Solutions to Questions – Chapter 22

Real Estate Investment Performance and Portfolio Considerations

Question 22-1

What are some of the difficulties of obtaining data to measure real estate investment performance?

Question 22-2

What are the distinguishing characteristics between REIT data and the NCREIF Property Index?

Question 22-3

What is the difference between arithmetic and geometric mean returns?

Question 22-4

What statistical concept do many portfolio managers use to represent risk when considering investment

performance?

Question 22-5

When NCREIF returns and REIT returns are compared, NCREIF returns exhibit a much lower pattern of

variation. Why might this be the case?

Question 22-6

Mean returns for portfolios are calculated by taking the weighted average of the mean returns for each investment

in the portfolio. Why won’t this approach work to calculate the standard deviation of portfolio returns?

Question 22-7

What is the difference between covariance and correlation? Why are these concepts so important in portfolio

analysis?

Question 22-8

Results reported in the chapter showed that by including either REITs or the NCREIF Index in a portfolio

containing S&P 500 securities, corporate bonds, and T bills, diversification benefits resulted. Why was this true?

Did those benefits come about for the same reason for each category of real estate investment?

Question 22-9

Results presented in the chapter are based on historical data. Of what use are these results to a portfolio manager

who may be making an investment decision today? Elaborate.

Question 22-10

Why should an investor consider investing globally?

Question 22-11

What are the risks of global investment?

Question 22-12

How can derivative security be used to hedge portfolio risk?

Solutions to Problems – Chapter 22

Real Estate Investment Performance and Portfolio Considerations

Problem 22-1

ET&T

MREAF

Common Stock Fund

Real Estate Fund

Unit

Quarterly

Unit

Quarterly

Period Ending

Value

Dividend

Value

Dividend

1

701.00

8.28

70.00

2.17

2

752.50

8.11

80.05

2.14

3

850.52

10.30

90.80

2.01

4

953.75

9.81

100.50

2.01

5

1,047.57

12.05

99.14

1.87

6

1,221.70

14.17

95.50

1.81

7

1,443.90

17.18

93.77

1.79

8

1,263.31

14.91

80.31

1.54

9

1,258.56

13.84

77.34

1.49

10

1,526.72

18.32

76.53

1.44

11

1,616.81

19.73

78.42

1.51

12

1,624.08

19.98

79.01

1.53

13

1,560.25

18.88

81.75

1.55

(a)

(b)

Common

Real Estate

Period

Stock Fund

Fund

1

NA

NA

2

8.50%

17.41%

3

14.39%

15.94%

4

13.29%

12.90%

5

11.10%

0.51%

6

17.97%

-1.85%

7

19.59%

0.06%

8

-11.47%

-12.71%

9

.72%

-1.84%

10

22.76%

0.81%

11

7.19%

4.44%

12

1.69%

2.70%

13

-2.77%

5.43%

Total

102.98%

43.81%

(b) Calculate Arithmetic Mean return

Calculate the Standard Deviation

Stock Fund

Real Estate fund

Period

(HPRa – HPRa)

(HPRa – HPRa)

(HPRb – HPRb)

(HPRb – HPRb)

1

2

-0.0008

0.0000

0.1376

0.0189

3

0.0581

0.0034

0.1229

0.0151

4

0.0471

0.0022

0.0925

0.0085

5

0.0252

0.0006

-0.0314

0.0010

6

0.0939

0.0088

-0.0550

0.0030

7

0.1101

0.0121

-0.0359

0.0013

8

-0.2006

0.0402

-0.1636

0.0268

9

-0.0786

0.0062

-0.0549

0.0030

10

0.1418

0.0201

-0.0284

0.0008

11

-0.0139

0.0002

0.0079

0.0001

12

-0.0690

0.0048

-0.0095

0.0001

13

-0.1135

0.0129

0.0178

0.0003

Total

0.1115

0.0790

Variance of Common Stock Fund = 0.1115 / 12 = 0.0093

Calculate the Geometric Mean

Stock Fund

Real Estate Fund

Period

(1 + HPRa)

(1 + HPRb)

