Solutions to Questions – Chapter 18

Structuring Real Estate Investments: Organizational Forms and Joint Ventures

Question 18-1

What is the difference between an IRR preference and an IRR lookback?

Question 18-2

What is the advantage of the limited partnership ownership form for real estate syndications?

Question 18-3

How can the general partner-syndicator structure the partnership to offer incentives to limited partners?

Question 18-4

Why is the Internal Revenue Service concerned with how partnership agreements in real estate are structured?

Question 18-5

What is the main difference between the way a partnership is taxed versus the way a corporation is taxed?

Question 18-6

What are special allocations?

Question 18-7

What causes the after-tax IRR (ATIRRe) for the general partner to differ from that of the limited partner?

Question 18-8

What is the significance of capital accounts? What causes the balance in a capital account to change each year?

Question 18-9

How does the risk associated with investment in a partnership differ for the general partner versus a limited

partner?

Question 18-10

What are the different ways that the general partner is compensated?

Question 18-11

How do you think the federal income tax policy affects the desirability of investing in real estate partnerships?

Question 18-12

What concerns should an investor in a real estate syndication have regarding general partners?

Question 18-13

Differentiate between public and private syndications? What is an accredited investor? Why is the distinction

used?

Question 18-14

How are general partners usually compensated in a syndication? What major concerns should investors consider

Question 18 – 15

What is the main difference between organizing a real estate venture a corporation versus a general partnership?

How does a limited partnership have some of the characteristics of both?

Solutions to Problems – Chapter 18

Partnerships, Joint Ventures, and Syndications

INTRODUCTION

The problems in this chapter parallel that of the example in the textbook. We have assumed the syndication expenses can not

be expensed or amortized. That is, they are capitalized but not depreciated. Note that this is similar to the tax treatment of

land. The proper way of handling syndication fees is somewhat controversial and depends on the specific nature of the

syndication expense. Some commentators have suggested that syndication costs might be amortizable over the life of a

limited partnership, but most practitioners are dubious of this position. Most writers suggest that fees paid for services

rendered in connection with acquisition of the property can be capitalized as part of the basis of the acquired asset and

depreciated over the recovery period of that asset. Examples of service relating to the acquisition of an asset include

negotiation of a lease of the partnership’s property, negotiation of the partnership’s purchase of real estate, and legal and

brokerage fees paid by the syndication with respect to acquisition of the asset. However, legal and marketing fees related to

the creation of the syndication securities are capitalized but cannot be depreciated. Rather, these fees would be deductible

only upon termination or liquidation of the partnership (see Promoters’ and Managers’ Compensation, Page 511).

For simplicity, we have chosen to simply assume that all “syndication fees” are capitalized but not depreciated. However, the

instructor may want to bring this issue to the attention of the students.

