Solutions to Questions – Chapter 9

Income-Producing Properties: Leases, Rents, and the Market for Space

Question 9-1

How does the use of leases shift the risk of rising operating expenses from lessor to the lessee?

Question 9-2

What is the difference between base rents and effective rents?

Question 9-3

What is meant by usable vs. rentable space?

Question 9-4

What are CAM charges?

Question 9-5

What are (a) pass through expenses, (b) recoverable expenses, (c) common area expenses? Give examples of each.

Question 9-6

What is an estoppel? Why is it used?

Question 9-7

What is meant by “loss to lease”?

Question 9-8

Adjustment:

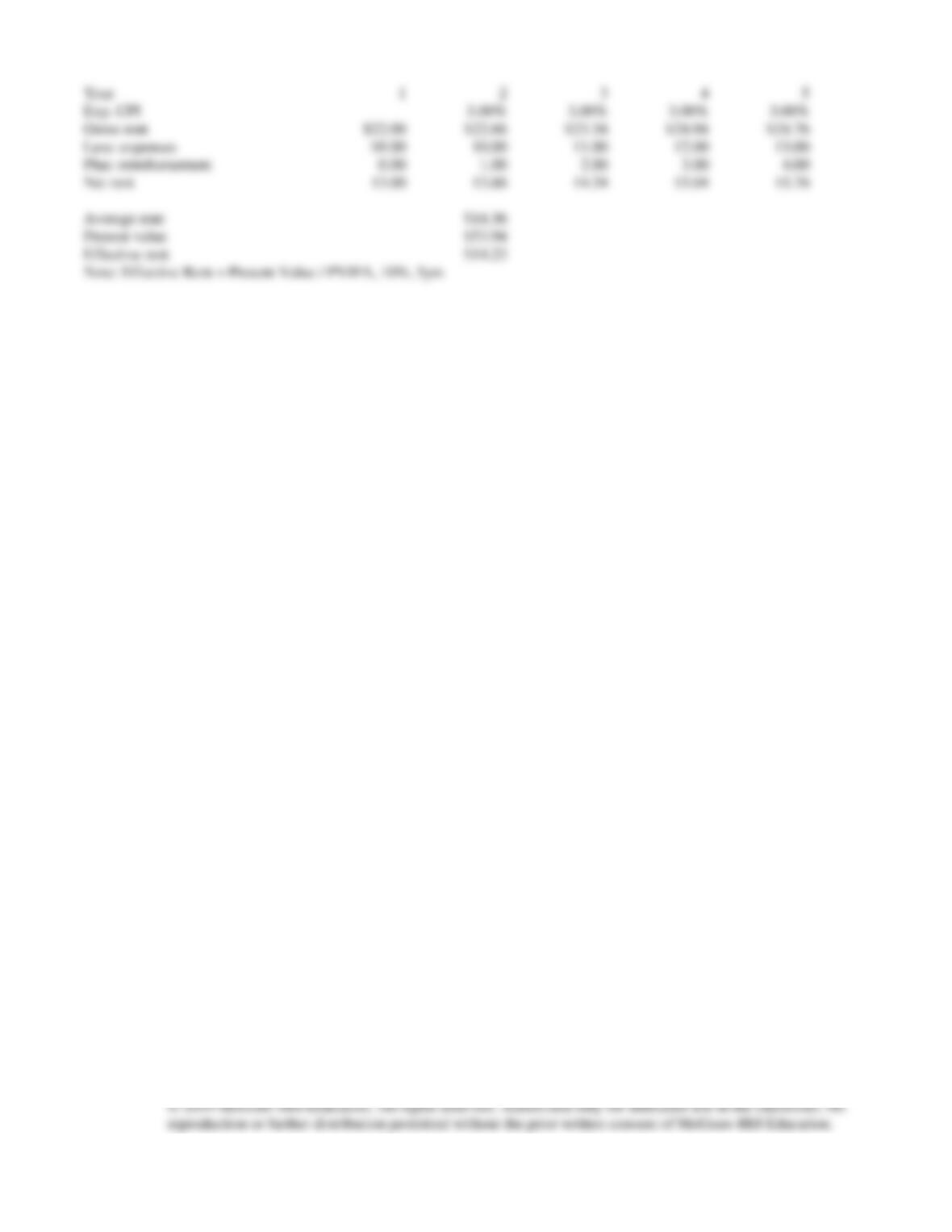

Year

1

2

3

4

5

Exp. CPI

Net Rent

$16.00

16.48

16.97

17.48

18.01

Average rent

$16.99

Present value

$64.04

Effective rent

$16.89

III. Gross Lease

Year

1

2

3

4

5

Gross rent

$30.00

$30.00

$30.00

$30.00

$30.00

Less: expenses

10.00

11.00

12.00

13.00

Net rent

21.00

20.00

19.00

18.00

17.00

Average rent

$19.00

Present value

$72.74

Effective rent

$19.19

Adjustment:

What types of expenses would property owners pay when operating and maintaining common areas? Give examples

for office, retail, and warehouse properties.

Solutions to Problems – Chapter 9

Introduction to Income-Producing Properties: Leases and Market for Space

Problem 9-1

a)

Discount rate

10.00%

I. Net Lease with Steps:

Year

1

2

3

4

5

Net Rent

$15.00

16.50

18.00

19.50

21.00

Average rent

$18.00

Present value

$67.15

Effective rent

$17.72

Year

1

2

3

4

5

Exp. CPI

3.00%

3.00%

3.00%

3.00%

Gross rent

$22.00

$22.66

$23.34

$24.04

$24.76

Less: expenses

$9.00

10.00

11.00

12.00

