Solution to Questions – Chapter 20

The Secondary Mortgage Market: CMOs and Derivative Securities

Question 20-1

What is a mortgage pay-through bond (MPTB)? How does it resemble a mortgage-backed bond (MBB)? How

does it differ?

Question 20-2

Are the overcollateralization requirements the same for mortgage pay-through bonds as for the mortgage-backed

bonds?

Question 20-3

Question 20-4

What is a CMO? Explain why a CMO has been called as much of a marketing innovation as a financial

innovation.

Question 20-5

What is meant by a derivative investment?

Question 20-6

Name the four major classes of mortgage-related securities. As an issuer, explain the reasons for choosing one

type over another.

Question 20-7

What is the major difference between a CMO and the other types of mortgage-related securities?

Question 20-8

Why are CMOs overcollateralized?

Question 20-9

What is the purpose of the accrual tranche? Could a CMO exist without a Z class? What would be the difference

between the CMO with and without the accrual class?

Question 20-10

Which tranches in a CMO issue are least subject to price variances related to changes in market interest rates?

Why?

Question 20-11

What is the primary distinction between mortgage-related securities backed by residential mortgages and those

backed by commercial mortgages?

Question 20-12

Name the major types of credit enhancement used for commercial-backed mortgage securities.

Question 20-13

What is a “floater”/”inverse–floater” tranche in a CMO offering?

Question 20-14

What is the role of the “scaler” in structuring an (F) and (IF) structure?

Question 20-15

Why would anyone want to purchase an (F) or (IF) derivative type of investment?

Question 20-16

What are (IO) and (PO) strips? Which tends to be more volatile in price? Why?

Question 20-17

In what ways is a CMBS structure different from a CMO backed by residential mortgages? Why is default risk

in a CMBS offering given more attention?

Question 20-18

How do CDOs differ from CMBS?

Solution to Problems – Chapter 20

The Secondary Mortgage Market: CMOs and Derivative Securities

Problem 20-1

(a) The Initial WAC is simply the coupon rate of each tranche weighted by the initial tranche balance

Weighted

Tranche

Balance

Weighting

Coupon Rate

Avg Coupon

A

40,500,000

37.50%

8.25%

3.09%

B

22,500,000

20.83%

9.00%

1.87%

Z

45,000,000

41.67%

10.00%

4.17%

Total

$108,000,000

WAC = 9.13%

(b) To calculate the maturity of each tranche, the yearly interest and principal paid on each tranche must be calculated.

Mortgage Pool

10

0.00

0.00

0.00

0.00

Tranche B

Amount

$22,500

Rate

9.00%

Year

Beg. Bal

Interest

Principal

End Bal

1

$22,500.00

$2,025.00

$0.00

$22,500.00

2

22,500.00

2,025.00

0.00

22,500.00

3

22,500.00

2,025.00

0.00

22,500.00

4

22,500.00

2,025.00

13,144.65

9,355.35

5

9,355.35

841.98

9,355.35

0.00

6

0.00

0.00

0.00

0.00

7

0.00

0.00

0.00

0.00

8

0.00

0.00

0.00

0.00

9

0.00

0.00

0.00

0.00

10

0.00

0.00

0.00

0.00

(c) The weighted average coupon each year is found by weighting the coupon rate for each class by the outstanding balance

of that class.

