Solutions to Questions – Chapter 12

Financial Leverage and Financing Alternatives

Question 12-1

What is financial leverage? Why is a one-year measure of return on investment inadequate in determining whether

positive or negative financial leverage exists?

Question 12-2

What is the break-even mortgage interest rate (BEIR) in the context of financial leverage? Would you ever expect

an investor to pay a break-even interest rate when financing a property? Why or why not?

Question 12-3

What is positive and negative financial leverage? How are returns or losses magnified as the degree of leverage

increases? How does leverage on a before-tax basis differ from leverage on an after-tax basis?

Question 12-4

In what way does leverage increase the riskiness of a loan?

Question 12-5

What is meant by a participation loan? What does the lender participate in? Why would a lender want to make a

participation loan? Why would an investor want to obtain a participation loan?

Question 12-6

What is meant by a sale-leaseback? Why would a building investor want to do a sale-leaseback of the land? What

is the benefit to the party that purchases the land under a sale-leaseback?

Question 12-7

Why might an investor prefer a loan with a lower interest rate and a participation?

Question 12-8

Why might a lender prefer a loan with a lower interest rate and a participation?

Question 12-9

How do you think participations affect the riskiness of a loan?

Question 12-10

What is the motivation for a sale-leaseback of the land?

Question 12-11

What criteria should be used to choose between two financing alternatives?

Question 12-12

What is the traditional cash equivalency approach to determine how below-market rate loans affect value?

Question 12-13

How can the effect of below-market rate loans on value be determined using investor criteria?

Solutions to Problems – Chapter 12

Financial Leverage and Financing Alternatives

INTRODUCTION

The problems in this chapter are designed to reinforce the students’ understanding of alternative methods of structuring debt

financing and how financing can affect the cash flows and the leverage of the real estate project. The conditions necessary

for positive financing leverage and how the use financial leverage affects risk are also discussed.

The third problem extends problem 5 in chapter 10 which involved calculation of the expected return and standard deviation

for an investment. In this chapter financing is added to the problem. Instructors should emphasize that the risk (measured b

the standard deviation) will always increase with leverage. However, whether the expected return increases depends on

whether leverage is favorable or unfavorable.

