Chapter 15 – Options Markets

CHAPTER FIFTEEN

OPTIONS MARKETS

CHAPTER OVERVIEW

This chapter describes characteristics of options, terminology used in the options’ markets,

option payoffs and profits to both option owners and sellers (called writers), and positions that

are comprised of combinations of options and stock or multiple option contracts. Option-like

assets, such as callable bonds, warrants, and collateralized loans are also described.

LEARNING OBJECTIVES

After studying this chapter, the student should be able to calculate potential profits resulting from

various option trading strategies and to formulate portfolio management strategies to modify the

risk-return attributes of the portfolio. The student should be able to identify the embedded

options in various assets and to determine how these option characteristics affect the prices of

these assets.

CHAPTER OUTLINE

1. The Option Contract

PPT 15-2 through PPT 15-9

A listed call option is a contract giving the holder the right to buy 100 shares of stock at a preset

price called the exercise or strike price. A listed put option is a contract giving the holder the

right to sell 100 shares of stock at a preset price. Expirations of 1,2,3,6, 9 months and sometimes

1 year are normal contract periods. Contracts expire on the Saturday following the third Friday

of the expiration month. Friday is the last day you can exercise. Contracts may be sold prior to

maturity. This is an important point. You don’t have to exercise to realize the value of the

option. In fact in most cases an option should be sold rather than exercised because exercising

forfeits the option’s time value (See Chapter 16). If a call option holder wishes to purchase the

stock, he or she will exercise the option. The option holder must pay the exercise price to the

American vs. European options

Chapter 15 – Options Markets

With an American style option the option can be exercised at any date after purchase whereas

with a European style option the option can only be exercised immediately before expiration

(only on the last Friday before expiration). Most options that are traded in this country are

American options. Foreign currency and stock index options that trade on the Chicago Board

Options Exchange are exceptions. European style options are cheaper, that is the motivation for

them. Note that the style (American vs. European) has nothing to do with where the options are

traded.

Options Uses

The OCC

The option exchanges operate the Option Clearing Corporation (OCC). An option buyer or

seller technically buys or sells from or to the OCC. The OCC backs performance of both

counterparties. This allows liquid anonymous trading to occur. To limit the OCC’s risk the

option seller (or writer) must post margin. The margin varies with option price and whether the

option position is covered or exposed. An in the money option requires more margin than an out

of the money option. Margin varies with the exposure of the option seller. A covered call writer

write a call on which they own stock. The writer can post the stock to satisfy the margin

requirement, whereas a naked call writer must post cash. When an option is exercised an option

seller is randomly selected. If a call is exercised the selected call writer must deliver 100 shares

of stock in exchange for receiving the strike price. If a put is exercised the selected put writer

must purchase 100 shares of stock at the strike price.

Options are available on a variety of financial assets including a host of interest rates products

and currencies. Index options are very popular instruments used in hedging. Options are also

available on other derivative instruments such as futures contracts. Most of the pricing and

payoff examples that are built in the text are stock options.

2. Values of Options at Expiration

PPT 15-10 through PPT 15-28

Chapter 15 – Options Markets

This section requires the use of some terminology:

Symbols & Valuation

Ct = Price paid for a call option at time t. t = 0 is today,

T = Immediately before the option’s expiration.

Pt = Price paid for a put option at time t.

St = Stock price at time t.

X = Exercise or Strike Price

A call is “in the money” if St > X. A put is “in the money” if St < X.

A call is “out of the money” if St < X. A put is “out of the money” if St > X.

An option is in the money if you could profitably exercise it right now. Basic option pricing

boundaries are developed below:

C and P are greater than zero because the holders have a choice to use them or not. A simple

arbitrage argument (shown above) can be used to demonstrate that the call price must be greater

than or equal to the difference between the stock price and the exercise price. This is the basis

for the price boundary of a call Ct ≥ Max (0, St – X).