A

B

Z

Total

WAC

Coupon

8.25%

9.00%

10.00%

End of Year

Balance

Balance

Balance

Balance

0

40500

22500

45000

108000

9.14%

1

28941

22500

49500

100941

9.28%

2

16226

22500

54450

93176

9.45%

3

2240

22500

59895

84635

9.69%

4

0

9355

65885

75240

9.88%

5

0

0

64905

64905

10.00%

6

0

0

53537

53537

10.00%

7

0

0

41031

41031

10.00%

8

0

0

27276

27276

10.00%

9

0

0

12144

12144

10.00%

(d)

Tranche a

Cash

Year

Beg. Bal

Interest

Principal

End Bal

Flow

1

$40,500.00

3,341.25

$11,558.86

$28,941.14

14,900.11

2

28,941.14

2,387.64

12,714.74

16,226.40

15,102.39

3

16,226.40

1,338.68

13,986.22

2,240.18

15,324.89

4

2,240.18

184.82

2,240.18

0.00

2,425.00

5

0.00

0.00

0.00

0.00

0.00

6

0.00

0.00

0.00

0.00

0.00

7

0.00

0.00

0.00

0.00

0.00

8

0.00

0.00

0.00

0.00

0.00

9

0.00

0.00

0.00

0.00

0.00

10

0.00

0.00

0.00

0.00

0.00

P V at

8.50%

$40,309

Tranche B

Cash

Year

Beg. Bal

Interest

Principal

End Bal

Flow

1

$22,500.00

$2,025.00

$0.00

$22,500.00

2,025.00

2

22,500.00

2,025.00

0.00

22,500.00

2,025.00

3

22,500.00

2,025.00

0.00

22,500.00

2,025.00

4

22,500.00

2,025.00

13,144.65

9,355.35

15,169.65

5

9,355.35

841.98

9,355.35

0.00

10,197.33

6

0.00

0.00

0.00

0.00

0.00

7

0.00

0.00

0.00

0.00

0.00

8

0.00

0.00

0.00

0.00

0.00

9

0.00

0.00

0.00

0.00

0.00

10

0.00

0.00

0.00

0.00

0.00

P V at

9.50%

$22,110

Tranche Z

Total

Cash

Year

Beg. Bal

Interest

Payment

End Bal

Flow

0

($45,000)

