Chapter 20 – Hedge Funds

CHAPTER 20

HEDGE FUNDS

1. No, a market-neutral hedge fund would not be a good candidate for an investor’s

entire retirement portfolio because such a fund is not a diversified portfolio. The

3. At the end of two years, the fund value must reach at least 104.04% of its base

4. a. Survivorship bias and backfill bias both result in upwardly biased hedge fund

index returns. Survivorship bias happens when unsuccessful funds cease

5. b. The S&P 500. The shared goal of all types of hedge funds is seeking absolute

returns— finding positive alpha which is above the required returns of the market

6. c. The extra layer of fees only.

7. a. A market-neutral hedge fund. Using the strategy, the fund tries to achieve a net

8. The incentive fee of a hedge fund is part of the hedge fund compensation structure;

Chapter 20 – Hedge Funds

9. There are a number of factors that make it harder to assess the performance of a

hedge fund portfolio manager than a typical mutual fund manager. Some of these

factors are:

• Hedge funds tend to invest in more illiquid assets so that an apparent alpha

may be in fact simply compensation for illiquidity.

• Hedge funds’ valuation of less liquid assets is questionable.

10. No, statistical arbitrage is not true arbitrage because it does not involve

establishing risk-free positions based on security mispricing. Statistical arbitrage

11. Management fee = .02 $1 billion = $20 million

Portfolio Rate

of Return (%)

Incentive Fee

(%)

Incentive Fee

($ million)

Total Fee

($ million)

Total Fee

(%)

a.

–5

0

0

20

2

b.

0

0

0

20

2

c.

5

0

0

20

2

d.

10

20

10 [.2 × (.10-.05)]

30

3

12. The incentive fee is typically equal to 20% of the hedge fund’s profits beyond a

particular benchmark rate of return. However, if a fund has experienced losses

in the past, then the fund may not be able to charge the incentive fee unless the

13.

a. First, compute the Black-Scholes value of a call option with the

following parameters:

S0 = 62

X = 66

Chapter 20 – Hedge Funds

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

R = .04

= .50

T = 1 year

Therefore: C = $11.685

The value of the annual incentive fee is:

.20 × C = .20 $11.685 = $2.337

b. Here we use the same parameters used in the Black-Scholes model in part

(a) with the exception that: X = 62

Now: C = $13.253

d. Here we use the same parameters used in the Black-Scholes model in part

(a) with the exception that: X = 62 and = .60

Now: C = $15.581

14.

a. The spreadsheet indicates that the end-of-month value for the S&P 500 in

September 1977 was 96.53, so the exercise price of the put written at the

At the end of October, the value of the index was 92.34, so the put would

have expired out of the money and the put writer’s payout was zero. Since

it is unusual for the S&P 500 to fall by more than 5 percent in one month,

all but ten of the 120 months between October 1977 and September 1987

would have a payout of zero. The first month with a positive payout

would have been January 1978. The exercise price of the put written at

the beginning of January 1978 would have been:

Chapter 20 – Hedge Funds

At the end of January, the value of the index was 89.25 (more than

a 6% decline), so the option writer’s payout would have been:

90.3450 – 89.25 = 1.0950

15.

a. In order to calculate the Sharpe ratio, we first calculate the rate of return

for each month in the period October 1982-September 1987. The end of

month value for the S&P 500 in September 1982 was 120.42, so the

exercise price for the October put is:

.95 120.42 = 114.3990

Since the October end of month value for the index was 133.72, the put

expired out of the money so that there is no payout for the writer of the

option. The rate of return the hedge fund earns on the index is therefore

equal to:

Chapter 20 – Hedge Funds

The May end of month value for the index was 150.55, and therefore

the payout for the writer of a put option on one unit of the index is:

152.0475 – 150.55 = 1.4975

The rate of return the hedge fund earns on the index is equal to:

The payout of 1.4975 per unit of the index reduces the hedge fund’s

rate of return by:

1.4975/160.05 = .00936 = .936%

The rate of return the hedge fund earns is therefore equal to:

– .05936 – .0936 = –6.872%

The end of month value of the fund is:

$100.25 million .93128 = $93.361 million

The rate of return for the month is:

($93.361/$100.00) – 1 = – .06639 = –6.639%

For the period October 1982-September 1987:

b. For the period October 1982-October 1987:

Mean monthly return = 1.238%

P

c. Extending the sample period by one month decreases the mean monthly

return. Moreover, the standard deviation jumps by more than 2 percentage

points, showing that there is considerable tail risk for the fund. The Sharpe

ratio also realized a drastic decline.