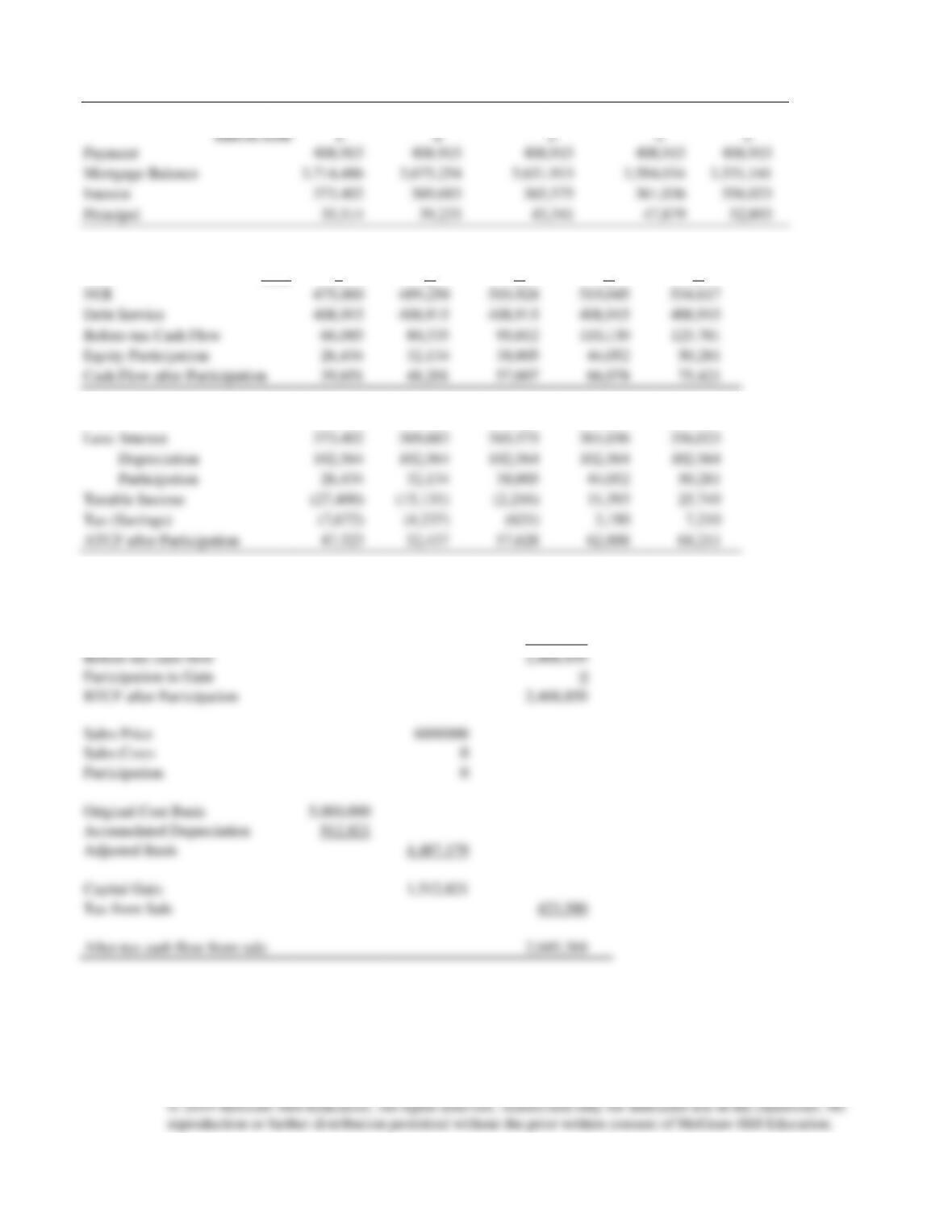

Problem 12-1

(REFER TO TEMPLATE 12_1.XLS)

(a) 70% LOAN (70% and 10% are the original variables contained in the template. It must be changed for any other

answer.)

Year

1

2

3

4

5

NOI

190,000

195,700

201,571

207,618

213,847

Debt Service

152,662

152,662

152,662

152,662

152,662

Before-tax Cash Flow

37,338

43,038

48,909

54,956

61,185

NOI

190,000

195,700

201,571

207,618

213,847

Less: Interest

139,403

138,015

136,481

134,787

132,915

Depreciation

58,182

58,182

58,182

58,182

58,182

Taxable Income

(7,585)

(497)

6,908

14,649

22,750

Tax (Savings)

(2,731)

(179)

2,487

5,274

8,190

After-tax Cash Flow

40,069

43,217

46,422

49,683

52,995

Cash flow from sale in year

5

Sales Price

2,318,548

Sales costs

0

Mortgage Balance

1,318,293

Before-tax cash flow

1,000,255

Original Cost Basis

2,000,000

Accumulated Depreciation

290,909

Adjusted Basis

1,709,091

Capital Gain

609,457

Tax from Sale

219,405

After-tax cash flow from sale

780,851

EQUITY

Year

0

1

2

3

4

5

BTCF

(600,000)

37,338

43,038

48,909

54,956

1,061,440

BTIRR on Equity

17.32%

Year

0

1

2

3

4

5

ATCF

(600,000)

40,069

43,217

46,422

49,683

833,846

ATIRR on Equity

12.33%

(a) 80% LOAN (Change 70 to 80% and 10 to 11%. All other variables are constant.)

