Chapter 15 – Options Markets

CHAPTER 15

OPTIONS MARKETS

1. Options provide numerous opportunities to modify the risk profile of a portfolio. The

simplest example of an option strategy that increases risk is investing in an ‘all options’

2. Options at the money have the highest time premium and thus the highest potential for

gain. Since the highest potential gain is at the money, the logical conclusion is that they

3. Each contract is for 100 shares: $7.25 100 = $725

4. Price at expiration: $71

Cost Payoff Profit

Call option, X = 70 2.02 1.00 -1.02

Put option, X = 70 0.24 0.00 -0.24

Call option, X = 72 0.67 0.00 -0.67

Put option, X = 72 0.90 1.00 0.10

Call option, X = 74 0.13 0.00 -0.13

Put option, X = 74 2.37 3.00 0.63

5. If the stock price drops to zero, you will make $80 – $5.72 per stock, or $74.28. Given

7. a. Maximum loss happens when the stock price is the same to the strike price upon

expiration. Both the call and the put expire worthless, and the investor’s outlay

Chapter 15 – Options Markets

for the purchase of both options is lost: $7.00 + $8.50 = $15.50

8. Option c is the only correct statement.

a. The value of the short position in the put is –$4 if the stock price is $76.

9. a. i. A long straddle produces gains if prices move up or down and limited losses if

10. The initial outlay of this position is $38, the purchase price of the stock, and the payoff

of such position will be between two boundaries, $35 and $40.

a. The maximum profit will thus be: $40 – $38 = $2, and the maximum loss will

be: $35 – $38 = –$3.

b.

Chapter 15 – Options Markets

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

(Final value – Original investment) # of shares

= ($45 – $1) 5,000 = $220,000

Net proceeds without using collar = ST # of shares

= $50 5,000 = $250,000

d. With the initial outlay of $1, the collar locks the net proceeds per share in

between the lower bound of $34 and the upper bound of $44. Given 5,000

shares, the total net proceeds will be between $170,000 and $220,000 when the

position is closed. If we simply continued to hold the shares without using the

collar, the upside potential is not limited but the downside is not protected.

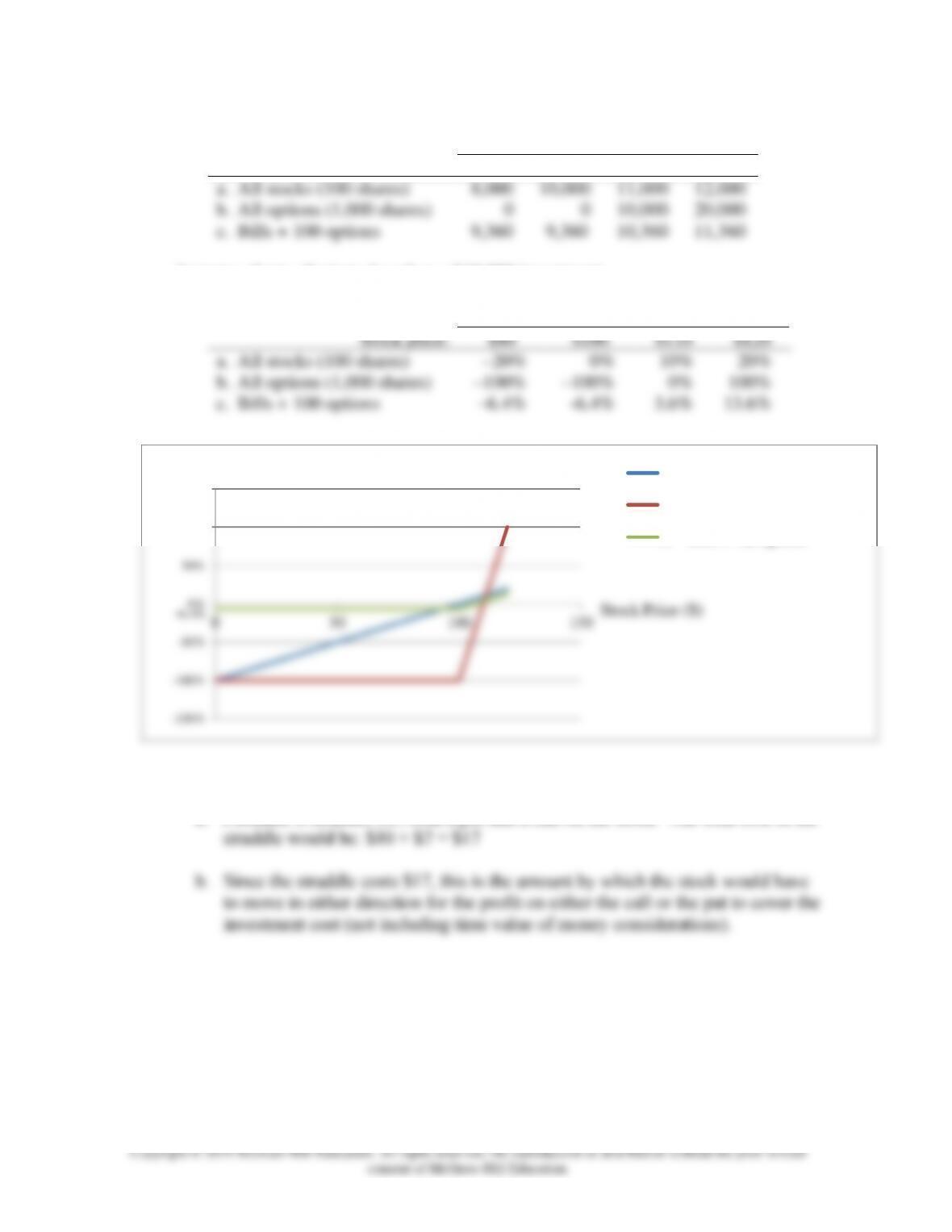

12. In terms of dollar returns:

Chapter 15 – Options Markets

Price of Stock Six Months from Now

Stock price:

