Chapter 18 – Portfolio Performance Evaluation

CHAPTER EIGHTEEN

PORTFOLIO PERFORMANCE EVALUATION

CHAPTER OVERVIEW

This chapter presents various performance measures that are used for evaluation of portfolios.

The process of decomposing portfolio returns into the various components of the portfolio-

building process is presented. Performance measures of market timing, security selection and

adding securities to a diversified portfolio are introduced.

LEARNING OBJECTIVES

After studying this chapter, the student should be able to calculate various risk-adjusted return

measures, including Jensen’s alpha, the Sharpe and Treynor ratios, the M2 measure, and the

CHAPTER OUTLINE

1. Investment Clients, Service Providers, Objectives of Performance Evaluation

PPT 18-2 through PPT 18-18

Passive management consists of choosing a capital allocation between cash and the risky

portfolio and choosing the asset allocation within the risky portfolio. However, how passive the

management actually is varies from, “set it and forget it,” to changing allocations in according to

perceptions of risk to keep current with portfolio goals. Active management is a step beyond.

Active management involves forecasting future rates of return on either/both asset classes and

individual securities. Passive management, even if the portfolio is updated, is basically focused

on the level of risk of the portfolio in conjunction with the stated portfolio goals. Active

management is far more difficult. Risk levels are fairly stable but expected returns are not.

Successful forecasting of future prices and rates of return is very difficult in the highly

competitive markets we have. It requires either private information, or perhaps some better

analytical or instinctual method of analysis. A true market timer focuses on allocation between

the risky and riskless portfolios, although most actually change broad class allocations and

reallocate within the risky portfolio as well. It is a stretch to call a market timer a passive

investor, so there is a bit of ambiguity here.

