Year

1

2

3

4

5

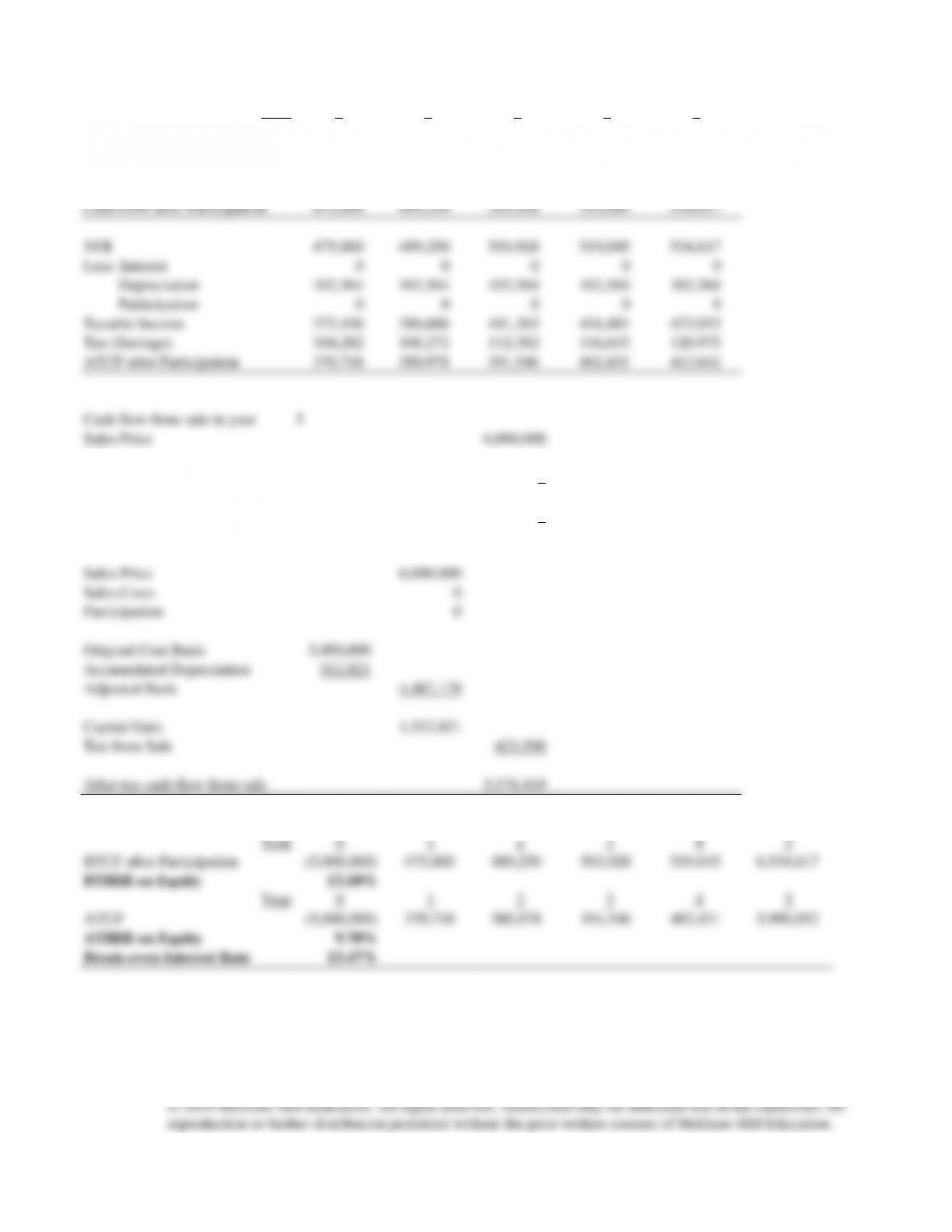

NOI

475,000

489,250

503,928

519,045

534,617

Debt Service

0

0

0

0

0

Before-tax Cash Flow

475,000

489,250

503,928

519,045

534,617

Equity Participation

0

0

0

0

0

Cash Flow after Participation

475,000

489,250

503,928

519,045

534,617

NOI

475,000

489,250

503,928

519,045

534,617

Less: Interest

0

0

0

0

0

Depreciation

102,564

102,564

102,564

102,564

102,564

Participation

0

0

0

0

0

Taxable Income

372,436

386,686

401,363

416,481

432,053

Tax (Savings)

