Chapter 21 – Taxes, Inflation, and Investment Strategy

CHAPTER TWENTY ONE

TAXES, INFLATION, AND INVESTMENT STRATEGY

CHAPTER OVERVIEW

This chapter presents material on developing a framework for retirement planning. The chapter

is built around a set of Excel models that can be used to plan for retirement. The first model

ignores inflation and taxes and subsequent models add the effects of inflation, a flat tax rate and

a progressive tax rate. This method allows students to see the effects on the retirement portfolio

of each one of these variables. Tax sheltered investments such as a traditional and a Roth IRA

are discussed. Defined benefit and defined contribution plans are also presented. Details about

Social Security taxes and benefits are provided. The chapter concludes with some other planning

considerations such as funding a child’s college education, the rent versus buy decision and life

annuities.

LEARNING OBJECTIVES

After studying this chapter the student should have an understanding of the basic elements

required to build a financial plan and how taxes and inflation will affect retirement income.

Students should be able to describe the basic types of tax sheltered retirement accounts and how

taxes will affect the performance of a traditional IRA and a Roth IRA. Students should be able to

understand the basics of Social Security payments although this remains a somewhat opaque

procedure.

CHAPTER OUTLINE

**Topics 1 through 6 of this chapter are written around a series of spreadsheets so the

Instructor’s Manual follows the same format. I have labeled each spreadsheet and

discussed the inputs and outputs beneath the appropriate spreadsheet.

1. Saving for the Long Run

PPT 21-2 through PPT 21-3

The development of the basic retirement plan involves identification of the time until retirement,

the allocation of the percentage allocation to saving, the life expectancy following retirement and

the expected rate of return. These key factors become the base of the plan. The first step in the

process involves specifying investment objectives. A planner will normally help their clients’

budget and even suggest changes in lifestyle to help them meet their goals. Often the planner

may have to tell the client that their goals aren’t realistic or encourage the clients to add other

priorities such as purchasing sufficient life and disability insurance and building sufficient

emergency savings.

Chapter 21 – Taxes, Inflation, and Investment Strategy

Spreadsheet 21.1: The Savings Plan

Specific Inputs: Retirement years = 25, income growth rate =7% (which is way too high for

many people); income at age 30 = $50,000, the rate of savings (% of income) which is very high

at 15%, and the rate or return on investment (ror) which is low at 6% for a retirement portfolio.

2. Accounting for Inflation

PPT 21-4 through PPT 21-9

Inflation reduces the purchasing power of the savings accumulation. Real and nominal

consumption can be related as follows: Real consumption = Nominal consumption / Price

Deflator. A simple example can be used to illustrate the point. Suppose inflation = 3% per year

and the nominal rate of return is 6%. What is the real rate of return?

Inflation turns the 6% nominal return into a 2.91% real return. This is before taxes are

considered. Since taxes are paid out of nominal earnings, the combine effect of inflation and

taxes results in even greater reductions than may be expected in real after tax rates of return.

return nominalROR

)iROR(

=

−

Chapter 21 – Taxes, Inflation, and Investment Strategy

The investor in the example is 30 years old. The size of the price deflator with 3% inflation at

age 35:

At age 65 =

Both of these numbers are in the spreadsheet. These deflators are used to convert the nominal

purchasing power in year t to starting date (age 30) dollars.