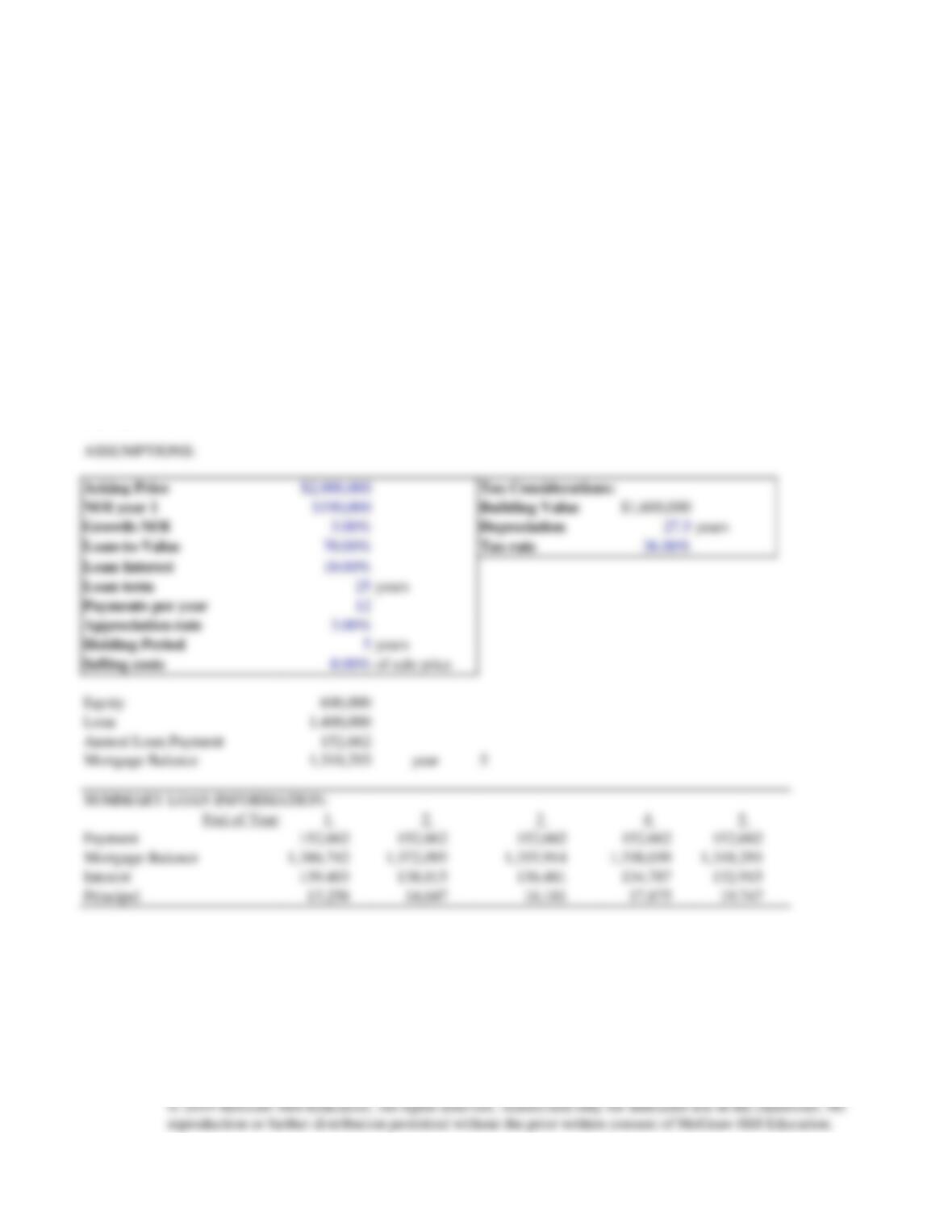

ASSUMPTIONS:

Asking Price

$2,000,000

Tax Considerations:

NOI year 1

$190,000

Building Value

$1,600,000

Growth-NOI

3.00%

Depreciation

27.5

years

Loan-to-Value

80.00%

Tax rate*

36.00%*

Loan Interest

11.00%

Loan term

25

years

Payments per year

12

Appreciation rate

3.00%

Holding Period

5

years

Selling costs

0.00%

of sale price

Equity

400,000

Loan

1,600,000

Annual Loan Payment

188,182

Mortgage Balance

1,519,278

year

5

SUMMARY LOAN INFORMATION:

End of Year

1

2

3

4

5

Payment

188,182

188,182

188,182

188,182

188,182

Mortgage Balance

1,587,185

1,572,887

1,556,934

1,539,136

1,519,278

Interest

175,367

173,884

172,229

170,383

168,324

Principal

12,815

14,298

15,953

17,799

19,858

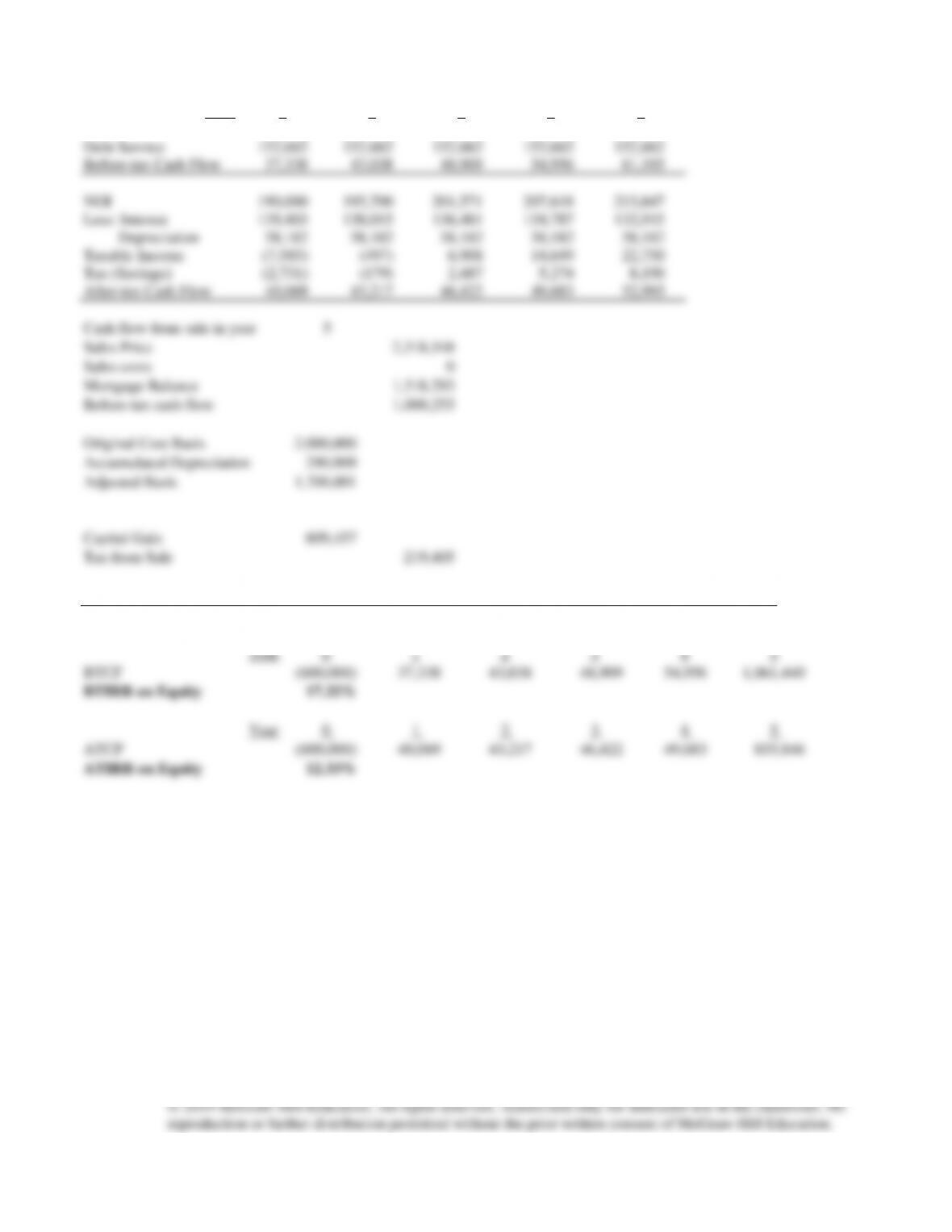

Year

1

2

3

4

5

NOI

190,000

195,700

201,571

207,618

213,847

Debt Service

188,182

188,182

188,182

188,182

188,182

Before-tax Cash Flow

1,818

7,518

13,389

19,436

25,665

NOI

190,000

195,700

201,571

207,618

213,847

Less: Interest

175,367

173,884

172,229

170,383

168,324

Depreciation

58,182

58,182

58,182

58,182

58,182

Taxable Income

(43,548)

(36,366)

(28,840)

(20,947)

(12,659)

Tax (Savings)

(15,677)

(13,092)

(10,382)

(7,541)

(4,557)

After-tax Cash Flow

17,496

20,610

23,772

26,977

30,222

Cash flow from sale in year

5

Sales Price

2,318,548

Sales costs

0

Mortgage Balance

1,519,278

Before-tax cash flow

799,270

Original Cost Basis

2,000,000

Accumulated Depreciation

290,909

Adjusted Basis

1,709,091

Capital Gain

609,457

Tax from Sale

219,405

*To be applied to all items of

income, capital gains and

recapture of depreciation.