Chapter 18 – Portfolio Performance Evaluation

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

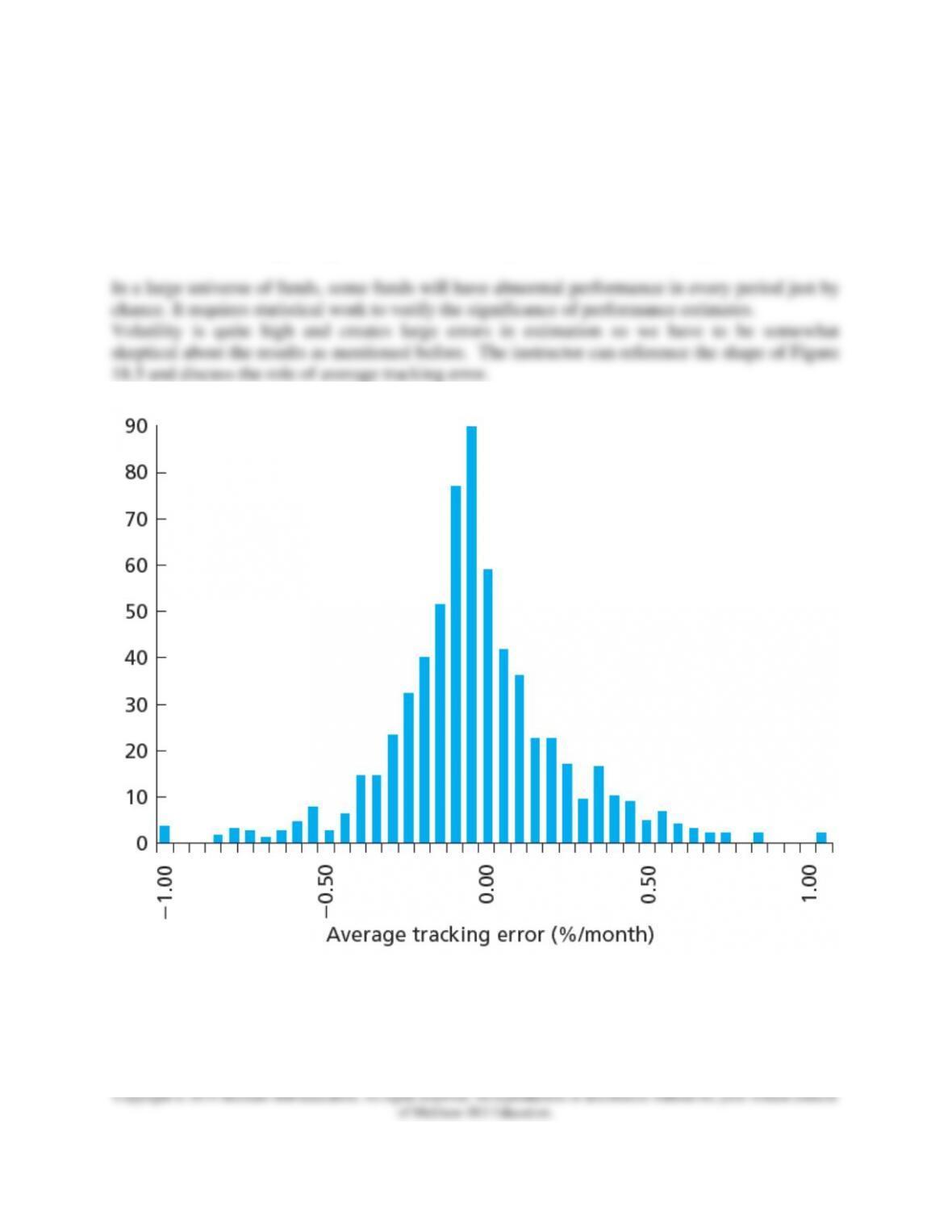

What is needed is a measure of abnormal performance. One can get more return in bull markets

by taking on more risk, this doesn’t mean the managers are adding value; can they generate good

returns consistently through time across different market cycles? It takes measures that

incorporate risk and it requires statistical work to make us believe the results are not just due to

chance.

How can managers generate abnormal performance? There are several means:

• Successful across asset allocations (time the market)

• Superior allocation within each asset class (weight sectors)

o Sectors or industries

o Overweight better performing sectors, underweight poorer performers

• Individual security selection (pick stocks)

o Pick the right stocks, those with performance better than expected

The most valuable activity and the toughest to do successfully is time the market.

Obtaining an accurate estimate of risk-adjusted performance for a portfolio manager is difficult

for several reasons. First, in order to measure abnormal performance one needs an accurate

model of normal performance. Is a single index model an adequate measure of expected

performance or should a multi-index model be used? Second, most of the sound measures of

risk-adjusted returns require stability for the portfolio. Most portfolios are actively managed and

the stability assumptions are not met. Third, in competitive markets with significant volatility,

identifying the actual level of abnormal performance that is likely to occur is very difficult. The

probability of a Type 2 error is quite high.

Basic performance measurement compares portfolio performance to some benchmark portfolio.

The comparison to the benchmark is only appropriate if the risk is the same. Comparison groups

are very popular within the industry. It is the simplest method and involves comparing

performance of funds with similar objectives. The market model or index model approaches are

theoretically superior because they explicitly adjust for different levels of systematic risk.

The Sharpe Measure is also widely accepted in industry. This measure indicates the slope of the

CAL and it is based on the portfolio risk premium and the total risk of the portfolio as measured

by standard deviation.

p

fp

σ

rr

Ratios Sharpe −

=

Chapter 18 – Portfolio Performance Evaluation

The Treynor measure also calculates the excess return to variability ratio but it uses the portfolio

beta as the risk measure. The Sharpe and the Treynor measures should result in similar rankings

for most widely diversified portfolios. With portfolios that are widely diversified, most of the

risk will be systematic.

One may want to compare the reward to risk ratios where risk is measured as solely systematic

risk.This measure asks the question, “How much excess return does one get for the level of

risk?” In a well diversified portfolio systematic risk will be the only remaining risk. This

measure might still be useful if we are analyzing a non-diversified portfolio such as a sector fund

that is held in conjunction with other funds that in total are diversified. This is an important

point to stress to the students.

The M2 measure is a variation of the Sharpe Ratio that is easier to interpret. The concept of the

Sharpe is easy to interpret but the Sharpe number is not. It was developed by Modigliani and

Modigliani; hence M2. One uses M2 to compare the performance of a managed portfolio (MP)

with a market index. The M2 measure creates a hypothetical complete portfolio that is composed

of T-bills and the MP that has the same standard deviation as the market index. This allows

comparing the portfolio return directly with the level of return of the market.

p

fp rr

Ratios Treynor

−

=

*

*

2()

M M P M

P

M

P P M P

PP

M

M M M M

M

M R R S S

where

R wR R S

R

RS

= − = −

= = =

==

Chapter 18 – Portfolio Performance Evaluation

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

When evaluating a portfolio to be mixed with a position in the passive benchmark portfolio one

must draw on insights of the Treynor-Black (TB) Model (See Chapter 6 for this model.)