104,282

108,272

112,382

116,615

120,975

ATCF after Participation

370,718

380,978

391,546

402,431

413,642

Cash flow from sale in year

5

Sales Price

6,000,000

Sales costs

0

Mortgage Balance

0

Before-tax cash flow

6,000,000

Participation in Gain

0

BTCF after Participation

6,000,000

Sales Price

6,000,000

Sales Costs

0

Participation

0

Original Cost Basis

5,000,000

Accumulated Depreciation

512,821

Adjusted Basis

4,487,179

Capital Gain

1,512,821

Tax from Sale

423,590

After-tax cash flow from sale

5,576,410

EQUITY

Year

0

1

2

3

4

5

BTCF after Participation

(5,000,000)

475,000

489,250

503,928

519,045

6,534,617

BTIRR on Equity

13.10%

Year

0

1

2

3

4

5

ATCF

(5,000,000)

370,718

380,978

391,546

402,431

5,990,052

ATIRR on Equity

9.70%

Break-even Interest Rate

13.47%

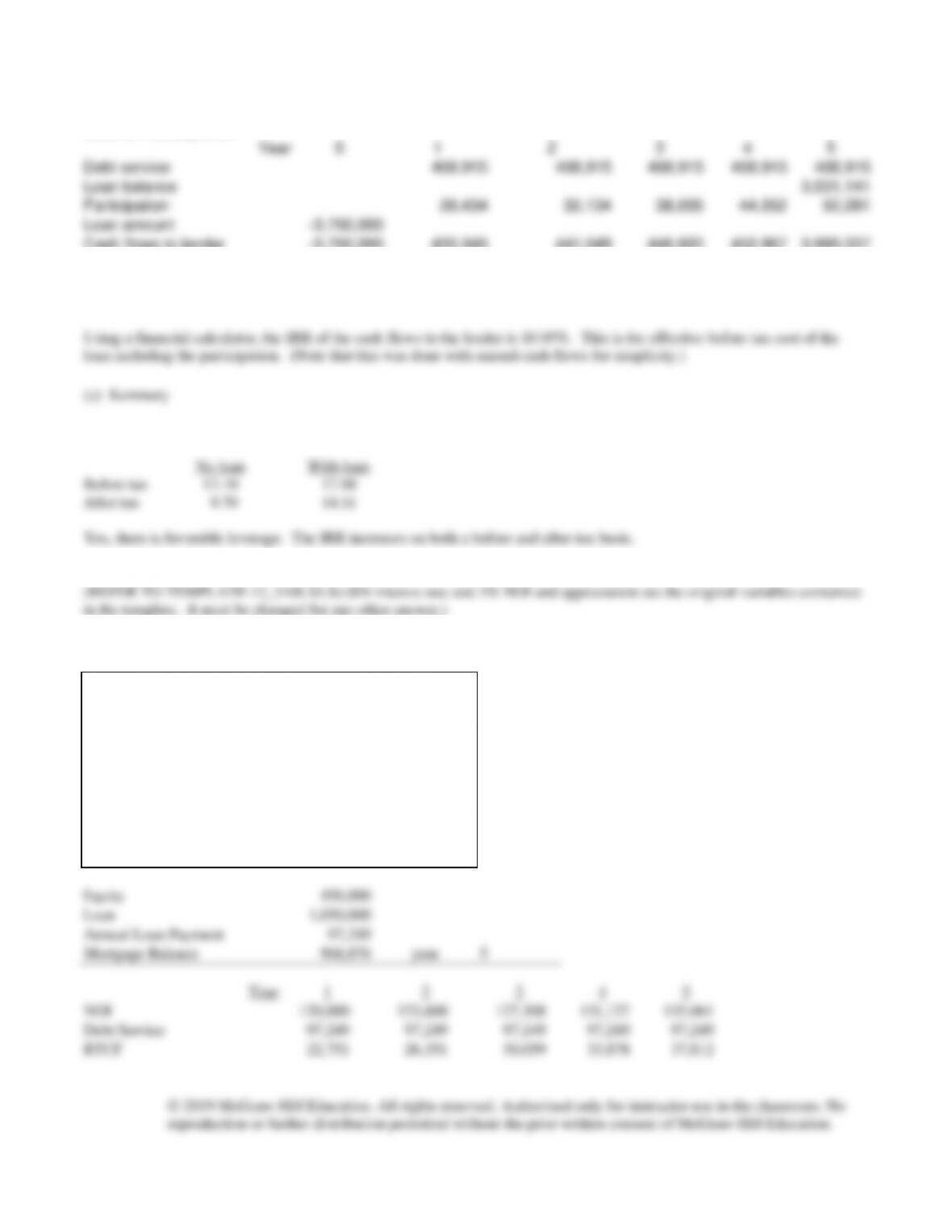

(b) continued – Projected cost of participation.

Cost of Participation

Year

0

1

2

3

4

5

Debt service

408,915

408,915

408,915

408,915

408,915

Loan balance

3,531,141

Participation

26,434

32,134

38,005

44,052

50,281

Loan amount

-3,750,000

Cash flows to lender

-3,750,000

435,349

441,049

446,920

452,967

3,990,337

IRR on Loan

10.95%

IRR

Problem 12-3

(a)

Asking Price

$1,500,000

Rent year 1

$120,000

Growth-NOI

3.00%

Loan-to-Value

70.00%

Loan Interest

8.00%

Loan term

25

years

Appreciation rate

3.00%

Holding Period

5

years

Selling costs

0.00%

of sale price

Required DCR

1.20

DCR

1.23

1.27

1.31

1.35

1.39

Cash flow from sale in year

5

Sales Price

1,738,911

Sales costs

0

Mortgage Balance

968,876

Before-tax cash flow

770,035

BTIRR on Equity

Year

0

1

2

3

4

5

BTCF

(450,000)

22,751

26,351

30,059

33,878

807,847

BTIRR on Equity

16.66%

In this case the DCR is greater than 1.23. Thus, the first-year NOI is 23% higher than necessary to support the debt service.

Based on this criteria, the loan would probably be acceptable.

(b) The maximum loan amount would be $1,067,478

Step 1, Calculate the payment:

(c) (Change 8 to 10% and 3 to 5%. All other variables are constant.)

