(d) Include prepayment penalty of 2% of $83,186.41 or $1,663.73

Solution i:

Problem 4-15

Points required to achieve a yield to 10% for the 25 year loan. Fv is now $83,186.41 = $1,663.73 = $84,850.14

Monthly payments PMT (n,i,PV,FV):

n = 300

i = 9% 12

Problem 4-16

(a) In order to find which loan is the better choice after 20 years, the effective interest rate for each loan must be calculated.

Loan A

Loan B

Principal

$75,000

$75,000

Nominal interest rate

6.00%

7.00%

Term (years)

30

30

Points

6

2

Payment

$449.66

$498.98

Loan Balance after 20 years

$40,502.43

$42,975.33

Loan Balance after 5 years

$69,790.32

$70,599.14

Loan A

Loan B

Loan A

i = .623917% * 12 = 7.49%

Loan B

The borrower would be indifferent between the two loans if the repayment period is 5 years.

Problem 4-17

(a) Monthly Payments = $1,382.50 to be made to the borrower

Note: Balance at the end

Note: Balance at the end

of 60 months = $70,599.14

Problem 4-18

Find the balance at the end of 5 years for a fully amortizing $200,000, 10% mortgage with a 25 year amortization schedule:

PV = -200,000 FV = 0

Problem 4- 19

CAM loan:

(a) Calculate constant monthly amortization:

$125,000 240 months = $520.83 per month

Calculate Monthly Interest:

Month

Beg.

Balance

Rate

Interest

Amortization

Total Payment

End Balance

1

125,000

*11%/12

1,145.83

520.83

1,666.66

124,479.17

2

124,479.17

*11%/12

1,141.05

520.83

1,661.88

123,958.34

3

123,958.34

*11%/12

1,136.28

520.83

1,657.11

123,437.51

4

123,437.51

*11%/12

1,131.51

520.83

1,652.34

122,916.68

5

122,916.68

*11%/12

1,126.74

520.83

1,647.57

122,395.85

6

122,395.85

*11%/12

1,121.96

520.83

1,642.79

121,875.02

(b) For a constant payment loan (CPM) we have:

PV = -$125,000

n = 240

i = 11% 12

FV = 0

Solve PMT = $1,290.24

(c) In the absence of point and origination fees, the effective interest rates on both loans will be an annual rate of 11%, compounded

monthly. This is true regardless of when either of the loans are repaid. Monthly payments are different, however i is the same for

both loans.

Problem 4-20

(a) Determine monthly payments based on interest being accrued daily.

Solve for interest due at the end of month one:

Problem 4- 21 Comprehensive Review Problem

(1) Fully amortizing:

(2) Partial amortizing:

(3) Interest only

(4) Negative amortization:

PV = -100,000 n = 240

i = 12% Solve PMTs = $949.46

FV = 150,000

B. Loan Balances for A.1. – A.4 after 5 years

n = 180

C. Interest at the end of month 61 for A.1 – A.4

D. APR* for loans in A.1 – A.4

E. Effective yield if loan prepaid EOY5. Balances must be calculated at EOY5 for each loan (not shown).

F. “Interest only” monthly payments in A.1 = $100,000 * (12% 12) or $1,000 per month for 36 mos. What must

payments be from yr. 4-17 to fully amortize the loan at the end of 240 mos.?

(2) n = 204 FV = 150,000

(3) 12% because there are no points

(4) 4 points charged, loan payoff 36 months, what is effective interest rate?

Problem 4-22

Problem 4-23

Chapter 4 Appendix

Questions

Question 4-A1

Why do monthly mortgage payments increase so sharply during periods of inflation? What does the tilt effect have to do with

this?

Question 4-A2

As inflation increases, the impact of the tilt effect is said to become even more burdensome on borrowers. Why is this so?

Problem 4A-1

(a) Year Payment

CFj = 498.57

nj = 12

CFj = 576.16

nj = 12

CFj = 665.82

nj = 12

CFj = 715.76

nj = 11*

Problem 4A-2

Excel template Ch4 GPM from course website modified to solve this problem.

