14-1

Solutions to Questions – Chapter 14

Disposition and Renovation of Income Properties

Question 14-1

What factors should an investor consider when trying to decide whether to dispose of a property that he has

owned for several years?

Question 14-2

Why might the actual holding period for a property be different from the holding period that was anticipated when

the property was purchased?

Question 14-3

What is the marginal rate of return? How is it calculated?

Question 14-4

What causes the marginal rate of return to change over time? How can the marginal rate of return be used to

decide when to sell a property?

Question 14-5

Why might the after-tax internal rate of return on equity (ATIRRe) differ for a new investor versus an existing

investor who keeps the property?

Question 14-6

What factors should be considered when deciding whether to renovate a property?

Question 14-7

Why is refinancing often done in conjunction with renovation?

Question 14-8

Why would refinancing be an alternative to sale of the property?

Question 14-9

How can tax law changes create incentives for investors to sell their properties to other investors?

Question 14-10

How important are taxes in the decision to sell a property?

Question 14-11

Are tax considerations important in renovation decisions?

Question 14-12

What are the benefits and costs of renovation?

Question 14-13

Do you think renovation is more or less risky than a new investment?

14-3

Question 14-14

What is meant by the “incremental cost of refinancing?”

Question 14-15

In general, what kinds of tax incentives are available for rehabilitation of real estate income property?

Question 14-16

Why would an investor consider doing an exchange or an installment sale?

Solutions to Problems – Chapter 14

Disposition and Renovation of Income Properties

INTRODUCTION

The four problems in this chapter deal with disposition and renovation decisions. Students are also expected to recognize that

refinancing is also an alternative to disposition (part g of problem 3), and refinancing is often a part of renovation (part b of

problem 4).

Problem 14-1

(a) If sold today If sold next year

Problem 14-2

14-5

Problem 14-3

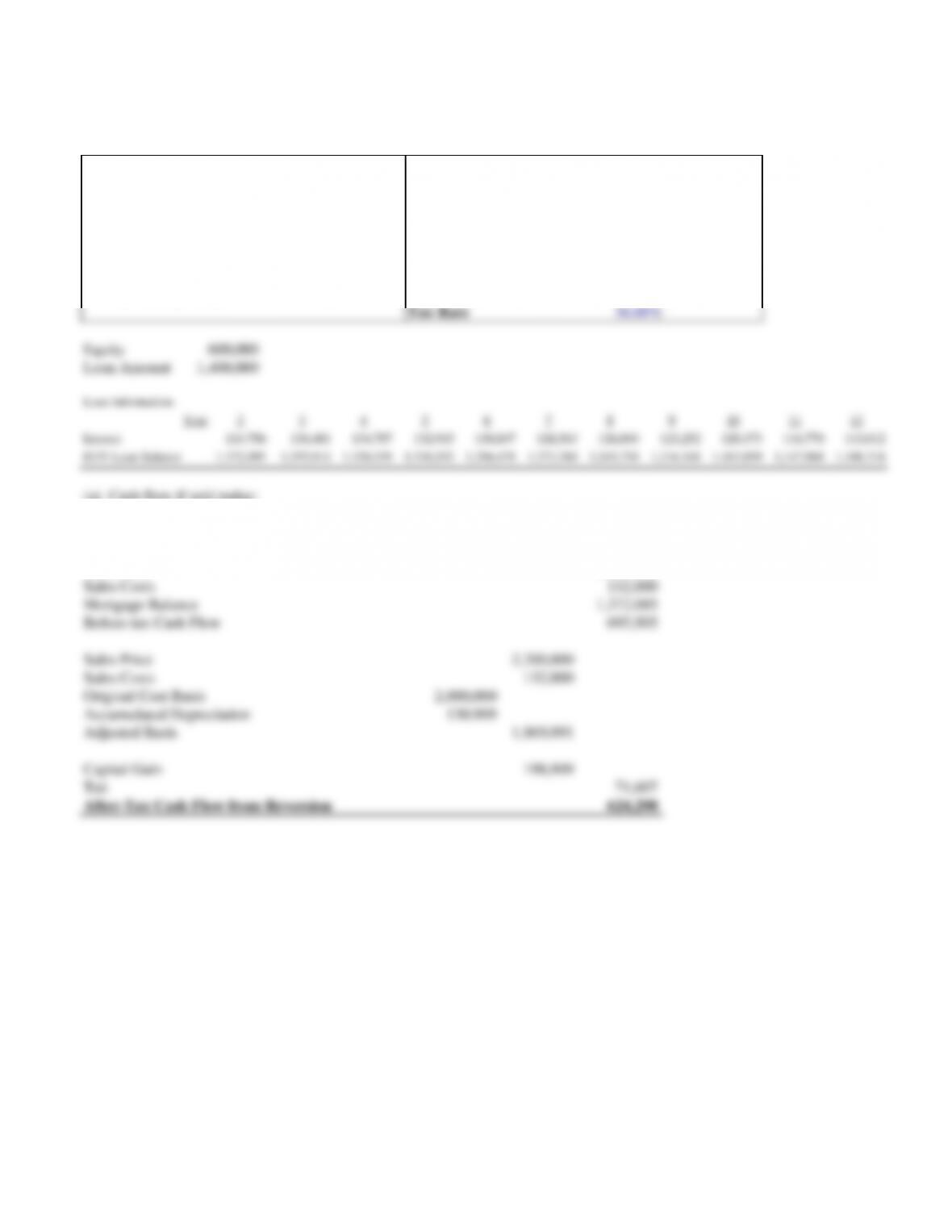

(REFER TO TEMPLATE 14_3.XLS)

ASSUMPTIONS:

EGI Year After Sale

350,000

Purchase Price

2,000,000

Projected Increase in EGI

3.00%

per year

Building Value

1,800,000

Operating Expenses

40.00%

of EGI

Land Value

200,000

Loan:

Years since Purchased

2

Loan-to-value ratio

70.00%

Resale Value Today

2,200,000

Interest

10.00%

Selling Expenses

6.00%

of sale price

Term

25

years

Appreciation Rate

3.00%

per year

Payments per year

12

Depreciable Life

27.5

years

Tax Rate

36.00%

Equity

600,000

Loan Amount

1,400,000

Loan Information:

Year

2

3

4

5

6

7

8

9

10

11

12

Interest

124,756

136,481

134,787

132,915

130,847

128,563

126,040

123,252

120,173

116,770

113,012

EOY Loan Balance

1,372,095

1,355,914

1,338,039

1,318,293

1,296,478

1,272,380

1,245,758

1,216,348

1,183,859

1,147,968

1,108,318

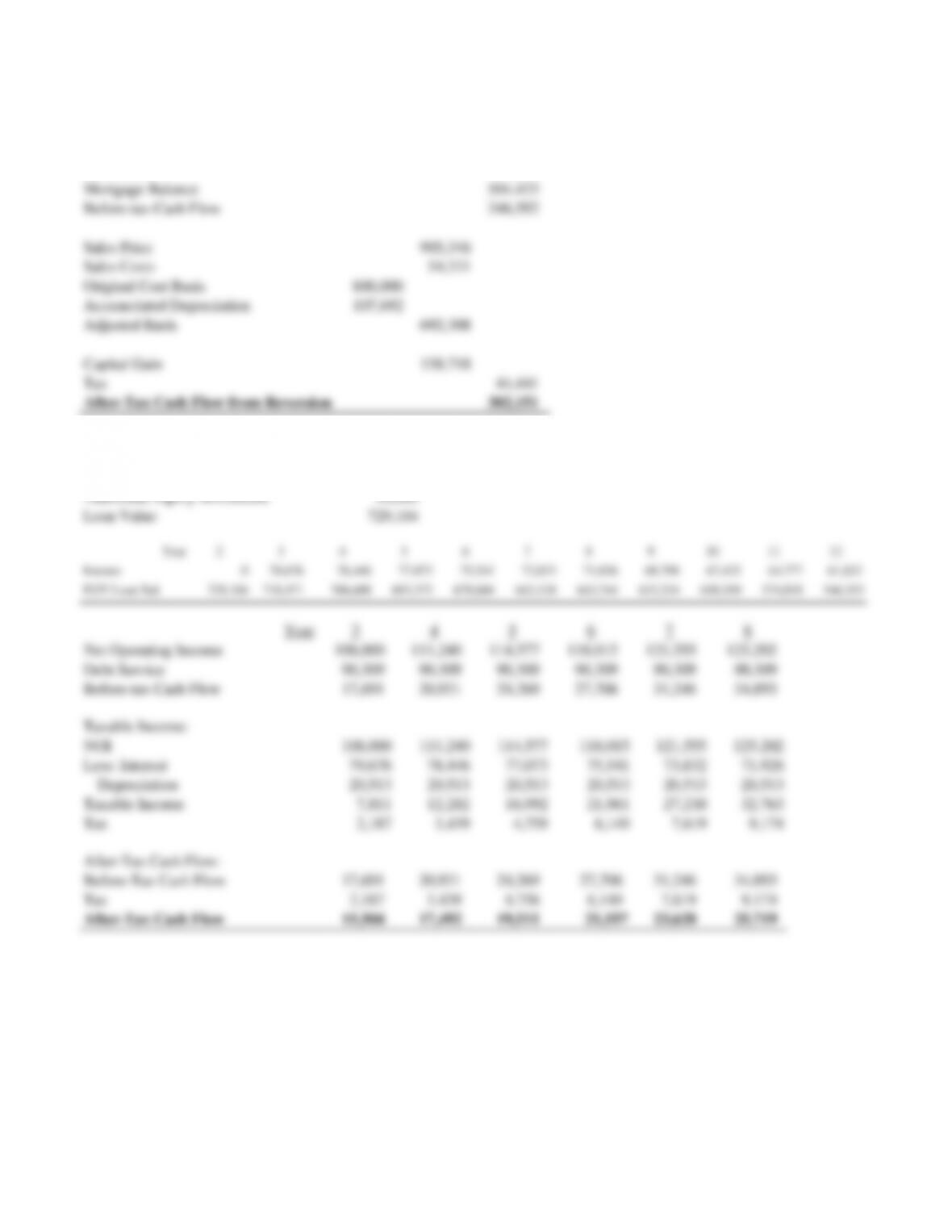

(a) Cash flow if sold today:

Cash Flows from Sale in Year

2

Sales Price

2,200,000

Sales Costs

132,000

Mortgage Balance

1,372,095

Before-tax Cash Flow

695,905

Sales Price

2,200,000

Sales Costs

132,000

Original Cost Basis

2,000,000

Accumulated Depreciation

130,909

Adjusted Basis

1,869,091

Capital Gain

198,909

Tax

71,607

After-Tax Cash Flow from Reversion

624,298

14-6

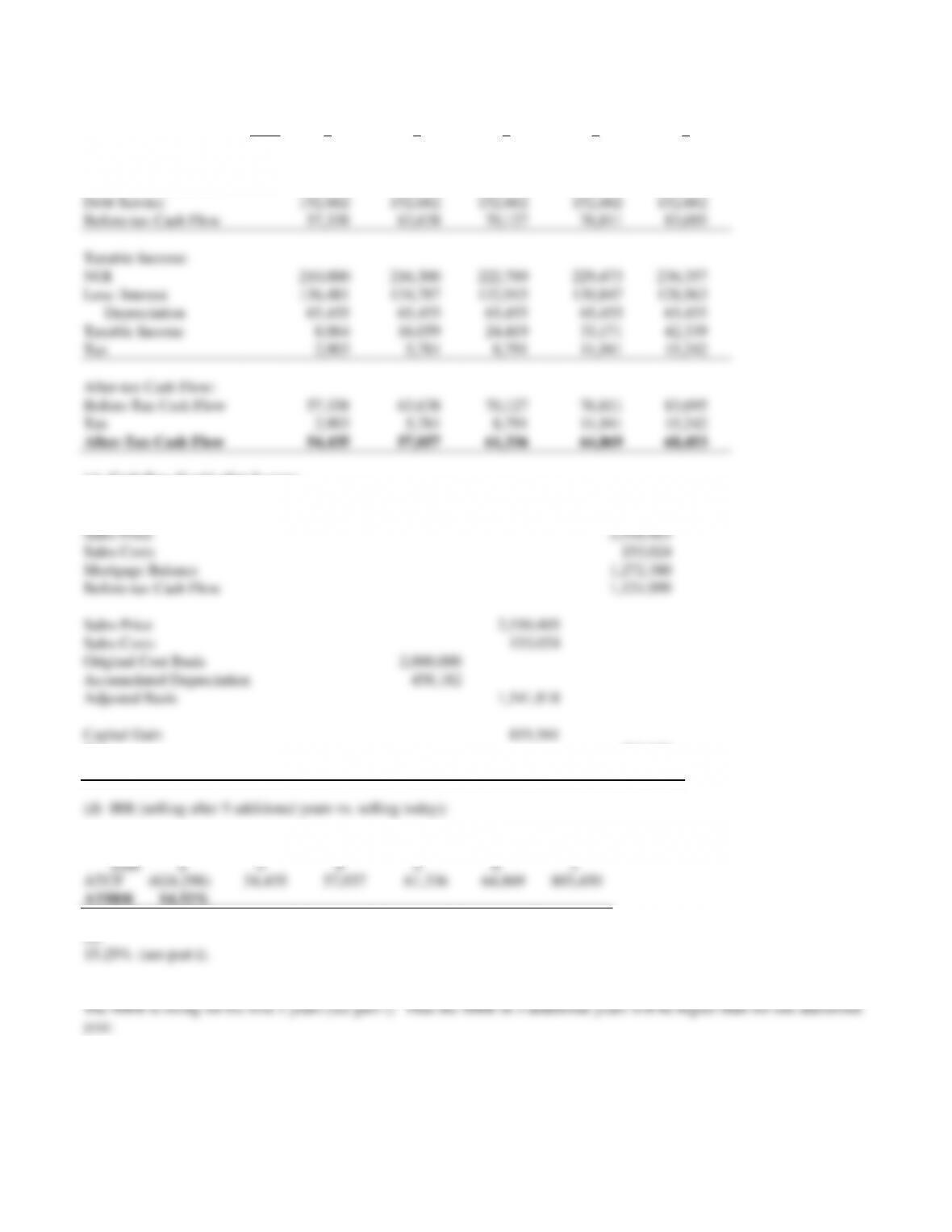

(b) Cash flow if not sold:

Year

3

4

5

6

7

Effective Gross Income

350,000

360,500

371,315

382,454

393,928

Operating Expenses

140,000

144,200

148,526

152,982

157,571

Net Operating Income

210,000

216,300

222,789

229,473

236,357

Debt Service

152,662

152,662

152,662

152,662

152,662

Before-tax Cash Flow

57,338

63,638

70,127

76,811

83,695

Taxable Income:

NOI

210,000

216,300

222,789

229,473

236,357

Less: Interest

136,481

134,787

132,915

130,847

128,563

Depreciation

65,455

65,455

65,455

65,455

65,455

Taxable Income

8,064

16,059

24,419

33,171

42,339

Tax

2,903

5,781

8,791

11,941

15,242

After-tax Cash Flow:

Before-Tax Cash Flow

57,338

63,638

70,127

76,811

83,695

Tax

2,903

5,781

8,791

11,941

15,242

After-Tax Cash Flow

54,435

57,857

61,336

64,869

68,453

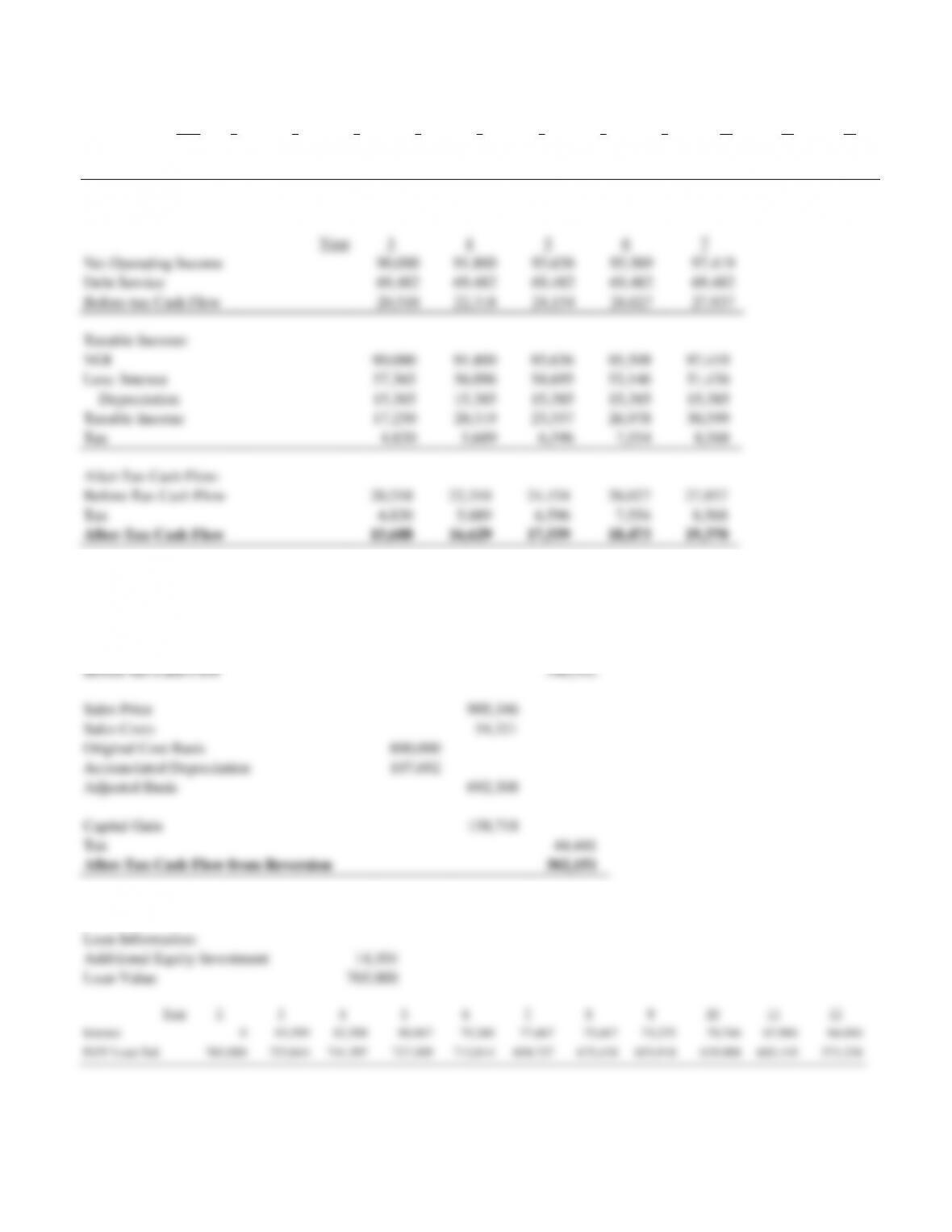

(c) Cash flow if sold after 5 years:

Cash Flows from Sale in Year

7

Sales Price

2,550,403

Sales Costs

153,024

Mortgage Balance

1,272,380

Before-tax Cash Flow

1,124,999

Sales Price

2,550,403

Sales Costs

153,024

Original Cost Basis

2,000,000

Accumulated Depreciation

458,182

Adjusted Basis

1,541,818

Capital Gain

855,561

Tax

308,002

After-Tax Cash Flow from Reversion

816,997

ATIRR on holding property 5 additional years:

Year

2

3

4

5

6

7

ATCF

(624,298)

54,435

57,857

61,336

64,869

885,450

ATIRR

14.32%

(e)

(f)

(g)

(h)

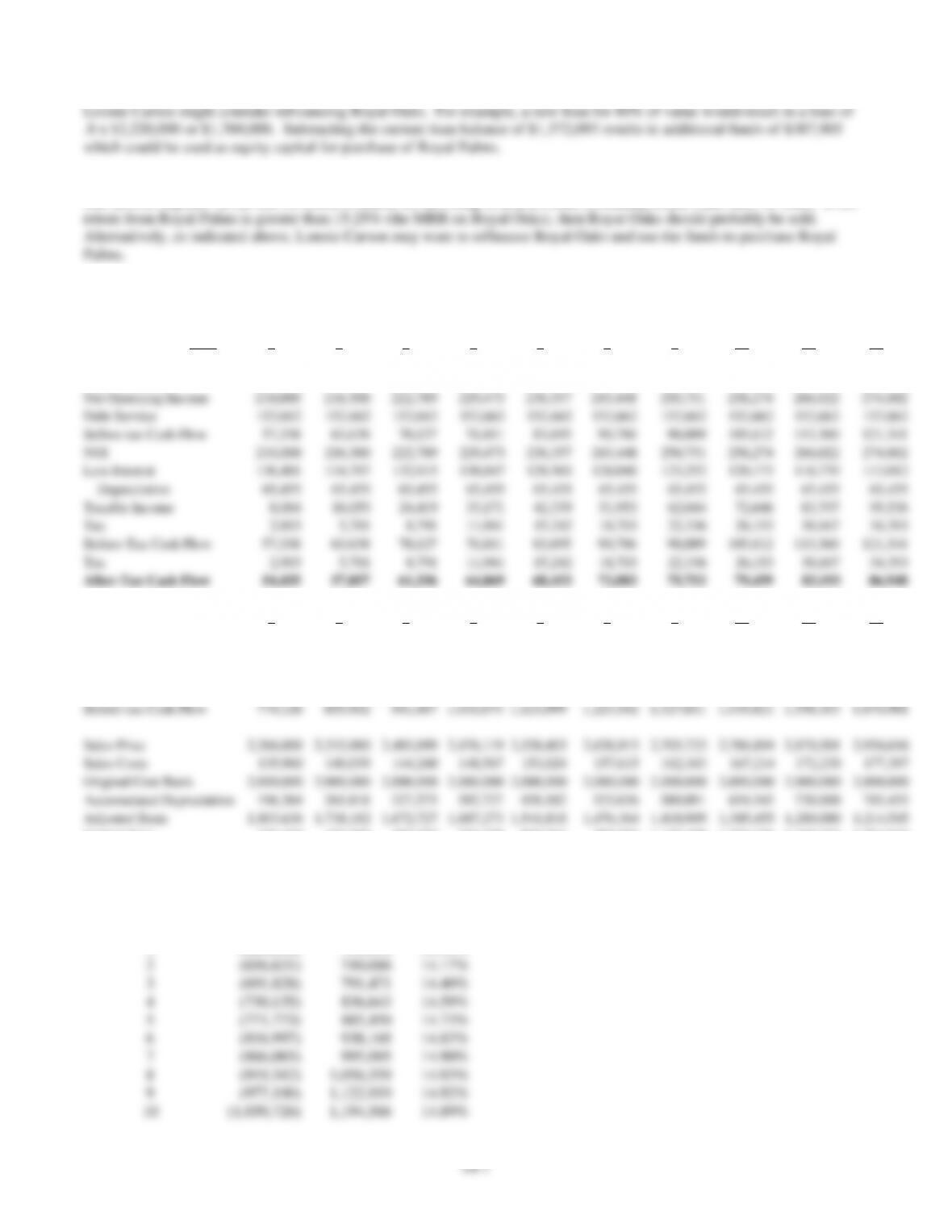

The answer depends on the rate of return available for investing in Royal Palms (assuming Royal Oaks must be sold). If the

(i)