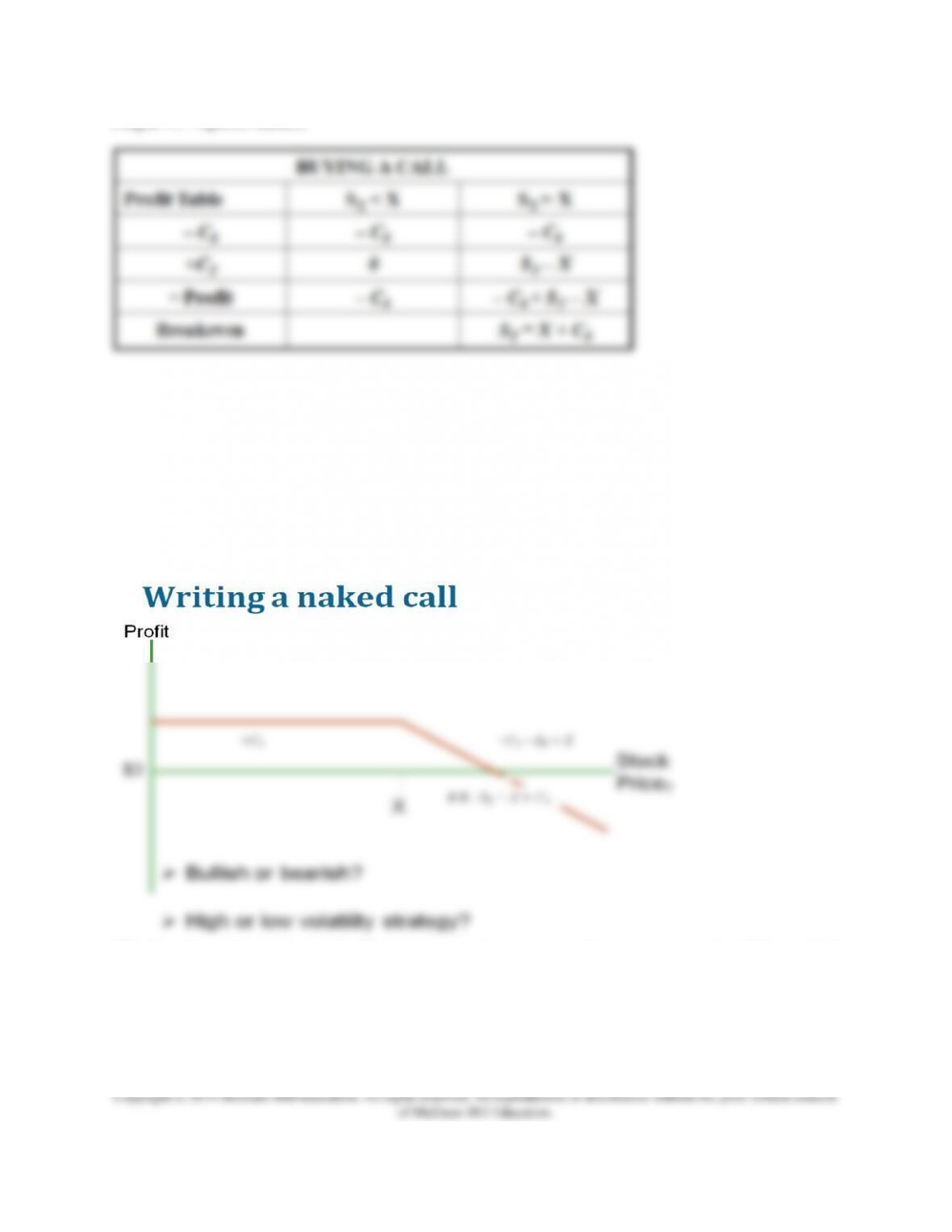

Constructing a profit table is an excellent method to model and understand the payoffs of any

option strategy and having students work though some of these tables is an excellent teaching

exercise. For example the profit at expiration of buying a call if ST < X is –C0, therefore profit is

a straight line at the level equal to –C0. If ST > X then profit = –C0 + ST – X. Since the horizontal

axis on the profit graph (see below) is ST and the profit equation in this region has a +1

coefficient, the profit diagram is a positive slope 45° line. See the profit table below:

Chapter 15 – Options Markets

Chapter 15 – Options Markets

The put writer has unlimited loss potential if the stock price falls. The profit for a put writer is

limited to a premium of the option. The text has an excellent boxed item entitled, “The Black

Hole: How Some Investors Lost All Their Money in the Market Crash.” The example of the risk

involved in writing naked puts surrounding the October 1987 Market Crash points out the

substantial risk in writing naked options. The profit graphs are based on the value of the option at

expiration.