13.00

Plus: reimbursement

0.00

1.00

2.00

3.00

4.00

Net rent

13.00

13.66

14.34

15.04

15.76

Average rent

$14.36

Present value

$53.94

Effective rent

$14.23

Note: Effective Rent = Present Value / PVIFA, 10%, 5yrs

Problem 9-2

(a) Total rentable area in building if leased to one tenant:

300,000 (total building area) – 45,000 (non-rentable area) = 255,000 sqft (rentable)

(b) Load Factor for 7th floor:

0

1

2

3

4

5

$23

$24

$25

$26

Problem 9-3

(a)

Year

0

1

2

3

4

5

Cash Flows

$20

$21

$22

$23

$24

(b)

Year

0

1

2

3

4

5

Cash Flows

$150,000

$24

$25

$26

$27

$28

Problem 9-5

(A) Option A is best because it gives higher effective rent psf. See the calculations below

Option A

Year

1

2

3

4

5

Base Rent

$25.00

$ 26.00

$ 27.00

$ 28.00

$ 29.00

CAM

$ 3.00

3.18

3.37

3.57

$ 3.79

Net Rent

$28.00

29.18

$30.37

$ 31.57

$ 32.79

Present Value

=NPV(10%,Rent_each_year)

$114.31

Effective rent/square

foot

$ 31.71

Option B

Year

1

2

3

4

5

Base Rent

$23.00

$24.00

$25.00

$26.00

$27.00

CAM

$ 3.00

$ 3.18

3.3708

3.57

3.79

Net Rent

$26.00

$27.18

$28.37

$29.57

$30.79

Sales

$850,000.000

935000

1028500

1131350

124485

Overage Rent

$ 0 –

$2,800

$10,280

$18,508

$27,559

PV of Net Rent

= NPV(10%,Ret_each_year)

$ 1,013,396.12

PV of Overage Rent

= NPV(10%,overage rent)

$ 36,949.02

PV of Total Rent Revenue

= Net Rent + Overage rent)

$ 1,050,345.14

Effective rent/square foot

= Effective rent/Rentable_ area

$ 29.14

(B) Even when sales is expected to grow by 20% per year, option A is still better than option B because it gives effective

rent of $31.71 compared to effective rent of $30.73 for option B.