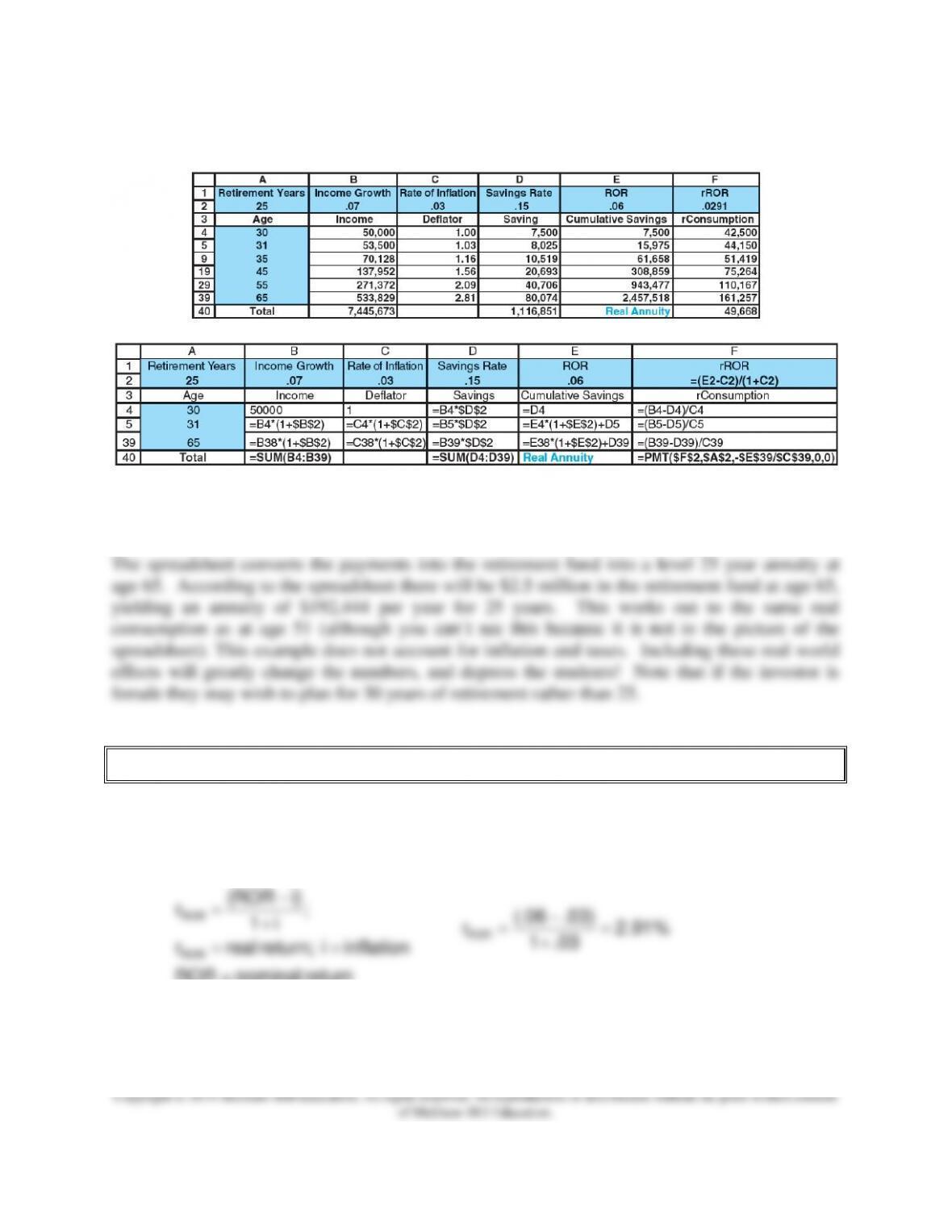

Spreadsheet 21.2 A Real Retirement Plan

The inputs are the same as before with inflation of 3% added. rConsumption is real consumption.

Thus the $192,244 nominal annuity buys only $49,668 in real purchasing power (the same

purchasing power as age 30). This will give the investor the same spending power as they had at

age 34. Notice the $2.5 million value of the retirement fund is worth only $873,631 in today’s

(age 30) purchasing power. Inflation continues after the investor retires. This indicates that the

investor’s standard of living will decline each year if they draw down a fixed retirement annuity.

16.103.1)i1( 5n ==+

81.203.1 35 =

Chapter 21 – Taxes, Inflation, and Investment Strategy

Should an investor take on more risk to offset inflation? What are the effects of increasing the

riskiness of the retirement portfolio? Increasing the risk increases the expected return, but also

the probability of not having enough to live on when the investor retires. As one gets older,

increasing the risk to make up for years in which one did not save is really rolling the dice. Nor

is it is not easy to reduce the risk level as you retire. It is particularly difficult if one has some

bad years of earnings. Does one want to sell at the market bottom to realign one’s portfolio?

There are some mutual funds, target date funds, that do this for an investor automatically but

they have recently come under criticism for large fees and poor performance.

Real returns based on historical averages

Investment

Average Real

Return

Stocks

9%

Government bonds

2.6%

Treasury bills

0.7%

Because we have had a long period of low inflation people forget how regressive the effects of

inflation really are. It erodes investment returns and drives up the cost of necessities which

reduces the standard of living of low income individuals, the group that can least afford it.

3. Accounting for Taxes

PPT 21-10 through PPT 21-11

Chapter 21 – Taxes, Inflation, and Investment Strategy

Taxes are a cash outflow from the funds that are available to meet the retirement needs. To

achieve the same retirement benefit, a larger percentage allocation to savings or higher rates of

return on investment is required. Inflation combined with taxes has a compounding impact

because higher inflation leads to higher taxes. The impact is larger with a progressive tax

structure.