After-tax cash flow from sale

579,866

EQUITY

Year

0

1

2

3

4

5

BTCF

(400,000)

1,818

7,518

13,389

19,436

824,935

BTIRR on Equity

17.12%

Year

0

1

2

3

4

5

ATCF

(400,000)

17,496

20,610

23,772

26,977

610,088

ATIRR on Equity

12.74%

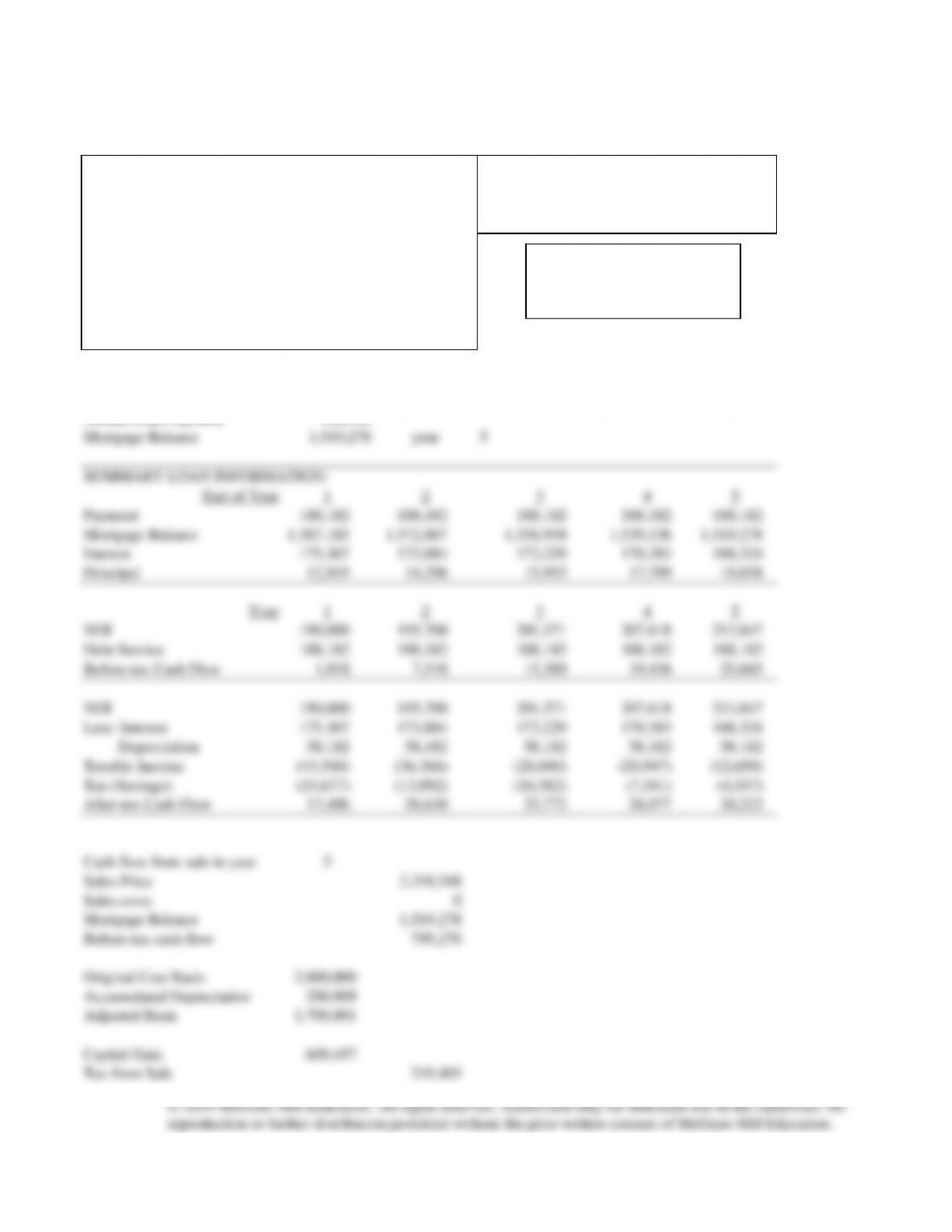

(b) BEIR

(To calculate the Break Even Interest Rate (BEIR), the ATIRR must first be calculated as if there were no

financing.)

ASSUMPTIONS:

Asking Price

$2,000,000

Tax Considerations:

NOI year 1

$190,000

Building Value

$1,600,000

Growth-NOI

3.00%

Depreciation

27.5

years

Loan-to-Value

0.00%

Tax rate

36.00%

Loan Interest

11.00%

Loan term

25

years

Payments per year

12

Appreciation rate

3.00%

Holding Period

5

years

Selling costs

0.00%

of sale price

Equity

2,000,000

Loan

0

Annual Loan Payment

0

Mortgage Balance

0

year

5

SUMMARY LOAN INFORMATION:

End of Year

1

2

3

4

5

Payment

0

0

0

0

0

Mortgage Balance

0

0

0

0

0

Interest

0

0

0

0

0

Principal

0

0

0

0

0

*To be applied to all items of

income, capital gains and

recapture of depreciation.