1

$45,000.00

4,500.00

0.00

$49,500.00

0.00

2

49,500.00

4,950.00

0.00

54,450.00

0.00

3

54,450.00

5,445.00

0.00

59,895.00

0.00

4

59,895.00

5,989.50

0.00

65,884.50

0.00

5

65,884.50

6,588.45

7,567.98

64,904.97

7,567.98

6

64,904.97

6,490.50

17,858.86

53,536.61

17,858.86

7

53,536.61

5,353.66

17,858.86

41,031.42

17,858.86

8

41,031.42

4,103.14

17,858.86

27,275.70

17,858.86

9

27,275.70

2,727.57

17,858.86

12,144.42

17,858.86

10

12,144.42

1,214.44

13,358.86

0.00

13,358.86

IRR

10.00%

P V at

9.75%

$45,768

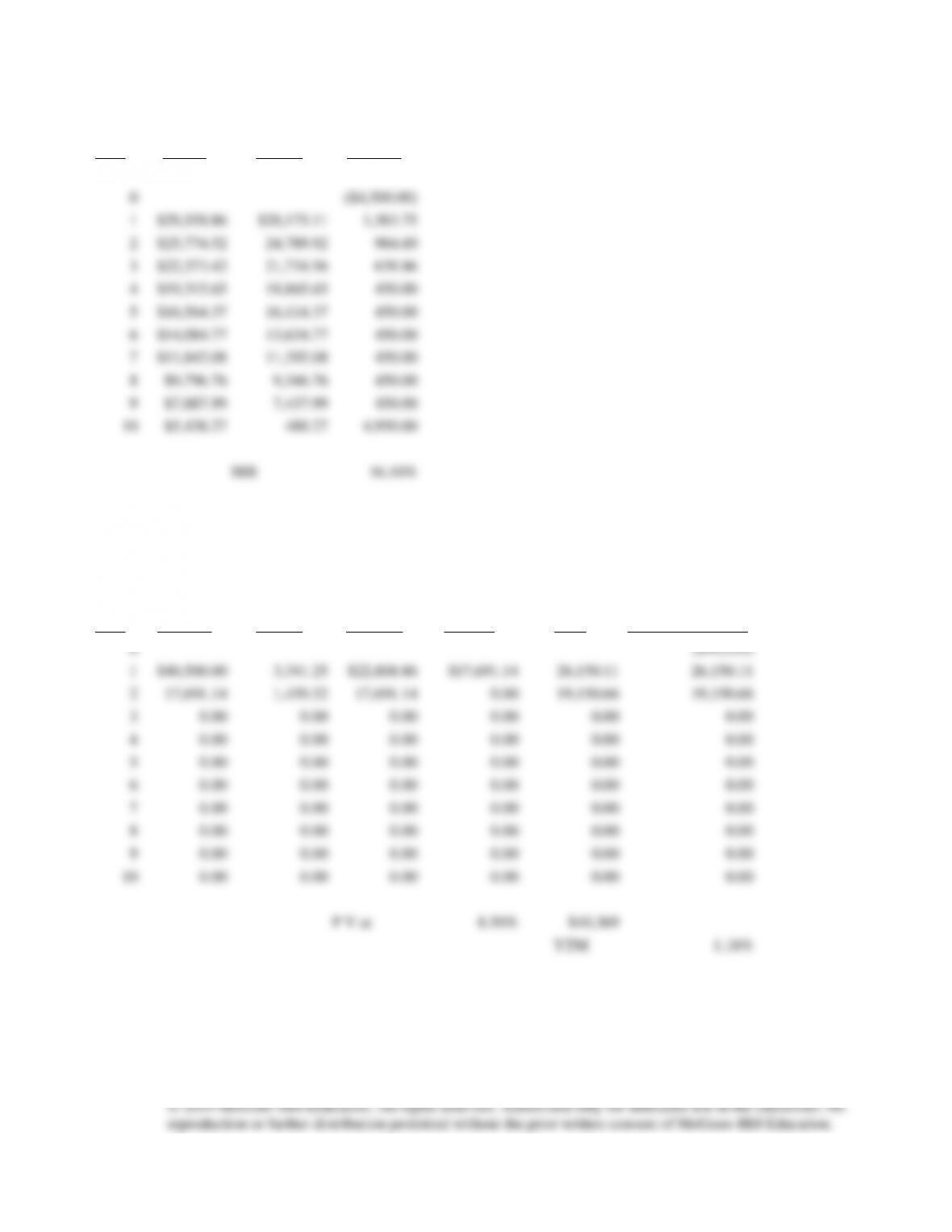

(e)

Residual Class

Total

Other

Year

in pool

Classes

Residual

0

($4,500.00)

1

$18,308.86

$16,925.11

1,383.75

2

$18,308.86

17,127.39

1,181.47

3

$18,308.86

17,349.89

958.96

4

$18,308.86

17,594.65

714.20

5

$18,308.86

17,765.30

543.55

6

$18,308.86

17,858.86

450.00

7

$18,308.86

17,858.86

450.00

8

$18,308.86

17,858.86

450.00

9

$18,308.86

17,858.86

450.00

10

$18,308.86

13,358.86

4,950.00

IRR

19.10%

(f)