Asking Price

$1,500,000

Rent year 1

$120,000

Growth-NOI

5.00%

Loan-to-Value

70.00%

Loan Interest

10.00%

Loan term

25

years

Appreciation rate

5.00%

Holding Period

5

years

Selling costs

0.00%

of sale price

Required DCR

1.20

Equity

450,000

Loan

1,050,000

Annual Loan Payment

114,496

Mortgage Balance

988,720

year

5

Year

1

2

3

4

5

NOI

120,000

126,000

132,300

138,915

145,861

Debt Service

114,496

114,496

114,496

114,496

114,496

BTCF

5,504

11,504

17,804

24,419

31,364

DCR

1.05

1.10

1.16

1.21

1.27

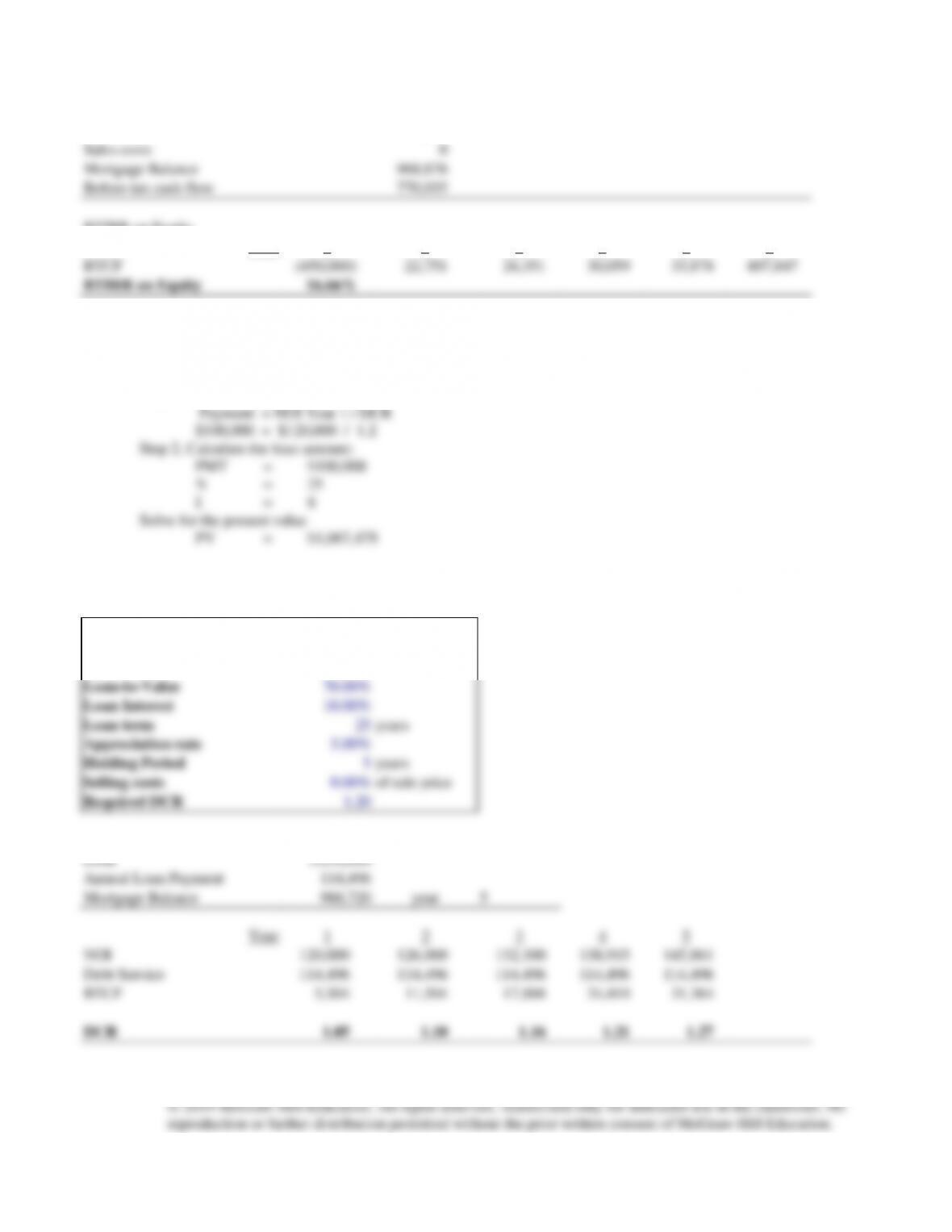

Cash flow from sale in year

5

Sales Price

1,914,422

Sales costs

0

Mortgage Balance

988,720

Before-tax cash flow

925,703

BTIRR on Equity

Year

0

1

2

3

4

5

BTCF

(450,000)

5,504

11,504

17,804

24,419

957,067

BTIRR on Equity

18.25%

The DCR is now much less than 1.2 and it is barely above 1.0. This does not provide a safety margin for the lender. It is not

likely that this loan would be made.