Marginal Rate of Return

Year

3

4

5

6

7

8

9

10

11

12

Effective Gross Income

350,000

360,500

371,315

382,454

393,928

405,746

417,918

430,456

443,370

456,671

Operating Expenses

140,000

144,200

148,526

152,982

157,571

162,298

167,167

172,182

177,348

182,668

Net Operating Income

210,000

216,300

222,789

229,473

236,357

243,448

250,751

258,274

266,022

274,002

Debt Service

152,662

152,662

152,662

152,662

152,662

152,662

152,662

152,662

152,662

152,662

Before-tax Cash Flow

57,338

63,638

70,127

76,811

83,695

90,786

98,089

105,612

113,360

121,341

NOI

210,000

216,300

222,789

229,473

236,357

243,448

250,751

258,274

266,022

274,002

Less Interest

136,481

134,787

132,915

130,847

128,563

126,040

123,252

120,173

116,770

113,012

Depreciation

65,455

65,455

65,455

65,455

65,455

65,455

65,455

65,455

65,455

65,455

Taxable Income

8,064

16,059

24,419

33,171

42,339

51,953

62,044

72,646

83,797

95,536

Tax

2,903

5,781

8,791

11,941

15,242

18,703

22,336

26,153

30,167

34,393

Before-Tax Cash Flow

57,338

63,638

70,127

76,811

83,695

90,786

98,089

105,612

113,360

121,341

Tax

2,903

5,781

8,791

11,941

15,242

18,703

22,336

26,153

30,167

34,393

After-Tax Cash Flow

54,435

57,857

61,336

64,869

68,453

72,083

75,753

79,459

83,193

86,948

ATCF From Sale

3

4

5

6

7

8

9

10

11

12

Sales Price

2,266,000

2,333,980

2,403,999

2,476,119

2,550,403

2,626,915

2,705,723

2,786,894

2,870,501

2,956,616

Sales Costs

135,960

140,039

144,240

148,567

153,024

157,615

162,343

167,214

172,230

177,397

Mortgage Balance

1,355,914

1,338,039

1,318,293

1,296,478

1,272,380

1,245,758

1,216,348

1,183,859

1,147,968

1,108,318

Before-tax Cash Flow

774,126

855,902

941,467

1,031,074

1,124,999

1,223,542

1,327,031

1,435,821

1,550,303

1,670,901

Sales Price

2,266,000

2,333,980

2,403,999

2,476,119

2,550,403

2,626,915

2,705,723

2,786,894

2,870,501

2,956,616

Sales Costs

135,960

140,039

144,240

148,567

153,024

157,615

162,343

167,214

172,230

177,397

Original Cost Basis

2,000,000

2,000,000

2,000,000

2,000,000

2,000,000

2,000,000

2,000,000

2,000,000

2,000,000

2,000,000

Accumulated Depreciation

196,364

261,818

327,273

392,727

458,182

523,636

589,091

654,545

720,000

785,455

Adjusted Basis

1,803,636

1,738,182

1,672,727

1,607,273

1,541,818

1,476,364

1,410,909

1,345,455

1,280,000

1,214,545

Capital Gain

326,404

455,759

587,032

720,279

855,561

992,937

1,132,470

1,274,226

1,418,271

1,564,674

Tax

117,505

164,073

211,332

259,301

308,002

357,457

407,689

458,721

510,578

563,283

ATCF From Sale

656,621

691,828

730,135

771,773

816,997

866,085

919,342

977,100

1,039,726

1,107,618

Marginal Rate of Return

Holding Period

CF0

CF1

MRR

1

(624,298)

711,056

13.90%

2

(656,621)

749,686

14.17%

3

(691,828)

791,471

14.40%

4

(730,135)

836,643

14.59%

5

(771,773)

885,450

14.73%

6

(816,997)

938,168

14.83%

7

(866,085)

995,095

14.90%

8

(919,342)

1,056,559

14.93%

9

(977,100)

1,122,919

14.92%

10

(1,039,726)

