Solutions to Questions – Chapter 5

Adjustable and Floating Rate Mortgage Loans

Question 5-1

In the previous chapter, significant problems regarding the ability of borrowers to meet mortgage payments and

the evolution of fixed interest rate mortgages with various payment patterns were discussed. Why didn’t this

evolution address problems faced by lenders? What have lenders done in recent years to overcome these

problems?

Question 5-2

How do inflationary expectations influence interest rates on mortgage loans?

Question 5-3

How does the price level adjusted mortgage (PLAM) address the problem of uncertainty in inflationary

expectations? What are some of the practical limitations in implementing a PLAM program?

Question 5-4

Why do adjustable rate mortgages (ARMs) seem to be a more suitable alternative for mortgage lending than

PLAMs?

Question 5-5

List each of the main terms likely to be negotiated in an ARM. What does pricing an ARM using these terms mean?

Question 5-6

What is the difference between interest rate risk and default risk? How do combinations of terms in ARMs affect

the allocation of risk between borrowers and lenders?

Question 5-7

Which of the following two ARMs is likely to be priced higher, that is, offered with a higher initial interest rate?

Question 5-8

What are forward rates of interest? How are they determined? What do they have to do with indexes used to

adjust ARM payments?

Question 5-9

Distinguish between the initial rate of interest and expected yield on an ARM. What is the general relationship

between the two? How do they generally reflect ARM terms?

Question 5-10

If an ARM is priced with an initial interest rate of 8 percent and a margin of 2 percent (when the ARM index is

also 8 percent at origination) and a fixed rate mortgage (FRM) with constant payment is available at 11 percent,

what does this imply about inflation and the forward rates in the yield curve at the time of origination? What is

implied if a FRM were available at 10 percent? 12 percent?

Solutions to Problems – Chapter 5

Adjustable Rate and Variable Payment Mortgages

Problem 5-1

(a) Compute the payments at the beginning of each year of the PLAM.

CFj nj

-$89,300

Problem 5-2

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

EOY

Balance

(1) – (7)

BOY

Balance

Annual

Interest

Rate

Monthly

Interest

Rate (2)/12

Payments

Monthly

Interest

(3) x (1)

Monthly

Amort

Annual

Amort.

Year

(4) –(5)

0

1

$200,000

6.00%

0.50%

$1,199.10

$1,000.00

$199.10

$2,456.02

$197,544

2

$197,544

7.00%

0.58%

$1,327.75

$1,152.34

$175.41

$2,173.82

$195,370

(a)

(b)

(c)

(d)

(e)

Problem 5-3

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

EOY

Balance

(1) – (7)

Annual

Interest

Rate

Monthly

Interest Rate

(2)/12

Monthly

Interest

(3) x (1)

Monthly

Amort

Annual

Amort.

BOY

Balance

(4) –(5)

Year

Payments

0

1

$150,000

7.00%

0.58%

$997.95

$875.00

$122.95

$1,523.71

$148,476

2

148,525

7.00%

0.58%

$997.95

$866.11

$131.84

$1,633.86

$146,842

3

146,942

7.00%

0.58%

$997.95

$856.58

$141.37

$1,751.98

$145,090

4

145,244

6.00%

0.50%

$905.34

$725.45

$179.89

$2,219.06

$142,871

(a)

Monthly Payment = $997.95

Loan Balance EOY 3 = $145,090

(b)

New Monthly Payment = $906.30

(c)

Interest only monthly payment = $875

Problem 5-4

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

EOY

Balance

(1) – (7)

Annual

Interest

Rate

Monthly

Interest

Rate

(2)/12

Monthly

Interest

Monthly

Amort

Annual

Amort.

BOY

Balance

(4) –(5)

Year

Payments

0

1

$100,000

2.00%

0.17%

$423.85

$166.67

$257.19

$3,114.70

$96,885

2

96,885

6.00%

0.50%

$635.55

$484.43

$151.12

$1,864.15

$95,021

(a)

Monthly payment during 1 year = $423.85

(b)

Monthly payment in 2 year = $635.55

(c)

Percentage increase in monthly payment = 50%

(d)

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

EOY

Balance

(1) – (7)

Annual

Interest

Rate

Monthly

Interest

Rate

(2)/12

Monthly

Interest (3)

x (1)

Monthly

Amort

Annual

Amort.