Assuming 10% prepayment

Mortgage Pool

Year

Beg. Bal

Payment

Interest

Principal

End Bal

Prepayment

1

$112,500.00

$18,308.86

11,250.00

$18,308.86

$94,191.14

11250.00

2

94,191.14

$16,355.40

9,419.11

$16,355.40

$77,835.74

9419.11

3

77,835.74

$14,589.84

7,783.57

$14,589.84

$63,245.90

7783.57

4

63,245.90

$12,991.06

6,324.59

$12,991.06

$50,254.84

6324.59

5

50,254.84

$11,538.88

5,025.48

$11,538.88

$38,715.96

5025.48

6

38,715.96

$10,213.17

3,871.60

$10,213.17

$28,502.79

3871.60

7

28,502.79

$8,991.80

2,850.28

$8,991.80

$19,510.99

2850.28

8

19,510.99

$7,845.66

1,951.10

$7,845.66

$11,665.33

1951.10

9

11,665.33

$6,721.45

1,166.53

$6,721.45

$4,943.88

1166.53

10

4,943.88

$5,438.27

494.39

$4,943.88

$0.00

494.39

Tranche A

Cash

Year

Beg. Bal

Interest

Principal

End Bal

Flow

1

$40,500.00

3,341.25

$22,808.86

$17,691.14

26,150.11

2

17,691.14

1,459.52

17,691.14

0.00

19,150.66

3

0.00

0.00

0.00

0.00

0.00

4

0.00

0.00

0.00

0.00

0.00

5

0.00

0.00

0.00

0.00

0.00

6

0.00

0.00

0.00

0.00

0.00

7

0.00

0.00

0.00

0.00

0.00

8

0.00

0.00

0.00

0.00

0.00

9

0.00

0.00

0.00

0.00

0.00

10

0.00

0.00

0.00

0.00

0.00

P V at

8.50%

$40,369

Tranche B

Cash

Year

Beg. Bal

Interest

Principal

End Bal

Flow

1

$22,500.00

$2,025.00

$0.00

$22,500.00

2,025.00

2

22,500.00

2,025.00

3,614.26

18,885.74

5,639.26

3

18,885.74

1,699.72

18,885.74

0.00

20,585.46

4

0.00

0.00

0.00

0.00

0.00

5

0.00

0.00

0.00

0.00

0.00

6

0.00

0.00

0.00

0.00

0.00

7

0.00

0.00

0.00

0.00

0.00

8

0.00

0.00

0.00

0.00

0.00

9

0.00

0.00

0.00

0.00

0.00

10

0.00

0.00

0.00

0.00

0.00

P V at

9.50%

$22,232

Tranche Z

Total

Cash

Year

Beg. Bal

Interest

Payment

End Bal

Flow

0

($45,000)

1

$45,000.00

4,500.00

0.00

$49,500.00

0.00

2

49,500.00

4,950.00

0.00

54,450.00

0.00

3

54,450.00

5,445.00

1,149.10

58,745.90

1,149.10

4

58,745.90

5,874.59

18,865.65

45,754.84

18,865.65

5

45,754.84

4,575.48

16,114.37

34,215.96

16,114.37

6

34,215.96

3,421.60

13,634.77

24,002.79

13,634.77

7

24,002.79

2,400.28

11,392.08

15,010.99

11,392.08

8

15,010.99

1,501.10

9,346.76

7,165.33

9,346.76

9

7,165.33

716.53

7,437.99

443.88

7,437.99

10

443.88

44.39

488.27

0.00

488.27

IRR

10.00%

P V at

9.75%

$45,588

Residual

Total

Other

Year

in pool

Classes

Residual

0

($4,500.00)