$80

$100

$110

$120

a. All stocks (100 shares)

8,000

10,000

11,000

12,000

b. All options (1,000 shares)

0

0

10,000

20,000

c. Bills + 100 options

9,360

9,360

10,360

11,360

In terms of rate of return, based on a $10,000 investment:

Price of Stock Six Months from Now

Stock price:

$80

$100

$110

$120

a. All stocks (100 shares)

–20%

0%

10%

20%

b. All options (1,000 shares)

–100%

–100%

0%

100%

c. Bills + 100 options

–6.4%

-6.4%

3.6%

13.6%

13.

a. Purchase a straddle, i.e., both a put and a call on the stock. The total cost of the

14.

a. Sell a straddle, i.e., sell a call and a put to realize premium income of:

$4 + $7 = $11

-150%

-100%

-50%

0%

50%

100%

150%

050 100 150

a. All stocks (100 shares)

b. All options (1,000 shares)

c. Bills + 100 options

Rate of Return

Stock Price ($)

–6.4%

Chapter 15 – Options Markets

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

b. If the stock ends up at $50, both of the options will be worthless and the profit

will be $11. This is the maximum possible profit since, at any other stock price,

you will have to pay off on either the call or the put.

c. The stock price can move by $11 (your initial revenue from writing the two at–

the-money options) in either direction before your profits become negative.

d. Buy the call, sell (write) the put, lend the present value of $50. The payoff is as

follows:

Final Payoff

Position

Initial Outlay

ST < X

ST > X

Long call

C = 7

0

ST – 50

Short put

–P = –4

–(50 – ST)

0

Lending

50/(1 + r)(1/4)

50

50

Total

7 – 4 + [50/(1 + r)(1/4)]

ST

ST

e. The initial outlay equals: (the present value of $50) + $3

In either scenario, you end up with the same payoff as you would if you bought

the stock itself.

15. a. By writing covered call options, Jones receives premium income of $30,000. If,

in January, the price of the stock is less than or equal to $45, he will keep the

stock plus the premium income. Since the stock will be called away from him if

its price exceeds $45 per share, the most he can have is:

$450,000 + $30,000 = $480,000

Stock Price

PortfolioValue

Less than $45

(10,000 times stock price) + $30,000

Greater than $45

$450,000 + $30,000 = $480,000

b. By buying put options with a $35 strike price, Jones will be paying $30,000 in

premiums in order to insure a minimum level for the final value of his position.

That minimum value is: ($35 10,000) – $30,000 = $320,000

This strategy allows for upside gain, but exposes Jones to the possibility of a

moderate loss equal to the cost of the puts. The payoff structure is:

Chapter 15 – Options Markets

Stock Price

Portfolio Value

Less than $35

$350,000 – $30,000 = $320,000

Greater than $35

(10,000 times stock price) – $30,000

c. The net cost of the collar is zero. The value of the portfolio will be as follows:

Stock Price

Portfolio Value

Less than $35

$350,000

Between $35 and $45

10,000 times stock price

Greater than $45

$450,000

If the stock price is less than or equal to $35, then the collar preserves the

$350,000 in principal. If the price exceeds $45, then Jones gains up to a cap of

$450,000. In between $35 and $45, his proceeds equal 10,000 times the stock

price.

The best strategy in this case is (c) since it satisfies the two requirements of

preserving the $350,000 in principal while offering a chance of getting $450,000.

Strategy (a) should be ruled out because it leaves Jones exposed to the risk of

substantial loss of principal.