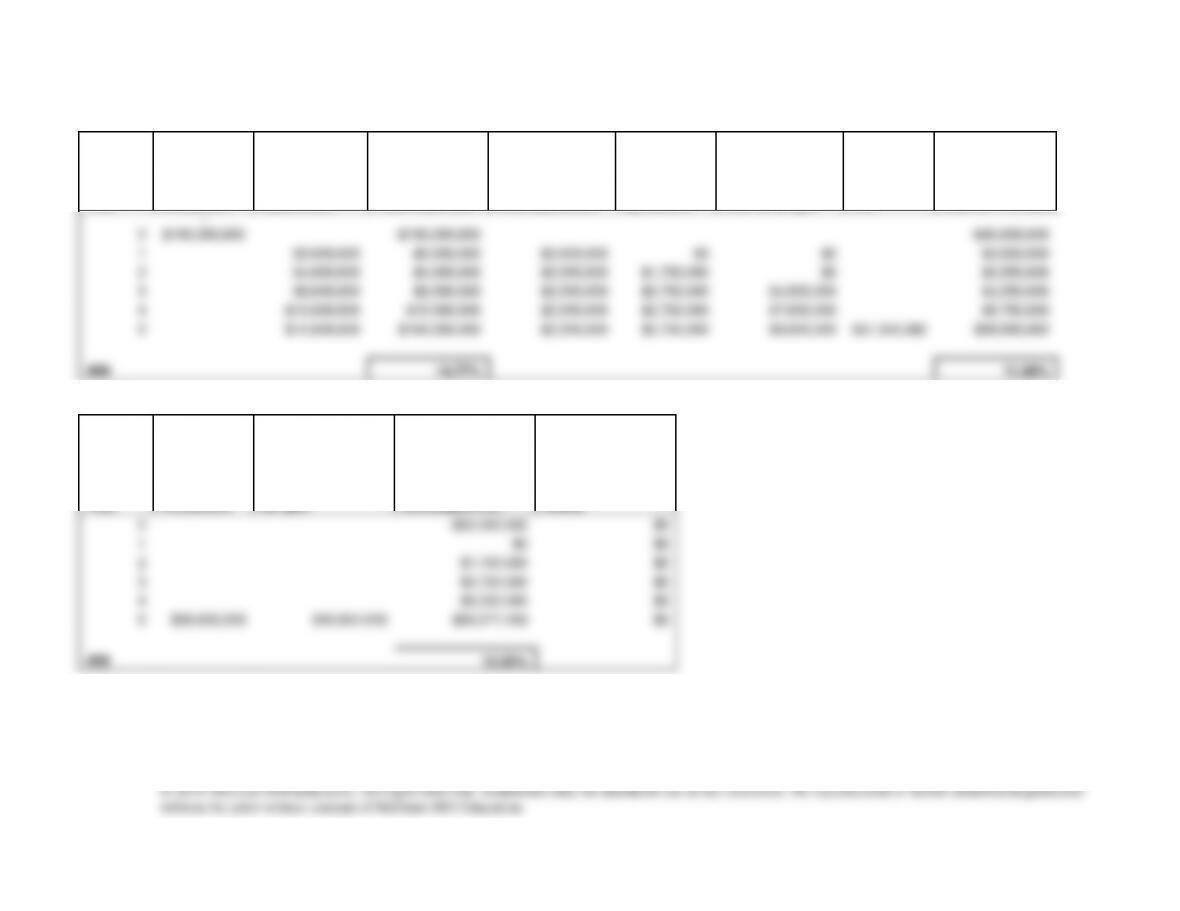

Problem 18-1

Table 1

Year

Initial

Investment

Cash flow from

Operations

Total Cash flow

ABC fund return

from operations

Newtown

Developers

Inc. return

from

operations

Remaining

operating cash

flow to be split

ABC fund

from sale

for 11%

IRR

ABC fund cash

flow for 11% IRR

0

–

$100,000,000

-$100,000,000

-$45,000,000

1

$2,000,000

$2,000,000

$2,000,000

$0

$0

$2,000,000

2

$4,000,000

$4,000,000

$2,250,000

$1,750,000

$0

$2,250,000

3

$9,000,000

$9,000,000

$2,250,000

$2,750,000

$4,000,000

$4,250,000

4

$12,000,000

$12,000,000

$2,250,000

$2,750,000

$7,000,000

$5,750,000

5

$14,000,000

$164,000,000

$2,250,000

$2,750,000

$9,000,000

$51,345,082

$58,095,082

IRR

14.77%

11.00%

Table 1 continued..

Year

Newtown

Developers

Inc. return of

initial

investment

Remaining cash

flow from sale to

be split

Newtown

Developers Inc.

Check

0

-$55,000,000

$0

1

$0

$0

2

$1,750,000

$0

3

$4,750,000

$0

4

$6,250,000

$0

5

$55,000,000

$43,654,918

$84,077,459

$0

IRR

12.62%

Year

Cash flow

from

Operations

ABC fund Inc.

return from

operations

Newtown

Developers Inc.

return from

operations

Remaining

operating cash

flow to be split

Year

ABC fund

Inc. cash

flow from

Operations

ABC fund Inc.

return of

initial

investment

ABC fund

additional

cash flow

from Sale

Total Cash

Flow

0

–

$45,000,000

1

$2,000,000

$2,000,000

$0

$0

1

$2,000,000

$2,000,000

2

$4,000,000

$2,250,000

$1,750,000

$0

2

$2,250,000

$2,250,000

3

$9,000,000

$2,250,000

$2,750,000

$4,000,000

3

$4,250,000

$4,250,000

4

$12,000,000

$2,250,000

$2,750,000

$7,000,000

4

$5,750,000

$5,750,000

5

$14,000,000

$2,250,000

$2,750,000

$9,000,000

5

$6,750,000

$45,000,000

$6,345,082

$58,095,082

11.00%

Year

ABC fund

Inc.