Chapter 4

Loan Balance on GPM

Spreadsheet Limitations: Projections for 5 years

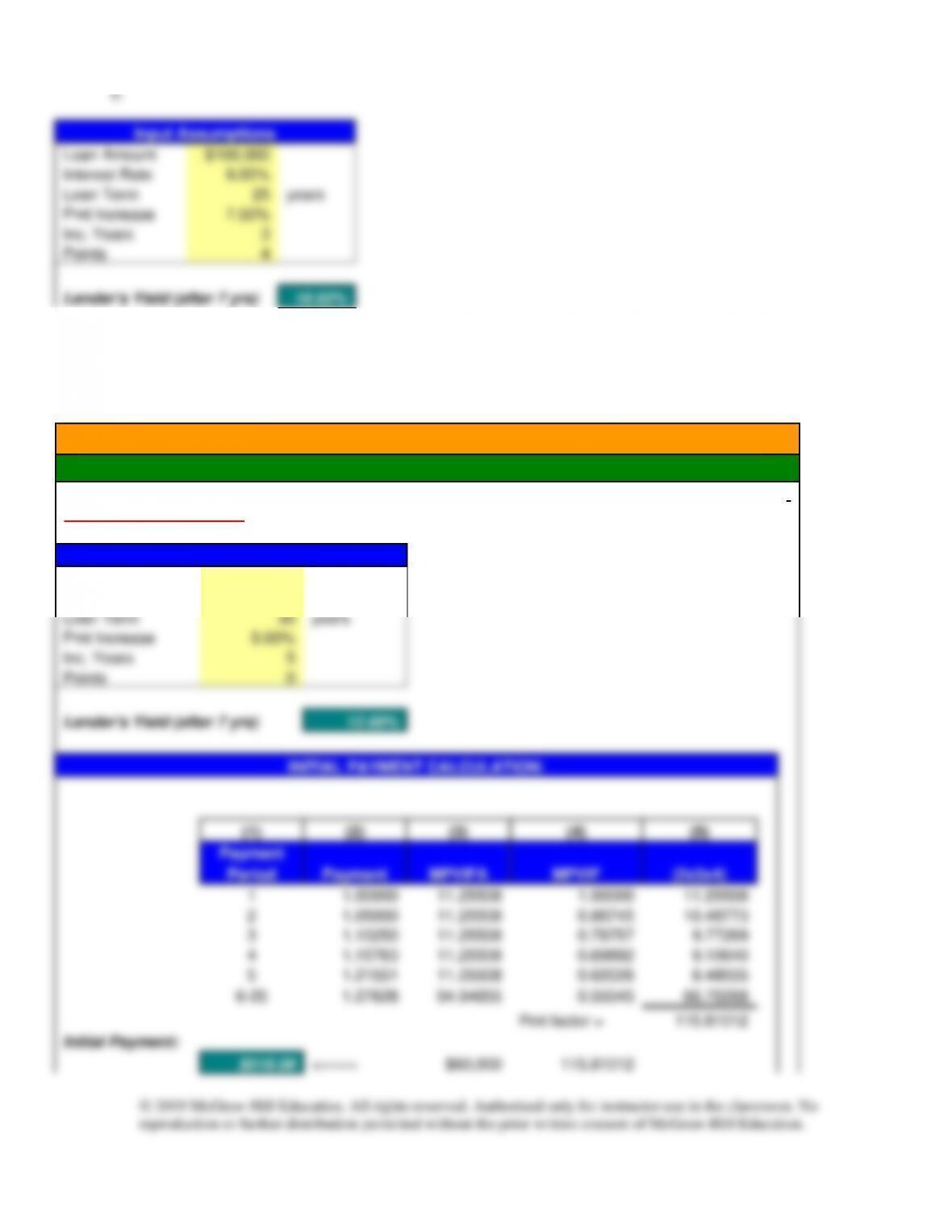

Input Assumptions

Loan Amount

$100,000

Interest Rate

9.00%

Loan Term

25

years

Pmt Increase

7.50%

Inc. Years

3

Points

4

Lender’s Yield (after 7 yrs)