Problem 12-4

(REFER TO TEMPLATE 12_4.XLS)

ASSUMPTIONS:

Purchase Price

2,500,000

NOI

200,000

Loan to Value Ratio

80.00%

Loan Interest Rate

12.00%

Payments per Year

12

Annual Payment Increase

10.00%

Required DCR

1.25

Holding Period

5

years

Year

1

2

3

4

5

NOI

200,000

200,000

200,000

200,000

200,000

Debt Service

160,000

176,000

193,600

212,960

234,256

DCR

1.25

1.14

1.03

0.94

0.85

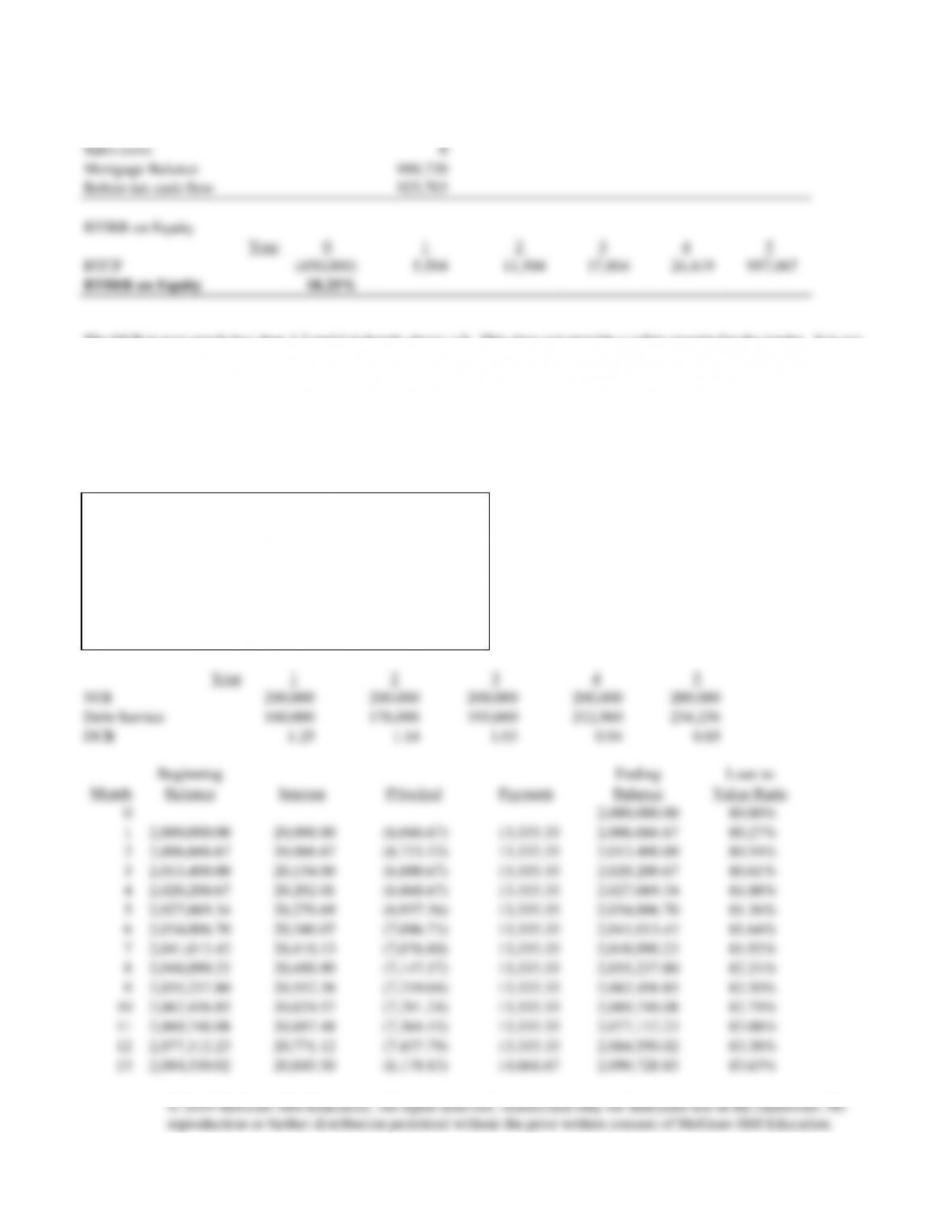

Beginning

Ending

Loan to

Month

Balance

Interest

Principal

Payment

Balance

Value Ratio

0

2,000,000.00

80.00%

1

2,000,000.00

20,000.00

(6,666.67)