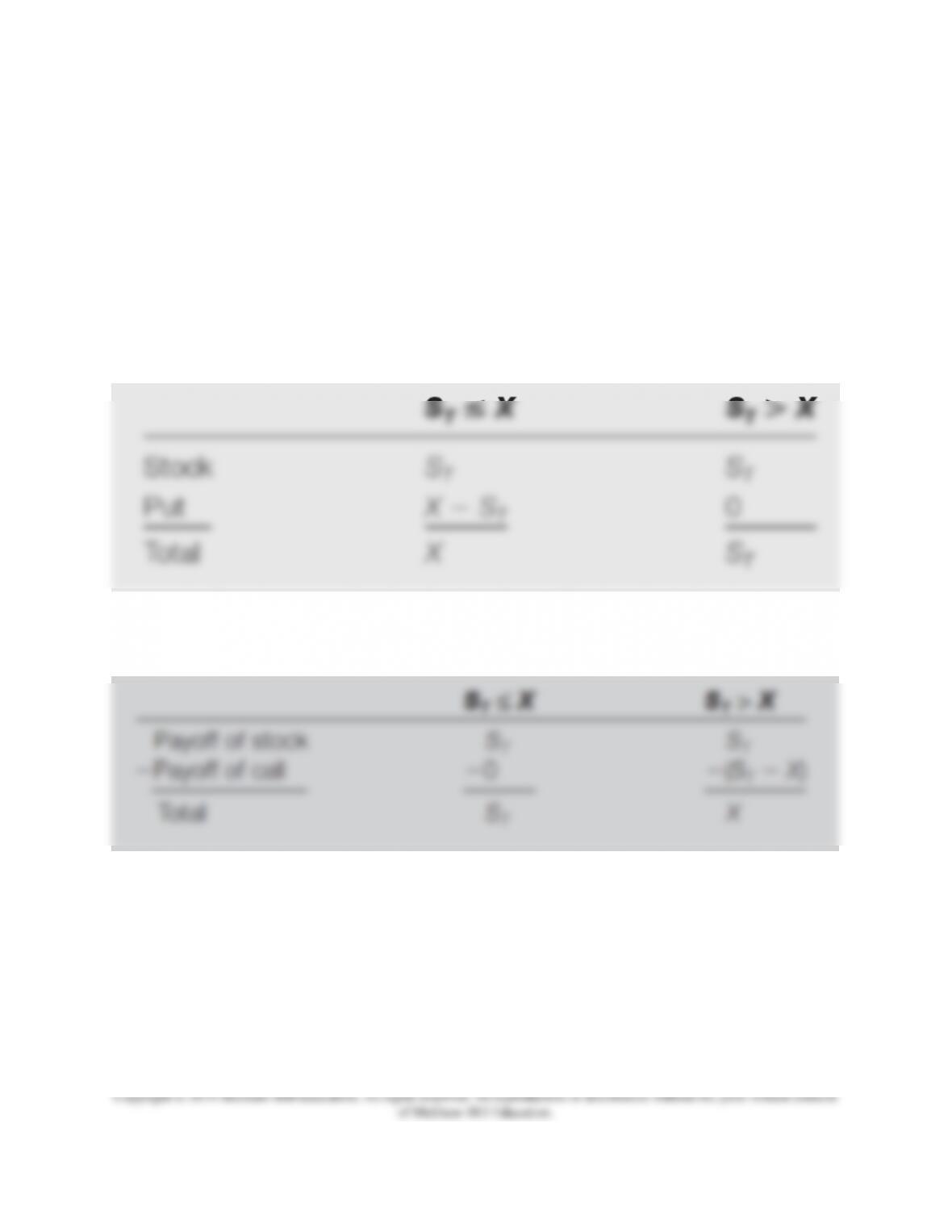

Some other strategies are illustrated in the PPT. A protective put involves the purchase of stock

and the purchase of puts on an equivalent number of shares. The strategy reduces upside

potential if the stock price rises by the cost of the put but it limits the loss if the stock declines in

price.