Our ranking is: (1) c (2) b (3) a

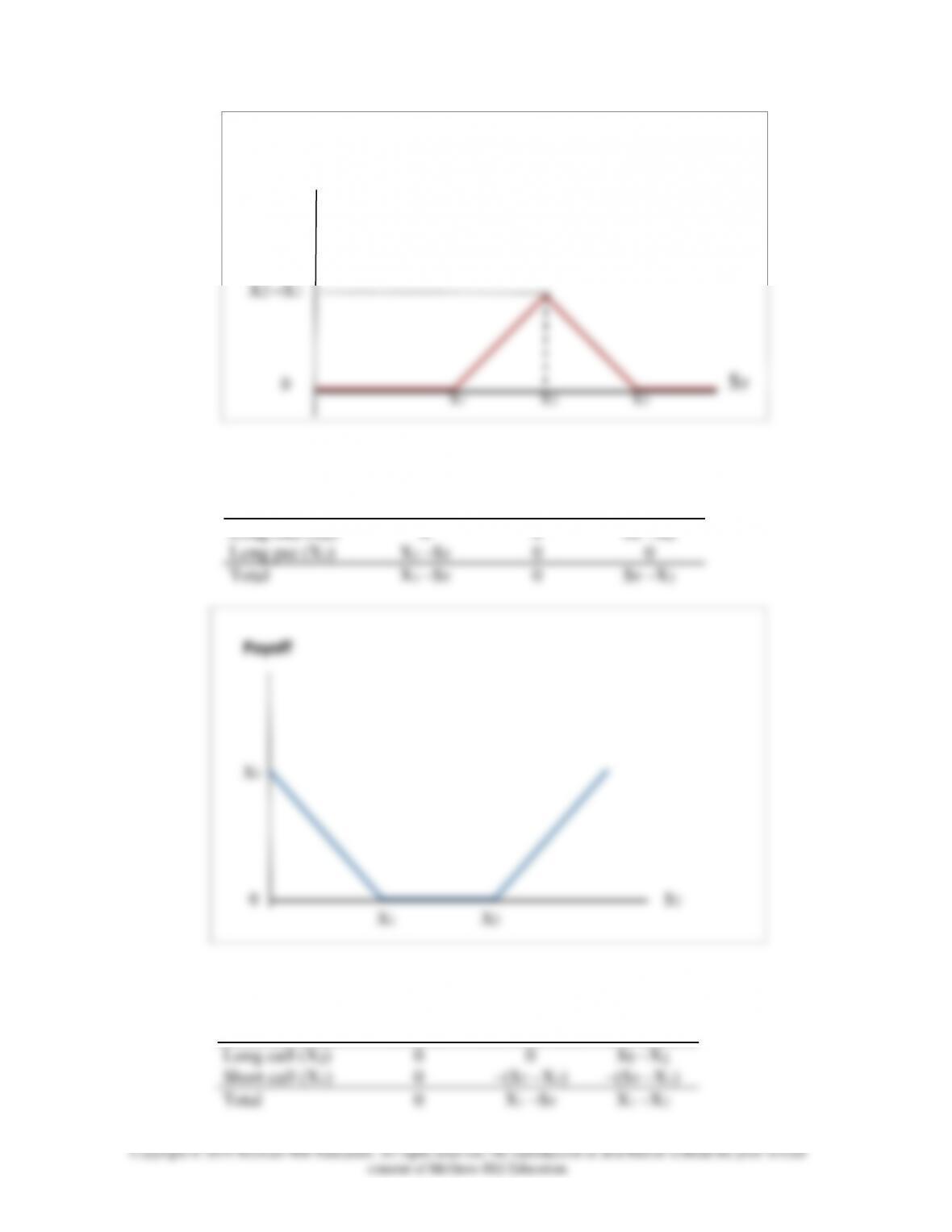

16.

a. Butterfly Spread

Position

ST < X1

X1 < ST < X2

X2 < ST < X3

X3 < ST

Long call (X1)

0

ST –X1

ST –X1

ST –X1

Short 2 calls (X2)

0

0

–2(ST –X2)

–2(ST –X2)

Long call (X3)

0

0

0

ST –X3

Total

0

ST –X1

2 X2 –X1 –ST

(X2–X1 ) – (X3–X2) = 0

Chapter 15 – Options Markets

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

b. Vertical combination

Position

ST < X1

X1 < ST < X2

ST > X2

Long call (X2)

0

0

ST –X2

Long put (X1)

X1 –ST

0

0

Total

X1 –ST

0

ST –X2

17. Bearish spread

Position

ST < X1

X1 < ST < X2

ST > X2

Long call (X2)

0

0

ST –X2

Short call (X1)

0

–(ST –X1)

–(ST –X1)