16.

a. Since the hedge fund manager has a long position in the Waterworks

stock, he should sell nine contracts, computed as follows:

$6,000,000 .75 45

=

Chapter 20 – Hedge Funds

b. The standard deviation of the monthly return of the hedged portfolio is

c. The expected rate of return of the market-neutral position is equal to

the risk-free rate plus the alpha: .005 + .02 = .025 = 2.5%

17.

a. The residual standard deviation of the portfolio is smaller than each stock’s

standard deviation by a factor of 100 = 10 or, equivalently, the residual

variance of the portfolio is smaller by a factor of 100. So, instead of a

18.

a. For the (now improperly) hedged portfolio:

Variance = ( .252 .052) + .062 = .00375625

Standard deviation =

00375625.

= .06129 = 6.129%

b. Since the manager has misestimated the beta of Waterworks, the manager

will sell six S&P 500 contracts:

$6,000,000 .50 30

$50 2,000

=

Chapter 20 – Hedge Funds

The portfolio is not completely hedged so the expected rate of return

is no longer 2.5%. We can determine the expected rate of return by

first computing the total dollar value of the stock plus futures

position. The dollar value of the stock portfolio is:

$6,000,000 (1 + rPortfolio)

=$6,000,000 [1 + rf + (rM – rf) + + e]

The dollar proceeds from the futures position equal:

30 contracts $50 (F0 − F1) = $1,500 [(S0 1.005) – S1]

The total value of the stock plus futures position at the end of the month is:

$6,127,500 + ($4,500,000 rM ) + ($6,000,000 e) +

$15,000 − ($3,000,000 rM)

The expected rate of return for the (improperly) hedged portfolio is:

($6,157,500/$6,000,000) – 1 = .02625 = 2.625%

Now the z-value for a rate of return of zero is:

c. The variance for the diversified (but improperly hedged) portfolio is:

(.252 .052) + .0062 = 1.9225

Standard deviation =

9225.1

= 1.3865%

The z-value for a rate of return of zero is:

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

written consent of McGraw-Hill Education.

The probability of a negative return is: N(−1.8933) = .0292

The probability of a negative return is now far greater than the result with

proper hedging.

d. The market exposure from improper hedging is far more important in

19. a., b., c.

Hedge

Fund 1

Hedge

Fund 2

Hedge

Fund 3

Fund

of Funds

Stand-

Alone

Fund

Start of year value (millions)

