Solutions to Questions – Chapter 16

Financing Project Development

Question 16-1

What are the sources of risk associated with project development?

Question 16-2

What are two development strategies that many developers follow?

Question 16-3

What contingencies are commonly found in permanent or take-out loan commitments? Why are they used? What

happens if they are not met by the developer?

Question 16-4

What is a standby commitment? When and why is it used?

Question 16-5

A presale agreement is said to be equivalent to a take-out commitment. What will the construction lender be

concerned about if the developer plans to use such an agreement in lieu of a take-out?

Question 16-6

What is the major concern construction lenders express about the income approach to estimating value? Why do

they prefer to use the cost approach when possible? In the latter case, if the developer has owned the land for five

years prior to development would the cost approach be more effective? Why or why not?

Question 16-7

What do we mean by overage in a retail lease agreement? How might it be calculated?

Question 16-8

What are “gross ups” in determining tenant reimbursements for operating expenses? Why are they used?

Question 16-9

What is sensitivity analysis? How might it be used in real estate development?

Question 16-10

It is sometimes said that land represents “residual” value. This statement reflects the fact that improvement costs

do not vary materially from one location to another whereas rents vary considerably. Hence, land values reflect

changes in rents (both up and down) from location to location. Do you agree or disagree?

Question 16-11

What are holdbacks in construction lending? Why is the practice of “holdbacks” used?

Solutions to Problems – Chapter 16

Financing Project Development

Problem 16-1

(a)

240 Unit Proposal

250 Unit Revised Proposal

Gross Revenue

$ 2,851,200

$ 2,970,000

Vacancy

142,000

148,500

Expenses

997,920

1,782,000

Net Operating Income

$ 1,710,720

$ 1,782,000

Cost

$22,000,000

$22,800,000

Return on Total Cost

7.78%

7.82%

(b) Assume a 240 percent luxury project at 83,000 per unit.

Problem 16-2

Parker Road Plaza

The following conventions were used:

Depreciation Schedule:

Category

Depreciation Period

Method

Capital Improvements (90%)

31.5 years

S/L

Tenant Improvements (10%)

7.0 years

DDB

The total amount to be depreciated is the total direct costs financed, $11,865,000, plus the estimated interest carry. These

costs are split between capital improvements (90% of the total) and tenant improvements (10% of the total). The mid-year

convention was not used on either the 31.5 year straight-line depreciation for capital improvements or the 7 year double

declining balance used for the tenant improvements. However, the use of double declining balance does allow for switching

to straight-line after the fourth year (with a double declining balance and a depreciation period of 7 years.)

Amortization Schedule:

Category

Depreciation Period

Method

Construction loan fees

1 year-

S/L

Permanent loan fees

10 years

S/L

The construction loan fee and the permanent loan fee are amortized over the lives of each loan, respectively. The

construction loan fee of $253,591 is amortized over the one year construction time period, while the permanent loan fee of

$316,988 is amortized over the ten year life of the permanent loan.

If the property is sold before the end of the depreciation/amortization periods, the basis in the property must be adjusted for

the amount of accumulated depreciation/amortization already taken.

(a) 240 Unit 250 Unit

Proposal Revised Proposal

(b) Assume a 240 percent luxury project at 83,000 per unit.

In order to get an 8% return on cost, we can approximate the rents required to achieve this as follows:

the location is suitable for an upgraded level of “luxury units” in that submarket/location.

PART I (a)

General Project Description

A. Site and Proposed Improvements

Site Area (in acres) 12

C. Loan Information

Construction Loan:

Summary of Cost Information for Parker Road Plaza

A. Land and Site Improvement Costs % of Total Costs Cost/(GBA) ft.

Site Acquisition and Closing Costs $2,250,000 14.5% $11.84

PART I (b)

Summary of Construction Loan Terms

Site Improvements $750,000

Total Hard Construction Costs $10,260,000

Interest Carry for Parker Road Plaza

Construction Loan Repayment Schedule and Yield Calculation for Construction Lender

(a)

(b)