1,194,566

14.89%

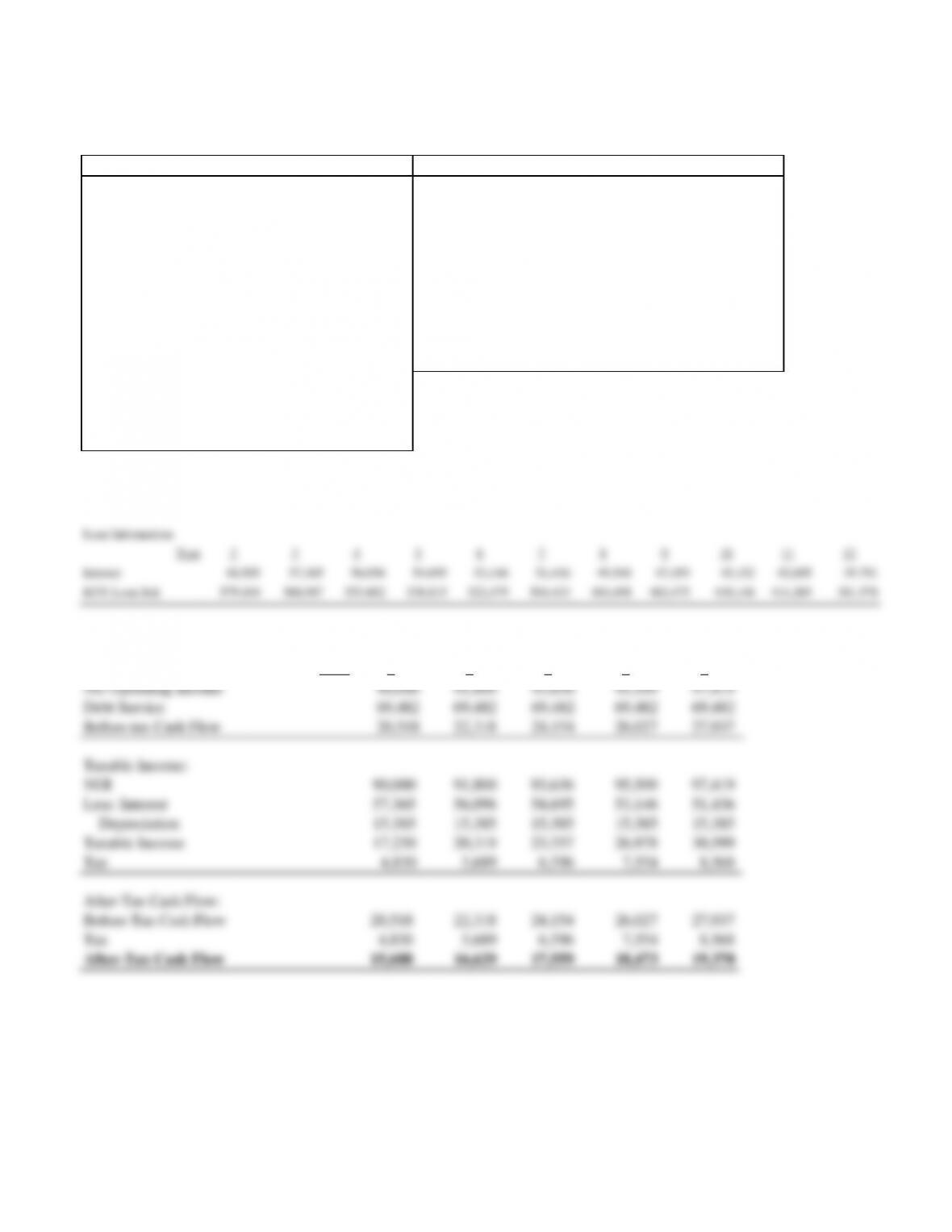

Problem 14-4

(REFER TO TEMPLATE 14_4a.XLS)

ASSUMPTIONS:

Year

Net Operating Income

Debt Service

Before-tax Cash Flow

Taxable Income:

NOI

Less: Interest

Taxable Income

After-Tax Cash Flow:

Before-Tax Cash Flow

After-Tax Cash Flow

CURRENT

IF RENOVATED

Purchase Price

800,000

Renovation Cost

200,000

Building Value

600,000

Initial Increase in NOI

20.00%

Land Value

200,000

Annual Increase in NOI

3.00%

Loan-to-value ratio

75.00%

Terminal Cap Rate

10.00%

Interest

10.00%

Selling Expenses

6.00%

of sale price

Term

20

years

New Loan:

Payments per year

12

% of Renovation Costs

75.00%

Years since Purchased

2

Interest Rate

11.00%

Current NOI

90,000

Term

20

Projected Increase in NOI

2.00%

per year

Payments per year

12

Resale Value Today

820,000

Appreciation Rate

2.00%

per year

Depreciable Life

39

years

Tax Rate

28.00%

Equity

200,000

Loan Amount

600,000

14-9

Cash Flows from Sale in Year

7

Sales Price

905,346

Sales Costs

54,321

Mortgage Balance

504,433

Before-tax Cash Flow

346,592

Sales Price

905,346

Sales Costs

54,321

Original Cost Basis

800,000

Accumulated Depreciation

107,692

Adjusted Basis

692,308

Capital Gain

158,718

Tax

44,441

After-Tax Cash Flow from Reversion

302,151

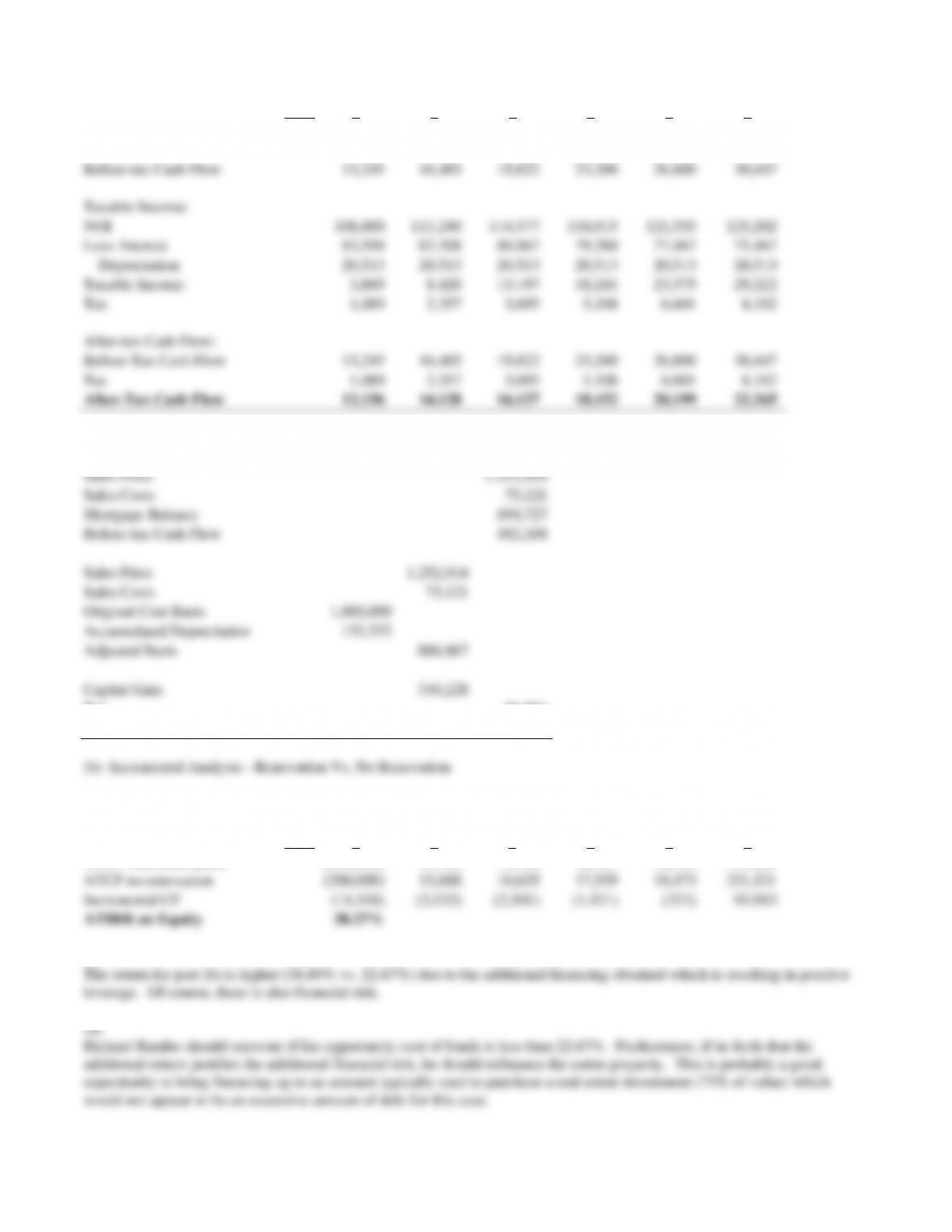

CASH FLOWS WITH RENOVATION

Loan Information:

Additional Equity Investment

50,000

Loan Value

729,104

Year

2

3

4

5

6

7

8

9

10

11

12

Interest

0

79,676

78,446

77,073

75,541

73,832

71,926

69,798

67,425

64,777

61,822

EOY Loan Bal.

