Solutions to Questions – Chapter 13

Risk Analysis

Question 13-1

What is meant by partitioning the internal rate of return? Why is this procedure meaningful?

Question 13-2

What is a risk premium? Why does such a premium exist between interest rates on mortgages and rates of return

earned on equity invested in real estate?

A risk premium is a higher expected rate of return paid to an investor as compensation for incurring additional risk

Question 13-3

What are some of the types of risk that should be considered when analyzing real estate and other categories of

investment?

Business Risk

Question 13-4

What is the difference between business risk and financial risk?

Question 13-5

Why is the variance (or standard deviation) used as a measure of risk? What are the advantages and

disadvantages of this risk measure?

Lower variability in returns is considered by many analysts to be associated with lower risk and vice versa.

Therefore, by using a statistical measure of variance, one has an indication of the extent risk is present in an

Question 13-6

What is meant by a ‘ real option’ ?

Question 13-7

What is meant by the term ‘overage’ for retail space ?

Question 13-8

How does the use of scenarios differ from sensitivity analysis ?

Question 13-9

How does the use of Monte Carlo Simulation differ from using scenarios?

Solutions to Problems – Chapter 13

Risk Analysis

INTRODUCTION

Problem 13-1

Investment A

Year BTCF PV

1 $5,000 $4,501

Investment B

Year BTCF PV

1 $2,000 $1,774

(a)

(c)

Problem 13-2

INVESTMENT I

(1)

(2)

(3)

(4)

(5)

(6)

Estimated

Expected

Deviation

Squared

Product

BTIRR

Return

(1) – (2)

Deviation

Probability

(4) x (5)

Optimistic

15.00

10.00

5.00

25.00

0.20

5.00

Most Likely

10.00

10.00

0.00

0.00

0.60

0.00

Pessimistic

5.00

10.00

-5.00

25.00

0.20

5.00

Variance

10.00

Std Deviation

3.16

INVESTMENT II

(1)

(2)

(3)

(4)

(5)

(6)

Estimated

Expected

Deviation

Squared

Product

BTIRR

Return

(1) – (2)

Deviation

Probability

(4) x (5)

Optimistic

20.00

14.00

6.00

36.00

0.20

7.20

Most Likely

15.00

14.00

1.00

1.00

0.60

0.60

Pessimistic

5.00

14.00

-9.00

81.00

0.20

16.20

Variance

24.00

Std Deviation

4.90

The expected BTIRR and standard deviation of the BTIRR are calculated above for Investment I and II. The expected

Problem 13-3

(REFER TO TEMPLATE 13_3.XLS)

ASSUMPTIONS:

Pessimistic

Most-Likely

Optimistic

Scenario Probability

30%

40%

30%

NOI

$200,000

$200,000

$200,000

Change in NOI

-2.00%

0.00%

3.00%

Sale Price

$1,800,000

$2,000,000

$2,200,000

Asking Price

$2,000,000

(a)