(c)

(d)

(e)

(f)

(g)

Monthly

Draws Direct

Costs

Interest

Total Monthly

Draws

(a) + (b)

Payments

Principal

Interest (g) x

(13%/12)

Total Payments

(d) + (e)

Ending Bal. (g)

Prev Bal + (c) – (d)

0

$0

$0

$0

$0

1

1,865,500

0

1,186,500

$0

$0

1,186,500

2

1,865,500

12,854

1,199,354

12,854

12,854

2,385,854

3

1,865,500

25,847

1,212,347

25,847

25,847

3,598,200

4

1,865,500

38,981

1,225,481

38,981

38,981

4,823,681

5

1,865,500

52,257

1,238,757

52,257

52,257

6,062,438

6

1,865,500

65,676

1,252,176

65,676

65,676

7,314,614

7

791,000

79,242,

870,242

79,242

79,242

8,184,856

8

791,000

88,669

879,669

88,669

88,669

9,064,525

9

791,000

98,199

889,199

98,199

98,199

9,953,724

10

791,000

107,832

898,832

107,832

107,832

10,852,556

11

791,000

117,569

908,569

117,569

117,569

11,761,125

12

791,000

127,412

918,412

$12,679,537

127,412

12,806,950

0

Total

$11,865,000

$814,537

$12,679,537

$12,679,537

814,537

$13,494,075

$0

Yield to Lender: The yield to the lender is calculated as the interest rate needed to equate the present value of the

construction loan fee to the present value of the cash flow stream of the lender which is calculated from the Construction

Loan Repayment Schedule as column (d) minus column (a).

Month

Cash Flows

0

253,591

1

(1,186,500)

2

(1,186,500)

3

(1,186,500)

4

(1,186,500)

5

(1,186,500)

6

(1,186,500)

7

(791,000)

8

(791,000)

9

(791,000)

10

(791,000)

11

(791,000)

12

11,888,537

PART I (c)

Summary of Permanent Loan Terms

Total Loan $12,679,537

Pro Forma Statement of Cash Flows – Construction Period

Draws Per Year (0)

Draws Per Year (1)