Year

1

2

3

4

5

Base Rent

$ 23.00

$ 24.00

$ 25.00

$ 26.00

$ 27.00

CAM

$ 3.00

$ 3.18

$ 3.37

$ 3.57

$ 3.79

Net Rent

$ 26.00

$ 27.18

$ 28.37

$ 29.57

$ 30.79

Sales

$850,000

$ 1,020,000

$ 1,224,000

$ 1,468,800

$ 1,762,560

Overage Rent

$ –

$ 9,600.00

$ 25,920.00

$ 45,504.00

$ 69,004.80

Calculate Effective Rent:

PV of Net Rent

= NPV (10%, Rent_each_year)

$1,013,396.12

PV of Overage Rent

= NPV (10%, Overage Rent)

$ 94,176.20

PV of Total Rent Revenue

= Net Rent + Overage Rent

$1,107,572.32

Effective rent/square foot

= Effective rent/Rentable_area)

$ 30.73

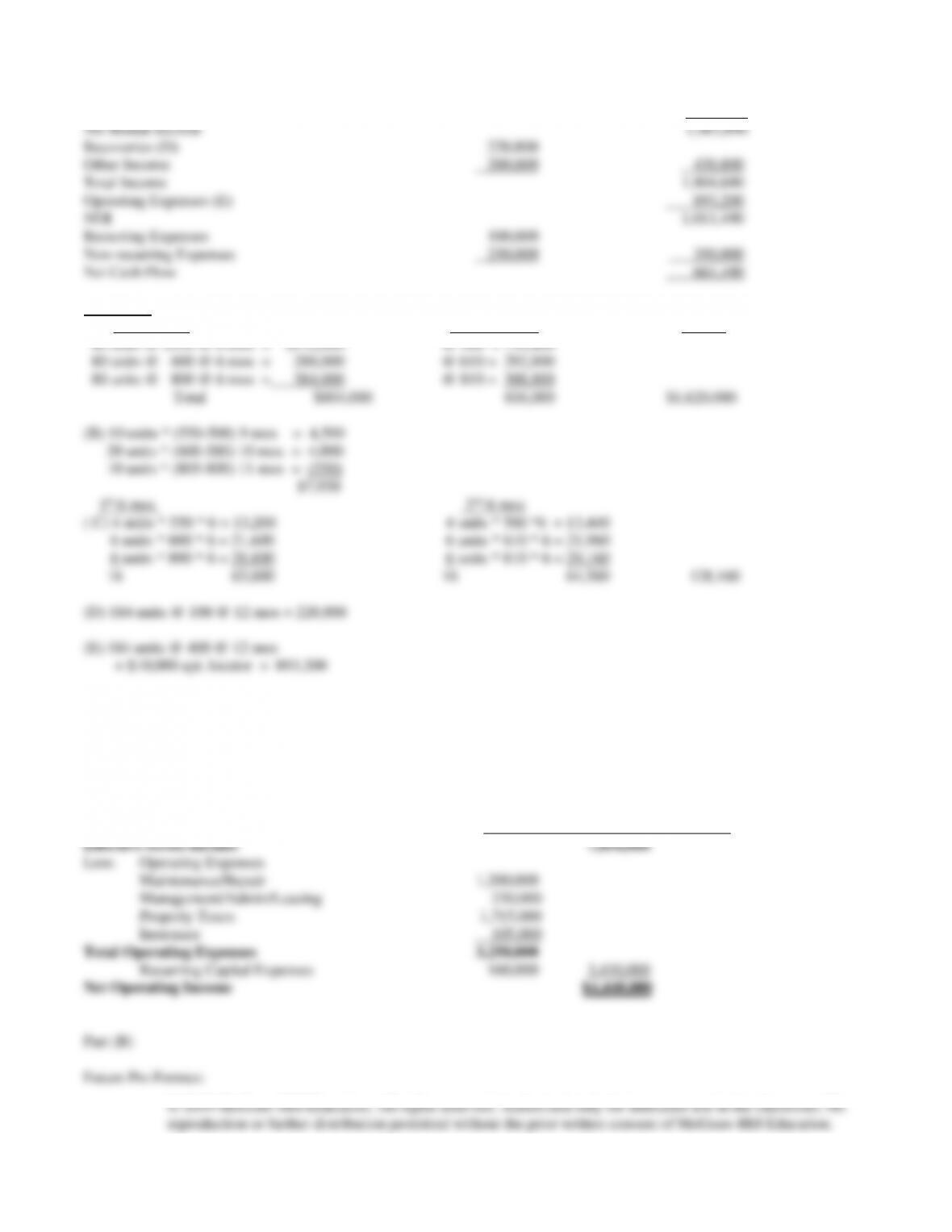

Problem 9-6 (see notes A-E below for explanation)

Gross Potential Income (A)

1,620,000

Loss to Lease (B)

7,950

Vacancy & Collection Loss ( C)

128,160

Net Rental Income

1,483,890

Recoveries (D)

220,800

Other Income

200,000

420,800

Total Income

1,904,690

Operating Expenses (E)

893,200

NOI

1,011,490

Recurring Expenses

100,000

Non-recurring Expenses

250,000

350,000

Net Cash Flow

661,490

Notes A-E

(A) 1st 6 months

2nd 6 months

Total

40 units @ $550 @ 6 mos = $132,000

@ 560 = 134,400

80 units @ 600 @ 6 mos = 288,000

@ 610 = 292,800

80 units @ 800 @ 6 mos = 384,000

@ 810 = 388,800

Total $804,000

816,000

$1,620,000

(B) 10 units * (550-500) 9 mos = 4,500

20 units * (600-580) 10 mos = 4,000

10 units * (805-800) 11 mos = (550)

$7,950

1st 6 mos

2nd 6 mos

( C) 4 units * 550 * 6 = 13,200

4 units * 560 *6 = 13,440

6 units * 600 * 6 = 21,600