13,333.33

2,006,666.67

80.27%

2

2,006,666.67

20,066.67

(6,733.33)

13,333.33

2,013,400.00

80.54%

3

2,013,400.00

20,134.00

(6,800.67)

13,333.33

2,020,200.67

80.81%

4

2,020,200.67

20,202.01

(6,868.67)

13,333.33

2,027,069.34

81.08%

5

2,027,069.34

20,270.69

(6,937.36)

13,333.33

2,034,006.70

81.36%

6

2,034,006.70

20,340.07

(7,006.73)

13,333.33

2,041,013.43

81.64%

7

2,041,013.43

20,410.13

(7,076.80)

13,333.33

2,048,090.23

81.92%

8

2,048,090.23

20,480.90

(7,147.57)

13,333.33

2,055,237.80

82.21%

9

2,055,237.80

20,552.38

(7,219.04)

13,333.33

2,062,456.85

82.50%

10

2,062,456.85

20,624.57

(7,291.24)

13,333.33

2,069,748.08

82.79%

11

2,069,748.08

20,697.48

(7,364.15)

13,333.33

2,077,112.23

83.08%

12

2,077,112.23

20,771.12

(7,437.79)

13,333.33

2,084,550.02

83.38%

13

2,084,550.02

20,845.50

(6,178.83)

14,666.67

2,090,728.85

83.63%

14

2,090,728.85

20,907.29

(6,240.62)

14,666.67

2,096,969.48

83.88%

15

2,096,969.48

20,969.69

(6,303.03)

14,666.67

2,103,272.50

84.13%

16

2,103,272.50

21,032.73

(6,366.06)

14,666.67

2,109,638.56

84.39%

17

2,109,638.56

21,096.39

(6,429.72)

14,666.67

2,116,068.28

84.64%

18

2,116,068.28

21,160.68

(6,494.02)

14,666.67

2,122,562.30

84.90%

19

2,122,562.30

21,225.62

(6,558.96)

14,666.67

2,129,121.25

85.16%

20

2,129,121.25

21,291.21

(6,624.55)

14,666.67

2,135,745.80

85.43%

21

2,135,745.80

21,357.46

(6,690.79)

14,666.67

2,142,436.59

85.70%

22

2,142,436.59

21,424.37

(6,757.70)

14,666.67

2,149,194.29

85.97%

23

2,149,194.29

21,491.94

(6,825.28)

14,666.67

2,156,019.57

86.24%

24

2,156,019.57

21,560.20

(6,893.53)

14,666.67

2,162,913.10

86.52%

25

2,162,913.10

21,629.13

(5,495.80)

16,133.33

2,168,408.89

86.74%

26

2,168,408.89

21,684.09

(5,550.76)

16,133.33

2,173,959.65

86.96%

27

2,173,959.65

21,739.60

(5,606.26)

16,133.33

2,179,565.91

87.18%

28

2,179,565.91

21,795.66

(5,662.33)

16,133.33

2,185,228.24

87.41%

29

2,185,228.24

21,852.28

(5,718.95)

16,133.33

2,190,947.19

87.64%

30

2,190,947.19

21,909.47

(5,776.14)

16,133.33

2,196,723.32

87.87%

31

2,196,723.32

21,967.23

(5,833.90)

16,133.33

2,202,557.22

88.10%

32

2,202,557.22

22,025.57

(5,892.24)

16,133.33

2,208,449.46

88.34%

33

2,208,449.46

22,084.49

(5,951.16)

16,133.33

2,214,400.62

88.58%

34

2,214,400.62

22,144.01

(6,010.67)

16,133.33

2,220,411.30

88.82%

35

2,220,411.30

22,204.11

(6,070.78)