Total

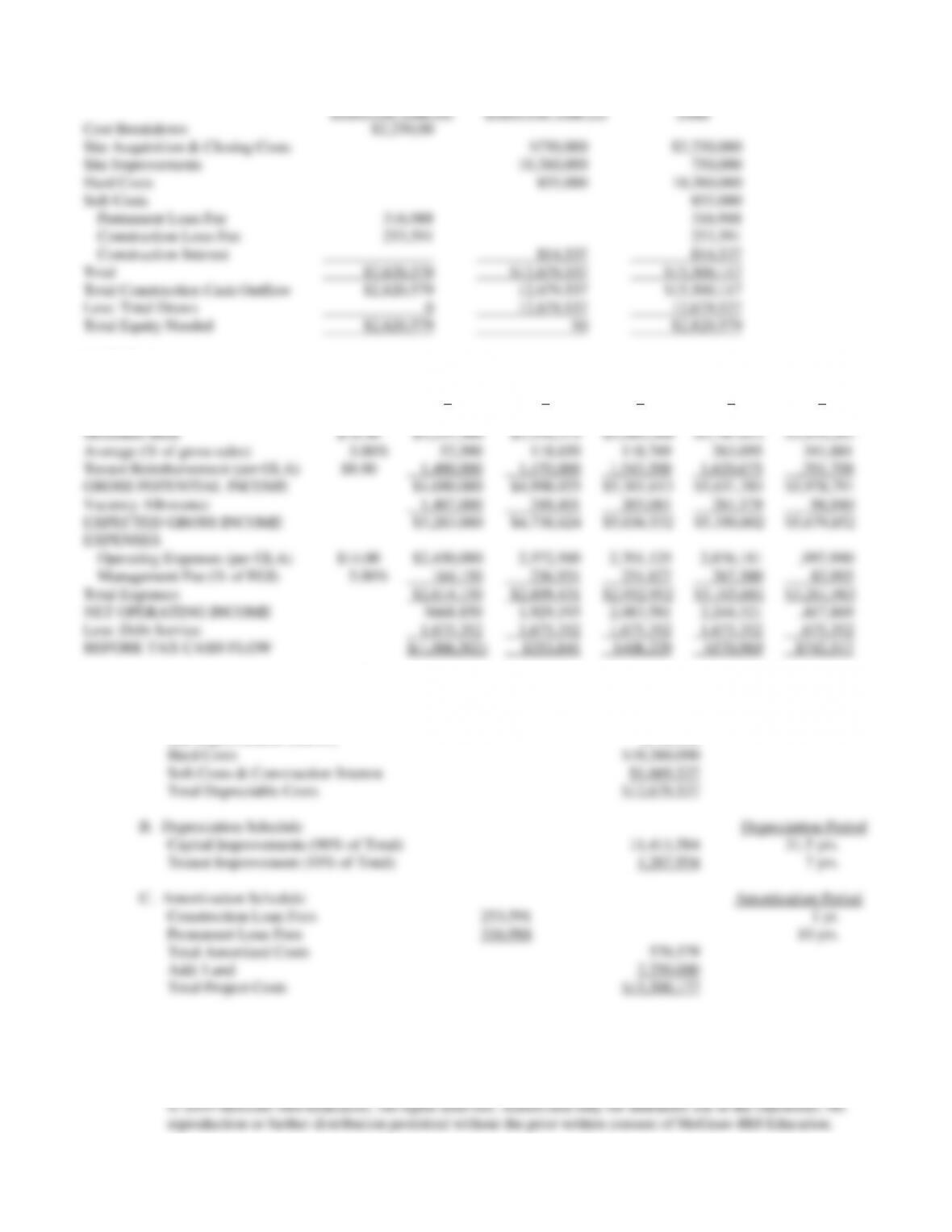

Cost Breakdown

$2,250,00

Site Acquisition & Closing Costs

$750,000

$2,250,000

Site Improvements

10,260,000

750,000

Hard Costs

855,000

10,260,000

Soft Costs

855,000

Permanent Loan Fee

316,988

316,988

Construction Loan Fee

253,591

253,591

Construction Interest

814,537

814,537

Total

$2,820,579

$12,679,537

$15,500,117

Total Construction Cash Outflow

$2,820,579

12,679,537

$15,500,117

Less: Total Draws

0

12,679,537

12,679,537

Total Equity Needed

$2,820,579

$0

$2,820,579

PART II (d)

Pro Forma Operating Statement – Parker Road Plaza

CASHFLOWS (EOP)

2

3

4

5

6

INCOME: Rent Increase @

5.00%

Minimum Rent

$18.50

$3,237,500

$3,339,375

$3,569,344

$3,747,811

$3,935,201

Average (% of gross sales)

3.00%

52,500

118,650

118,769

263,095

341,881

Tenant Reimbursement (per GLA)

$8.00

1,400,000

1,470,000

1,543,500

1,620,675

,701,709

GROSS POTENTIAL INCOME

$4,690,000

$4,998,025

$5,301,613

$5,631,581

$5,978,791

Vacancy Allowance

1,407,000

249,401

265,081

281,579

98,940

EXPECTED GROSS INCOME

$3,283,000

$4,738,624

$5,036,532

$5,350,002

$5,679,852

EXPENSES

Operating Expenses (per GLA)

$14.00

$2,450,000

2,572,500

2,701,125

2,836,181

,997,990

Management Fee (% of EGI)

5.00%

164,150

236,931

251,827

267,500

83,993

Total Expenses

$2,614,150

$2,809,431

$2,952,952

$3,103,681

$3,261,983

NET OPERATING INCOME

$668,850

1,929,193

2,083,581

2,246,321

,417,869

Less: Debt Service

1,675,352

1,675,352

1,675,352

1,675,352

,675,352

BEFORE TAX CASH FLOW

$(1,006,502)