Newtown Developers

Inc.

0

-$45,000,000

-$55,000,000

1

$2,000,000

$0

2

$2,250,000

$1,750,000

3

$4,250,000

$4,750,000

4

$5,750,000

$6,250,000

5

$79,922,541

$84,077,459

IRR

17.30%

12.62%

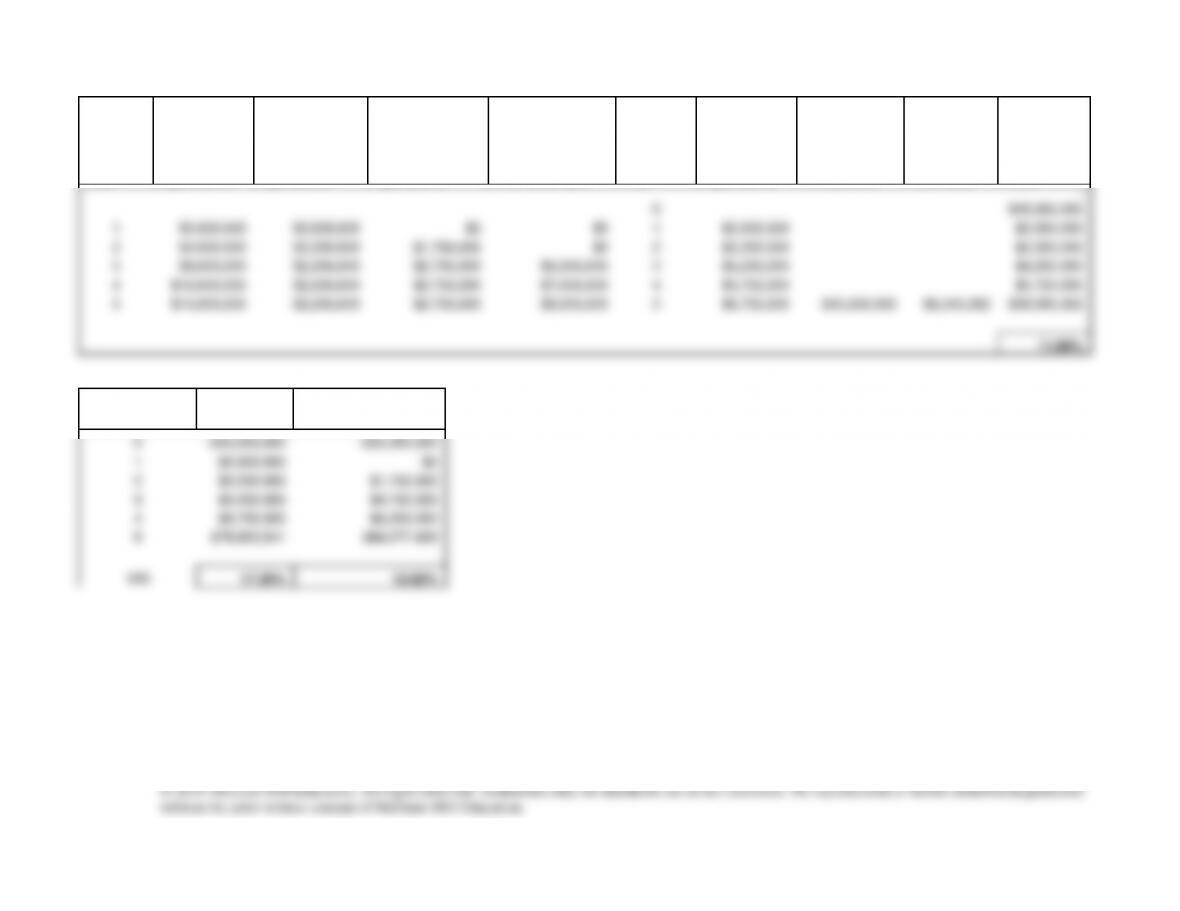

Problem 18-2

(REFER TO TEMPLATE 18_1.XLS)

ASSUMPTIONS:

COST BREAKDOWN

FINANCING

Land

1,000,000

Loan Amount

8,000,000

Improvements

9,000,000

Interest rate

11.00%

Points

100,000

Term

25

Subtotal

10,100,000

Points

100,000

Organization fee

100,000

Pmts / Year

12

Syndication expenses

100,000

Amortized over loan term

Total funding required

10,300,000

Annual Pmt

940,909

Years amortized

5

PARTNERSHIP FACTS AND EQUITY REQUIREMENTS

Equity capital

Cash distrib.