Spreadsheet 21.4, Saving With a Simple Tax Code

The effects of inflation and taxes together really have major impacts on the ability to meet

investment goals. In this case the real retirement annuity is $37,882 with very modest inflation

of 3%, saving a lot of their income, 15% and a tax rate of 25%. Note that the tax rate should

(roughly) be the sum of federal, state and local income taxes.

At this point one must recognize that one will probably have to take some risk in a portfolio to

generate a large enough expected return. SEC studies have shown that most people under invest

in equities but stocks are probably their best bet (among liquid assets) at earning sufficiently high

rates of return to generate a reasonable retirement income.

Investors pay income taxes and pay taxes on unsheltered savings. One can use the numbers in

Spreadsheet 21.4 to illustrate the effect on the overall tax rate:

Income

(1) Lifetime labor income

$7,445,673

Total exemptions during working years

$949,139

(2) Lifetime Taxable labor income

6,496,534

Taxes

During labor years

1,884,163

During retirement

203,199

(3) Lifetime taxes

2,087,362

Lifetime average tax rate = (3) / (1)

28%

Lifetime tax rate on taxable income = (3)/ (2)

32%

As a result the average tax rate is elevated above the marginal tax rate of 25%.

4. The Economics of Tax Shelters

PPT 21-12 through PPT 21-15

Chapter 21 – Taxes, Inflation, and Investment Strategy

Tax shelters are means of postponing taxes as long as possible. One can’t get rid of taxes, one

can only postpone them. The discussion on tax shelters contains general discussion of the

benefits of using shelters as well as descriptions the major tax shelter accounts that are generally

available. Performance of some shelters such as a traditional IRA depends in part on variability

in tax rates and differences in tax rates during the accumulation phase as well the retirement

phase.

Spreadsheet 21.5 Savings with a Flat Tax and IRA Style Tax Shelter

This spreadsheet redoes sheet 21.4 with the tax shelter. It still uses a flat tax rate. All funds in

the retirement account are subject to taxation. Total lifetime taxes increases from $2.1 million to

$2.5 million. This increase occurs because one earns more on their investments without the tax

drain so the investor pay more taxes ($3.7 million versus $1.9 million before). The real annuity

is increased from $37,882 to $76,052. There is a large value to the shelter. Taxes on income

during the working years reduce the future value of the investments dramatically.

Spreadsheet 21.7, IRA with a Progressive Tax Code

The real annuity is increased considerably in this case; it is now up to $83,380. This is better than

with a flat tax rate for the reasons noted above.

5. A Menu of Tax Shelters

PPT 21-16 through PPT 21-23

Individual Retirement Accounts (IRAs) were created by the Tax Reform Act of 1986. Current

rules allow investors to contribute up to $5,000 per year to a retirement account. Individuals age

50 and older may contribute another $1,000 per year. There is a 10% tax penalty for withdrawal

of funds prior to age 59 ½ and the investor must begin withdrawals by age 70 ½. Any

withdrawals before age 59 ½ are subject to the ordinary income tax rate and a 10% tax penalty.

There are various hardship exclusions to the tax penalty however, including one for first time

homebuyers. Actually withdrawing the money for this reason would be a bad idea however

because one would lose the compound value of the money withdrawn (unless the house grows in

value at the same rate or more).

Chapter 21 – Taxes, Inflation, and Investment Strategy

There are two types of IRAs. With traditional IRAs contributions are tax deductible and the

earnings are tax deferred until withdrawn. With a Roth IRA contributions are not tax deductible

but earnings on the account are not taxed when withdrawn.

Spreadsheet 21.8 Roth IRA with Progressive Tax Code

The effectiveness of the Roth IRA as a tax shelter is independent of tax rates during retirement.

The tradeoff with a Roth IRA is deciding whether it is worth it to forego the deductibility of

contributions that come with a traditional IRA in order to gain the tax free withdrawals upon

retirement that the Roth IRA provides.

Table 21.2 Traditional vs. Roth IRA Tax Shelters under a Progressive Tax Code

With defined benefit (DB) plans the employer promises to pay a defined or known benefit to

employees when they retire. The benefit is typically a percentage of salary based on years of

service. The employer must fund the pension obligation by setting aside a certain amount of

funds in a pension trust. Many of these funds are managed by life insurance firms (listed under

separate account business). A fully funded pension plan is one where the firm has set aside the

full present value of expected future payments. Many plans are only partially funded. The

Pension Benefit Guaranty Corporation (PBGC) guarantees pension benefits in the event of

corporate bankruptcy, but plan participants often get an inferior pension plan if the plan is

actually administered by the PBGC as a result of bankruptcy. We need some law changes in this

area to protect pensions and medical coverage in the event of bankruptcy and takeovers. The

PBGC is very underfunded and a few large bankruptcies would force a government bailout of

“Penny Benny” as it is called.