Total

0

X1 –ST

X1 –X2

Payoff

X2–X1

0

X1X2X3

ST

Chapter 15 – Options Markets

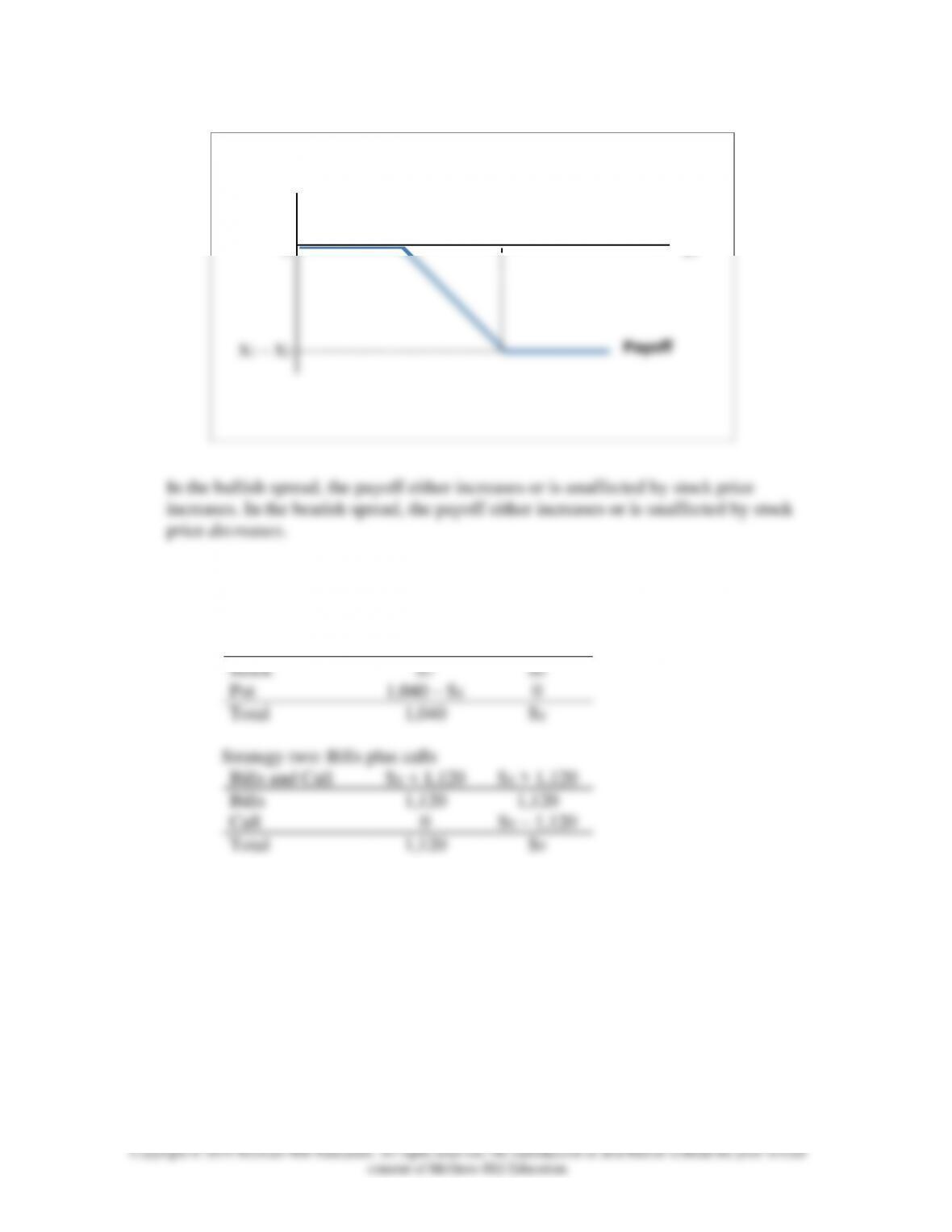

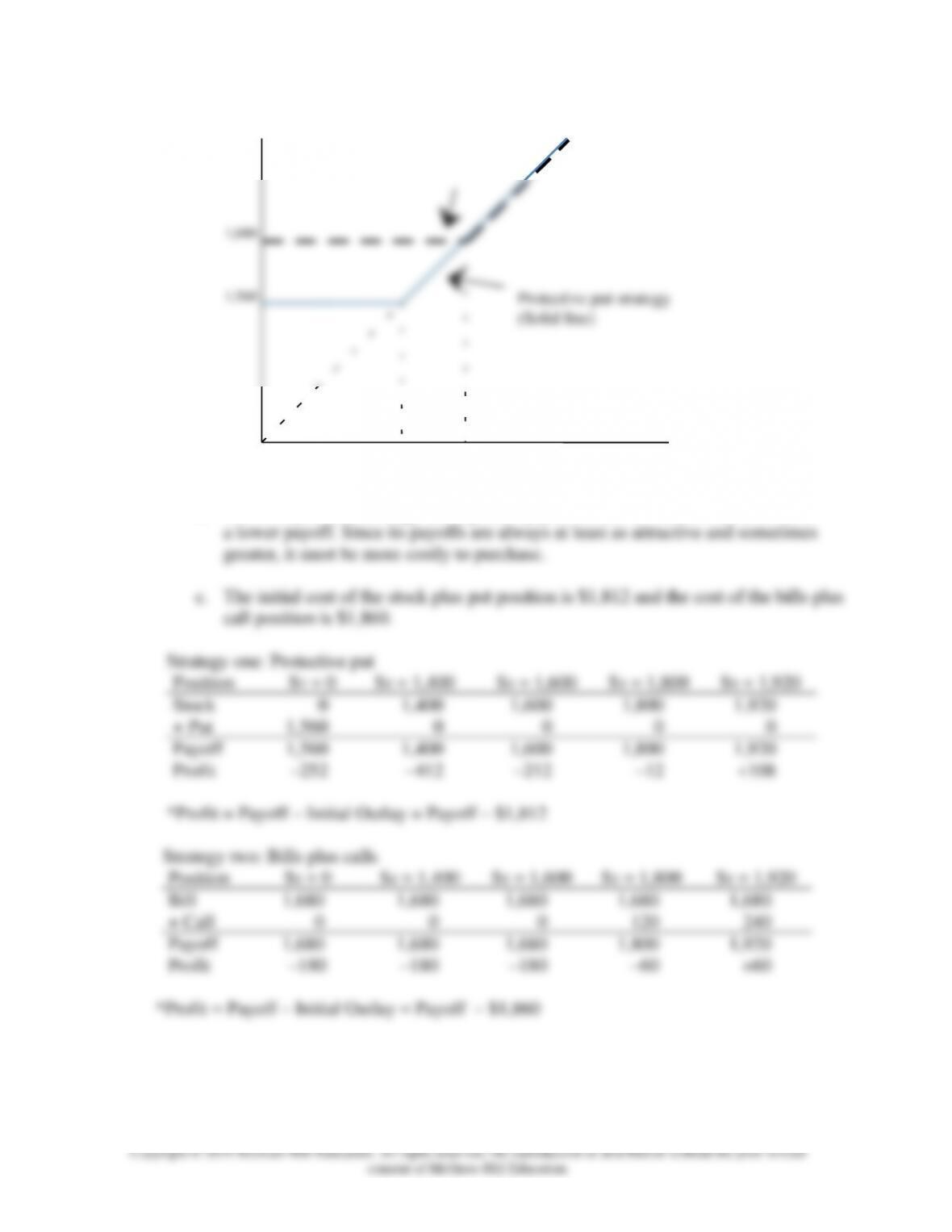

18. a. Strategy one: Protective put

Protective Put

ST < 1,040

ST > 1,040

Stock

ST

ST

Put

1,040 – ST

0

Total

1,040

ST

Strategy two: Bills plus calls

Bills and Call

ST < 1,120

ST > 1,120

Bills

1,120

1,120

Call

0

ST – 1,120

Total

1,120

ST

Payoff

0

X1–X2

X1

X2ST

Chapter 15 – Options Markets

Payoff

S

T

1,680

1,560

1,560

1,680

Bills plus calls

(Dashed line)

Protective put strategy