1

2

1.0850

1.1741

3

1.1439

1.1594

4

1.1329

1.1290

5

1.1110

1.0051

6

1.1797

0.9815

7

1.1959

1.0006

8

0.8853

0.8729

9

1.0072

0.9816

10

1.2276

1.0081

11

1.0719

1.0444

12

1.0169

1.0270

13

.9723

1.0543

Geometric Mean of Stock Fund = 0.0814

(c) Correlation between Common Stock Fund and Real Estate Fund

Correlation between Stock Fund and Real Estate Fund =[COVab] / [Std. Dev. (a) x Std. Dev. (b)]

COVab = [HPRa – HPRa] x [HPRb – HPRb] / N

[HPRa – HPRa] *

Period

(HPRa – HPRa)

(HPRb – HPRb)

[HPRb – HPRb]

1

2

-0.0008

0.1376

-0.0001

3

0.0581

0.1229

0.0071

4

0.0471

0.0925

0.0044

5

0.0252

-0.0314

-0.0008

6

0.0939

-0.0550

-0.0052

7

0.1101

-0.0359

-0.0040

8

-0.2006

-0.1636

0.0328

9

-0.0786

-0.0549

0.0043

10

0.1418

-0.0284

-1.0040

11

-0.0139

0.0079

-0.0001

12

-0.0690

-0.0095

0.0007

13

-0.1135

0.0178

-0.0020

Total

0.0331

Covariance between Stock Fund and Real Estate Fund = 0.0331 / 12.00 = 0.0028

(d) In order for a portfolio of assets to provide diversification, the standard deviation of the portfolio must be less than the

weighted average standard deviations of the individual assets.