1

$29,558.86

$28,175.11

1,383.75

2

$25,774.52

24,789.92

984.60

3

$22,373.42

21,734.56

638.86

4

$19,315.65

18,865.65

450.00

5

$16,564.37

16,114.37

450.00

6

$14,084.77

13,634.77

450.00

7

$11,842.08

11,392.08

450.00

8

$9,796.76

9,346.76

450.00

9

$7,887.99

7,437.99

450.00

10

$5,438.27

488.27

4,950.00

IRR

16.10%

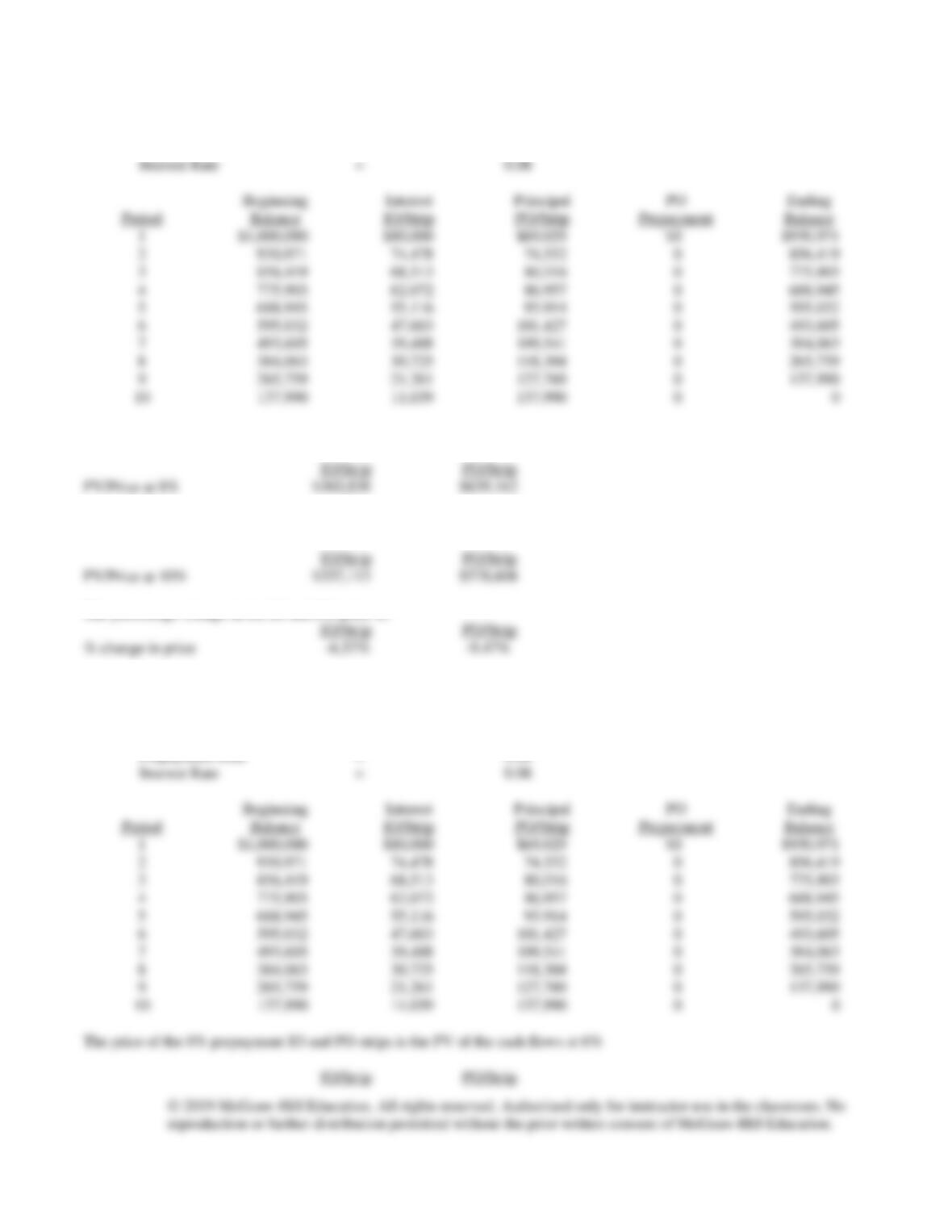

(g)

10 percent price increase after issue

Tranche A

Cash

Year

Beg. Bal

Interest

Principal

End Bal

Flow

10% Price Increase

0

($44,550)