6 units * 610 * 6 = 21,960

6 units * 800 * 6 = 28,800

6 units * 810 * 6 = 29,160

16 63,600

16 64,560

128,160

(D) 184 units @ 100 @ 12 mos = 220,800

(E) 184 units @ 400 @ 12 mos

+ $10,000 apt. locator = 893,200

Problem 9-7

Part (A) SUMMER PLACE MALL

Revenue: Base Rents (400,000 sq. ft. @ $20) 8,000,000

Add: Overage Rents 400,000

CAM recoveries 250,000

Less: Vacancy @ 10% of Base Rents 800,000

© 2019 McGraw-Hill Education. All rights reserved. Authorized only for instructor use in the classroom. No

reproduction or further distribution permitted without the prior written consent of McGraw-Hill Education.

1) The possibility of vacancy reduction from a high level of 10%.

2) Operating expenses in the pro forma may be underestimated as to utility expense which may not be included in the

statement.

3) The likelihood of overage rents continuing or increasing from current levels.

4) A lease rollover schedule should be developed to assess the probability of lease renewal among 40 tenants.

5) A market analysis to determine the likelihood of new retail (competitive) space coming into the marketplace.

Problem 9-8

Part (A) BETTS DISTRIBUTION CENTER

Rent: (200,000 sq. ft. @$7.00) 1,400,000

Add: Recoveries @ $1.50 300,000

Insurance 15,000

Problem 9-9

Part (A) WEST OFFICE PLAZA

Revenue: (300,000 sq. ft. @$20) 6,000,000

Add: Other Income (parking) 450,000

Problem 9-10

(a) Only the leases with CPI adjustments are affected. The effective rent for the net lease with a CPI adjustment increases to