Tax. Income

Alloc. gain

contribution

Operations

Operations

Sale

General partner

10.00%

10.00%

10.00%

15.00%

Limited Partners

90.00%

90.00%

90.00%

85.00%

# of Limited Partners

35

OPERATING AND TAX PROJECTIONS

INITIAL EQUITY REQUIREMENTS

Potential gross income

1,750,000

Land

1,000,000

Projected growth in PGI

3.00%

Improvements

9,000,000

Vacancy and coll. Loss

10.00%

of PGI

Points on Loan

100,000

Operating Expenses

35.00%

of EGI

Organization fee

100,000

Depreciable Life

31.5

years

Syndication fee

100,000

Projected Resale

13,500,000

Total

10,300,000

Tax rate-Limited Partner

28.00%

Less loan

8,000,000

Tax rate-General Partner

28.00%

Equity

2,300,000

Selling Expenses

5.00%

General Partner

230,000

Holding Period

5

years

Limited Partners

2,070,000

Loan Information:

Year

1

2

3

4

5

Interest

876,833

869,419

861,146

851,916

841,618

Loan Balance

7,935,925

7,864,435

7,784,672

7,695,680

7,596,389

Depreciation per year

285,714

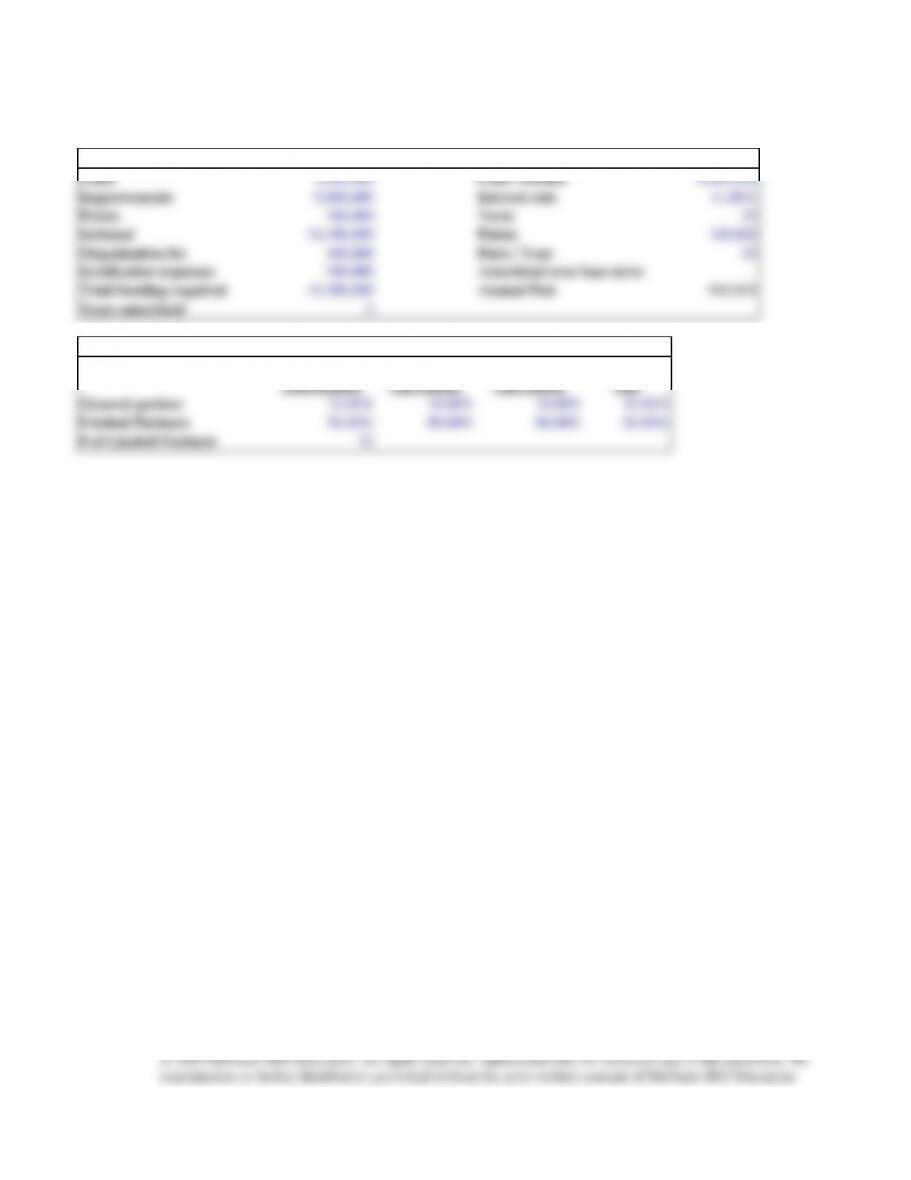

STATEMENT OF BEFORE-TAX CASH FLOW

Year

1

2

3

4

5

Potential gross income

1,750,000

1,802,500

1,856,575

1,912,272