1

$40,500.00

3,341.25

$22,808.86

$17,691.14

26,150.11

26,150.11

2

17,691.14

1,459.52

17,691.14

0.00

19,150.66

19,150.66

3

0.00

0.00

0.00

0.00

0.00

0.00

4

0.00

0.00

0.00

0.00

0.00

0.00

5

0.00

0.00

0.00

0.00

0.00

0.00

6

0.00

0.00

0.00

0.00

0.00

0.00

7

0.00

0.00

0.00

0.00

0.00

0.00

8

0.00

0.00

0.00

0.00

0.00

0.00

9

0.00

0.00

0.00

0.00

0.00

0.00

10

0.00

0.00

0.00

0.00

0.00

0.00

P V at

8.50%

$40,369

YTM

1.18%

Tranche B

Cash

Year

Beg. Bal

Interest

Principal

End Bal

Flow

10% Price Increase

0

($24,750)

1

$22,500.00

$2,025.00

$0.00

$22,500.00

2,025.00

2,025.00

2

22,500.00

2,025.00

3,614.26

18,885.74

5,639.26

5,639.26

3

18,885.74

1,699.72

18,885.74

0.00

20,585.46

20,585.46

4

0.00

0.00

0.00

0.00

0.00

0.00

5

0.00

0.00

0.00

0.00

0.00

0.00

6

0.00

0.00

0.00

0.00

0.00

0.00

7

0.00

0.00

0.00

0.00

0.00

0.00

8

0.00

0.00

0.00

0.00

0.00

0.00

9

0.00

0.00

0.00

0.00

0.00

0.00

10

0.00

0.00

0.00

0.00

0.00

0.00

P V at

9.50%

$22,232

YTM

5.12%

Class Z

Total

Cash

Year

Beg. Bal

Interest

Payment

End Bal

Flow

10% Price Increase

0

($45,000)

($49,500)

1

$45,000.00

4,500.00

0.00

$49,500.00

0.00

0.00

2

49,500.00

4,950.00

0.00

54,450.00

0.00

0.00

3

54,450.00

5,445.00

1,149.10

58,745.90

1,149.10

1,149.10

4

58,745.90

5,874.59

18,865.65

45,754.84

18,865.65

18,865.65

5

45,754.84

4,575.48

16,114.37

34,215.96

16,114.37

16,114.37

6

34,215.96

3,421.60

13,634.77

24,002.79

13,634.77

13,634.77

7

24,002.79

2,400.28

11,392.08

15,010.99

11,392.08

11,392.08

8

15,010.99

1,501.10

9,346.76

7,165.33

9,346.76

9,346.76

9

7,165.33

716.53

7,437.99

443.88

7,437.99

7,437.99

10

443.88

44.39

488.27

0.00

488.27

488.27

YTM

8.18%

PV at

9.75%

$45,588

Problem 20-2

(a) Beginning Balance = $1,000,000

Prepayment Rate = 0.00

PV/Price at 6%

$387,480

$709,390

IO/Strip

PO/Strip

$221,902

Scale

Interest Rate

Interest Payable

(F) Floater

0.50

0.08

1,000,000

0.50

0.08

$160,000

Scale

Interest Rate

Interest Payable

(F) Floater

0.60

0.08

800,000

0.40

0.08

$160,000

Beginning

Interest

Principal

PO

Ending

Period

Balance

IO/Strip

PO/Strip

Prepayment

Balance

1

$1,000,000

$80,000

$69,029

$200,000

$730,971

2

730,971

58,478

58,536

146,194

526,241

3

526,241

42,099

49,474

105,248

371,518

4

371,518

29,721

41,637

74,304

255,578

5

255,578

20,446

34,839

51,116

169,623

6

169,623

13,570

28,913

33,925

106,785

7

106,785

8,543

23,698

21,357

61,730

8

61,730

4,938

19,015

12,346

30,369

9

30,369

2,430

14,601

6,074

9,695

10

9,695

776

9,695

0

0

The price of the 20% prepayment IO and PO strips is the PV of the cash flows at 6%