If you are a fund manager you may try to analyze several companies. If a manager has the ability

to find undervalued stocks, what strategy should a portfolio manager use in investing in those

stocks? The percentage of funds allocated to undervalued stocks depends, in part, on the ability

of the manager. If a manager has perfect foresight, theoretically all funds should be placed in the

most undervalued stocks. If the manager has substantial funds however, buying pressure could

make that impossible. The risk of such a strategy would be extreme in any case. Most portfolio

managers would not have perfect ability in identifying undervalued securities. For most

managers, the process involves some passive investment in stocks in addition to acquiring the

undervalued stocks. The Treynor-Black Model is used to combine an actively managed portfolio

with a passively managed portfolio. To determine the optimal allocations the portfolio managers

must be able to forecast expected returns and risk for both the actively managed and passively

managed portfolios. The relevant measure of risk for the actively managed portfolio is its ratio

of alpha to nonsystematic risk.

Chapter 18 – Portfolio Performance Evaluation

Using a reward-to-risk measure that is similar to the Sharpe Measure, the optimal combination of

active and passive portfolios can be determined. The idea is to choose the portfolio, which when

combined with the passive benchmark, generates an efficient frontier with the best return per unit

of risk as measured by the standard deviation. This is found by combining the Sharpe ratio of

the benchmark M with the information ratio of portfolio P:

Summary of measures and usage

Performance

Measure Definition Application

Sharpe p

R/

as the

When choosing

among portfolios

competing

optimal risky portfolio

Treynor Rp/

When ranking many

portfolios that will be

mixed to form the

optimal risky portfolio

Information

ratio p

/ e

When evaluating a

portfolio to be mixed

with a position in the

passive benchmark

portfolio

→

This edition of the text goes much further in explaining alpha and its relationship to other

performance measures.

= Correlation between RP & RM

A positive alpha does not guarantee a higher Sharpe than the benchmark because SM(r-1) < 0.

Thus a positive alpha is a necessary but not a sufficient condition for net performance

improvement.

The alpha must be large enough to offset increase in residual risk from moving away from the

diversified optimum. Take note though that this conclusion about alpha changes if one can use

short sales and hedge out the risks.

Alpha and the Treynor measure

A positive alpha does not guarantee a higher Treynor ranking because one must know the beta as

well. Alpha and the Information Ratio:

P

P

MMP )1(SSS

+−=−

P

P

MP TT

=−

P

e

P

σ

α

Ratio nInformatio =

Chapter 18 – Portfolio Performance Evaluation

A positive alpha does not guarantee a higher square of the information ratio because a higher

alpha may come with higher residual risk.

Alpha Capture & Transport

If an analyst finds an undervalued security and invests in it, market moves may still wipe out any

gains. Remember this is called fundamental risk. However, one can hedge out market risk via

shorting a stock index or stock index futures to establish a market neutral position. Recall that

ETFs can be shorted.

This should eliminate any systematic risk and leave the investor with the stock’s positive alpha.

The process to establish a zero beta or market neutral position is called alpha capture or alpha

transport.

To hedge out systematic risk, short sell βP dollars of the index for every dollar invested in the

portfolio, investing the proceeds in T-bills. The excess return on this zero beta position is:

(the excess return per $ invested in P)

(the excess return on the β dollars sold in M)

(the excess returns on the T-bills is always zero)

The Sharpe ratio for Z, SZ, simplifies to the information ratio because ρ = 0 by construction

because with a zero beta, the correlation between Z and M = 0. Note that one could write alpha

as alpha p or alpha z.

When short positions and leverage are allowed a significant non-zero alpha is a sufficient

condition for an improvement in the Sharpe and information ratio. Because this hedge portfolio

establishes a zero beta portfolio, the Treynor measure is undefined. Note that the evidence

indicates that it is difficult to find positive alphas, although it may be easier to find negative

alphas.

