Chapter 11 – Managing Bond Portfolios

CHAPTER 11

MANAGING BOND PORTFOLIOS

1. Duration can be thought of as a weighted average of the ‘maturities’ of the cash flows

paid to holders of the perpetuity, where the weight for each cash flow is equal to the

2. A zero coupon, long maturity bond will have the highest duration and will, therefore,

produce the largest price change when interest rates change.

3.

a. Engage in active bond management, specifically bond swaps

4. Change in Price = – (Modified Duration Change in YTM) Price

5. d. None of the above.

6. The increase will be larger than the decrease in price.

7. While it is true that short-term rates are more volatile than long-term rates, the longer

8. When YTM = 6%, the duration is 2.8334.

Chapter 11 – Managing Bond Portfolios

(1)

(2)

(3)

(4)

(5)

Time until

Payment

(Years)

Payment

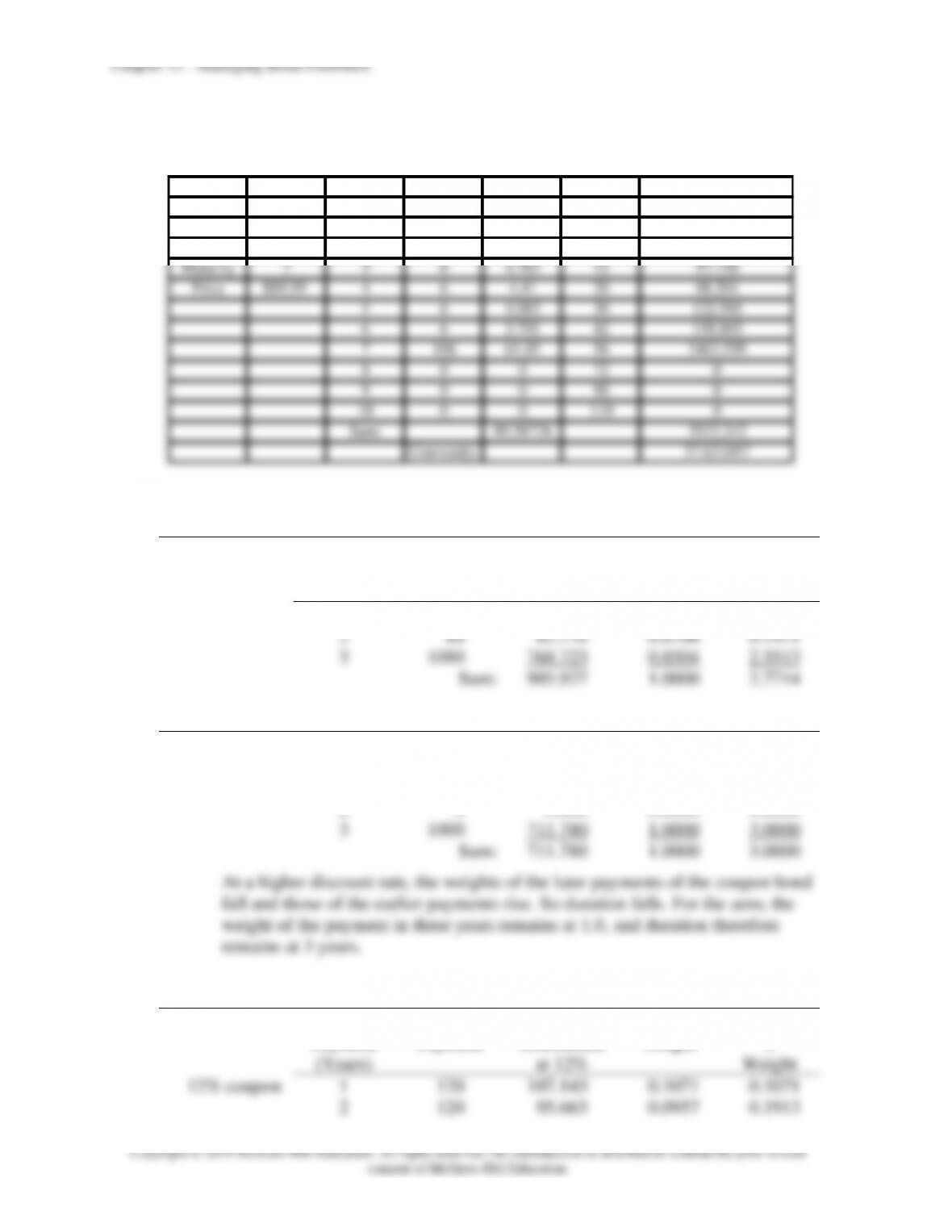

Payment

Discounted at

6%

Weight

Column (1)

