Apple’s excess returns against those of S&P 500, and obtain the following

data. The Beta of Apple is 1.21.

Chapter 06 – Efficient Diversification

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.48

R Square

0.23

Adjusted R Square

0.21

Standard Error

0.06

Observations

60

Coefficients

Standard

Error

t Stat

P-value

Intercept

0.00

0.01

0.25

0.80

S&P 500

1.21

0.29

4.12

0.00

23. A scatter plot results in the following diagram. The slope of the regression line is 2.0

and intercept is 1.0.

y = 1.0 + 2.0 x

-2

-1

0

1

2

3

4

-1 -0.5 0 0.5 1

Market Return, Percent

Generic

Return,

Percent

24. a. Regression output produces the following:

alpha = 3.1792, beta = 1.3916, Residual St Dev = 11.5932

Chapter 06 – Efficient Diversification

c. Information Ratio = αG/(eG) = 3.1792/11.5932 = .2742

O

O = αG /2(eG)

SUMMARY OUTPUT: Regression of Google on S&P 500 (excess returns)

Regression Statistics

Multiple R 0.4391

R Square 0.1928

Adjusted R Square 0.1767

Standard Error 11.5932

Observations 52.0000

Coefficients

Standard

Error

t Stat P-value

Intercept 3.1792 1.6265 1.9546 0.0562

S&P 500 1.3916 0.4027 3.4560 0.0011

Google Spy

Google 1.00

S&P 500 0.44 1.00

25.

a.

Outcome A:

No Fire

Outcome B:

Fire!

Payout

$110

$

(99,890)

b.

Expected

Return

Variance

Standard

Deviation

$10.00

9990000

3161

c.

Outcome:

No Fire

Outcome:

One Fire

Outcome:

Two Fires

Paytout

$

220

$

(99,780)

$

(199,780)

Probability

99.8001%

0.1998%

0.0001%

d.

Expected

Return

Variance

Standard

Deviation

$20.00

11466315

3386

e. Risk pooling increased the total variance of profit.

f.

Outcome:

No Fire

Outcome:

One Fire

Outcome:

Two Fires

Payout

$

110

$

(49,890)

$

(99,890)

Probability

99.8001%

0.1998%

0.0001%

g.

Expected

Return

Variance

Standard

Deviation

$10.00

2866579

1693

h. Risk has dropped significantly while the expected

profit is the same as (b). This demonstrates the power

of Risk Sharing as a necessary complement to Risk

Pooling. (g) is a superior outcome to (b) [Same

Expected Reward, Lower Risk]

i. Risk Pooling builds both expected payout and

variance. Risk Sharing implies profit sharing so expected

payout is halved, but so has standard deviation

Chapter 06 – Efficient Diversification

CFA 1

Answer:

CFA 2 Answer:

Fund D represents the single best addition to complement Stephenson’s current

portfolio, given his selection criteria. First, Fund D’s expected return (14.0 percent) has

the potential to increase the portfolio’s return somewhat. Second, Fund D’s relatively

CFA 3

Answer:

a. Subscript OP refers to the original portfolio, ABC to the new stock, and NP

to the new portfolio.

i. E(rNP) = wOP E(rOP ) + wABC E(rABC ) = ( .9 .67) + ( .1 1.25) = .7280%

b. Subscript OP refers to the original portfolio, GS to government securities, and

NP to the new portfolio.

Chapter 06 – Efficient Diversification

ii. CovOP , GS = CorrOP , GS OP GS = 0 2.37 0 = 0

c. Adding the risk-free government securities would result in a lower beta for the

new portfolio. The new portfolio beta will be a weighted average of the individual

security betas in the portfolio; the presence of the risk-free securities would lower

that weighted average.

d. The comment is not correct. Although the respective standard deviations and

expected returns for the two securities under consideration are identical, the

correlation coefficients between each security and the original portfolio are

CFA 4 Answer:

a. Restricting the portfolio to 20 stocks, rather than 40 to 50, will very likely

increase the risk of the portfolio, due to the reduction in diversification. Such an

increase might be acceptable if the expected return is increased sufficiently.

CFA 5

Answer:

Chapter 06 – Efficient Diversification

Risk reduction benefits from diversification are not a linear function of the number of

CFA 6

Answer:

The point is well taken because the committee should be concerned with the volatility

CFA 7

Answer:

a. Systematic risk refers to fluctuations in asset prices caused by macroeconomic

factors that are common to all risky assets; hence systematic risk is often

referred to as market risk. Examples of systematic risk factors include the

business cycle, inflation, monetary policy, and technological changes.

Chapter 06 – Efficient Diversification

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

securities increases, the total risk (variance) of the portfolio approaches its

systematic variance.