Evidence indicates one should use a multi-index model such as the Fama-French model (FF)

(See Chapter 7) to establish the expected return:

This allows an estimation of alpha:

ptPMtPPt eαRβR++=

ptPMtPZ eαRβR++=

MtPRβ−

0

ptPZ eαR+=

P

ZαR=

P

P

Z

P

P

MMZ S or )1(SSS

=

+−=−

ptPHMLtHMLSMBtSMBMtPPt eαrβrβRβR++++=

P

HMLt

HML

SMBt

SMB

Mt

P

Pt αrβrβRβR+++=

Chapter 18 – Portfolio Performance Evaluation

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

If the multi-index model is a better estimator of expected returns then alphas deemed significant

from a single index model are suspect. Evidence indicates that the indices such as the S&P500

have positive alphas when calculated against the FF model, even when a fourth momentum

factor is added. This probably tells us we still don’t have the proper model of expected returns

so all performance evaluation should be viewed skeptically.

The assumptions of stability that underlie the measures of abnormal performance limit their

effectiveness. Actively managed portfolios are, by their nature, not stable. The beta of the

portfolio may be changing substantially over the measurement period. Use of the average beta

for the period could lead to errors in assessing abnormal performance.

2. Style Analysis

PPT 18-19 through PPT 18-22

In recent years style analysis has become popular with the investment industry. The initial work

in style analysis was conducted by Nobel Prize winner Bill Sharpe. A 1992 study of mutual fund

performance found that 91.5% of variation in return could be explained by the funds’ allocations

to bills, bonds and stocks. Style analysis attempts to explain percentage returns by allocation to

style. Style analysis has become popular with the industry.

