Chapter 02 – Asset Classes and Financial Instruments

CHAPTER TWO

ASSET CLASSES AND FINANCIAL INSTRUMENTS

CHAPTER OVERVIEW

One of the early investment decisions that must be made in building a portfolio is asset

allocation. This chapter introduces some of the major features of different asset classes and

some of the instruments within each asset class. The chapter first covers money market

securities. Money markets are the markets for securities with an original issue maturity of one

LEARNING OBJECTIVES

Upon completion of this chapter the student should have an understanding of the various

financial instruments available to the potential investor. Readers should understand the

differences between discount yields and bond-equivalent yields and some money-market-rate-

quote conventions. The student should have an insight as to the interpretation, composition, and

calculation process involved in the various market indexes presented on the evening news.

Finally, the student should have a basic understanding of options and futures contracts.

CHAPTER OUTLINE

PPT 2-2 through PPT 2-3

The major classes of financial assets or securities are presented in PPT slide 2. This material can

be used to discuss the chapter outline and the purposes of these markets. Instruments may be

classified by whether they represent money market instruments, which are primarily used for

savings, or capital market instruments. Savings may be defined as short-term investments that

pay a low rate of return but do not risk the principal invested. Capital market investments will

entail chance of loss of some or even all of the principal invested but promise higher rates of

return that allow significant growth in portfolio value.

2. Money Market Instruments

Chapter 02 – Asset Classes and Financial Instruments

PPT 2-4 through PPT 2-20

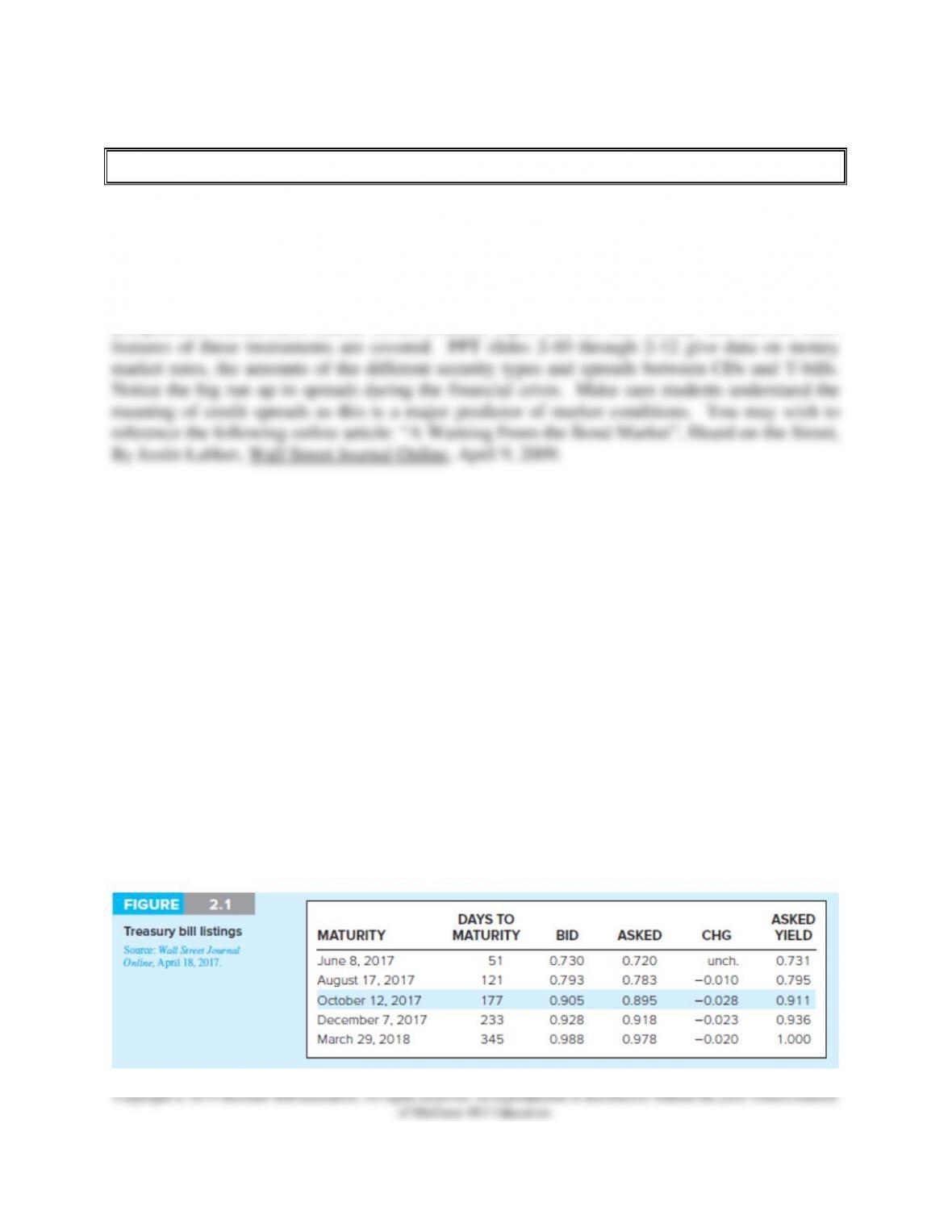

The major money market instruments that are discussed in the text are presented in PPT 2-4