$253,841

$408,229

$570,969

$742,517

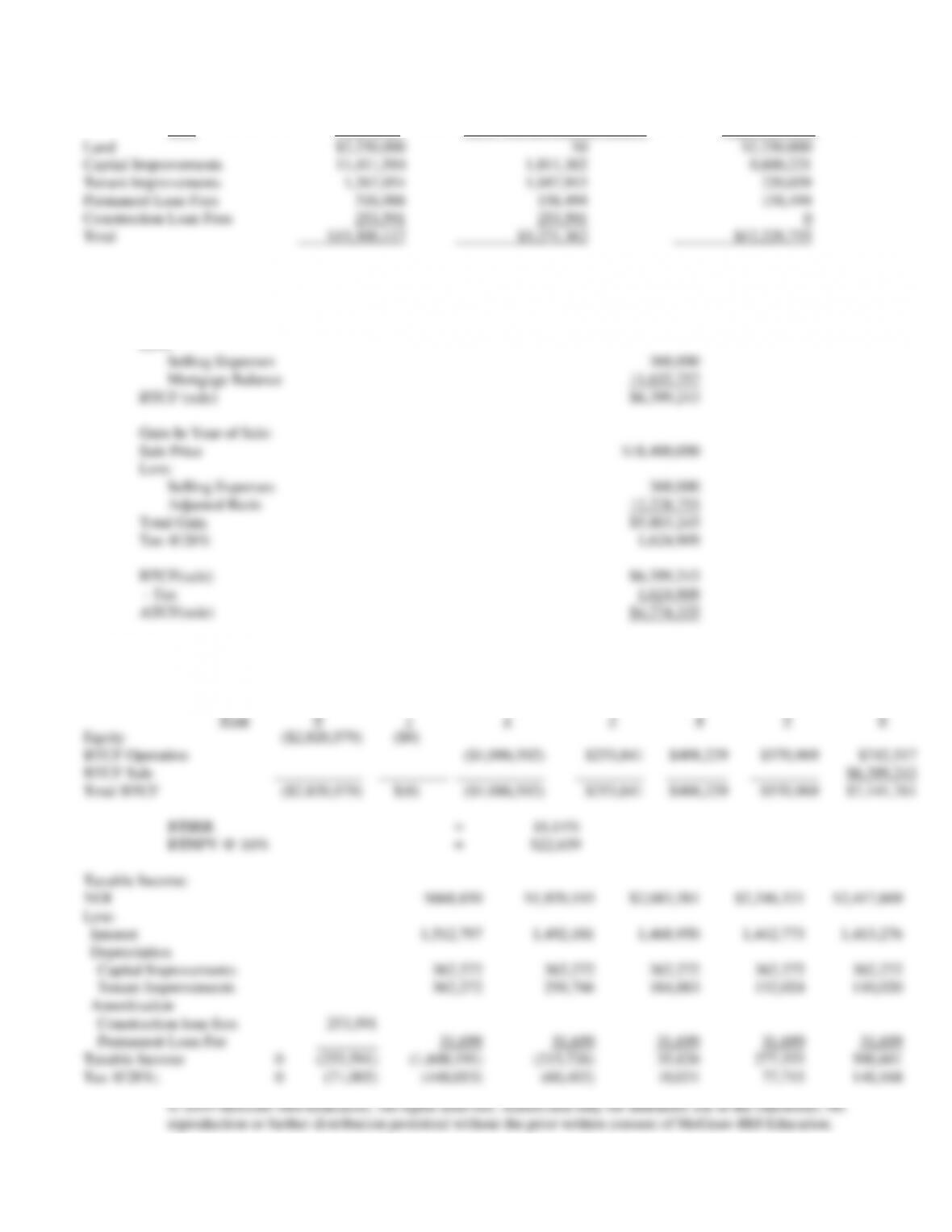

Depreciation and Amortization Schedule – Parker Road Plaza

A. Depreciable Costs

Site Improvements (on/off) $750,000

Adjusted Basis at the End of Year 6

Item

Total Cost

Less: Accum Deprec/Amort.