Chapter 21 – Taxes, Inflation, and Investment Strategy

Defined contribution (DC) plans include 401k and 403b plans. The employee and the employer

contribute set (defined) amounts to an investment plan. The employee’s retirement benefit

depends on the investment performance. Employees are typically given a choice of mutual funds

managed by a fund family such as Vanguard or Fidelity. Because of the employer contributions

individuals should participate in these plans before funding IRAs. DC plans are becoming the

standard, although substantial DB assets remain. Some firms offer both. Note that the

employees have no corporate bankruptcy risk in a DC plan. If the sponsoring corporation went

bankrupt no creditor could seize the plan’s assets. The 401k and 403b terms come from the

relevant sections of the tax code. 401k plans are used in the for-profit sector and 403b plans are

for non-profits, but they are very similar to one another in function and regulations.

Table 21.3 Investing Roth IRA Contributions into Stock and Bonds

Some investors make the mistake of putting stocks in their IRA and buy bonds outside their IRA.

The interest income on bonds is taxed each year and is taxed at the ordinary income rate. Much

of the gain on stocks is taxed at the lower capital gains tax rate.

Chapter 21 – Taxes, Inflation, and Investment Strategy

6. Social Security

PPT 21-24 through PPT 21-25

Social Security (SS) is a federal pension plan established to provide minimum retirement

benefits to all workers. Technically it is the Old Age and Survivors Disability Fund. It is

unfunded although it is in surplus on a current year basis, but it is projected to go in the red

around 2016.

U.S. citizens pay 6.2% of their income to SS, plus 1.45% toward Medicare and their employer

matches their contribution.

1

SS is a means of redistributing income. In dollar terms taxes are

regressive, rising with income but low income workers receive a relatively larger share of

preretirement income upon retirement than higher income workers.

Citizens pay in every working year but only the top 35 years of earnings & contributions count

for determining benefits. A lifetime real annuity is paid in full if one retires at age 67, one

receives a reduced amount if one retires earlier (as early as 62) or one receives a larger benefit if

one retires later (as late as 70). The retirement ages will be going up to help for younger people

to reduce the fiscal problems of the plan.

There are four steps required to calculate an individual’s benefits:

1. The series of the taxed annual earnings is compiled

2. Indexing Factor Series: All past earnings are converted to today’s dollars using the

Average Wage Index (AWI)

3. Average Indexed Monthly Earnings (AIME)

The 35 highest annual indexed contributions are summed and then divided by (35 x 12) =

420. This number is the AIME. If an individual works less than 35 years their AIME

may be low because the number is still divided by 420.

4. Primary Insurance Amount (PIA): The PIA is the amount the individual receives each

year. No exact formula is provided for this calculation. The income replacement rate is

the percentage of the working income received in retirement. The income replacement

rate is substantially higher for low income individuals than for those with higher income.

SS benefits may be taxed if household income is greater than $32,000. Benefits are taxed at 50%

if household income is greater than $44,000. Table 21.5, Social Security Annuities if You Were

to Retire in 2009 at Age 65, provides examples of the annuity that would be paid for individuals

with different levels of income.

1

Actually you would pay the 7.65% taxes on the first $106,800 of your income in 2009. On your paycheck this will be in the

FICA section. Note that between the employee and the employer 12.4% is being paid in to fund SS.

Chapter 21 – Taxes, Inflation, and Investment Strategy

7. Additional Considerations

PPT 21-26 through PPT 21-28

The text identifies and very briefly describes how specific considerations such as funding a

child’s college education, should be built into the financial plan. Financing a child’s education

involves the same procedure as funding retirement. One gains no equity in renting, and equity is

a safeguard for tough times. Too many people try to buy too much house and this can limit their

ability to save as well as stress their relationships. Houses are illiquid investments whose value

does not always increase.

transfers.

Excel Applications

The best method to cover the material in this chapter involves the integrated use of the models

that are available on the web. The impact that each of the factors has on performance can be

demonstrated in class. The power point presentation gives an overall framework to the

discussion but if the material is to be covered in detail, using the excel applications is essential.