Year

1

2

3

4

5

NOI

190,000

195,700

201,571

207,618

213,847

Debt Service

0

0

0

0

0

Before-tax Cash Flow

190,000

195,700

201,571

207,618

213,847

NOI

190,000

195,700

201,571

207,618

213,847

Less: Interest

0

0

0

0

0

Depreciation

58,182

58,182

58,182

58,182

58,182

Taxable Income

131,818

137,518

143,389

149,436

155,665

Tax (Savings)

47,455

49,507

51,620

53,797

56,039

After-tax Cash Flow

142,545

146,193

149,951

153,821

157,807

Cash flow from sale in year

5

Sales Price

2,318,548

Sales costs

0

Mortgage Balance

0

Before-tax cash flow

2,318,548

Original Cost Basis

2,000,000

Accumulated Depreciation

290,909

Adjusted Basis

1,709,091

Capital Gain

609,457

Tax from Sale

219,405

After-tax cash flow from sale

2,099,144

EQUITY

Year

0

1

2

3

4

5

BTCF

(2,000,000)

190,000

195,700

201,571

207,618

2,532,395

BTIRR on Equity

12.50%

Year

0

1

2

3

4

5

ATCF

(2,000,000)

142,545

146,193

149,951

153,821

2,256,951

ATIRR on Equity

8.31%

Break-even Interest Rate

12.99%

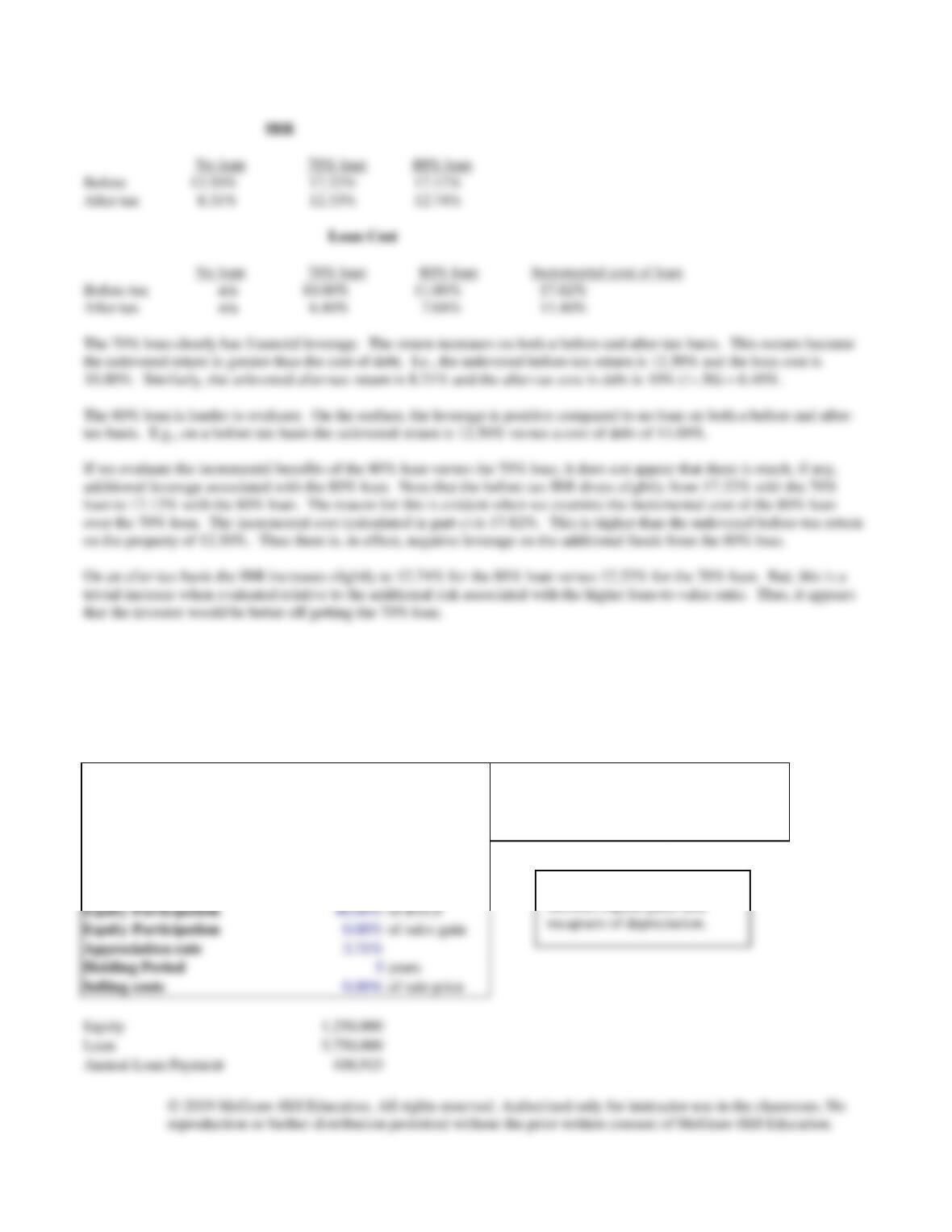

(c) The incremental amount of financing is $200,000. The incremental payment is $2,960 and the incremental loan balance

is $200,985. Thus, $200,000 = $2,960 (MPVIFA, ?%, 5 yrs) + $200,985 (MPVIF, ?%, 5 yrs).

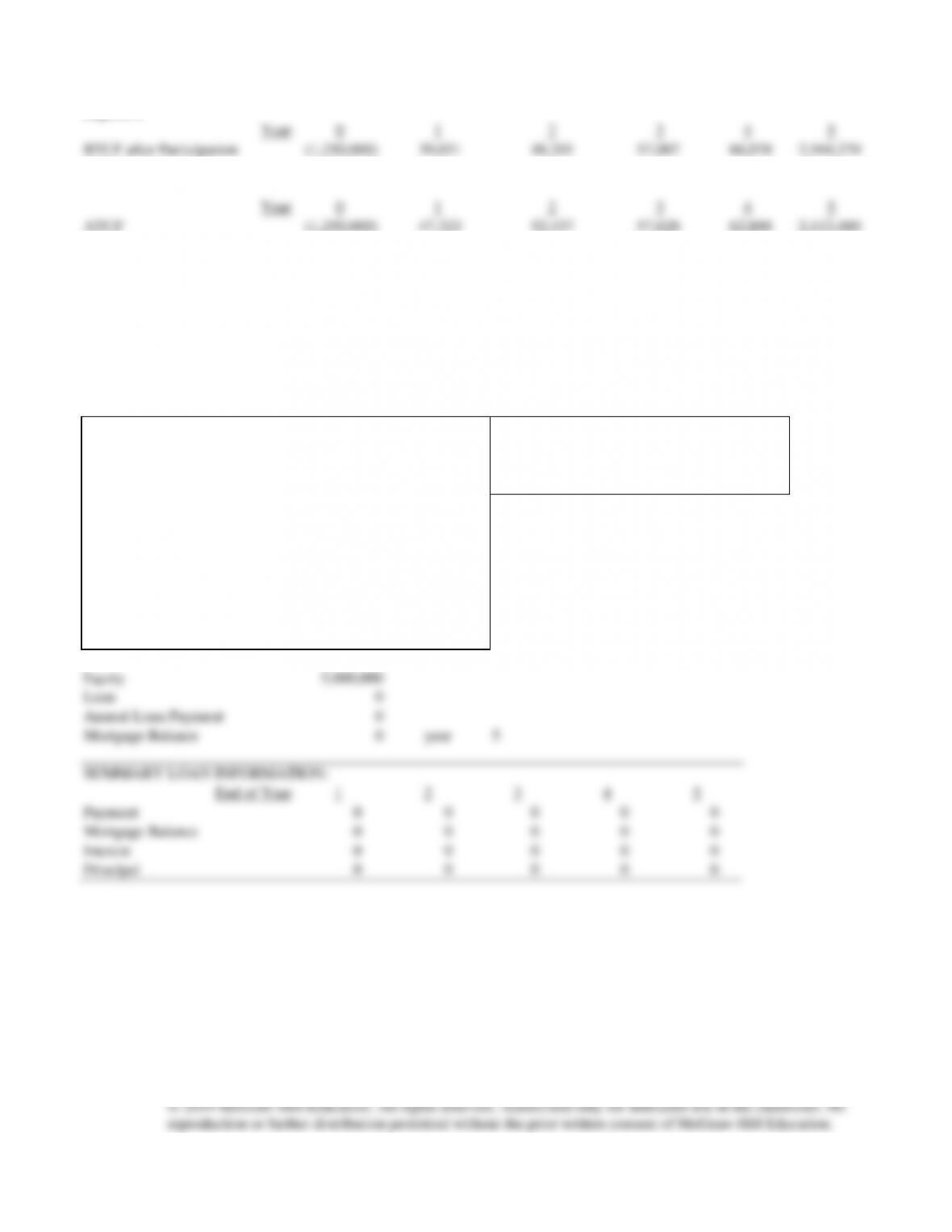

(d) To answer this question it is helpful to prepare the following summary:

Problem 12-2

(REFER TO TEMPLATE 12_2.XLS)

(a)

ASSUMPTIONS:

Asking Price

$5,000,000

Tax Considerations:

NOI year 1

$475,000

Building Value

$4,000,000

Growth-NOI

3.00%

Depreciation

39

years

Loan-to-Value

75.00%

Tax rate

28.00%

Loan Interest

10.00%

Loan term

25

years

Payments per year

12

Equity Participation

40.00%

of BTCF

Equity Participation

0.00%

of sales gain

Appreciation rate

3.71%

Holding Period

5

years

Selling costs

0.00%

of sale price

Equity

1,250,000

Loan

3,750,000

Annual Loan Payment

408,915

*To be applied to all items of

income, capital gains and

recapture of depreciation.

Mortgage Balance

3,531,141

year

5

SUMMARY LOAN INFORMATION:

End of Year

1

2

3

4

5

Payment

408,915

408,915

408,915

408,915

408,915

Mortgage Balance

3,714,486

3,675,254

3,631,913

3,584,034

3,531,141

Interest

373,402

369,683

365,575

361,036

356,023

Principal

35,514

39,233

43,341

47,879

52,893

Year

1

2

3

4

5

NOI

475,000

489,250

503,928

519,045

534,617

Debt Service

408,915

408,915

408,915

408,915

408,915

Before-tax Cash Flow

66,085

80,335

95,012

110,130

125,701

Equity Participation

26,434

32,134

38,005

44,052

50,281

Cash Flow after Participation

39,651

48,201

57,007

66,078

75,421

NOI

475,000

489,250

503,928

519,045

534,617

Less: Interest

373,402

369,683

365,575

361,036

356,023

Depreciation

102,564

102,564

102,564

102,564

102,564

Participation

26,434

32,134

38,005

44,052

50,281

Taxable Income

(27,400)

(15,131)

(2,216)

11,393

25,749

Tax (Savings)

(7,672)

(4,237)

(621)

3,190

7,210

ATCF after Participation

47,323

52,437

57,628

62,888

68,211

Cash flow from sale in year

5

Sales Price

6,000,000

Sales costs

0

Mortgage Balance

3,531,141

Before-tax cash flow

2,468,859

Participation in Gain

0

BTCF after Participation

2,468,859

Sales Price

6000000

Sales Costs

0

Participation

0

Original Cost Basis

5,000,000

Accumulated Depreciation

512,821

Adjusted Basis

4,487,179

Capital Gain

1,512,821

Tax from Sale

423,590

After-tax cash flow from sale

2,045,269

Payment

0

0

0

Mortgage Balance

0

0

0

Interest

0

0

0

Principal

0

0

0

EQUITY

Year

0

1

2

3

4

5

BTCF after Participation

(1,250,000)

39,651

48,201

57,007

66,078

2,544,279

BTIRR on Equity

17.98%

Year

0

1

2

3

4

5

ATCF

(1,250,000)

47,323

52,437

57,628

62,888

2,113,480

ATIRR on Equity

14.11%

(b) BEIR (To calculate the Break Even Interest Rate (BEIR), the ATIRR must first be calculated as if there were no

financing.)

NO LOAN (Change 75 to 0% and remove the participation by changing 40 to 0%. All other variables are constant.)

ASSUMPTIONS:

Asking Price

$5,000,000

Tax Considerations:

NOI year 1

$475,000

Building Value

$4,000,000

Growth-NOI

3.00%

Depreciation

39

years

Loan-to-Value

0.00%

Tax rate

28.00%

Loan Interest

10.00%

Loan term

25

years

Payments per year

12

Equity Participation

0.00%

of BTCF

Equity Participation

0.00%

of sales gain

Appreciation rate

3.71%

Holding Period

5

years

Selling costs

0.00%

of sale price

Equity

5,000,000

Loan

0

Annual Loan Payment

0

Mortgage Balance

0

year

5