Adjusted Basis

Land

$2,250,000

$0

$2,250,000

Capital Improvements

11,411,584

1,811,362

9,600,221

Tenant Improvements

1,267,954

1,047,915

220,039

Permanent Loan Fees

316,988

158,494

158,494

Construction Loan Fees

253,591

253,591

0

Total

$15,500,117

$3,271,362

$12,228,755

Sale of Parker Road Plaza

Sale Price $18,400,000

Less:

PART II (d) and (e)

Profitability Analysis – Parker Road Plaza

Before Tax Cash Flows:

Year

0

1

2

3

4

5

6

Equity

($2,820,579)

($0)

BTCF Operation

($1,006,502)

$253,841

$408,229

$570,969

$742,517

BTCF Sale

$6,399,243

Total BTCF

($2,820,579)

$(0)

($1,006,502)

$253,841

$408,229

$570,969

$7,141,761

BTIRR = 16.14%

BTNPV @ 16% = $22,639

Taxable Income:

NOI

$668,850

$1,929,193

$2,083,581

$2,246,321

$2,417,869

Less:

Interest

1,512,797

1,492,181

1,468,950

1,442,773

1,413,276

Depreciation

Capital Improvements

362,272

362,272

362,272

362,272

362,272

Tenant Improvements

362,272

258,766

184,883

132,024

110,020

Amortization

Construction loan fees

253,591

Permanent Loan Fee

31,699

31,699

31,699

31,699

31,699

Taxable Income

0

(253,591)

(1,600,191)

(215,726)

35,826

277,553

500,601

Tax @28%;

0

(71,005)

(448,053)

(60,403)

10,031

77,715

140,168

© 2019 McGraw-Hill Education. All rights reserved. Authorized only for instructor use in the classroom. No

After Tax Cash Flows:

Total BTCF

($2,820,579)

($0)

($1,006,502)

$253,841

$408,229

$570,969

$7,141,761

Less: Taxes*

0

(71,005)

(448,053)

(60,403)

10,031

77,715

1,765,077

ATCF

($2,820,579)

$71,005

($558,448)