(Solid line)

0

b. The bills plus call strategy has a greater payoff for some values of ST and never

Chapter 15 – Options Markets

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Profit

Bills plus calls

Protective put

-180

-252

1,560

1,680

S

T

0

d. The stock and put strategy is riskier. It does worse when the market is down,

and better when the market is up. Therefore, its beta is higher.

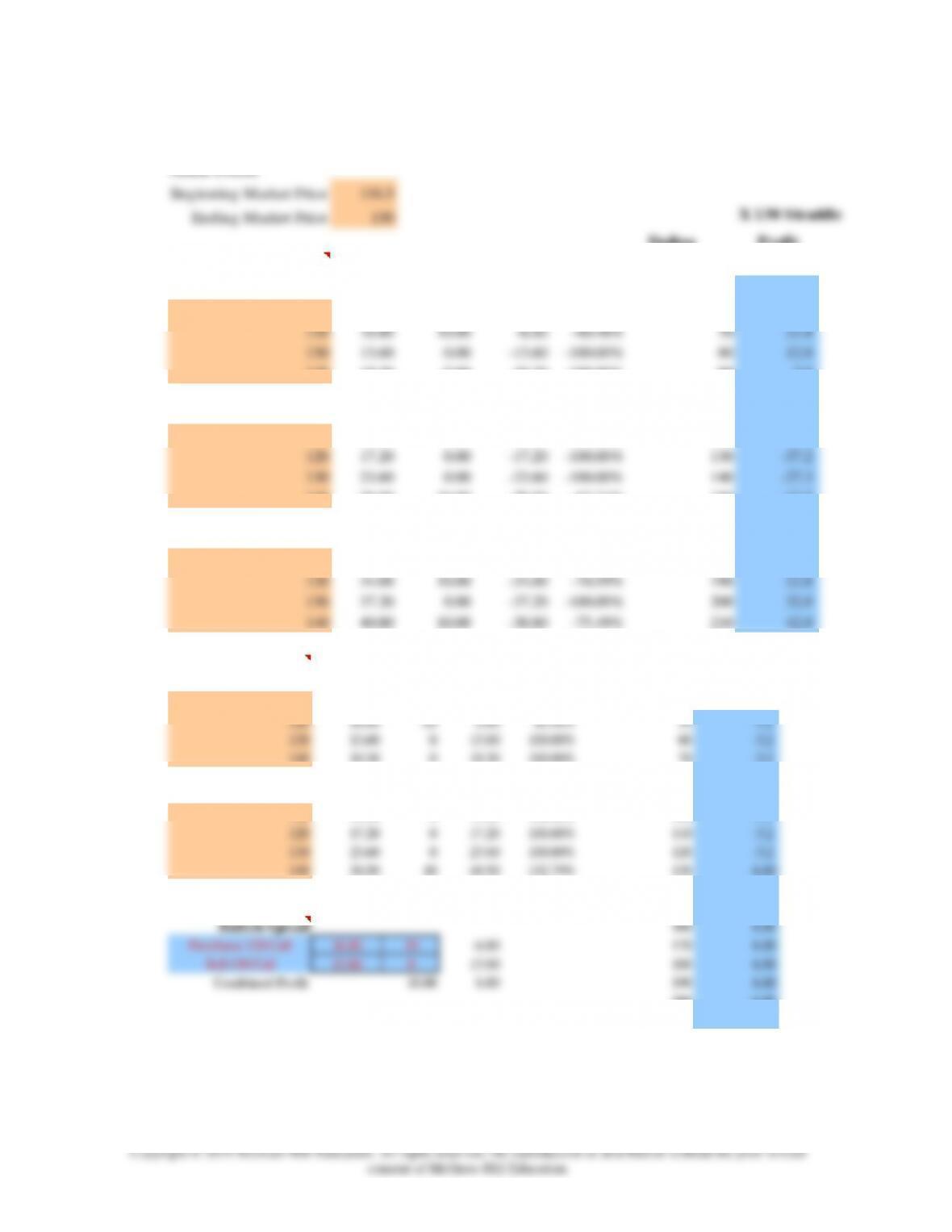

19. The Excel spreadsheet for both parts (a) and (b) is shown on the next page, and the

profit diagrams are on the following page.