through PPT 2-14. Treasury bills, certificates of deposit (CDs) and commercial paper are

covered in the most detail. The issuer, typical or maximum maturity, denomination, liquidity,

default risk, interest type and tax status are presented for these instruments. The majority of

undergraduate students will have very little knowledge of the workings of these investments and

this is very useful information for them. Generally less detail is provided for bankers’

acceptances, Eurodollars, federal funds, LIBOR, repos and the call money rate but the main

Money Market Mutual Funds (MMMF) and the Credit Crisis of 2008:

PPT 2-15 shows that between 2005 and 2008 money market mutual funds (MMMFs) grew by

88%. Why? After years of declining growth rates, MMMF inflows accelerated rapidly as

investors fled risky assets during the crisis and sought safety in money funds. However, MMMFs

had their own crisis in 2008 after Lehman Brothers filed for bankruptcy on September 15

because some money funds had invested heavily in Lehman commercial paper. On Sept. 16 a

MMMF, the Reserve Primary Fund, “broke the buck.” What does this mean? MMMF shares

normally have a value of $1.00 plus any accrued interest, but fund shares are never supposed to

fall below $1.00. Some investors use these funds to pay bills as most have a checking feature

and count on the shares maintaining their value. Reserve Primary Fund shares fell below $1.00

as the fund’s losses mounted. A run on money market funds ensued. The U.S. Treasury

temporarily offered to insure all money funds (for an insurance fee) to stop the run. Assets in

these funds total about $3.4 trillion.

Money Market Yields:

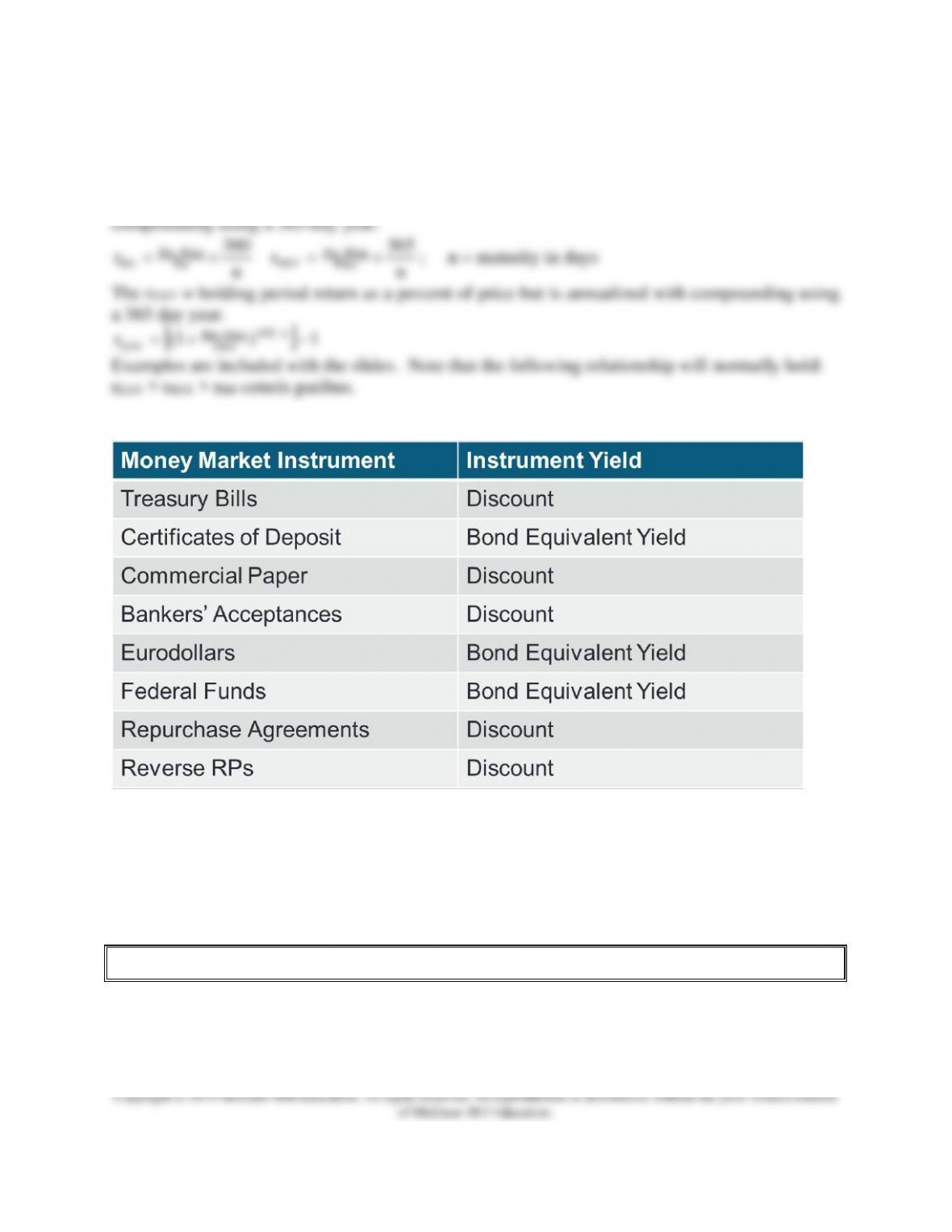

Money market yield sample calculations are presented and illustrated in this set of slides. The

bank discount rate rBD is compared to the bond equivalent yield rBEY and the effective annual

yield rEAY.

Chapter 02 – Asset Classes and Financial Instruments

rBD is calculated as a return as a percentage of the face value or par value of the instrument and is

quoted as annualized without compounding using a 360 day year. rBEY is calculated as a return as

a percentage of the initial price of the instrument and is quoted as annualized without

Money Market Instruments and Yield Type

Note: CDs, Euro$ and Federal Funds all use add-on quotes which are not quite the same as BEY,

since the add on uses a 360-day year. However, “add ons” are not covered in the text. To

convert from add on to BEY use the following: BEY = radd on * (365/360)

3. The Bond Market

PPT 2-21 through PPT 2-29

Chapter 02 – Asset Classes and Financial Instruments

Debt instruments are issued by both government (sometimes called public) and by private

entities. The Treasury and Agency issues have the direct or implied guarantee of the federal

government. As state and local entities issue municipal bonds, performance on these bonds does

not have the same degree of safety as a federal government issue. The interest income on

municipal bonds is not subject to federal taxes so the taxable equivalent yield is used for

comparison.

Agency issues have either explicit or implicit backing by the Federal Government and their

securities normally carry an interest rate only a few basis points over a comparable-maturity

Treasury instrument. Federal agencies have different charters but are generally charged with

assisting socially deserving sectors of the economy in obtaining credit. The major example is

housing, although farm lending and small business loans are other good examples. However, the

major agencies are home-mortgage related, and include the Federal National Mortgage

Association (FNMA or Fannie Mae); the Federal Home Loan Mortgage Corporation (FHLMC or

Freddie Mac); the Government National Mortgage Association (GNMA or Ginnie Mae); and the

Federal Home Loan Banks. GNMA has always been a government agency. GNMA backs pools

of FHA- and VA- insured mortgages (for a fee) created by private pool of organizers. FNMA

was originally a government agency that provided financing to originators of FHA and VA

mortgages, but was privatized in 1968. FHLMC was created in 1972 to assist in financing of

conventional mortgages. In September 2008, the federal government took over FNMA and

FHLMC and created a new regulator, the Federal Housing Financing Authority. FNMA and

FHLMC together finance or back about $6 trillion in home mortgages. This represents about

50% of the U.S. market.

Chapter 02 – Asset Classes and Financial Instruments

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Private Issues:

Private issues include corporate debt and equity issues and asset-backed securities, including

mortgage- backed securities. Bonds issued by private corporations are subject to greater default

risk than bonds issued by government entities. Corporate bonds often contain imbedded options

such as a call feature which allows an existing corporation to repurchase the bond from issuers

when rates have fallen. Some bonds are convertible which allows the bond investor to convert

the bond to a set number of shares of common stock.

Most bonds are rated by one or more of the major ratings agencies approved by the federal

government. The major agencies are Standard & Poors, Moody’s and Fitch. The rating

measures default risk. The higher the rating the lower the interest rate required to issue the

bonds. The two major classes of bonds with respect to default risk are investment grade and

speculative grade. Investment grade bonds are much more marketable and carry significantly

lower interest rates than speculative grade bonds. Speculative grade bonds are euphemistically

called ‘junk’ bonds. Spreads on junk bonds reached record highs in 2008 and 2009.