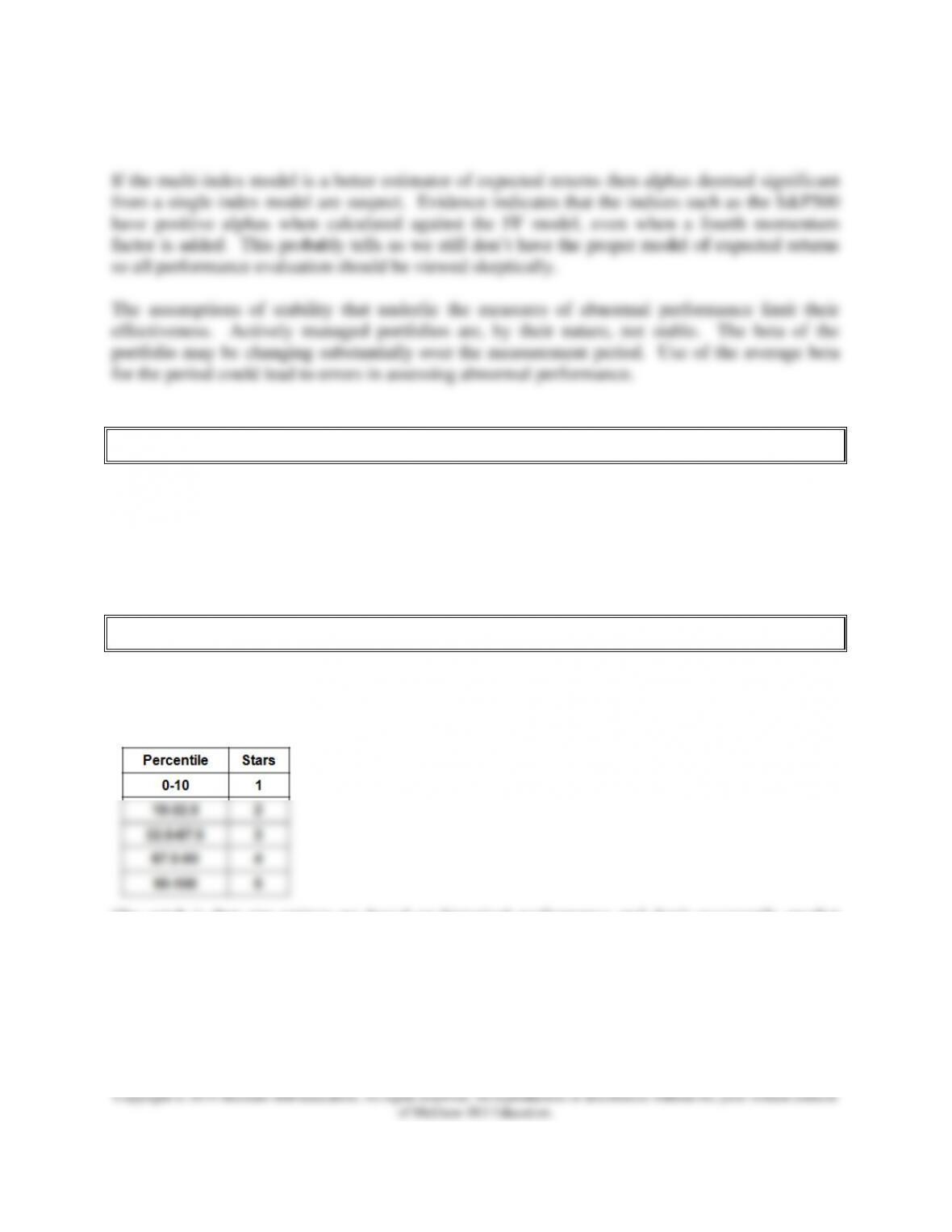

3. Morningstar’s Risk-Adjusted Rating

PPT 18-23 through PPT 18-24

The Morning Star Rating System has also become very popular with the investment community.

The risk adjusted returns they report are very highly correlated with the Sharpe Ratio. The Star

System ranks funds within peer groups based on percentiles as follows:

The catch is that star ratings are based on historical performance and don’t necessarily predict

future performance.

Chapter 18 – Portfolio Performance Evaluation

4. Risk Adjustment with Changing Portfolio Composition

PPT 18-25 through PPT 18-26

Performance measures assume a fund maintains a constant level of risk. This assumption is

violated for most funds and is particularly problematic for funds that engage in active asset

allocation. To see how this affects performance the text constructs a simple example that

students readily grasp and is reproduced here:

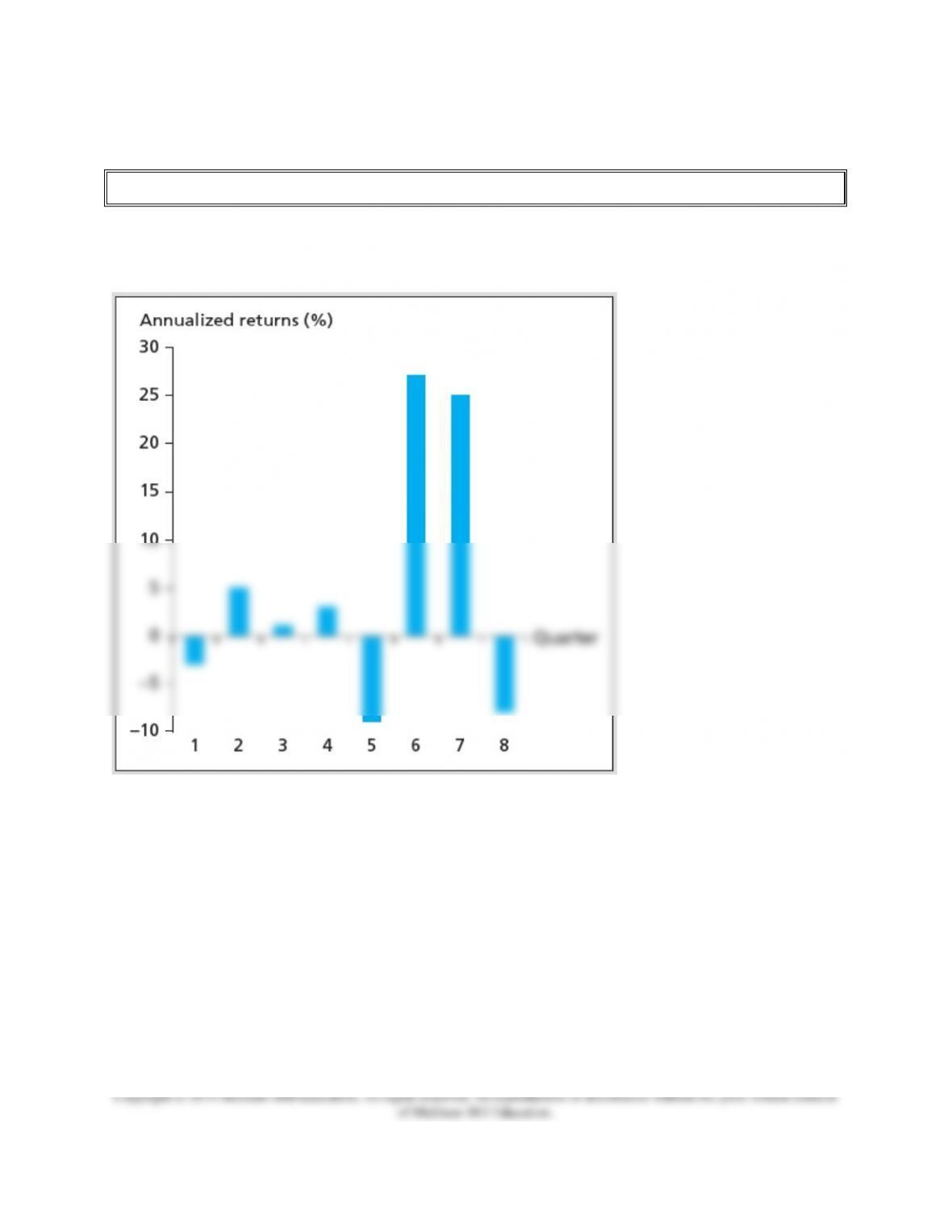

Suppose the Sharpe of the benchmark M = 0.4. We want to know if the active portfolio returns

depicted in the graph generated a superior Sharpe ratio. The fund used a low risk strategy for the

first four quarters and then switched to a high risk strategy for the final four quarters and

generated the following set of excess returns:

First 4 qtrs excess returns are -3%, 5%, 1% and 3%, consistent with the predicted mean and SD

2nd 4 qtrs excess returns are -9%, 27% , 25% and -8%, also consistent with predictions for the

higher volatility period.

Chapter 18 – Portfolio Performance Evaluation

In both years the fund outperformed M which had a Sharpe of 0.4. However if one calculates the

fund’s Sharpe over all 8 quarters one finds an average excess return of 5.125% and a standard

deviation of 13.8% for an Overall Sharpe ratio = 0.37. Switching strategies in the middle creates

the appearance of volatility. Note this violates the assumption of stationary risk. If one didn’t

know about the strategy change one would incorrectly state that the fund underperformed M.

5. Market Timing

Chapter 18 – Portfolio Performance Evaluation

PPT 18-26 through PPT 18-31

If a portfolio manager could time general movements in the market, the performance would be

similar to a call option. When market returns are lower than money market instruments, the

manager would switch out of equities and into money markets. When stock returns will be

higher than money market instruments, all of the funds would be invested in stock. The result

would be higher returns and a smaller standard deviation. A graphical display of perfect market

timing is displayed in the PPT. With less than perfect timing ability, the problem of identifying a

superior market timer becomes a much more difficult task. A long horizon is needed to measure

the ability to time the market to ensure that the manager truly has superior ability to time. We

have not seen a large number of bull and bear markets in recent years. This reduces the accuracy

of testing a manager’s ability to call turns. If the manager of a portfolio can time the market, that

manager would increase the beta on the portfolio when the market is expected to rise. When the

market experiences lower returns or losses, the manager reduces the beta of the portfolio.

The timer doesn’t have to perfectly forecast the cash or the stock market, he or she just has to