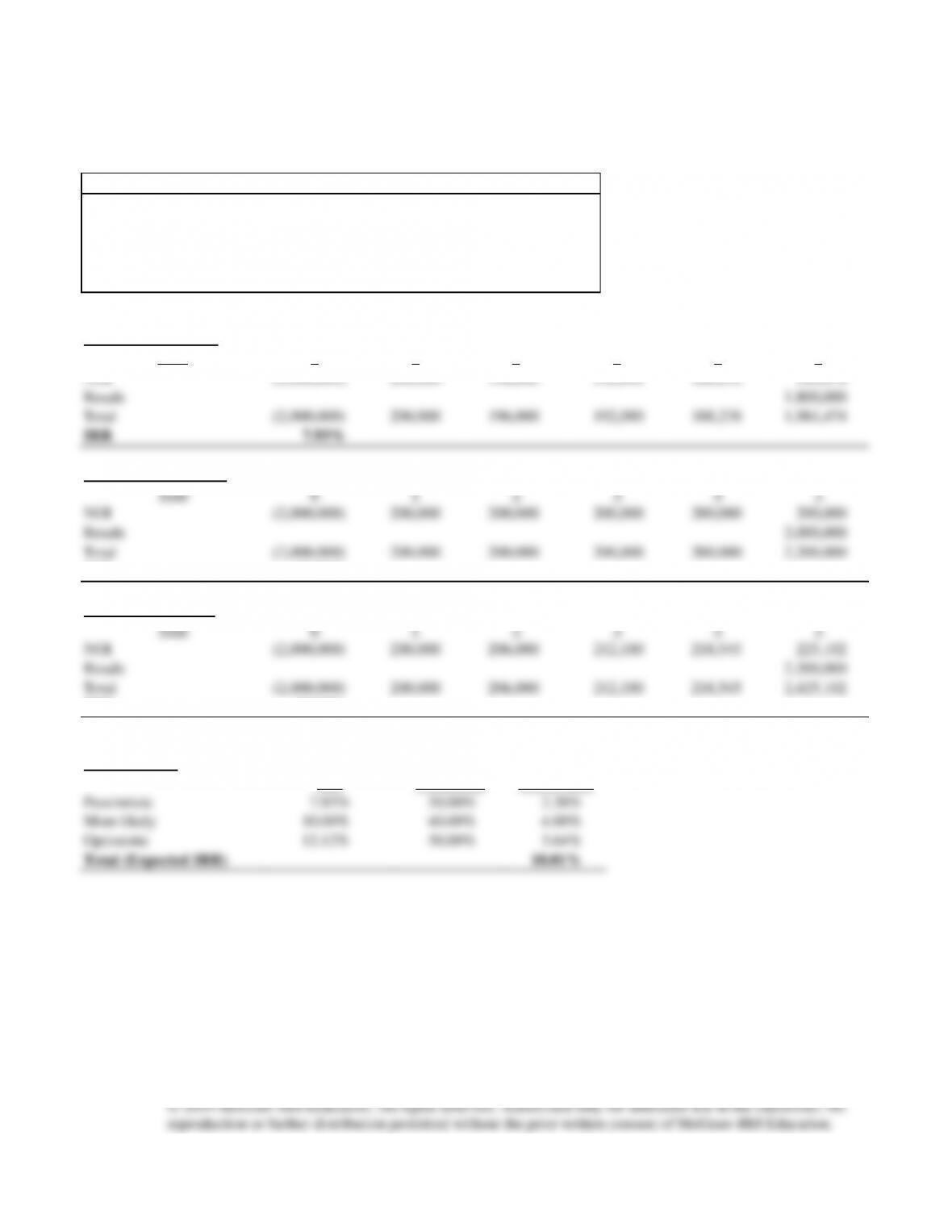

Pessimistic Scenario

Year

0

1

2

3

4

5

NOI

(2,000,000)

200,000

196,000

192,080

188,238

184,474

Resale

1,800,000

Total

(2,000,000)

200,000

196,000

192,080

188,238

1,984,474

IRR

7.93%

Most-Likely Scenario

Year

0

1

2

3

4

5

NOI

(2,000,000)

200,000

200,000

200,000

200,000

200,000

Resale

2,000,000

Total

(2,000,000)

200,000

200,000

200,000

200,000

2,200,000

IRR

10.00%

Optimistic Scenario

Year

0

1

2

3

4

5

NOI

(2,000,000)

200,000

206,000

212,180

218,545

225,102

Resale

2,200,000

Total

(2,000,000)

200,000

206,000

212,180

218,545

2,425,102

IRR

12.12%

(b)

Expected IRR

IRR

Probability

IRR x Prob.

Pessimistic

7.93%

30.00%

2.38%

Most-likely

10.00%

40.00%

4.00%

Optimistic

12.12%

30.00%

3.64%

Total (Expected IRR)

10.01%

(c)

Variance & Standard Deviation

Square of IRR

-Expected IRR

Probability

IRR x Prob.

Pessimistic

0.04%

30.00%

0.01%

Most-likely

0.00%

40.00%

0.00%

Optimistic

0.04%

30.00%

0.01%

Variance

0.0263%

Std. Dev.

1.62%

(d)

Problem 13-4

(REFER TO TEMPLATE 13_4.XLS)

ASSUMPTIONS:

Pessimistic

Most-Likely

Optimistic

Scenario Probability

30%

40%

30%

NOI

200,000

200,000

200,000

Change in NOI

-2.00%

0.00%

3.00%

Sale Price

1,800,000

2,000,000

2,200,000

Holding Period

5

Asking Price

2,000,000

Loan Amount

1,500,000

Loan Term

15

years

Loan Interest Rate

10.00%

Payments per Year

12

Equity

500,000

Annual Debt Service

193,429

Mortgage Balance

1,219,749

end of year

5

(a) IRR AND STANDARD DEVIATION OF RETURN ON EQUITY:

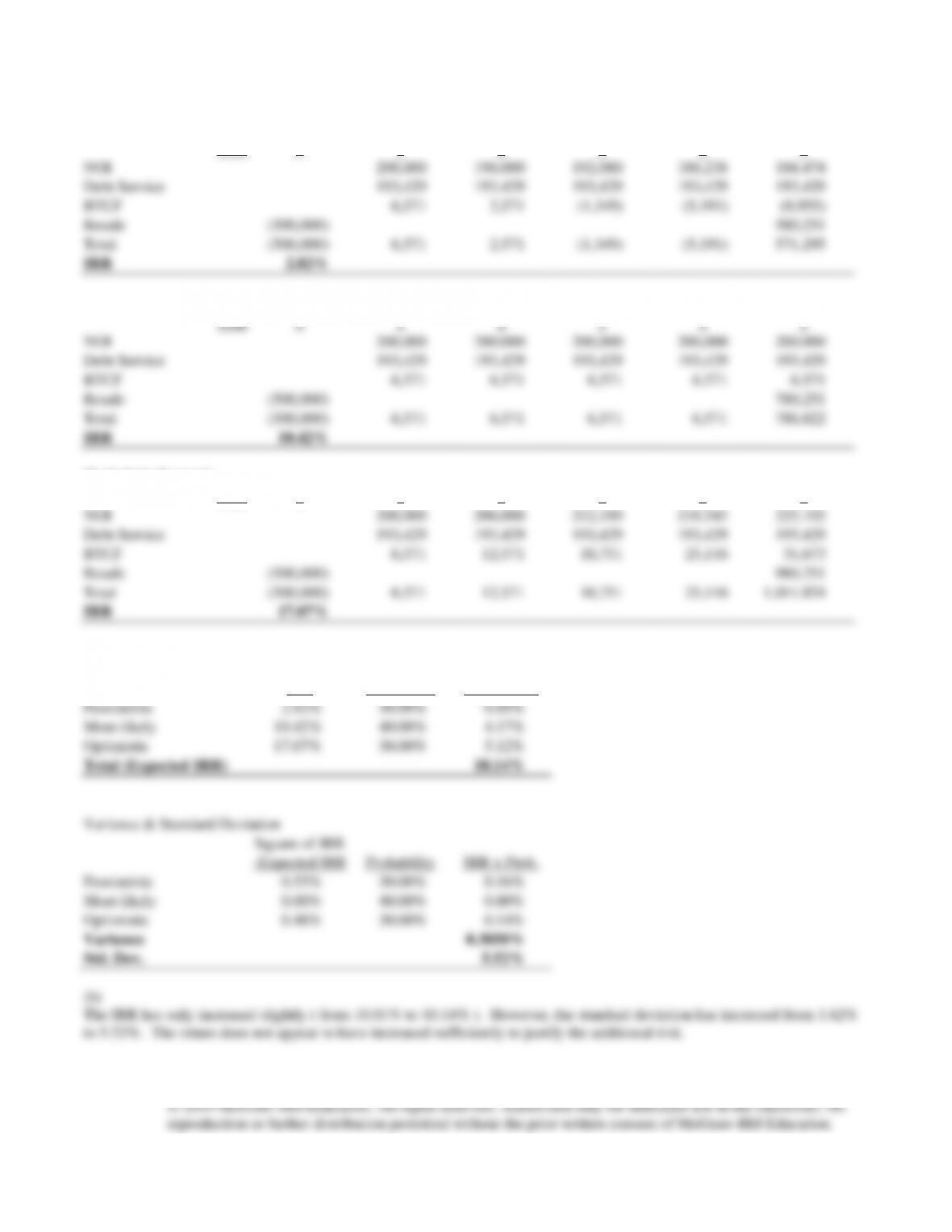

Pessimistic Scenario

Year

0

1

2

3

4

5

NOI

200,000

196,000

192,080

188,238

184,474

Debt Service

193,429

193,429

193,429

193,429

193,429

BTCF

6,571

2,571

(1,349)

(5,191)

(8,955)

Resale

(500,000)

580,251

Total

(500,000)

6,571

2,571

(1,349)

(5,191)

571,295

IRR

2.82%

Most-Likely Scenario

Year

0

1

2

3

4

5

NOI

200,000

200,000

200,000

200,000

200,000

Debt Service

193,429

193,429

193,429

193,429

193,429

BTCF

6,571

6,571

6,571

6,571

6,571

Resale

(500,000)

780,251

Total

(500,000)

6,571

6,571

6,571

6,571

786,822

IRR

10.42%

Optimistic Scenario

Year

0

1

2

3

4

5

NOI

200,000

206,000

212,180

218,545

225,102

Debt Service

193,429

193,429

193,429

193,429

193,429

BTCF

6,571

12,571

18,751

25,116

31,673

Resale

(500,000)

980,251

Total

(500,000)

6,571

12,571

18,751

25,116

1,011,924

IRR

17.07%

Expected IRR

IRR

Probability

IRR x Prob.

Pessimistic

2.82%

30.00%

0.85%

Most-likely

10.42%

40.00%

4.17%

Optimistic

17.07%

30.00%

5.12%

Total (Expected IRR)

10.14%

Variance & Standard Deviation

Square of IRR

-Expected IRR

Probability

IRR x Prob.

Pessimistic

0.53%

30.00%

0.16%

Most-likely

0.00%

40.00%

0.00%

Optimistic

0.48%

30.00%

0.14%

Variance

0.3050%

Std. Dev.

5.52%

(b)

The IRR has only increased slightly ( from 10.01% to 10.14% ). However, the standard deviation has increased from 1.62%

to 5.52%. The return does not appear to have increased sufficiently to justify the additional risk.

Problem 13-5

The value of the land at the end of the year if the NOI is $150,000 is as follows:

Property Value = NOI / (Discount rate – growth rate)

Problem 13-6

Problem 13-7