The mortgage market is now larger than the corporate bond market. Securities backed by

mortgages have also grown to compose a major element of the overall bond market. A pass–

through security represents a proportional (pro-rata) share of a pool of mortgages. The mortgage-

backed market has grown rapidly in recent years as shown in Text Figure 2.6. Originally only

“conforming mortgages” were securitized and used to back mortgage securities. Conforming

mortgages met traditional creditworthiness standards such as a maximum 80% loan-to-value

ratio; maximum debt-to-income ratio of around 30%; and a quality-credit score. Until about

2006, Fannie and Freddie only underwrote or guaranteed conforming mortgages. Under political

pressure to make housing available to low-income families however, Fannie and Freddie began

securitizing and backing subprime mortgages (mortgages to households with insufficient income

to qualify for a standard mortgage) and so called “Alt–A” mortgages which lie between

conforming and subprime in terms of credit risk. Most of the mortgages in the lower-quality

categories originated since 2006 have deteriorated in value. The term “underwater” means the

homeowners owe more than the market value of their home, creating an incentive to default.

Foreclosures depress local home prices, and add to the credit problems of banks and thrifts that

supply mortgage credit, hence the government’s efforts to limit the number of foreclosures.

3. Equity Securities

PPT 2-32 through PPT 2-37

Chapter 02 – Asset Classes and Financial Instruments

Several key points are relevant in the discussion of equity instruments. First, common stock

owners have a residual claim on the earnings (dividends) of the firm. Debt holders and preferred

stockholders have priority over common stockholders in the event of distress or bankruptcy.

Stockholders do have limited liability and a shareholder cannot lose more than their initial

investment. Common stockholders typically have the right to vote on the board of directors and

the board can hire and fire managers. Even though stockholders have the right to vote it may be

difficult to effect change because of a low concentration of stock holdings among many small

investors. For instance in the April 2009 shareholder meeting of Citicorp shareholders all

existing directors were reelected even though many shareholders were very vocal in their

disapproval of Citicorp’s performance (Citicorp had abysmal performance in 2008 and had to be

bailed out by the government; most shareholder value was destroyed).

Michael Jacobs, a former Treasury official, wrote in The Wall Street Journal that Citicorp had

few directors with experience in the financial markets and GE had only one director with

experience in a financial institution even though GE Capital is a major component of the firm.

Problems at GE Capital led to a loss of GE’s AAA credit rating.

1

Preferred shareholders have a priority claim to income in the form of dividends. Ordinary

preferred stockholders are limited to the fixed dividend while common shareholders do not have

limits. The partial tax exemption on dividends of one corporation being received by another

corporation is important in discussing preferred stock. Preferred and common dividends are not

tax deductible to the issuing firm. Corporations are given a tax exemption on 70% of preferred

dividends earned.

4. Stock and Bond Market Indexes

PPT 2-38 through PPT 2-41

1

“How Business Schools Have Failed Business: Why Not More Education on the Responsibility of Boards?” by Michael

Jacobs, The Wall Street Journal Online, April 24, 2009.

Chapter 02 – Asset Classes and Financial Instruments

Stock indexes are used to track average returns, compare investment managers’ performance to

an index and as a base for derivative instruments. Key factors to consider in constructing an

index include a) what the index is supposed to measure, b) whether a representative sample of

firms can be used or whether all firms must be included, c) how the index should be constructed.

The examples of domestic indexes displayed in the PPT slides illustrate the diversity of indexes

in use. The Wilshire, being the broadest of the indexes, captures the overall domestic market.

The DJIA captures the returns from the ‘bluest of blue chips’ or a sample of very large well-

known firms. The sample of domestic indexes also fit well with discussion of uses of the index.

If the index will be used to assess the performance of a manager that invests in Small-Cap firms,

the DJIA would not be as appropriate a benchmark as the NASDAQ Composite.

The creator of an index must decide how to weight the securities included in the index. Price-

weighted indexes use the stock’s price as the weight for that security. Price-weighted averages

are probably the poorest form of index because high price stocks have a bigger weight in the

index (there is no theoretical reason for this) and stock splits arbitrarily reduce that weight. The

other choices are market-value weighted (most common) and equal-value weighted. Which of

these two is better depends on your objectives. In a value-weighted index the amount invested in

each stock in the index is proportional to the market value of the firm. The market value of the

firm is the weight for each stock. Changes in the value of larger firms affect the index more than

changes in the value of the stock of a firm with smaller market capitalization. Value-weighted

indexes are more common and are probably a better indicator of the overall change in stocks’