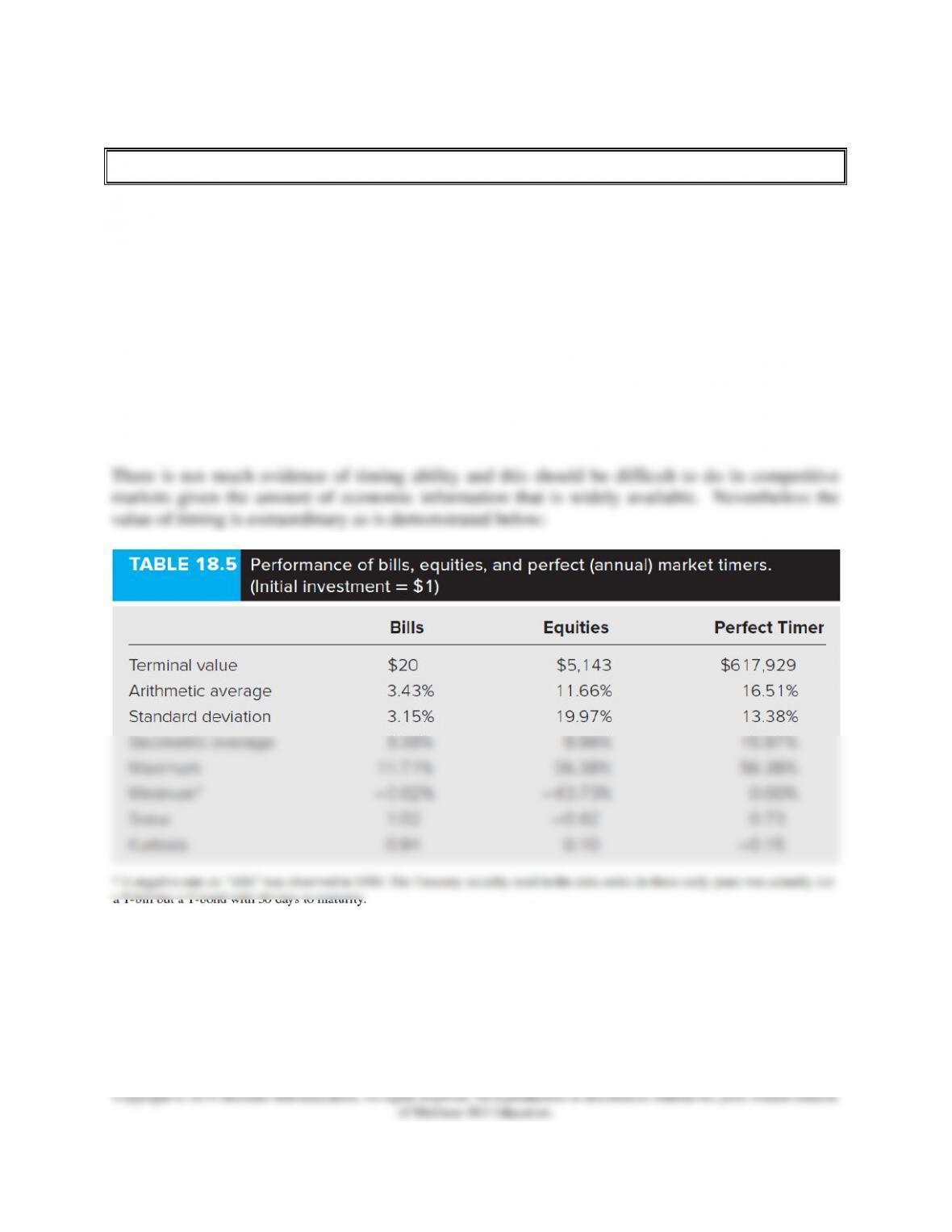

know which one will do better. The time period is 82 years so part of the size of the numbers is

the long time period for compounding. As stated above, there isn’t much evidence of timing

ability but one can understand the lure of it with the size of gains that are possible.

6. Performance Attribution Procedures

Chapter 18 – Portfolio Performance Evaluation

PPT 18-32 through PPT 18-36

Decomposing overall performance into components allows the analyst to determine what aspects

of portfolio choices contributed to good or bad performance.

Major performance determinants include the broad asset allocation among types of securities,

industry weighting in equity portfolio, security choice, and the timing of purchases and sales.

We would like to be able to ascertain the effects of these choices on portfolio performance.

The second step is to calculate the contribution to performance of both sector and security

selection. The next step is to calculate the contribution of the equity sector allocation to total

performance. Finally the security selection component can be inferred by subtracting the sector

allocation return from the total equity extra return. The analysis concludes with a summary of

the performance differences into appropriate categories. Table 18.6 offers a useful example in

the PPT.

Excel Applications

Two Excel applications can be used to enhance the students’ understanding of the material

covered in this chapter. The first application allows the students to perform attribution analysis.

The second application calculates the performance measures presented in this chapter. It allows

students to compare the measures and rankings.