$314,244

$398,198

$493,254

$5,376,683

Problem 16-3

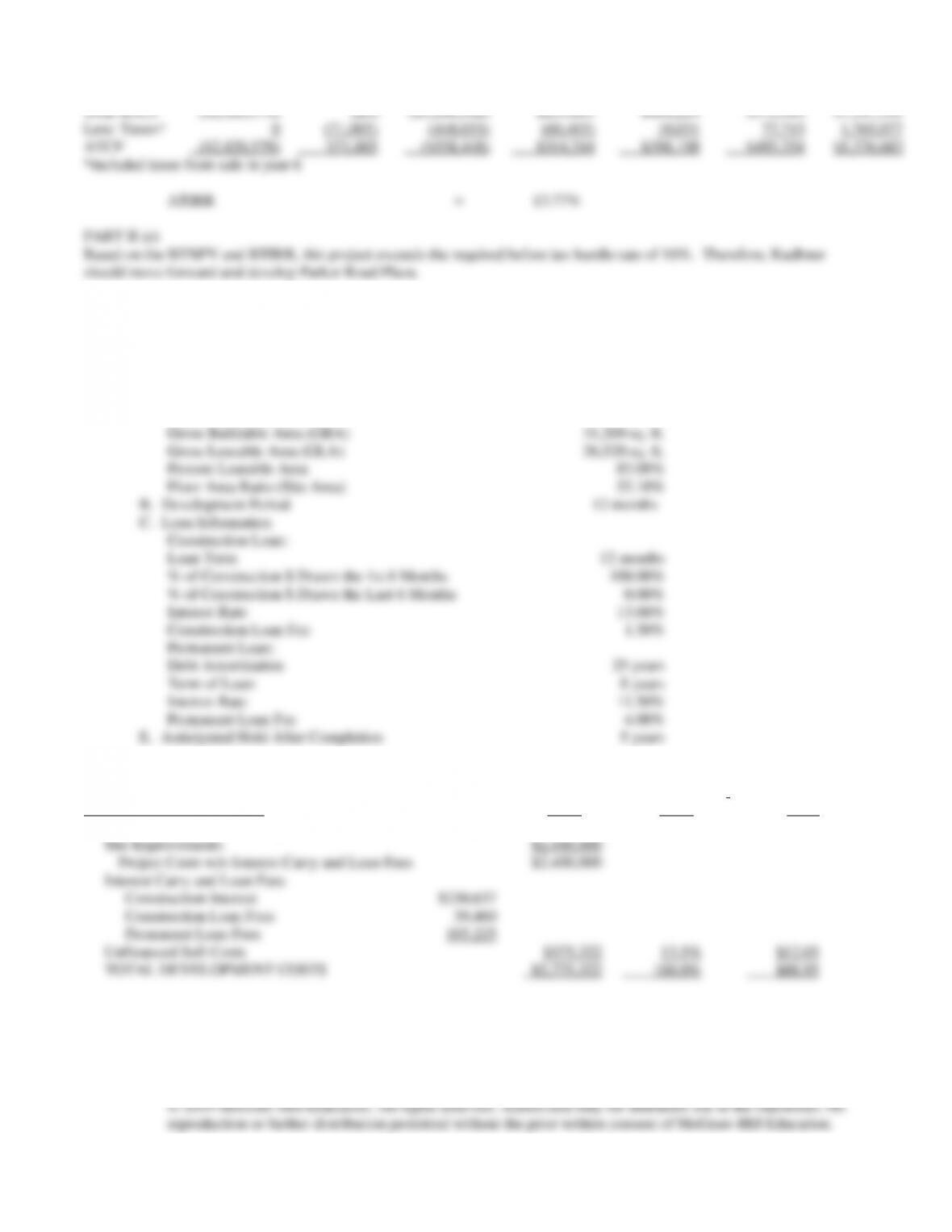

Timbercreek Office Building

(a)

General Project Description

A. Site and Proposed Improvements

Site Area (in Acres)

1.3

Gross Buildable Area (GBA)

31,200 sq. ft.

Gross Leasable Area (GLA)

26,520 sq. ft.

Percent Leasable Area

85.00%

Floor Area Ratio (Site Area)

55.10%

B. Development Period

12 months

C. Loan Information

Construction Loan:

Loan Term

12 months

% of Construction $ Drawn the 1st 6 Months

100.00%

% of Construction $ Drawn the Last 6 Months

0.00%

Interest Rate

13.00%

Construction Loan Fee

1.50%

Permanent Loan:

Debt Amortization

25 years

Term of Loan

8 years

Interest Rate

11.50%

Permanent Loan Fee

4.00%

E. Anticipated Hold After Completion

5 years

Summary of Cost Information for Proposed Office Building

Land and Site Improvements

Costs

Percent of Total

Costs

Cost per Sq. Ft.

GBA

Site Acquisition and Closing Costs

TBD

0.0%

$0.00

Site Improvements

$2,400,000

Project Costs w/o Interest Carry and Loan Fees

$2,400,000

Interest Carry and Loan Fees

Construction Interest

$230,637

Construction Loan Fees

39,460

Permanent Loan Fees

105,225

Unfinanced Soft Costs

$375,322

13.5%

$12.03

TOTAL DEVELOPMENT COSTS

$2,775,322

100.0%

$88.95

Estimation of Loan Costs and Equity Requirements for the Development

Site Improvements

$2,400,000

Total Direct Costs Which Will Be Financed

$2,400,000

Estimated Interest Carry (calculated below)

230,637

Total Loan Amount

$2,630,637

Total Development Costs

$2,775,322

Less: Total Loan Amount

2,630,637

Total Equity Requirements for Development

$144,685

Estimated Interest Carry for Proposed Office Building

Construction Loan Repayment Schedule

(a)

(b)

(c)

(d)

(e)

(f)

(g)