×

Column (4)

1

60

56.60

0.0566

0.0566

2

60

53.40

0.0534

0.1068

3

1060

890.00

0.8900

2.6700

Column Sum:

1000.00

1.0000

2.8334

When YTM = 10%, the duration is 2.8238

(1)

(2)

(3)

(4)

(5)

Time until

Payment

(Years)

Payment

Payment

Discounted at

10%

Weight

Column (1)

×

Column (4)

1

60

54.55

0.0606

0.0606

2

60

49.59

0.0551

0.1101

3

1060

796.39

0.8844

2.6531

Column Sum:

900.53

1.0000

2.8238

When the yield to maturity increases, the duration decreases.

9. Using Equation 11.2, the percentage change in the bond price is:

P

P

10.1

0050.0

1−=−=

+

y

y

10. The computation of duration is as follows:

Interest Rate (YTM) is 10%.

(1)

(2)

(3)

(4)

(5)

Time until

Payment

(Years)

Payment

(in millions

of dollars)

Payment

Discounted

At 10%

Weight

Column (1)

×

Column (4)

1

1

0.9091

0.2744

0.2744

2

2

1.6529

0.4989

0.9977

3

1

0.7513

0.2267

0.6803

Column Sum:

3.3133

1.0000

1.9524

Duration = 1.9524 years

11. The duration of the perpetuity is: (1 + y)/y = 1.10/0.10 = 11 years

Let w be the weight of the zero-coupon bond. Then we find w by solving:

12. Using Equation 11.2, the percentage change in the bond price will be:

P

P

08.1

0010.0

y1

y=

−

+

13. a. Bond B has a higher yield to maturity than bond A since its coupon payments and

maturity are equal to those of A, while its price is lower. (Perhaps the yield is

higher because of differences in credit risk.) Therefore, the duration of Bond B

b. Bond A has a lower yield and a lower coupon, both of which cause it to have a

14. Choose the longer-duration bond to benefit from a rate decrease.

a. The Aaa-rated bond has the lower yield to maturity and therefore the longer

duration.

b. The lower-coupon bond has the longer duration and more de facto call protection.

15.

a. The present value of the obligation is $17,832.65 and the duration is 1.4808 years,

as shown in the following table:

Computation of duration, interest rate = 8%

(1)

(2)

(3)

(4)

(5)

Time until

Payment

(Years)

Payment

Payment

Discounted

at 8%

Weight

Column (1)

×

Column (4)

1

10,000

9,259.26

0.5192

0.51923

2

10,000

8,573.39

0.4808

0.96154

Column Sum:

17,832.65

1.0000

1.48077

b. To immunize the obligation, invest in a zero-coupon bond maturing in 1.4808 years.

Since the present value of the zero-coupon bond must be $17,832.65, the face value

Chapter 11 – Managing Bond Portfolios

c. If the interest rate increases to 9%, the zero-coupon bond would fall in value to:

26.985,19$

d. If the interest rate falls to 7%, the zero-coupon bond would rise in value to:

26.985,19$

16. a. PV of obligation = $2 million/0.16 = $12.5 million

Duration of obligation = 1.16/0.16 = 7.25 years

Call w the weight on the five-year maturity bond (with duration of 4 years). Then:

b. The price of the 20-year bond is:

[60 Annuity factor(16%, 20)] + [1000 PV factor(16%, 20)] = $407.1

Therefore, the bond sells for 0.4071 times its par value, so that:

17. a. Shorten his portfolio duration to decrease the sensitivity to the expected rate increase.

Chapter 11 – Managing Bond Portfolios

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

18. Change in price = – (Modified duration Change in YTM) Price

= – 3.5851 0.01 $100

= – $3.5851

The price will decrease by $3.59.