A covered call involves ownership of stock and writing a call option. It is referred to as covered

since the stock is owned if the option buyer exercised their option. The position has limited

upside potential and offers some protection to the owner of the stock if the stock price declines.

A straddle is constructed by purchasing a call and a put with the same exercise date and maturity

date. A straddle will result in profits if the stock price increases or decreases enough to

overcome the premiums for the options.

Chapter 15 – Options Markets

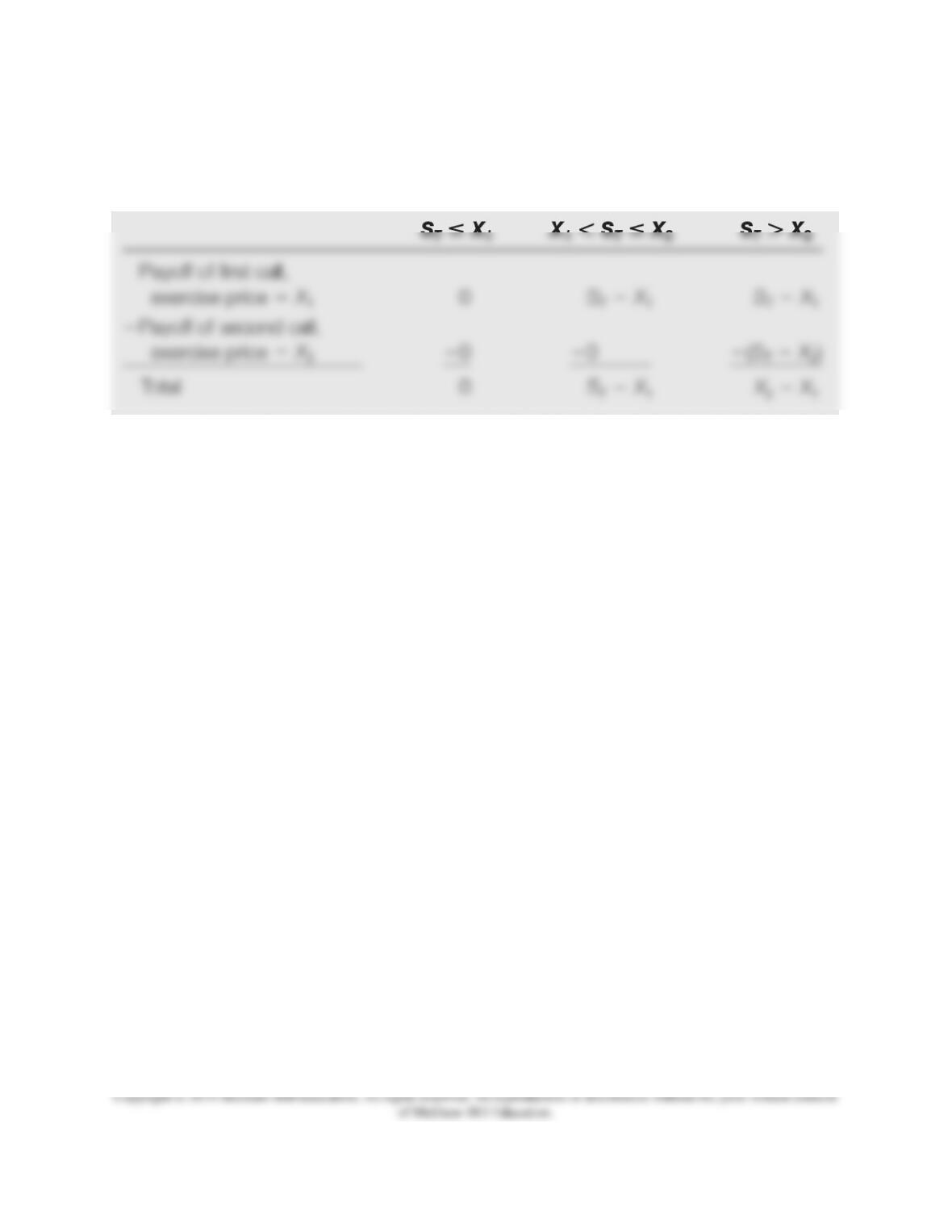

Bullish spreads allow an option investor to gain a limited amount of profit if the stock price rises

while also protecting the investor if the stock price declines.

A collar is an options strategy that brackets the value of a portfolio between two bounds and may

be appropriate for an investor who has a target wealth goal but is unwilling to risk losses beyond

a certain level.

Warnings about Option Strategies

Options may have to move 10-15% or more in a short time period before an investor recovers the

price & commission. Most options expire worthless. Options are by definition short term

instruments; an investor can ride out bad times in spot markets but not in options. The limited

loss feature makes options appear safer than they are. You have to compare equal dollar

investments in stocks and options to truly see the higher risk of the option position. Options are

traded in a highly competitive market and are priced according to expected volatility of the

underlying asset. To profit in options you must be able to forecast price or volatility better than

the competition and your gains must exceed your transactions costs. This is a tall order in a

competitive market. Many brokers and planners recommend writing covered calls to gain some

steady income, and most of the time the stock will not be called away from you. However, the

investor never gets the occasional large stock price run up and suffers most of the loss of a big

price drop. This strategy eliminates any positive skew of stock returns and is likely to leave the

investor with a portfolio of poorer performers. Writing naked calls (writing calls when you do

not own the stock) limits the writer’s gain to the call premium but exposes the writer to unlimited

loss, and this is a poor strategy in volatile markets.

Chapter 15 – Options Markets

3. Optionlike Securities

PPT 15-29 through PPT 15-35

Many securities are complex products that include imbedded options. The payoffs and profits