Monthly

Draws Direct

Costs

Interest

Total Monthly

Draws (a) + (b)

Payments

Principal

Interest (g) x

(13%/12)

Total Payments

(d) + (e)

Ending Bal. (g)

Prev Bal + (c) –

(d)

0

$0

$0

$0

$0

1

400,000

0

400,000

$0

$0

400,000

2

400,000

4,333

404,333

4,333

4,333

804,333

3

400,000

8,714

408,714

8,714

8,714

1,213,047

4

400,000

13,141

413,141

13,141

13,141

1,626,188

5

400,000

17,617

417,617

17,617

17,617

2,043,805

6

400,000

22,141

422,141

22,141

22,141

2,465,947

7

0

26,714

26,714

26,714

26,714

2,492,661

8

0

27,004

27,004

27,004

27,004

2,519,665

9

0

27,296

27,296

27,296

27,296

2,546,961

10

0

27,592

27,592

27,592

27,592

2,574,553

11

0

27,891

27,891

27,891

27,891

2,602,444

12

0

28,193

28,193

$2,630,637

28,193

2,658,831

0

Total

$2,400,000

$230,637

$2,630,637

$2,630,637

$230,637

$2,861,275

$0

(b)

Summary of Permanent Loan Terms

Total Loan

$2,630,637

Debt Amortization

25 years

Term of Loan

8 years

Interest Rate

11.50%

Debt Service/Month

$26,740

Debt Service/Year

$320,875

4.00% Permanent Loan Fee

$105,225

Pro Forma Statement of Cash Flows – Construction Period

Draws per Year (0)

Draws per Year (1)