16,133.33

2,226,482.08

89.06%

36

2,226,482.08

22,264.82

(6,131.49)

16,133.33

2,232,613.56

89.30%

37

2,232,613.56

22,326.14

(4,579.47)

17,746.67

2,237,193.03

89.49%

38

2,237,193.03

22,371.93

(4,625.26)

17,746.67

2,241,818.30

89.67%

39

2,241,818.30

22,418.18

(4,671.52)

17,746.67

2,246,489.81

89.86%

40

2,246,489.81

22,464.90

(4,718.23)

17,746.67

2,251,208.05

90.05%

41

2,251,208.05

22,512.08

(4,765.41)

17,746.67

2,255,973.46

90.24%

42

2,255,973.46

22,559.73

(4,813.07)

17,746.67

2,260,786.53

90.43%

43

2,260,786.53

22,607.87

(4,861.20)

17,746.67

2,265,647.73

90.63%

44

2,265,647.73

22,656.48

(4,909.81)

17,746.67

2,270,557.54

90.82%

45

2,270,557.54

22,705.58

(4,958.91)

17,746.67

2,275,516.44

91.02%

46

2,275,516.44

22,755.16

(5,008.50)

17,746.67

2,280,524.94

91.22%

47

2,280,524.94

22,805.25

(5,058.58)

17,746.67

2,285,583.53

91.42%

48

2,285,583.53

22,855.84

(5,109.17)

17,746.67

2,290,692.69

91.63%

49

2,290,692.69

22,906.93

(3,385.59)

19,521.33

2,294,078.29

91.76%

50

2,294,078.29

22,940.78

(3,419.45)

19,521.33

2,297,497.74

91.90%

51

2,297,497.74

22,974.98

(3,453.64)

19,521.33

2,300,951.38

92.04%

52

2,300,951.38

23,009.51

(3,488.18)

19,521.33

2,304,439.56

92.18%

53

2,304,439.56

23,044.40

(3,523.06)

19,521.33

2,307,962.62

92.32%

54

2,307,962.62

23,079.63

(3,558.29)

19,521.33

2,311,520.92

92.46%

55

2,311,520.92

23,115.21

(3,593.88)

19,521.33

2,315,114.79

92.60%

56

2,315,114.79

23,151.15

(3,629.81)

19,521.33

2,318,744.61

92.75%

57

2,318,744.61

23,187.45

(3,666.11)

19,521.33

2,322,410.72

92.90%

58

2,322,410.72

23,224.11

(3,702.77)

19,521.33

2,326,113.49

93.04%

59

2,326,113.49

23,261.13

(3,739.80)

19,521.33

2,329,853.30

93.19%

60

2,329,853.30

23,298.53

(3,777.20)

19,521.33

2,333,630.50

93.35%

(a)

(b)

Problem 12-5

(b)

Interest accrues at 10%. On $1,000,000 this is $100,000 per year or $8,333.33 per month. In this case, payments do not

cover the interest, although the loan would not be amortized in 30 years. For this reason the future value of the loan will be

(c)

Using the same approach as above we can get the balance after 5 years.

(d)

To amortize the loan over the remaining 10 years, we can use a financial calculator as follows:

Problem 12-6

Purchase price

$1,000,000

Loan amount

$900,000

Interest rate

8.00%

Initial NOI

$100,000

Loan term

20

Growth in NOI

3.00%

Monthly payment

$7,527.96

Base for participation

$100,000

Annual payment

$90,335.53

Participation % of NOI

50.00%

Terminal cap rate

10.00%

Participation in price increase

50.00%

Resale price

$1,343,916

Purchase price

$1,000,000

Increase in value

$343,916

Participation in sale

$171,958

Loan balance at resale

$620,466

Year

NOI

Excess over base

Participation

Debt service

Lender cash flow

0

-$900,000

1

100,000

0

0

90,336

90,336

2

103,000

3,000

1,500

90,336

91,836

3

106,090

6,090

3,045

90,336

93,381

4

109,273

9,273

4,636

90,336

94,972

5

112,551

12,551

6,275

90,336

96,611

6

115,927

15,927

7,964

90,336

98,299

7

119,405

19,405

9,703

90,336

100,038

8

122,987

22,987

11,494

90,336

101,829

9

126,677

26,677

13,339

90,336

103,674

10

130,477

30,477

187,197

90,336

897,998

*

11

134,392

IRR

9.95%

*Includes participation in NOI, Resale, and loan balance

Problem 12-7

(a)