The portfolio will be comprised of 50.00% Common Stock and

50.00% Real Estate Equities

Common

Real Estate

Period

Stock Fund

Fund

Portfolio

1

NA

NA

NA

2

0.0850

0.1741

0.1296

3

0.1439

0.1594

0.1517

4

0.1329

0.1290

0.1309

5

0.1110

0.0051

0.0580

6

0.1797

-0.0185

0.0806

7

0.1959

0.0006

0.0983

8

-0.1147

-0.1271

-0.1209

9

0.0072

-0.0184

-0.0056

10

0.2276

0.0081

0.1179

11

0.0719

0.0444

0.0582

12

0.0169

0.0270

0.0219

13

-0.0277

0.0543

0.0133

1.0298

0.4381

0.7339

Weighted Average Standard Deviation (each asset weighted 50%) = 0.0888

(e) Optional

Weight

of Common

Portfolio

Portfolio

Stock

Return

Risk

0%

3.65%

8.11%

10%

4.14%

7.69%

20%

4.64%

7.39%

30%

5.13%

7.22%

40%

5.62%

7.20%

50%

6.12%

7.31%

60%

6.61%

7.57%

70%

7.10%

7.94%

80%

7.60%

8.42%

90%

8.09%

8.99%

100%

8.58%

9.64%

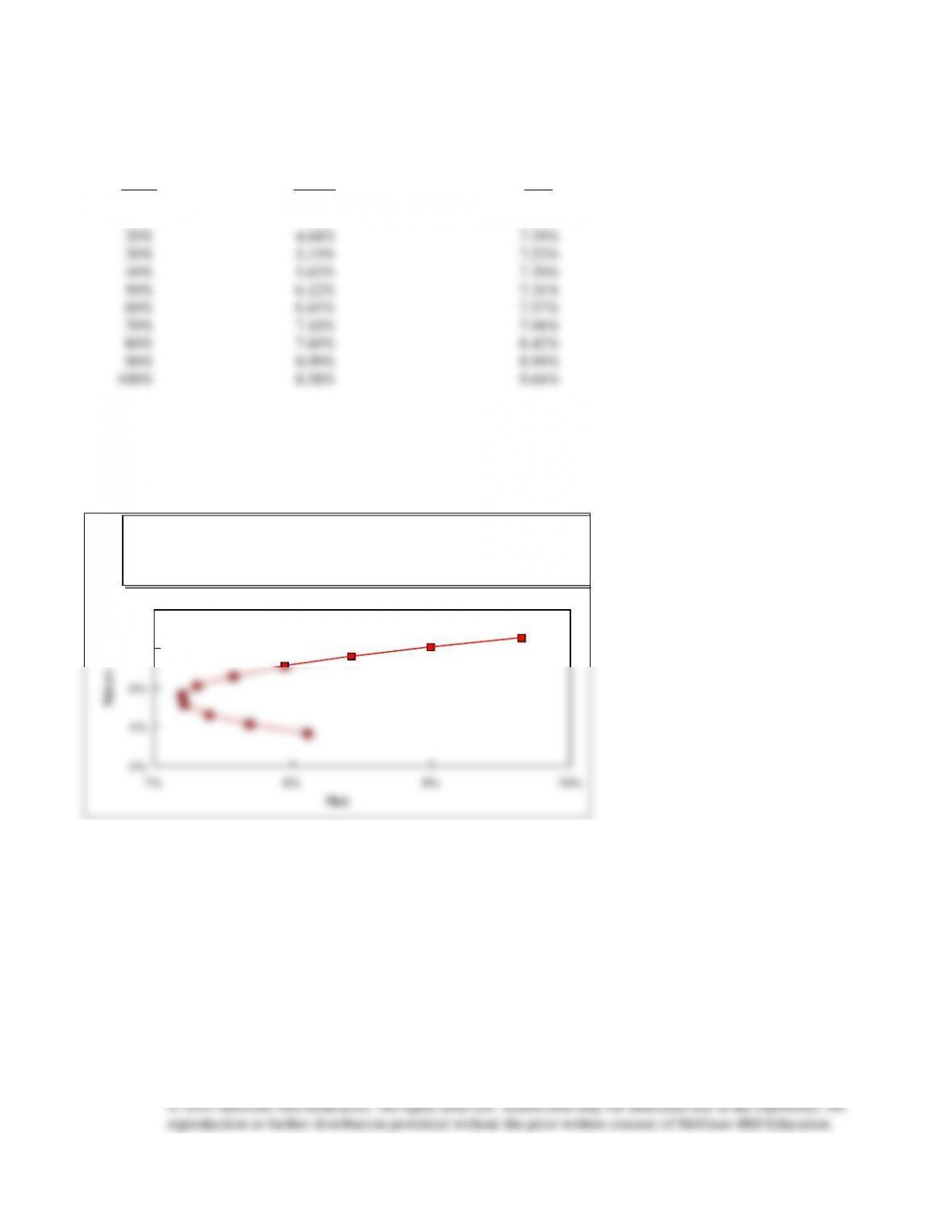

(f) Based on the exhibit below, it would appear that substantial risk reduction occurs as more of the real estate fund is

combined with the stock fund. However, mean returns on the portfolio increase sharply as more common stock is added.

How much stock should be combined with real estate will depend on the degree of risk aversion of the portfolio manager,

however, the trade off between risk and return can be clearly seen in the Exhibit.

7% 8% 9% 10%

2%

4%

6%

8%

10%

Risk

Return

Portfolio of Stocks and Real Estate

Return vs. Risk

Problem 22-2

See below:

Portfolio

Portfolio

% S&P

% NCREIF

Variance

Stand. Dev

Return

Return x 100

0.00%

100.00%

0.03%

1.76%

2.32%

2.32

5.00%

95.00%

0.03%

1.64%

2.41%

2.41

10.00%

90.00%

0.03%

1.61%

2.50%

2.50

15.00%

85.00%

0.03%

1.68%

2.58%

2.58

20.00%

80.00%

0.03%

1.83%

2.67%

2.67

25.00%

75.00%

0.04%

2.05%

2.76%

2.76

30.00%

70.00%

0.05%

2.32%

2.84%

2.84

35.00%

65.00%

0.07%

2.62%

2.93%

2.93

40.00%

60.00%

0.09%

2.94%

3.02%

3.02

45.00%

55.00%

0.11%

3.28%

3.10%

3.10

50.00%

50.00%

0.13%

3.63%

3.19%

3.19

55.00%

45.00%

0.16%

3.99%

3.28%

3.28

60.00%

40.00%

0.19%

4.36%

3.36%

3.36

65.00%

35.00%

0.22%

4.73%

3.45%

3.45

70.00%

30.00%

0.26%

5.11%

3.54%

3.54

75.00%

25.00%

0.30%

5.49%

3.62%

3.62

80.00%

20.00%

0.34%

5.87%

3.71%

3.71

85.00%

15.00%

0.39%

6.25%

3.80%

3.80

90.00%

10.00%

0.44%

6.64%

3.88%

3.88

95.00%

5.00%

0.49%

7.02%

3.97%

3.97

100.00%

0.00%

0.55%

7.41%

4.06%

4.06