Chapter 15 – Options Markets

a. & b.

Stock Prices

Beginning Market Price 116.5

Ending Market Price 130 X 130 Straddle

Ending Profit

Buying Options: Stock Price –37.20

Call Options Strike Price Payoff Profit Return % 50 42.8

110 22.80 20.00 –2.80 -12.28% 60 32.8

120 16.80 10.00 –6.80 -40.48% 70 22.8

130 13.60 0.00 –13.60 –100.00% 80 12.8

140 10.30 0.00 –10.30 –100.00% 90 2.8

100 –7.2

Put Options Strike Price Payoff Profit Return % 110 –17.2

110 12.60 0.00 –12.60 –100.00% 120 –27.2

120 17.20 0.00 –17.20 –100.00% 130 –37.2

130 23.60 0.00 –23.60 –100.00% 140 –27.2

140 30.50 10.00 –20.50 -67.21% 150 –17.2

160 –7.2

Straddle Price Payoff Profit Return % 170 2.8

110 35.40 20.00 –15.40 -43.50% 180 12.8

120 34.00 10.00 –24.00 -70.59% 190 22.8

130 37.20 0.00 –37.20 –100.00% 200 32.8

140 40.80 10.00 –30.80 -75.49% 210 42.8

Selling Options: Bullish

Call Options Strike Price Payoff Profit Return % Ending Spread

110 22.80 -20 2.80 12.28% Stock Price 6.80

120 16.80 -10 6.80 40.48% 50 -3.2

130 13.60 0 13.60 100.00% 60 –3.2

140 10.30 0 10.30 100.00% 70 –3.2

80 -3.2

120 17.20 0 17.20 100.00% 110 -3.2