19. a. The duration of the perpetuity is: 1.05/0.05 = 21 years

Let w be the weight of the zero-coupon bond, so that we find w by solving:

(w 5) + [(1 – w) 21] = 10 w = 11/16 = 0.6875

20. Macaulay Duration and Modified Duration are calculated using Excel as follows:

Inputs

Formula in column B

Settlement date

5/27/2018

=DATE(2018,5,27)

Maturity date

11/15/2028

=DATE(2027,11,15)

Coupon rate

0.07

0.07

Yield to maturity

0.08

0.08

Coupons per year

2

2

Outputs

Macaulay Duration

6.9659

=DURATION(B2,B3,B4,B5,B6)

Modified Duration

6.6980

=MDURATION(B2,B3,B4,B5,B6)

21. Macaulay Duration and Modified Duration are calculated using Excel as follows:

Inputs

Formula in column B

Settlement date

5/27/2018

=DATE(2018,5,27)

Maturity date

11/15/2027

=DATE(2027,11,15)

Coupon rate

0.07

0.07

Yield to maturity

0.08

0.08

Coupons per year

1

1

Outputs

Macaulay Duration

6.8844

=DURATION(B2,B3,B4,B5,B6)

Modified Duration

6.3745

=MDURATION(B2,B3,B4,B5,B6)

Chapter 11 – Managing Bond Portfolios

Generally, we would expect duration to increase when the frequency of payment

decreases from two payments per year to one payment per year because more of the

bond’s payments are made further in to the future when payments are made annually.

22. a. The duration of the perpetuity is: 1.10/0.10 = 11 years

The present value of the payments is: $1 million/0.10 = $10 million

Let w be the weight of the five-year zero-coupon bond and therefore (1 – w) is

the weight of the twenty-year zero-coupon bond. Then we find w by solving:

(w 5) + [(1 – w) 20] = 11 w = 9/15 = 0.60

23. Convexity is calculated using the Excel spreadsheet below:

Time (t) Cash flow PV(CF) t + t^2 (t + t^2) x PV(CF)

Coupon 6 1 6 5.556 2 11.111

YTM 0.08 2 6 5.144 6 30.864

Maturity 7 3 6 4.763 12 57.156

Price $89.59 4 6 4.41 20 88.204

5 6 4.083 30 122.505

6 6 3.781 42 158.803

7106 61.85 56 3463.599

8 0 0 72 0

9 0 0 90 0

10 0 0 110 0

Sum: 89.58726 3932.242

Convexity: 37.631057

24. a. Interest rate = 12%

Time until

Payment

(Years)

Payment

Payment

Discounted

at 12%

Weight

Time

×

Weight

8% coupon

1

80

71.429

0.0790

0.0790

2

80

63.776

0.0706

0.1411

3

1080

768.723

0.8504

2.5513

Sum:

903.927

1.0000

2.7714

Zero-coupon

1

0

0.000

0.0000

0.0000

2

0

0.000

0.0000

0.0000

3

1000

711.780

1.0000

3.0000

Sum:

711.780

1.0000

3.0000

b. Continue to use a yield to maturity of 12%:

Time until

Payment

(Years)

Payment

Payment

Discounted

at 12%

Weight

Time

×

Weight

12% coupon

1

120

107.143

0.1071

0.1071

2

120

95.663

0.0957

0.1913

Chapter 11 – Managing Bond Portfolios

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

3

1120

797.194

0.7972

2.3916

Sum:

1000.000

1.0000

2.6901

The weights of the earlier payments are higher when the coupon increases.

Therefore, duration falls.

25.

a.

A B C D E F G

1Time (t) Cash flow PV(CF) t + t^2 (t + t^2) x PV(CF)

2 Coupon 80 180 72.727273 2 145.4545455

3YTM 0.1 280 66.115702 6 396.6942149

4Maturity 3 31080 811.420 12 9737.040

5Price $950.263 Sum 950.263 10279.189

6

7 Convexity: 8.939838

=G5/(E5*(1+B2)^2)

b.