associated with securities that contain imbedded options will present payoffs that are similar to

options or groups of options. Examples that demonstrate the impact of embedded options include

callable bonds, convertible bonds, collateralized loans and levered equity and these are covered

in the PPT. The discussion of convertible bonds is particularly important because students

routinely think that convertible bonds are a good deal that combine the safety of a bond with the

upside potential of equity. There is no free lunch (other than diversification) in finance. When

issued the convertible option is out of the money and investors must accept a lower yield rate to

get it. Often stock prices will have to increase 20% to 25% before conversion becomes

profitable. Virtually all convertibles are callable as well. The issuing firm may call the bond

when it is profitable to convert in order to ‘force’ conversion. This may shorten the expected

maturity of the bond.

4. Exotic Options

PPT 15-36

Discussion of these options is useful in making students aware of the all the various types of

options that are available to construct different desired payoffs. Asian- Payoffs depend on the

average (rather than the final) price of the underlying asset during a portion of the life of the

option. Barrier Options’ value depends on whether the underlying asset price has passed through

some barrier during the life of the option. For example “down-and-out” options expire worthless

if the stock price drops below a specified barrier. A lookback option payoff depends on the

minimum or maximum price during life of option. Currency Translated Options allow a variable

amount of foreign currency based on the performance of an investment to be translated to dollars

at a fixed exchange rate. Digital options pay a fixed amount if the option is in the money

regardless of how far in the money the option goes. Digital options are being used to make bets

on economic data such as the number of jobless claims or inflation.

Excel Applications

Chapter 15 – Options Markets

There are two spreadsheet applications available on the web site. The first one allows the

students to examine the changes in profitability and rates of return for an example that is similar

to the example in the text. The spreadsheet can be modified to allow for different combinations

of options, lending and levels of stock ownership. The second spreadsheet allows students to

examine the changes in payoffs and rates of returns for various spread and straddle strategies.