10.02%

INITIAL PAYMENT CALCULATION:

(1)

(2)

(3)

(4)

(5)

Payment

Period

Payment

MPVIFA

MPVIF

(2x3x4)

1

1.00000

11.43491

1.00000

11.43491

2

1.07500

11.43491

0.91424

11.23830

3

1.15563

11.43491

0.83583

11.04507

4

1.24230

11.43491

0.76415

10.85516

5

1.24230

11.43491

0.69861

9.92420

6-25

1.24230

111.14495

0.63870

88.18848

Pmt factor =

142.68613

Initial Payment:

$700.84

<====

$100,000

142.68613

Loan Amt

/ Pmt Factor

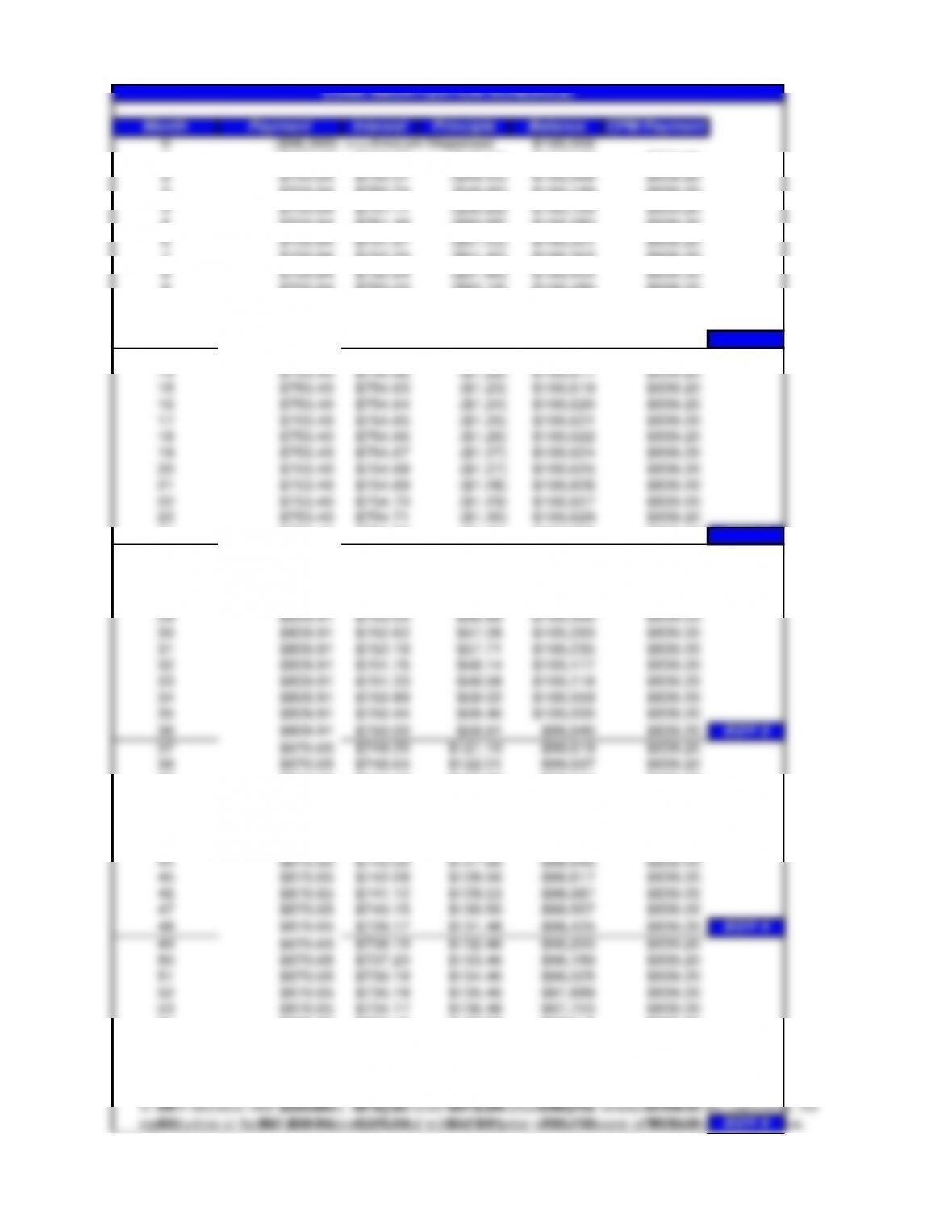

a. Calculation of initial payment is shown above. Payments for years 2 through 5 are shown in the exhibit below.

b. The loan balance at the end of year 3 is shown in the exhibit below.

36 $809.91 $750.00 $59.91 $99,940 $839.20 EOY 3

Month Payment Interest Principle Balance

CPM Payment

0 ($96,000) <==Amount Dispersed $100,000

1$700.84 $750.00 ($49.16) $100,049 $839.20

2$700.84 $750.37 ($49.53) $100,099 $839.20

3$700.84 $750.74 ($49.90) $100,149 $839.20

4$700.84 $751.11 ($50.28) $100,199 $839.20

5$700.84 $751.49 ($50.65) $100,250 $839.20

6$700.84 $751.87 ($51.03) $100,301 $839.20

7$700.84 $752.25 ($51.42) $100,352 $839.20

9$700.84 $753.03 ($52.19) $100,456 $839.20

11 $700.84 $753.81 ($52.98) $100,562 $839.20

13 $753.40 $754.61 ($1.21) $100,616 $839.20

15 $753.40 $754.63 ($1.23) $100,619 $839.20

16 $753.40 $754.64 ($1.24) $100,620 $839.20

17 $753.40 $754.65 ($1.25) $100,621 $839.20