130 23.60 0 23.60 100.00% 120 -3.2

140 30.50 10 40.50 132.79% 130 6.80

140 6.80

Money Spread Price Payoff Profit 150 6.80

Sell 130 Call 13.60 0 13.60 180 6.80

Combined Profit 10.00 6.80 190 6.80

200 6.80

210 6.80

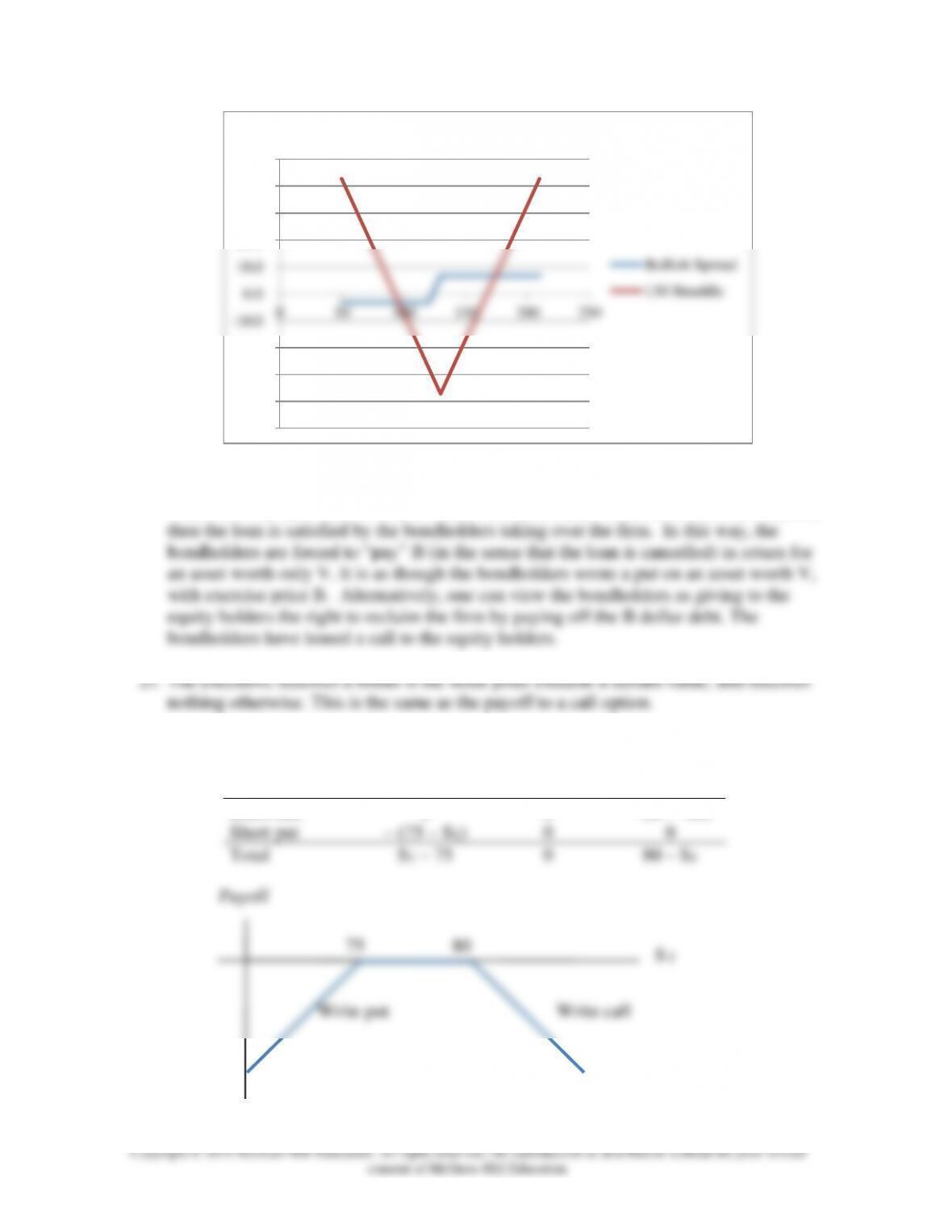

Chapter 15 – Options Markets

20. The bondholders have, in effect, made a loan which requires repayment of B dollars,

where B is the face value of bonds. If, however, the value of the firm (V) is less than B,

22. a.

Position

ST < 75

75 < ST < 80

ST > 80

Short call

0

0

– (ST – 80)

Short put

– (75 – ST)

0

0

Total

ST – 75

0

80 – ST

S

T

75

80

Payoff

Write call

Write put

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

050 100 150 200 250

Bullish Spread

130 Straddle

Spreads & Straddles

Chapter 15 – Options Markets

b. Proceeds from writing options (from Figure 15.1):

Call = $2.64

c. You will break even when either the short position in the put or the short

position in the call results in a cash outflow of $6.61. For the put, this requires

that:

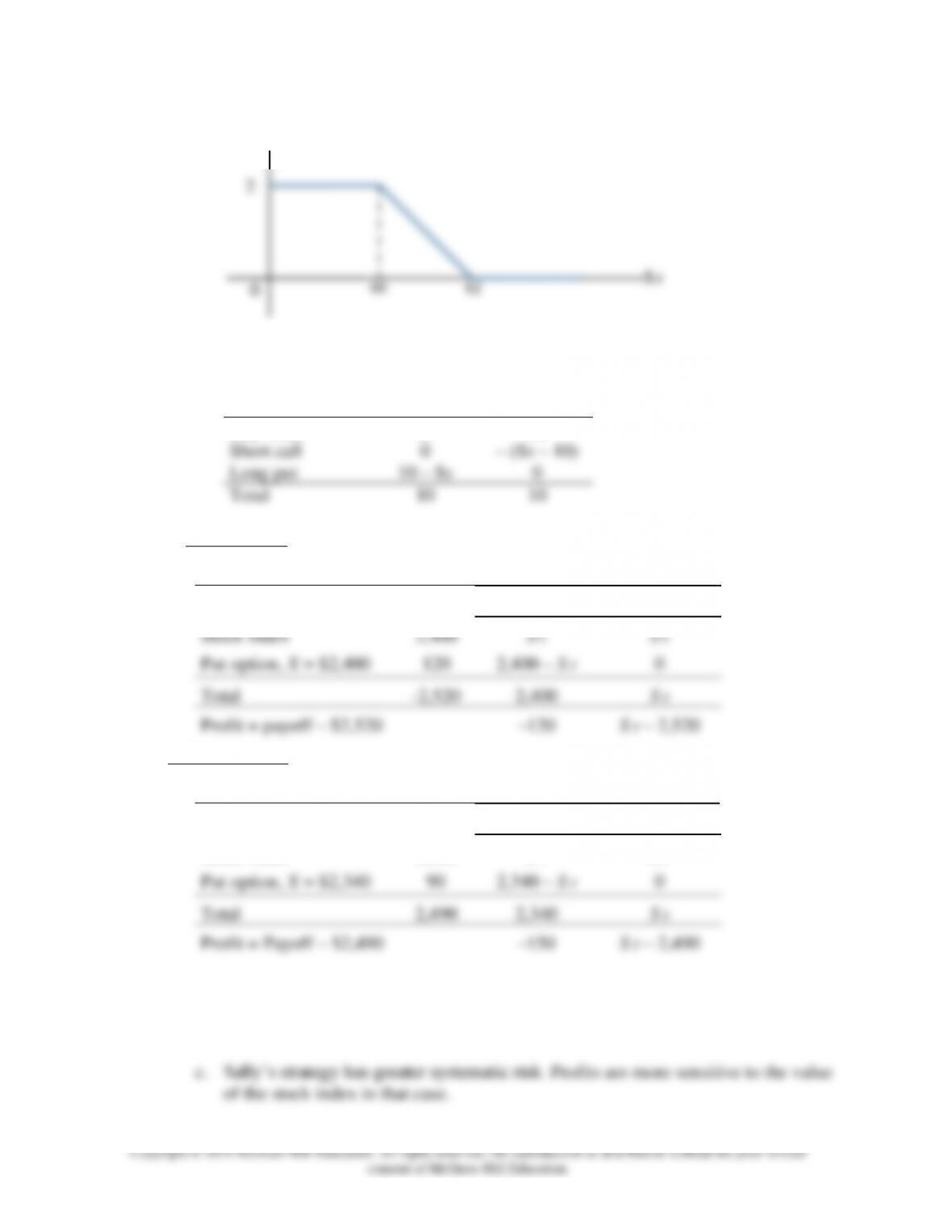

23. a.