5. Derivative Securities

PPT 2-42 through PPT 2-48

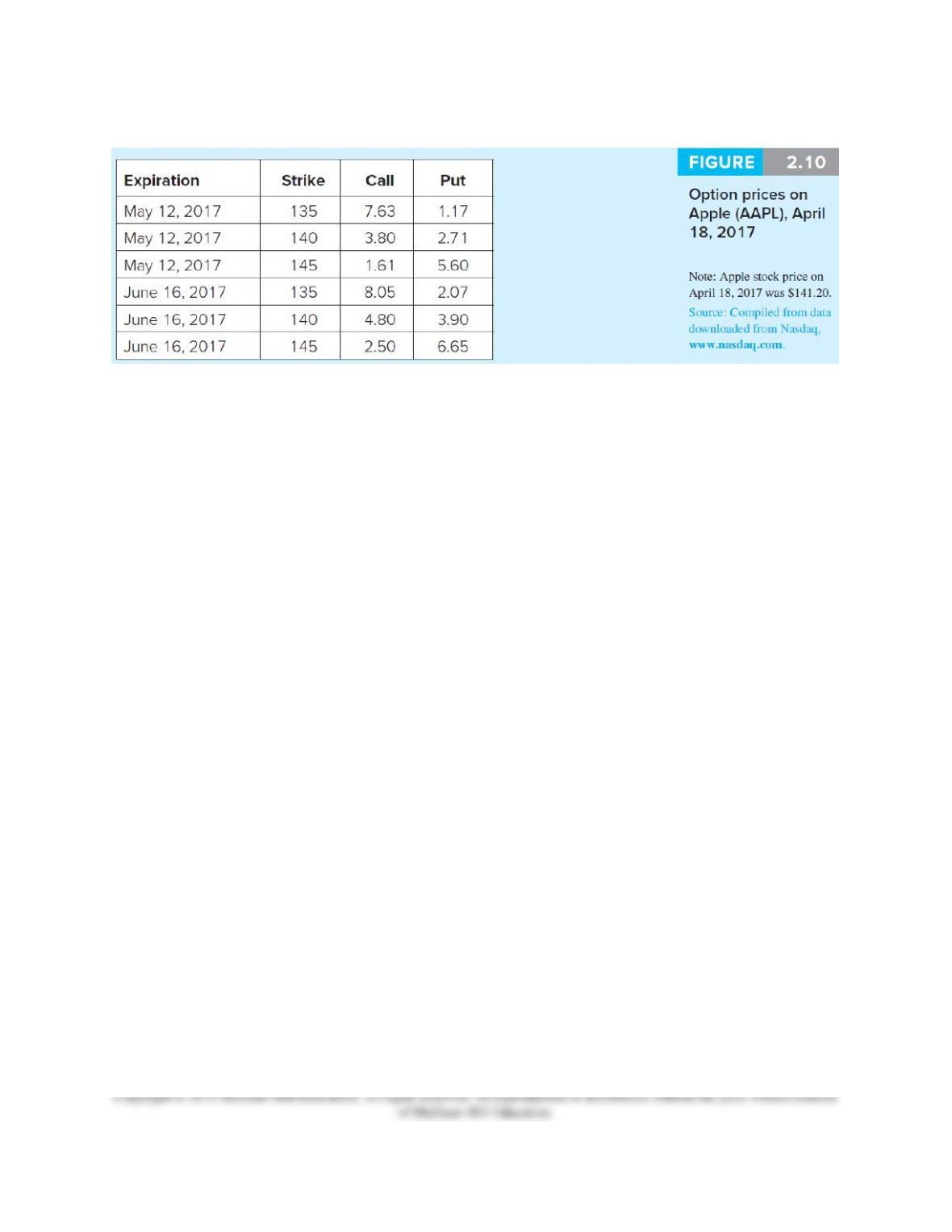

Listed call options are explained and illustrated on slides 41 through 49. Calls and puts are

defined and Text Figure 2.10 is used to illustrate option quotes and very basic option positions.

The effect of exercise price and time to expiration on a call and a put are illustrated with this

figure. A very basic definition of a futures contract is provided on PPT slide 45. Figure 2.11 is

used to illustrate how to read a futures price quote for a corn futures contract.

Chapter 02 – Asset Classes and Financial Instruments

The main point to emphasize in the option and futures discussion is that futures entail a

commitment to a future purchase or sale whereas options give the holder the right to buy (with a

call) or sell (with a put) the underlying commodity. The instructor should be aware that options

and futures markets are highly competitive. On the whole many futures markets are cheaper and

more liquid than options markets. The “right” associated with the option is more expensive.