BOY

Balance

(4) –(5)

Year

Payments

0

1

$100,000

2.00%

0.17%

$423.85

$166.67

$257.19

$3,114.70

$96,885

2

96,885

2.00%

0.17%

$423.85

$161.48

$262.38

$3,177.57

$93,708

3

93,708

2.00%

0.17%

$423.85

$156.18

$267.67

$3,241.71

$90,466

4

90,466

6.00%

0.50%

$617.95

$452.33

$165.62

$2,043.02

$88,423

Monthly payments at beginning of year 4 = $ 617.95

Problem 5-5

Problem 5-6

Compute the payments, loan balance, and yield for an unrestricted ARM

Problem 5-7

Compute the payments, loan balances, and yield for an ARM that has a maximum 5% annual payment cap and allows

negative amortization.

Principal = $150,000

Term = 30 years

Problem 5-8

Compute the payments, loan balances, and yield for an ARM that has a 1% annual and 3% lifetime interest rate cap and

does not accumulate negative amortization.

Principal = $150,000

Points = 2.00%

Term = 30 years

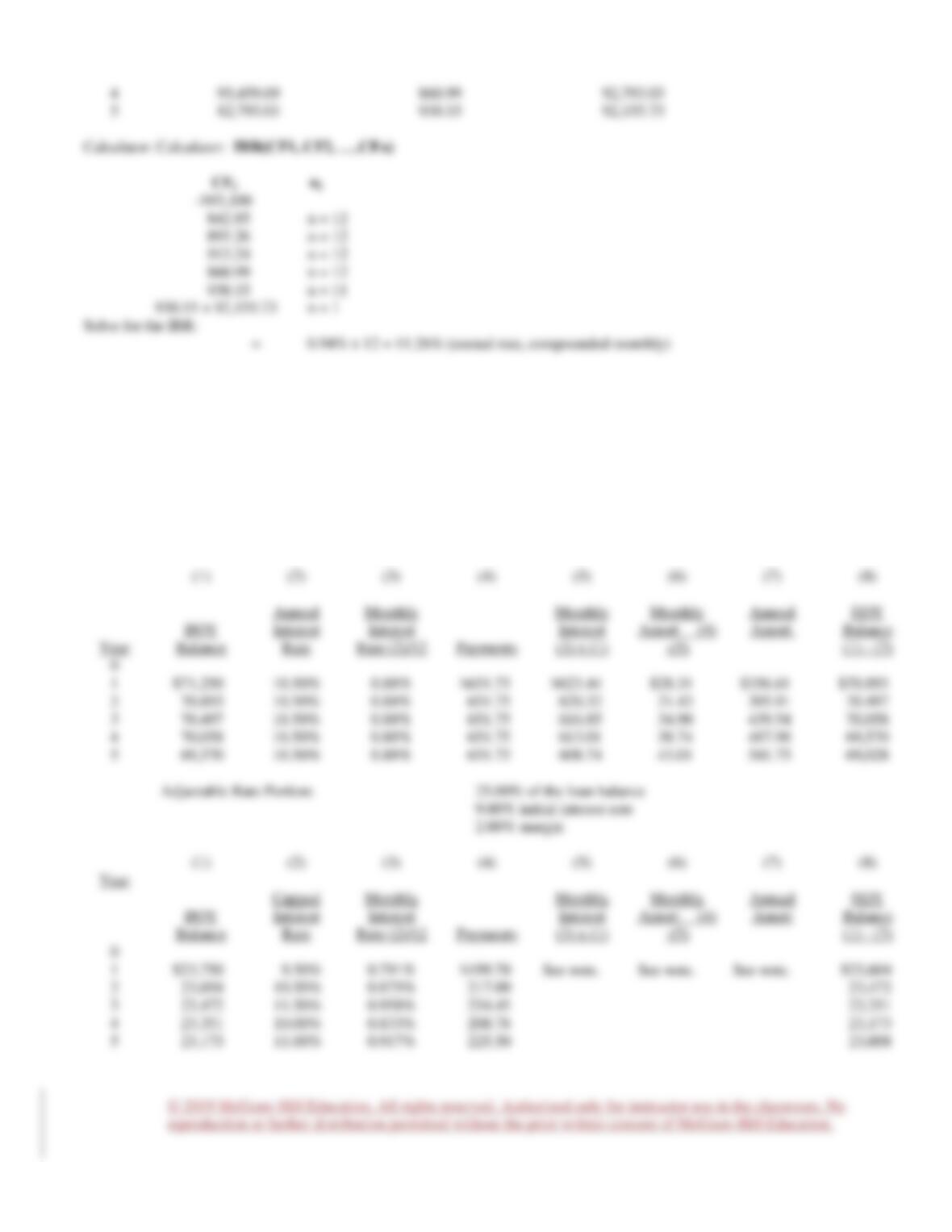

Problem 5-9

(a) Compute the payments, loan balances, and yield for a Stable Home Mortgage which is comprised of a fixed and

adjustable rate component.

Loan Amount = $95,000

Points = 2.00%

Fixed Rate Portion: 75.00% of the loan balance

10.50% annual interest rate

30 year term

© 2019 McGraw-Hill Education. All rights reserved. Authorized only for instructor use in the classroom. No

reproduction or further distribution permitted without the prior written consent of McGraw-Hill Education.

4

93,459.69

860.99

92,793.03

5

82,793.03

930.15

92,155.73

Calculator: Calculator: IRR(CF1, CF2, ….CFn)

CFj nj

-$93,100

842.85 n = 12

895.26 n = 12

913.24 n = 12

860.99 n = 12

930.15 n = 11