Purchase price

$1,000,000

Loan amount

$900,000

Interest rate

9.00%

Initial NOI

$100,000

Loan term

20

Growth in NOI

3.00%

Monthly payment

$8,097.53

Base for participation

$100,000

Annual payment

$97,170.40

Participation % of NOI

50.00%

Terminal cap rate

10.00%

Conversion percentage

60.00%

Resale price

$1,343,916

Conversion value

$806,350

Loan balance at resale

$639,233

Lender cash flow if no default

$806,350

(lender gets higher of conversion value or loan balance)

Lender cash flow if default allowed

$806,350

(lender gets property if less than loan balance at resale)

Year

Debt service

Lender cash flow

0

-$900,000

1

97,170

97,170

2

97,170

97,170

3

97,170

97,170

4

97,170

97,170

5

97,170

97,170

6

97,170

97,170

7

97,170

97,170

8

97,170

97,170

9

97,170

97,170

10

97,170

903,520

*

IRR

10.15%

*Includes debt service plus either loan balance, conversion value or default proceeds.

Note: In this case the lender would want to convert to ownership in the property because 60% of the resale value is

greater than the loan balance.

(b)

Purchase price

$1,000,000

Loan amount

$900,000

Interest rate

9.00%

Initial NOI

$100,000

Loan term

20

Growth in NOI

3.00%

Monthly payment

$8,097.53

Base for participation

$100,000

Annual payment

$97,170.40

Participation % of NOI

50.00%

Terminal cap rate

10.00%

Conversion percentage

60.00%

Resale price

$1,000,000

Conversion value

$600,000

Loan balance at resale

$639,233

Lender cash flow if no default

$639,233

(lender gets higher of conversion value or loan balance)

Lender cash flow if default allowed

$639,233

(lender gets property if less than loan balance at resale)

Year

Debt service

Lender cash flow

0

-$900,000

1

97,170

97,170

2

97,170

97,170

3

97,170

97,170

4

97,170

97,170

5

97,170

97,170

6

97,170

97,170

7

97,170

97,170

8

97,170

97,170

9

97,170

97,170

10

97,170

736,403

*

IRR

8.88%

*Includes debt service plus either loan balance, conversion value or default proceeds.

Note: In this case the lender would not want to convert because the mortgage balance after 10 years is greater than

(c)

Purchase price

$1,000,000

Loan amount

$900,000

Interest rate

9.00%

Initial NOI

$100,000

Loan term

20

Growth in NOI

3.00%

Monthly payment

$8,097.53

Base for participation

$100,000

Annual payment

$97,170.40

Participation % of NOI

50.00%

Terminal cap rate

10.00%

Conversion percentage

60.00%

Resale price

$500,000

Conversion value

$300,000

Loan balance at resale

$639,233

Lender cash flow if no default

$639,233

(lender gets higher of conversion value or loan balance)

Lender cash flow if default allowed

$500,000

(lender gets property if less than loan balance at resale)

Year

Debt service

Lender cash flow

0

-$900,000

1

97,170

97,170

2

97,170

97,170

3

97,170

97,170

4

97,170

97,170

5

97,170

97,170

6

97,170

97,170

7

97,170

97,170

8

97,170

97,170

9

97,170

97,170

10

97,170

597,170

*

IRR

7.68%

*Includes debt service plus either loan balance, conversion value or default proceeds.

Problem 12-8

This question is like an example in the chapter.

(a) Reinvestment Rate = 6% + 1.5%

Problem 12-9

Problem 12-10