A B C D E F G

1Time (t) Cash flow PV(CF) t + t^2 (t + t^2) x PV(CF)

2YTM 0.1 1 0 0 2 0

3Maturity 3 2 0 0 6 0

4Price $751.315 31000 751.315 12 9015.778

5 Sum 751.315 9015.778

6

7 Convexity: 9.917355

=G5/(E5*(1+B2)^2)

26.

a. Using a financial calculator, we find that the price of the bond is:

For yield to maturity of 7%: $1,620.45

b. Using the duration rule, assuming yield to maturity falls to 7%:

y

c. Using the duration-with-convexity rule, assuming yield to maturity falls to 7%:

Chapter 11 – Managing Bond Portfolios

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Predicted price change = [−Duration × ∆y

1 + y + (0.5 × Convexity × (∆y)2)] P0

= [(−11.54 × -0.01

1.08 )+ (0.5 × 192.4 × (−0.01)2)] $1,450.31 = $168.92

Therefore: Predicted price = $168.92 + $1,450.31 = $1,619.23

d. The actual price at a 7% yield to maturity is $1,620.45. Therefore:

28.605,1$45.620,1$ ==

−

45.620,1$

Conclusion: The duration-with-convexity rule provides more accurate

approximations to the actual change in price. In this example, the percentage

error using convexity with duration is less than one-tenth the error using

duration only to estimate the price change.

e. For yield to maturity of 9%, the price of the bond is $1,308.21

Using the duration rule, assuming yield to maturity increases to 9%:

Predicted price change = – Duration

0

P

y1

y

+

97.154$31.450,1$

08.1

01.0 −=

+

21.308,1$

Using the duration-with-convexity rule, assuming yield to maturity rises to 9%:

Predicted price change =

Chapter 11 – Managing Bond Portfolios

Therefore: Predicted price = –$141.02 + $1,450.31 = $1,309.29

21.308,1$

21.308,1$29.309,1$ ==

−

Conclusion: Similar to the decrease in YTM, using the duration-with-convexity

rule for the increase in YTM predicts a more fine-tuned estimate of price than the

duration rule alone.

27. You should buy the three-year bond because it will offer a 9% holding-period return

over the next year, which is greater than the return on either of the other bonds, as

shown below:

Maturity One year Two years Three years

YTM at beginning of year 7.00% 8.00% 9.00%

Beginning of year price $1,009.35 $1,000.00 $974.69

End of year price (at 9% YTM) $1,000.00 $990.83 $982.41

Capital gain −$ 9.35 −$ 9.17 $7.72

Coupon $80.00 $80.00 $80.00

One year total $ return $70.65 $70.83 $87.72

One year total rate of return 7.00% 7.08% 9.00%

28.

a. The maturity of the 30-year bond will fall to 25 years, and the yield is forecast to

be 8%. Therefore, the price forecast for the bond is:

$893.25 [n = 25; i = 8; FV = 1,000; PMT = 70]

Therefore, total proceeds will be:

$394.60 + $893.25 = $1,287.85

b. The maturity of the 20-year bond will fall to 15 years, and its yield is forecast to be

7.5%. Therefore, the price forecast for the bond is:

$911.73 [n = 15; i = 7.5; FV = 1000; PMT = 65]

Chapter 11 – Managing Bond Portfolios

Therefore, total proceeds will be:

29.

a. Using a financial calculator, we find that the price of the zero-coupon bond

(with $1000 face value) is:

The price of the 6% coupon bond is:

i. Zero Coupon Bond

84.374$28.333$−=

−

Chapter 11 – Managing Bond Portfolios

b. Now assume yield to maturity falls to 7%. The price of the zero increases to

$422.04, and the price of the coupon bond increases to $875.91.

Zero Coupon Bond

84.374$04.422$=

−

Chapter 11 – Managing Bond Portfolios

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

B: Lower yield to maturity than bond E

E: Highest coupon, shortest maturity, highest yield of all bonds

CFA 2 Answer:

a. Modified duration =

YTM1

durationMacaulay

+

CFA 3

Answer:

a. Scenario (i): Strong economic recovery with rising inflation expectations.