1,969,640

Vacancy and collection loss

175,000

180,250

185,658

191,227

196,964

Effective gross income

1,575,000

1,622,250

1,670,918

1,721,045

1,772,676

Operating Expenses

551,250

567,788

584,821

602,366

620,437

Net operating income

1,023,750

1,054,463

1,086,096

1,118,679

1,152,240

Debt service

940,909

940,909

940,909

940,909

940,909

Before-tax cash flow

82,841

113,554

145,188

177,771

211,331

Distribution of BTCF

General Partner

8,284

11,355

14,519

17,777

21,133

Limited Partners

74,557

102,199

130,669

159,994

190,198

STATEMENT OF INCOME (LOSS)

Year

1

2

3

4

5

Net operating income

1,023,750

1,054,463

1,086,096

1,118,679

1,152,240

Less: Interest

876,833

869,419

861,146

851,916

841,618

Depreciation

285,714

285,714

285,714

285,714

285,714

Amortization of:

Organization fee

20,000

20,000

20,000

20,000

20,000

Loan fee

4,000

4,000

4,000

4,000

84,000

Taxable income

(162,798)

(124,670)

(84,764)

(42,951)

(79,092)

Distribution of Taxable Income

General Partner

(16,280)

(12,467)

(8,476)

(4,295)

(7,909)

Limited Partners

(146,518)

(112,203)

(76,287)

(38,656)

(71,183)