Total

Cost Breakdown

Site Acquisition & Closing Costs

TBD

$0

Site Improvements

$2,400,000

2,400,000

Permanent Loan Fee

$105,225

105,225

Construction Loan Fee

39,460

39,460

Construction Interest

230,637

230,637

Total

$114,685

$2,630,637

$2,775,322

Total Construction Cash Outflow

$114,685

$2,630,637

$2,775,322

Less: Total Draws

0

2,630,637

2,630,637

Total Equity Needed

$114,685

$0

$114,685

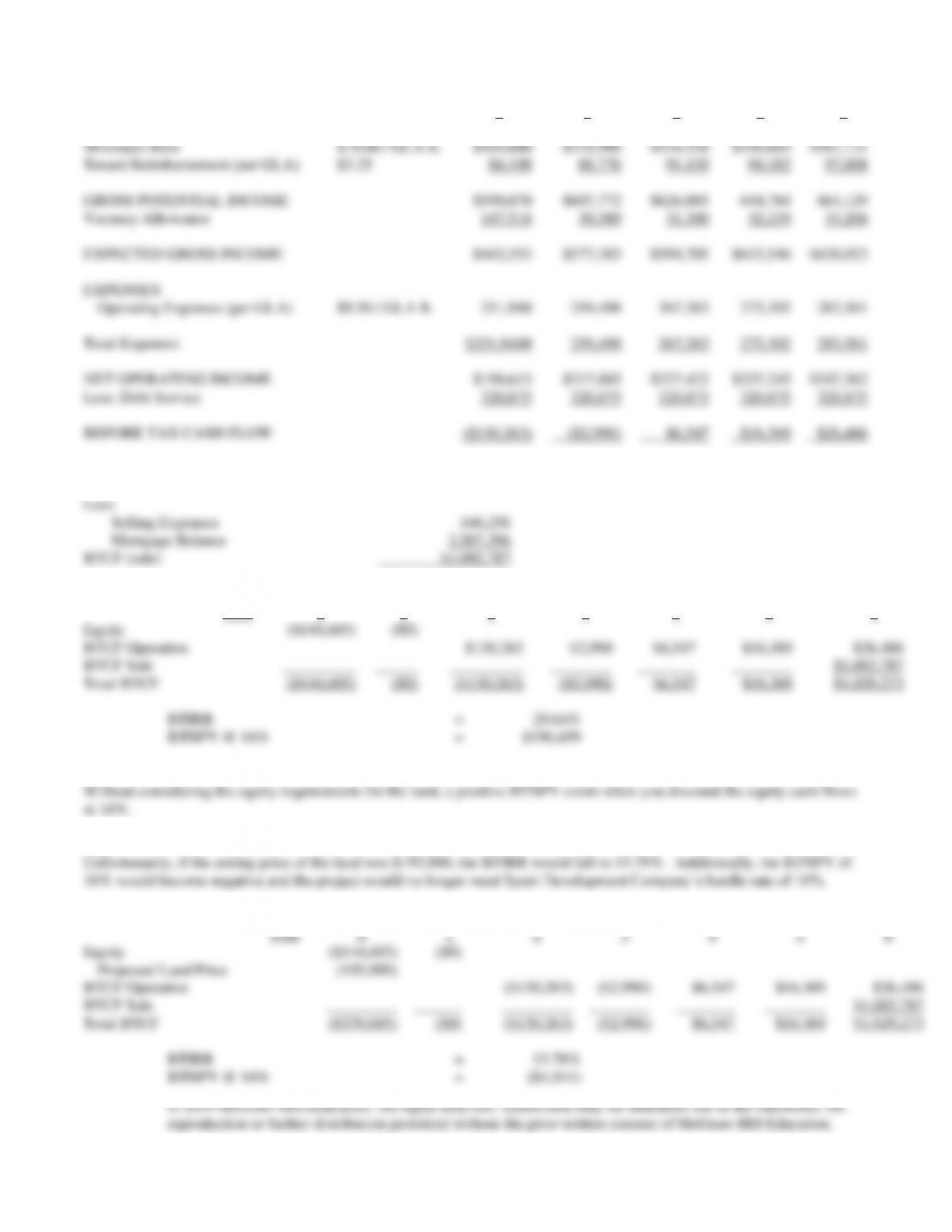

Pro Forma Operating Statement – Parker Road Plaza

CASHFLOWS (EOP)

2

3

4

5

6

INCOME: Rent Increase @

3.00% yr.

Minimum Rent

$19.00 / GLA ft.

$503,880

$518,996

$534,556

$550,603

$567,121

Tenant Reimbursement (per GLA)

$3.25

86,190

88,776

91,439

94,182

97,008

GROSS POTENTIAL INCOME

$590,070

$607,772

$626,005

644,784

664,129

Vacancy Allowance

147,518

30,389

31,300

32,239

33,206

EXPECTED GROSS INCOME

$442,553

$577,383

$594,705

$612,546

$630,923

EXPENSES

Operating Expenses (per GLA)

$9.50 / GLA ft.

251,940

259,498

267,283

275,302

283,561

Total Expenses

$251,9400

259,498

267,283

275,302

283,561

NET OPERATING INCOME

$190,613

$317,885

$327,422

$337,245

$347,362

Less: Debt Service

320,875

320,875

320,875

320,875

320,875

BEFORE TAX CASH FLOW

($130,263)

($2,990)

$6,547

$16,369

$26,486

Sale of Proposed Office Building

Sale Price

$3,656,400*

Less:

Selling Expenses

146,258

Mortgage Balance

2,507,396

BTCF (sale)

$1,002,787

Profitability Analysis for Proposed Office Building

Year

0

1

2

3

4

5

6

Equity

($144,685)

($0)

BTCF Operation

$130,263

$2,990

$6,547

$16,369

$26,486

BTCF Sale

$1,002,787

Total BTCF

($144,685)

($0)

($130,263)

($2,990)

$6,547

$16,369

$1,029,273

(c)

(d)

Before Tax Cash Flows

Year

0

1

2

3

4

5

6

Equity

($144,685)

($0)

Proposed Land Price

(195,000)

BTCF Operation

($130,263)

($2,990)

$6,547

$16,369

$26,486

BTCF Sale

$1,002,787

Total BTCF

($339,685)

($0)

($130,263)

($2,990)

$6,547

$16,369

$1,029,273

Problem 16-4