18 $753.40 $754.66 ($1.26) $100,622 $839.20

19 $753.40 $754.67 ($1.27) $100,624 $839.20

23 $753.40 $754.71 ($1.30) $100,629 $839.20

29 $809.91 $753.05 $56.86 $100,350 $839.20

30 $809.91 $752.62 $57.28 $100,293 $839.20

31 $809.91 $752.19 $57.71 $100,235 $839.20

32 $809.91 $751.76 $58.14 $100,177 $839.20

33 $809.91 $751.33 $58.58 $100,118 $839.20

34 $809.91 $750.89 $59.02 $100,059 $839.20

LOAN AMORTIZATION SCHEDULE:

c.

Input Assumptions

Loan Amount

$100,000

Interest Rate

9.00%

Loan Term

25

years

Pmt Increase

7.50%

Inc. Years

3

Points

4

Lender’s Yield (after 7 yrs)

10.02%

Problem 4A-3

The initial payment would now be $518.09 as shown below.

Chapter 4

Loan Balance on GPM

Spreadsheet Limitations: Projections for 7 years

Input Assumptions

Loan Amount

$60,000

Interest Rate

12.00%

Loan Term

30

years

Pmt Increase

5.00%

Inc. Years

5

Points

0

Lender’s Yield (after 7 yrs)

12.00%

INITIAL PAYMENT CALCULATION:

(1)

(2)

(3)

(4)

(5)

Payment

Period

Payment

MPVIFA

MPVIF

(2x3x4)

1

1.00000

11.25508

1.00000

11.25508

2

1.05000

11.25508

0.88745

10.48773

3

1.10250

11.25508

0.78757

9.77269

4

1.15763

11.25508

0.69892

9.10640

5

1.21551

11.25508

0.62026

8.48555

6-25

1.27628

94.94655

0.55045

66.70268

Pmt factor =

115.81012

Initial Payment:

$518.09

<====

$60,000

115.81012

Loan Amt

/ Pmt Factor