S

T

0

5

Payoff

Profit

Net outlay

95

90

Value

24. Buy the X = 62 put (which should cost more than it does) and write the X = 60 put.

Since the options have the same price, the net outlay is zero. The proceeds at maturity

will be between 0 and 2 and will never be negative.

Position

ST < 60

60 < ST < 62

ST > 62

Long put (X = 62)

62 – ST

62 –ST

0

Short put (X = 60)

– (60 – ST)

0

0

Total

2

62 – ST

0

Chapter 15 – Options Markets

S

T

0

2

62

60

Payoff = Profit, because net outlay is 0.

25. This riskless strategy will yield a payoff of $10 for either position.. Therefore, the risk-

free rate is: ($10/$9.50) – 1 = .0526 = 5.26%

Position

ST < 10

ST > 10

Buy stock

ST

ST

Short call

0

– (ST – 10)

Long put

10 – ST

0

Total

10

10

26. a. Joe’s strategy

Position

Cost

Payoff

S T 2,400

S T > 2,400

Stock index

2,400

S T

S T

Put option, X = $2,400

120

2,400 – S T

0

Total

-2,520

2,400

S T

Profit = payoff – $2,520

–120

S T – 2,520

Sally’s strategy

Position

Cost

Payoff

S T 2,340

S T > 2,340

Stock index

2,400

S T

S T

Put option, X = $2,340

90

2,340 – S T

0

Total

2,490

2,340

S T

Profit = Payoff – $2,490

–150

S T – 2,490

b. Sally does better when the stock price is high, but worse when the stock price is

low.

Chapter 15 – Options Markets

27. The initial proceeds are: $9 – $3 = $6

a. The payoff is either negative or zero:

Position

ST < 50

50 < ST < 60

ST > 60

Long call (X = 60)

0

0

ST – 60

Short call (X = 50)

0

– (ST – 50)

– (ST – 50)

Total

0

– (ST – 50)

–10

b.

S

T

0

6

Payoff

Profit

-4

60

50

Value

-10

c. Breakeven occurs when the payoff offsets the initial proceeds of $6, which occurs

28. Buy a share of stock, write a call with X = 50, write a call with X = 60, and buy a call with

X = 110.

Position

ST < 50

50 < ST < 60

60 < ST < 110

ST > 110

Buy stock

ST

ST

ST

ST

Short call (X = 50)

0

– (ST – 50)

– (ST – 50)

– (ST – 50)

Short call (X = 60)

0

0

– (ST – 60)

– (ST – 60)

Long call (X = 110)

0

0

0

ST – 110

Total

ST

50

110 –ST

0

The investor is making a volatility bet. Profits will be highest when volatility is

low, such that if the stock price ends up in the interval between $50 and $60.

29. a. The farmer has the option to sell the crop to the government, for a guaranteed

minimum price, if the market price is too low.

Chapter 15 – Options Markets

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

c. If the supported price is denoted PS and the market price PM, then we can say

that the farmer has a put option to sell the crop (the asset) at an exercise price of

PS even if the market price of the underlying asset (PM) is less than PS.

CFA 1

Answer:

CFA 2

Answer:

a. Donie should choose the long strangle strategy. A long strangle option strategy

consists of buying a put and a call with the same expiration date and the same

underlying asset, but different exercise prices. In a strangle strategy, the call has

an exercise price above the stock price and the put has an exercise price below

b. i. The maximum possible loss per share is $9.00, which is the total cost of the

two options ($5.00 + $4.00).

CFA 3

Answer:

a. If an investor buys a call option and writes a put option on a T-bond, then, at

maturity, the total payoff to the position is (ST – X), where ST is the price of the

b. Such a position would increase the portfolio duration, just as adding a T-bond

Chapter 15 – Options Markets

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

established.

c. Futures can be bought and sold very cheaply and quickly. They give the manager

flexibility to pursue strategies or particular bonds that seem attractively priced

without worrying about the impact of these actions on portfolio duration. The

futures can be used to make adjustments to duration necessitated by other portfolio

actions.

CFA 4

Answer:

d. Conversion value of a convertible bond is the value of the security if it is

converted immediately. That is:

e. Market conversion price is the price that an investor effectively pays for the

common stock if the convertible bond is purchased:

CFA 5

Answer:

a. i. The current market conversion price is computed as follows:

ii. The expected one-year return for the Ytel convertible bond is:

iii. The expected one-year return for the Ytel common equity is:

b. The two components of a convertible bond’s value are:

• The straight bond value, which is the convertible bond’s value as a bond, and;

• The option value, which is the value associated with the potential conversion

into equity.

i. In response to the increase in Ytel’s common equity price, the straight bond value

should stay the same and the option value should increase.

Chapter 15 – Options Markets

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

The increase in equity price does not affect the straight bond value component of

the Ytel convertible. The increase in equity price increases the option value

component significantly, because the call option becomes deep “in the money”

when the $51 per share equity price is compared to the convertible’s conversion

price of: $1,000/25 = $40 per share.

ii. In response to the increase in interest rates, the straight bond value should

decrease and the option value should increase.

The increase in interest rates decreases the straight bond value component (bond

values decline as interest rates increase) of the convertible bond and increases the

value of the equity call option component (call option values increase as interest

rates increase). This increase may be small or even unnoticeable when compared to

the change in the option value resulting from the increase in the equity price.