729,104

718,471

706,608

693,372

678,604

662,128

643,744

623,234

600,350

574,818

546,332

Year

3

4

5

6

7

8

Net Operating Income

108,000

111,240

114,577

118,015

121,555

125,202

Debt Service

90,309

90,309

90,309

90,309

90,309

90,309

Before-tax Cash Flow

17,691

20,931

24,269

27,706

31,246

34,893

Taxable Income:

NOI

108,000

111,240

114,577

118,015

121,555

125,202

Less: Interest

79,676

78,446

77,073

75,541

73,832

71,926

Depreciation

20,513

20,513

20,513

20,513

20,513

20,513

Taxable Income

7,811

12,282

16,992

21,961

27,210

32,763

Tax

2,187

3,439

4,758

6,149

7,619

9,174

After-Tax Cash Flow:

Before-Tax Cash Flow

17,691

20,931

24,269

27,706

31,246

34,893

Tax

2,187

3,439

4,758

6,149

7,619

9,174

After-Tax Cash Flow

15,504

17,492

19,511

21,557

23,628

25,719

14–10

Cash Flows from Sale in Year

7

Sales Price

1,252,016

Sales Costs

75,121

Mortgage Balance

662,128

Before-tax Cash Flow

514,767

Sales Price

1,252,016

Sales Costs

75,121

Original Cost Basis

1,000,000

Accumulated Depreciation

133,333

Adjusted Basis

866,667

Capital Gain

310,228

Tax

86,864

After-Tax Cash Flow from Reversion

427,904

(a) Incremental Analysis – Renovation Vs. No Renovation

INCREMENTAL ANALYSIS – RENOVATION VS. NO RENOVATION

Year

2

3

4

5

6

7

ATCF with renovation

(250,000)

15,504

17,492

19,511

21,557

451,531

ATCF no renovation

(200,000)

15,688

16,629

17,559

18,473

321,521

Incremental CF

(50,000)

(184)

863

1,952

3,084

130,010

ATIRR on Equity

22.49%

(b)

(REFER TO TEMPLATE 14_4b.XLS)

ASSUMPTIONS:

CURRENT

IF RENOVATED

Purchase Price

800,000

Renovation Cost

200,000

Building Value

600,000

Initial Increase in NOI

20.00%

Land Value

200,000

Annual Increase in NOI

3.00%

Loan-to-value ratio

75.00%

Terminal Cap Rate

10.00%

Interest

10.00%

Selling Expenses

6.00%

of sale price

Term

20

years

New Loan:

Payments per year

12

% of Renovation Costs

75.00%

Years since Purchased

2

Interest Rate

11.00%

Current NOI

90,000

Term

20

Projected Increase in NOI

2.00%

per year

Payments per year

12

Resale Value Today

820,000

Appreciation Rate

2.00%

per year

Depreciable Life

39

years

Tax Rate

28.00%

Equity

200,000

Loan Amount

600,000

2

3

4

5

6

7

8

9

10

11

12

Interest

83,599

80,867

79,260

77,467

75,467

70,744

67,966

64,866

EOY Loan Bal.

753,844

727,509

712,014

675,438

629,908

603,119

Loan Information:

Year

2

3

4

5

6

7

8

9

10

11

12

Interest

48,585

57,365

56,096

54,695

53,146

51,436

49,546

47,459

45,152

42,605

39,791

EOY Loan Bal.

579,104

566,987

553,602

538,815

522,479

504,433

484,498

462,475

438,146

411,269

381,578

CASH FLOWS WITHOUT RENOVATION

NOI

108,000

111,240

114,577

118,015

121,555

125,202

Less: Interest

83,599

82,308

80,867

79,260

77,467

20,513

20,513

20,513

20,513

20,513

Taxable Income

After-tax Cash Flow:

Before-Tax Cash Flow

13,245

16,485

19,822

23,260

26,800

Sales Price

Sales Costs

Mortgage Balance

Before-tax Cash Flow

Sales Price

Sales Costs

Original Cost Basis

Accumulated Depreciation

133,333

Adjusted Basis

Capital Gain

Year

2

3

4

5

6

7

ATCF with renovation

415,504

ATCF no renovation

15,688

16,629

17,559

18,473

Incremental CF

Year

3

4

5

6

7

8

Net Operating Income

108,000

111,240

114,577

118,015

121,555

125,202

Debt Service

94,755

94,755

94,755

94,755

94,755

94,755

Before-tax Cash Flow

13,245

16,485

19,822

23,260

26,800

30,447

Problem 14-5

Problem 14-6

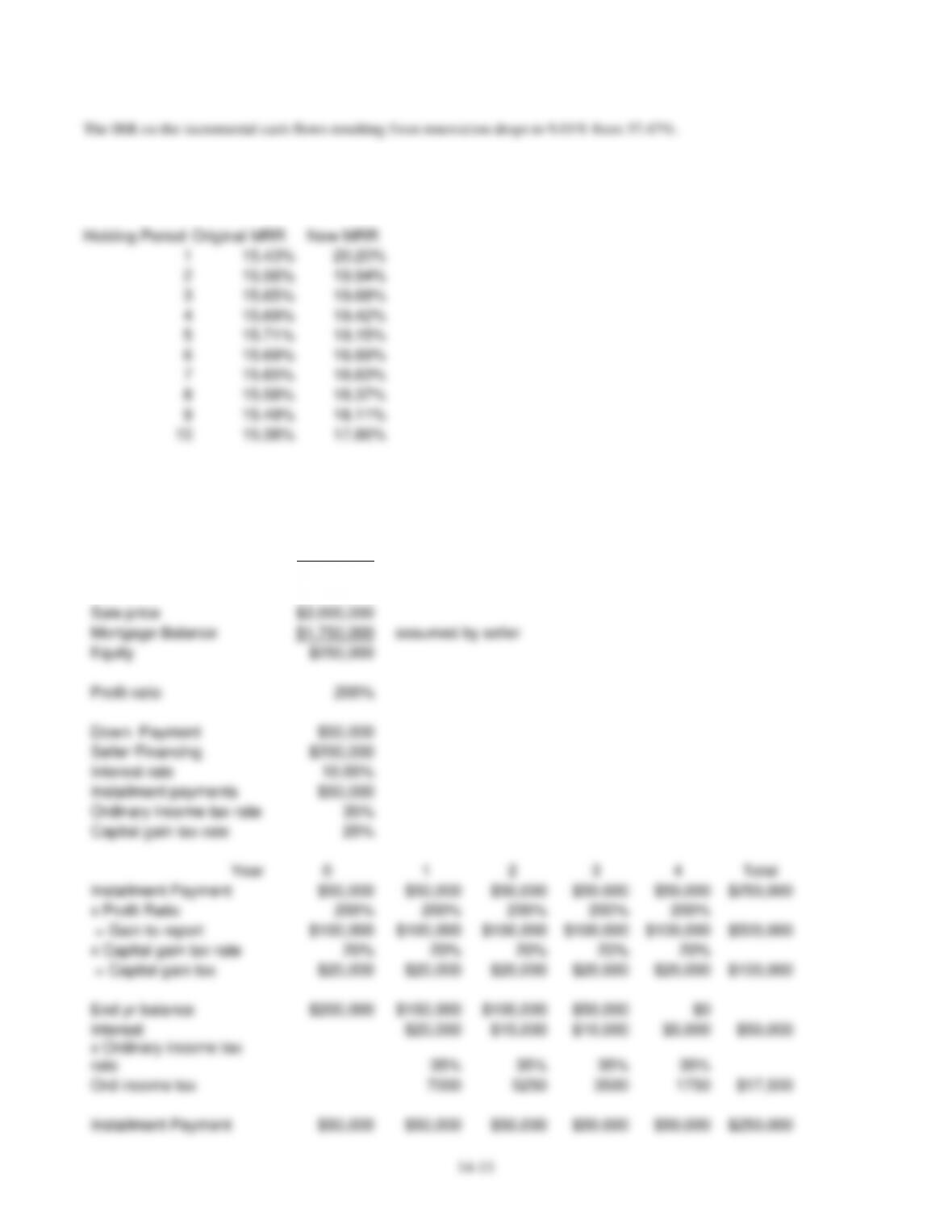

The marginal rate of return (MRR) starts off higher and decreases at a faster rate over time as shown below.

Holding Period

Original MRR

New MRR

1

15.43%

20.20%

2

15.56%

19.94%

3

15.65%

19.68%

4

15.69%

19.42%

5

15.71%

19.15%

6

15.69%

18.89%

7

15.65%

18.63%

8

15.58%

18.37%

9

15.49%

18.11%

10

15.38%

17.86%

Problem 14-7 part a

Sale price

$2,000,000

Adjusted basis

$1,500,000

Capital gain

$500,000

Sale price

$2,000,000

Mortgage Balance

$1,750,000

assumed by seller

Equity

$250,000

Profit ratio

200%

Down Payment

$50,000

Seller Financing

$200,000

Interest rate

10.00%

Installment payments

$50,000

Ordinary income tax rate

35%

Capital gain tax rate

20%

Year

0

1

2

3

4

Total

Installment Payment

$50,000

$50,000

$50,000

$50,000

$50,000

$250,000

x Profit Ratio

200%

200%

200%

200%

200%

= Gain to report

$100,000

$100,000

$100,000

$100,000

$100,000

$500,000

x Capital gain tax rate

20%

20%

20%

20%

20%

= Capital gain tax

$20,000

$20,000

$20,000

$20,000

$20,000

$100,000

End yr balance

$200,000

$150,000

$100,000

$50,000

$0

Interest

$20,000

$15,000

$10,000

$5,000

$50,000

x Ordinary income tax

rate

35%

35%

35%

35%

Ord income tax

7000

5250

3500

1750

$17,500

Installment Payment

$50,000

$50,000

$50,000

$50,000

$50,000

$250,000

14–14

Less ordinary income tax

$0

$7,000

$5,250

$3,500

$1,750

Less capital gain tax

$20,000

$20,000

$20,000

$20,000

$20,000

After tax cash flow

$30,000

$43,000

$39,750

$36,500

$33,250

Discount rate

7.00%

PV

$160,067

Cash Sale

Sale price

$2,000,000

Gain to report

$500,000

Tax

$100,000

Mortgage balance

$1,750,000

After Tax Cash Flow

(PV)

$150,000

Part b.

Exchange versus Regular Sale and Purchase New

Prop

Calc of tax savings if exchanged:

Sale Price if sold today

$2,000,000

Adjusted Basis today

1,500,000

Gain if sold today

$500,000

Capital Gain Tax Rate

20%

Tax if sold today

$100,000

Calc of add dep benefits if not exchanged:

Depreciable life

30

Add depreciation if sale & purchase new

$16,667

Ord inc. tax rate

35%

Dep. tax savings if sale & purchase new

$5,833

Calc of additioal tax at end of holding period if exchanged:

Holding period

5

Additional Gain at sale of exchanged prop

Deferred gain

$500,000

Less: difference in accum dep

$83,333

Net

$416,667

Cap gains tax rate at end of holding period

20%

Additional tax at sale of exchanged prop

$83,333

Calc of return on tax savings from exchange:

PV

($100,000)

PMT

$5,833

FV

$83,333

N

5

Rate

2.67%

This means that by paying the taxes today instead of doing the exchange the investor is only earning 2.67% on his or her

money. This is quite low suggesting that it is better to do the exchange.