Interest rates and bond yields will most likely rise, and the prices of both bonds

will fall. The probability that the callable bond will be called declines, so that it

b. If yield to maturity (YTM) on Bond B falls by 75 basis points:

Chapter 11 – Managing Bond Portfolios

c. For Bond A (the callable bond), bond life and therefore bond cash flows are

uncertain. If one ignores the call feature and analyzes the bond on a “to maturity”

basis, all calculations for yield and duration are distorted. Durations are too long

CFA 4

Answer:

a. The Aa bond initially has the higher yield to maturity (yield spread of 40 b.p.

versus 31 b.p.), but the Aa bond is expected to have a widening spread relative

b. Other variables that one should consider:

• Potential changes in issue-specific credit quality: If the credit quality of the

bonds changes, spreads relative to Treasuries will also change.

CFA 5 Answer:

Chapter 11 – Managing Bond Portfolios

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

25-year maturity: ∆P/P = −23.81 × 0.50% = −11.9050%

Strategy I: ∆P/P = (0.5 × 3.6225%) + [0.5 × (−11.9050%)] = −4.1413%

For Strategy II:

15-year maturity: ∆P/P = −14.35 × 0.25% = −3.5875%

CFA 6

Answer:

a. For an option-free bond, the effective duration and modified duration are

approximately the same. The duration of the bond described in Table 22A is

calculated as follows:

Modified Duration = – ∆P/(P × ∆y)

b. The total percentage price change for the bond described in Table 22A is

estimated as follows:

CFA 7

Answer:

CFA 8

Answer:

a. The two risks are price risk and reinvestment rate risk. The former refers to

bond price volatility as interest rates fluctuate, the latter to uncertainty in the

rate at which coupon income can be reinvested.

b. Immunization is the process of structuring a bond portfolio in such a manner that

the value of the portfolio (including proceeds reinvested) will reach a given target

Chapter 11 – Managing Bond Portfolios

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

c. Duration matching is superior to maturity matching because bonds of equal

duration — not those of equal maturity — are equally sensitive to interest rate

fluctuations.

CFA 9

Answer:

The economic climate is one of impending interest rate increases. Hence, we will want

to shorten portfolio duration.

a. Choose the short maturity (2019) bond.

b. The Arizona bond likely has lower duration. Coupons are about equal, but the

CFA 10

Answer:

a. (4) A low coupon and a long maturity

CFA 11

Answer:

a. A manager who believes that the level of interest rates will change should

engage in a rate anticipation swap, lengthening duration if rates are expected to

fall, and shortening duration if rates are expected to rise.

b. A change in yield spreads across sectors would call for an inter-market spread

Chapter 11 – Managing Bond Portfolios

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

c. A belief that the yield spread on a particular instrument will change calls for a

substitution swap in which that security is sold if its relative yield is expected to rise

or is bought if its yield is expected to fall compared to other similar bonds.

CFA 12

Answer:

a. This swap would have been made if the investor anticipated a decline in long-term

interest rates and an increase in long-term bond prices. The deeper discount, lower

coupon 2⅜% bond would provide more opportunity for capital gains, greater call

protection, and greater protection against declining reinvestment rates at a cost of

only a modest drop in yield.

b. This swap was probably done by an investor who believed the 24 basis point yield

c. This swap would have been made if the investor were bearish on the bond market.

The zero coupon note would be extremely vulnerable to an increase in interest rates

since the yield to maturity, determined by the discount at the time of purchase, is

locked in. This is in contrast to the floating rate note, for which interest is adjusted

periodically to reflect current returns on debt instruments. The funds received in

interest income on the floating rate notes could be used at a later time to purchase

long-term bonds at more attractive yields.

Chapter 11 – Managing Bond Portfolios

Copyright © 2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

First, that the appreciation potential of the Z mart convertible, based primarily

on the intrinsic value of Z mart common stock, was no longer as attractive as it

had been.

Second, that the yields on long-term bonds were at a cyclical high, causing bond

portfolio managers who could take A2-risk bonds to reach for high yields and long

maturities, either to lock them in or take a capital gain when rates subsequently

declined.

Third, while waiting for rates to decline, the investor will enjoy an increase in

coupon income. Basically, the investor is swapping an equity-equivalent for a long-

term corporate bond.