(c) Impact of 2% increase in interest rate under 50% proportions

Scale

Interest Rate

Interest Payable

(F) Floater

$1,000,000

0.50

0.10

$100,000

(IF) Inverse Floater

1,000,000

0.50

0.06

60,000

$160,000

F receives $100,000 and IF receives $60,000

Impact of 2% increase in interest rate under 60% / 40% proportions

Scale

Interest Rate

Interest Payable

(F) Floater

$1,200,000

0.60

0.10

$120,000

(IF) Inverse Floater

800,000

0.40

0.05

40,000

$160,000

Impact of 2% decrease in interest rate under 50% proportions

Scale

Interest Rate

Interest Payable

(F) Floater

$1,000,000

0.50

0.06

$60,000

(IF) Inverse Floater

1,000,000

0.50

0.10

100,000

$160,000

Impact of 2% decrease in interest rate under 60% / 40% proportions

Scale

Interest Rate

Interest Payable

(F) Floater

$1,200,000

0.60

0.06

$72,000

(IF) Inverse Floater

800,000

0.40

0.11

88,000

$160,000

Summary

Yield

2% increase

2% decrease

Proportions

of Issue

in interest rate

in interest rate

Case (a)

(F)

50%

8%

10

6

(IF)

50%

8%

6

10

Case (b)

(F)

60%

8%

10

6

(IF)

40%

8%

5

11

In case (a) there is an equal impact of changing interest rates on the F and IF yields, that is, each either increases or decreases

by 2%. In case (b) however, IF investors will experience greater volatility in yield. This is because the proportion of each

class comprising the tranche is now 60 – 40. Therefore, for each 1% change in the underlying interest rate, IF investors will

realize a change in yield of 1.5%.

Problem 20-4

See table below:

Prepayment

Rate

IRR on

Residual

0.00%

19.10%

5.00%

17.33%

10.00%

16.10%

15.00%

15.53%

20.00%

14.99%

25.00%

14.74%

30.00%

14.74%

Problem 20-5

See below:

Libor

(F) Rate

(IF) Rate

F interest

IF Interest

Total interest

0%

0.00%

24.00%

$0

$1,200,000

$1,200,000

1%

1.00%

21.00%

150,000

1,050,000

1,200,000

2%

2.00%

18.00%

300,000

900,000

1,200,000

3%

3.00%

15.00%

450,000

750,000

1,200,000

4%

4.00%

12.00%

600,000

600,000

1,200,000

5%

5.00%

9.00%

750,000

450,000

1,200,000

6%

6.00%

6.00%

900,000

300,000

1,200,000

7%

7.00%

3.00%

1,050,000

150,000

1,200,000

8%

8.00%

0.00%

1,200,000

0

1,200,000

Note that the inverse floater now starts at a higher rate with Libor equal to 0% and decreases at a faster rate than before.