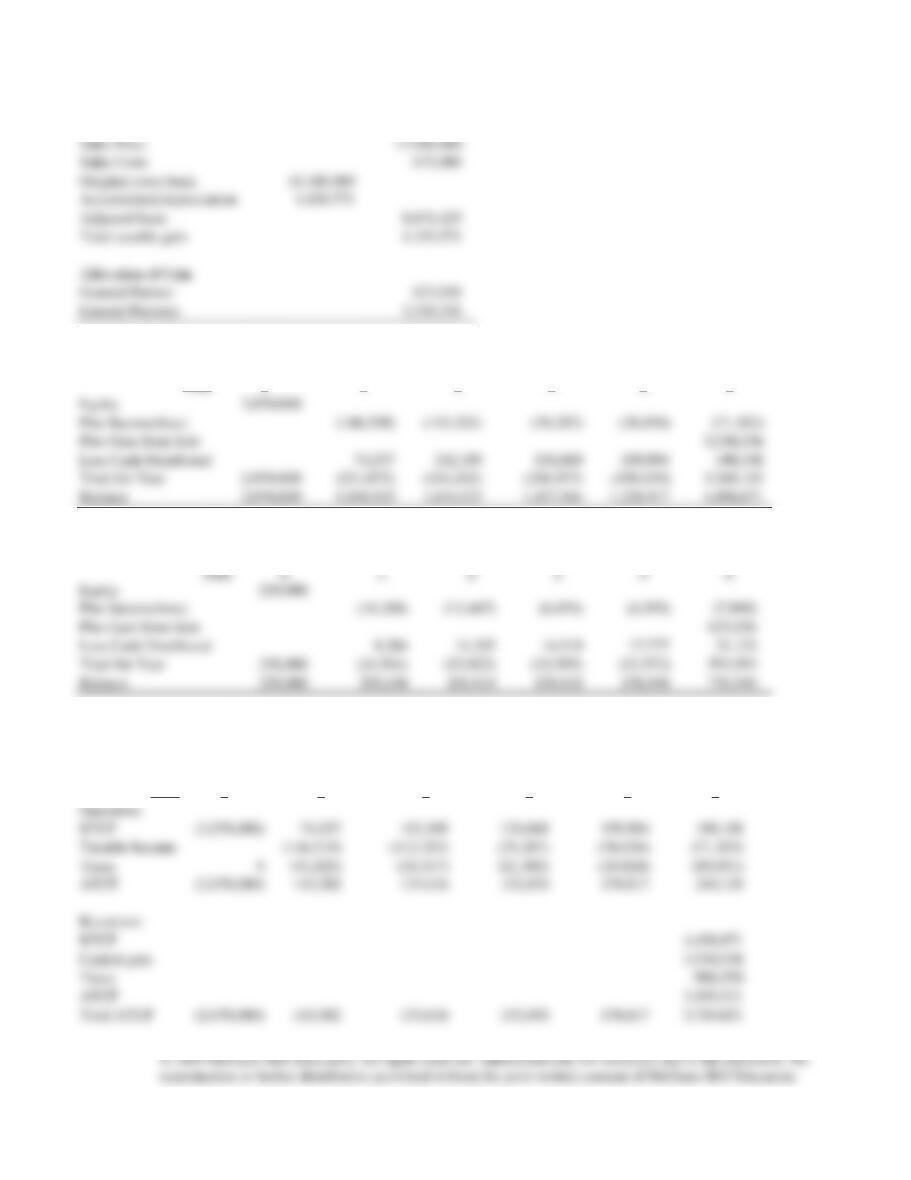

CALCULATION OF CAPITAL GAIN

Sales Price

13,500,000

Sales Costs

675,000

Original costs basis

10,100,000

Accumulated depreciation

1,428,571

Adjusted basis

8,671,429

Total taxable gain

4,153,571

Allocation of Gain

General Partner

623,036

Limited Partners

3,530,536

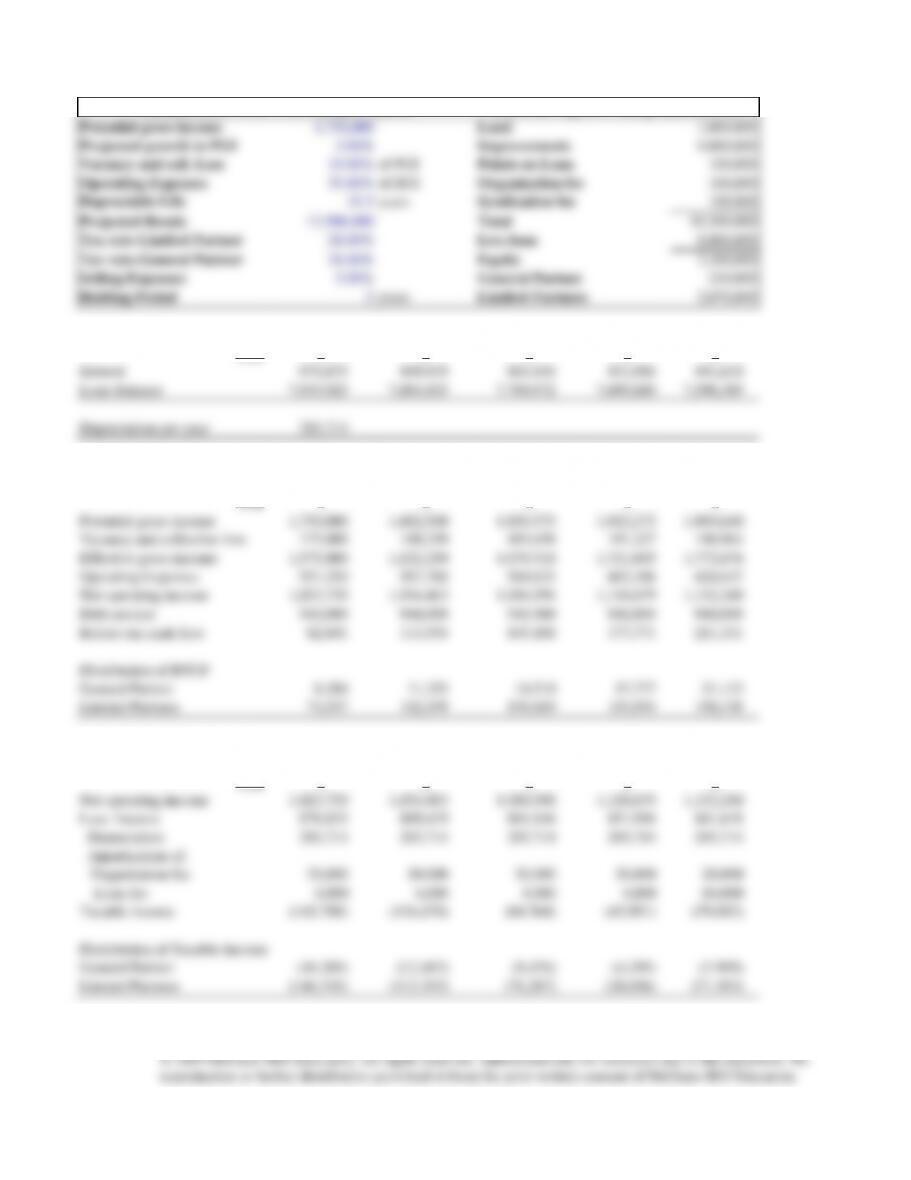

CAPITAL ACCOUNTS – LIMITED PARTNERS

Year

0

1

2

3

4

5

Equity

2,070,000

Plus Income(loss)

(146,518)

(112,203)

(76,287)

(38,656)

(71,183)

Plus Gain from Sale

3,530,536

Less Cash Distributed

74,557

102,199

130,669

159,994

190,198

Total for Year

2,070,000

(221,075)

(214,402)

(206,957)

(198,650)

3,269,155

Balance

2,070,000

1,848,925

1,634,523

1,427,566

1,228,917

4,498,071

CAPITAL ACCOUNTS – GENERAL PARTNER

Year

0

1

2

3

4

5

Equity

230,000

Plus Income(loss)

(16,280)

(12,467)

(8,476)

(4,295)

(7,909)

Plus Gain from Sale

623,036

Less Cash Distributed

8,284

11,355

14,519

17,777

21,133

Total for Year

230,000

(24,564)

(23,822)

(22,995)

(22,072)

593,993

Balance

230,000

205,436

181,614

158,618

136,546

730,540

(a)

ATIRR:

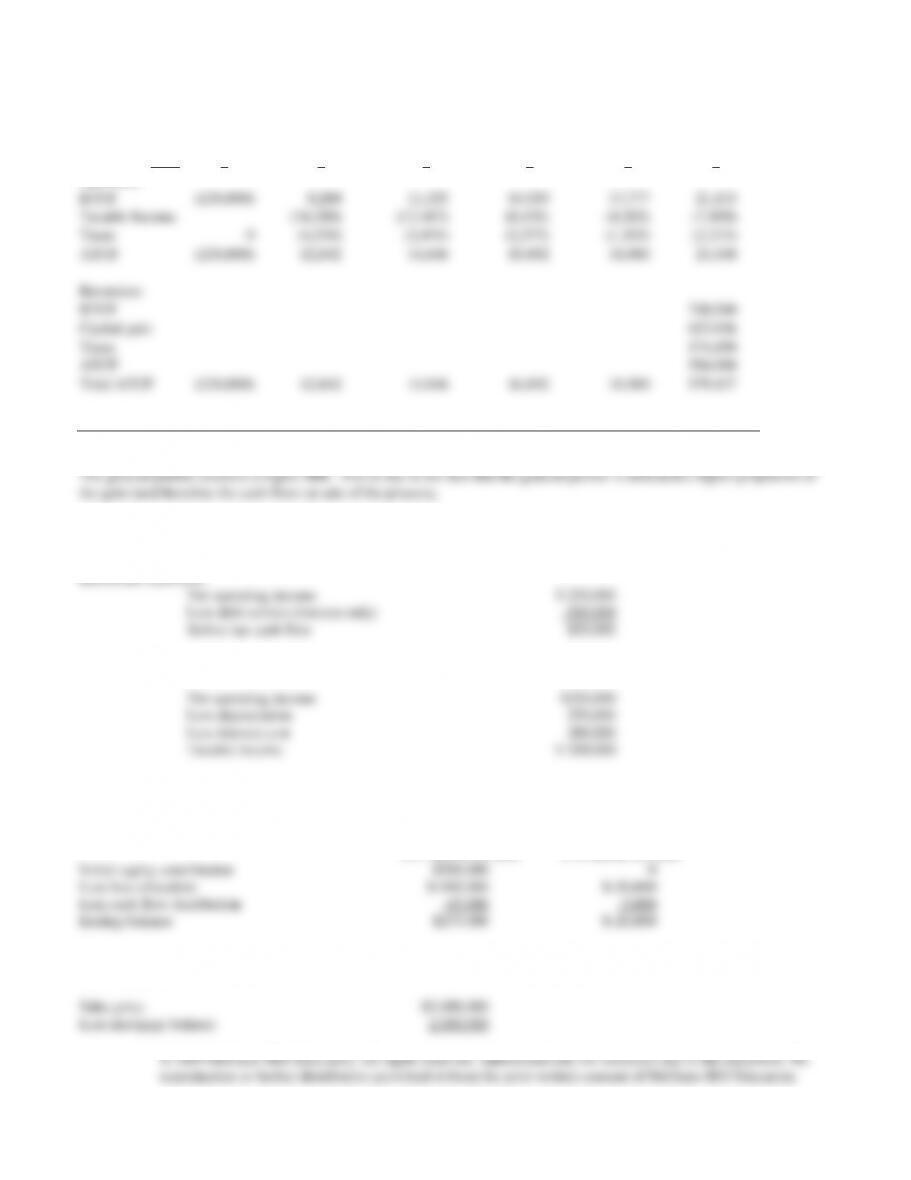

AFTER-TAX CASH FLOW AND ATIRR – LIMITED PARTNERS

Year

0

1

2

3

4

5

Operation:

BTCF

(2,070,000)

74,557

102,199

130,669

159,994

190,198

Taxable Income

(146,518)

(112,203)

(76,287)

(38,656)

(71,183)

Taxes

0

(41,025)

(31,417)

(21,360)

(10,824)

(19,931)

ATCF

(2,070,000)

115,582

133,616

152,030

170,817

210,129

Reversion:

BTCF

4,498,071

Capital gain

3,530,536

Taxes

988,550

ATCF

3,509,521

Total ATCF

(2,070,000)

115,582

133,616

152,030

170,817

3,719,651

ATIRR

17.11%

(b)

ATIRR:

AFTER-TAX CASH FLOW AND ATIRR – GENERAL PARTNER

Year

0

1

2

3

4

5

Operation:

BTCF

(230,000)

8,284

11,355

14,519

17,777

21,133

Taxable Income

(16,280)

(12,467)

(8,476)

(4,295)

(7,909)

Taxes

0

(4,558)

(3,491)

(2,373)

(1,203)

(2,215)

ATCF

(230,000)

12,842

14,846

16,892

18,980

23,348

Reversion:

BTCF

730,540

Capital gain

623,036

Taxes

174,450

ATCF

556,090

Total ATCF

(230,000)

12,842

14,846

16,892

18,980

579,437

ATIRR

24.53%

(c)

Problem 18-3

Before tax cash flow:

Taxable income:

(a)

Capital Accounts after First Year of Operations

A’s Capital Account B’s Capital Account

(b)

Cash from sale

(c)

Cash distributions from sale

(d)

Capital gain from sale after 1 year:

(e)

Capital Accounts after Sale of Building

A’s Capital Account B’s Capital Account

Problem 18-4

The general partner’s return is now 13.68% versus 22.24% and the limited partner’s return is also 13.68% versus 13.15%.