$100.0

$100.0

$100.0

$300.0

$300.0

Gross portfolio rate of return

20%

10%

30%

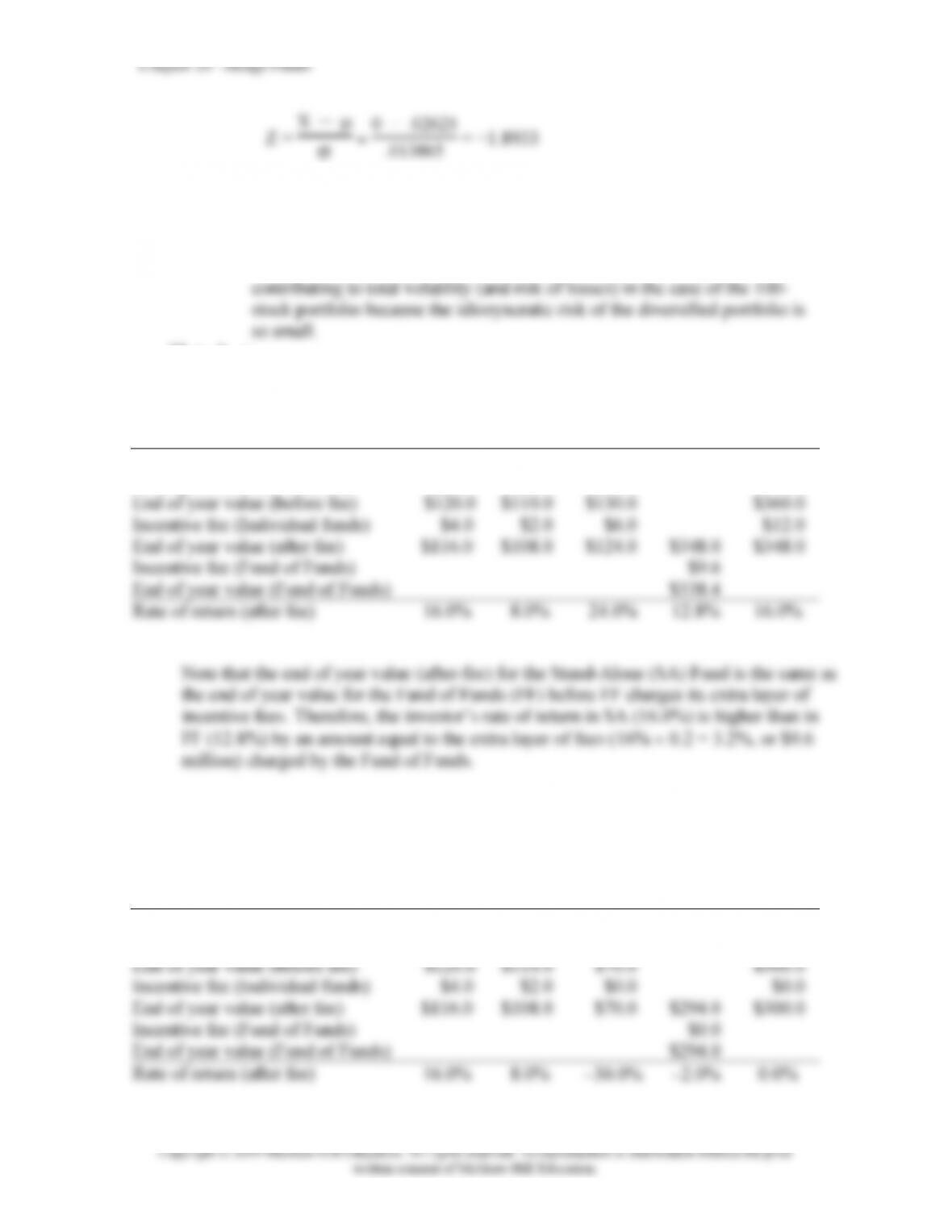

End of year value (before fee)

$120.0

$110.0

$130.0

$360.0

Incentive fee (Individual funds)

$4.0

$2.0

$6.0

$12.0

End of year value (after fee)

$116.0

$108.0

$124.0

$348.0

$348.0

Incentive fee (Fund of Funds)

$9.6

End of year value (Fund of Funds)

$338.4

Rate of return (after fee)

16.0%

8.0%

24.0%

12.8%

16.0%

d.

Hedge

Fund 1

Hedge

Fund 2

Hedge

Fund 3

Fund

of Funds

Stand-

Alone

Fund

Start of year value (millions)

$100.0

$100.0

$100.0

$300.0

$300.0

Gross portfolio rate of return

20%

10%

−30%

End of year value (before fee)

$120.0

$110.0

$70.0

$300.0

Incentive fee (Individual funds)

$4.0

$2.0

$0.0

$0.0

End of year value (after fee)

$116.0

$108.0

$70.0

$294.0

$300.0

Incentive fee (Fund of Funds)

$0.0

End of year value (Fund of Funds)

$294.0

Rate of return (after fee)

16.0%

8.0%

−30.0%

−2.0%

0.0%

Chapter 20 – Hedge Funds

e. Now, the end of year value (after fee) for SA is $300, while the end of

year value for FF is only $294, despite the fact that neither SA nor FF

charges an incentive fee. The reason for the difference is the fact that the