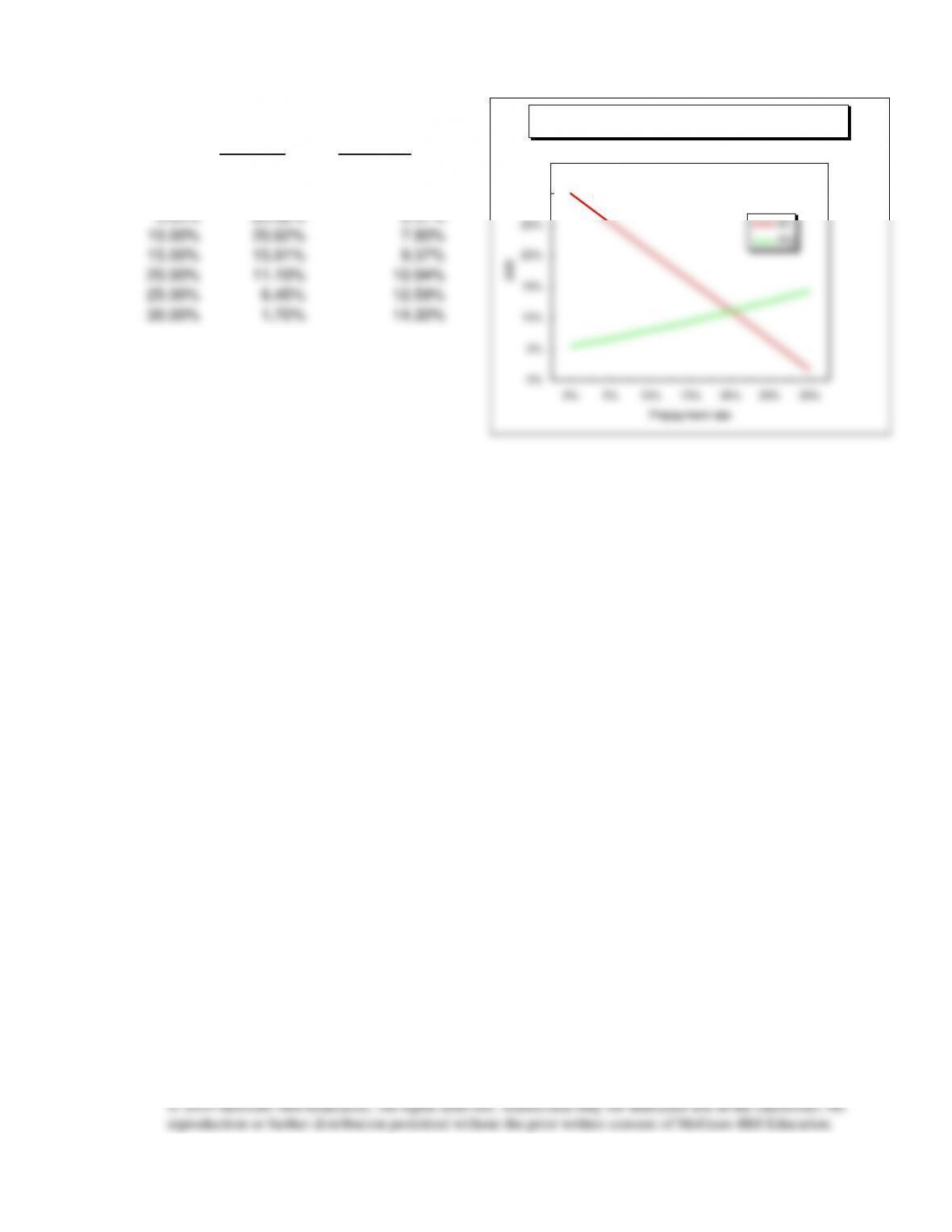

Problem 20-6

See below:

IRR of IO

IRR of PO

Prepayment

0.00%

30.00%

5.38%

5.00%

25.32%

6.57%

10.00%

20.62%

7.90%

15.00%

15.91%

9.37%

20.00%

11.19%

10.94%

25.00%

6.45%

12.59%

30.00%

1.70%

14.30%

IRR on IO and PO vs. Prepayment

0%

5%

10%

15%

20%

25%

30%

35%

0% 5% 10% 15% 20% 25% 30%

Prepayment rate

IRR

IO

PO

Problem 20-7

Solutions to Problems – Chapter 20 Appendix

The Secondary Mortgage Market: CMOs and Derivative Securities

Problem 20A-1

(a) Interest Payments of a Corporate Bond = $10,000

Duration Calculation of a Corporate Bond:

Weighting

Present

Weighted PV

Period

Payment

Factor

Value

of Payment

0

1

10,000

1.0

0.9091

14,795

2

10,000

2.0

0.8264

26,901

3

10,000

3.0

0.7513

36,693

4

10,000

4.0

0.6830

44,464

5

10,000

5.0

0.6209

50,527

5

100,000

5.0

0.6209

191,532

Total

$364,903

Duration = Total weighted present value of payments

(b) New price for corporate bond if interest rate falls from 10% to 7%

New price for mortgage bond if interest rate falls from 10% to 7%

Difference = 10% –7% = 3.00%