930.15 + 92,155.73 n = 1

Solve for the IRR:

= 0.94% x 12 = 11.26% (annual rate, compounded monthly)

(b) Adjustable rate portion now has an initial rate of 9.5% and an annual interest rate cap of 1%

Loan Amount = $95,000

Points = 2.00%

Fixed Rate Portion: 75.00% of the loan balance

10.50% annual interest rate

30 year term

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Year

BOY

Balance

Annual

Interest

Rate

Monthly

Interest

Rate (2)/12

Payments

Monthly

Interest

(3) x (1)

Monthly

Amort (4)

-(5)

Annual

Amort.

EOY

Balance

(1) – (7)

0

1

$71,250

10.50%

0.88%

$651.75

$623.44

$28.31

$356.61

$70.893

2

70,893

10.50%

0.88%

651.75

620.32

31.43

395.91

70.497

3

70,497

10.50%

0.88%

651.75

616.85

34.90

439.54

70,058

4

70,058

10.50%

0.88%

651.75

613.01

38.74

487.98

69,570

5

69,570

10.50%

0.88%

651.75

608.74

43.01

541.75

69,028

Adjustable Rate Portion: 25.00% of the loan balance

9.00% initial interest rate

2.00% margin

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Year

BOY

Balance

Capped

Interest

Rate

Monthly

Interest

Rate (2)/12

Payments

Monthly

Interest

(3) x (1)

Monthly

Amort (4)

-(5)

Annual

Amort

EOY

Balance

(1) – (7)

0

1

$23,750

9.50%

0.791%

$199.70

See note.

See note.

See note.

$23,604

2

23,604

10.50%

0.875%

217.00

23,472

3

23,472

11.50%

0.958%

234.45

23,351

4

23,351

10.00%

0.833%

208.78

23,173

5

23,173

11.00%

0.917%

225.50

23,008

Problem 5-10

(a) Loan Balance at the end of year five is $116,333.93

Solution:

n = 5×12 or 60

i = 12/12 or 1

PV = -$100,000

Problem 5-11

Problem 5-12

Problem 5-13