Solution to Questions – Chapter 10

Valuation of Income Properties: Appraisal and the Market for Capital

Question 10-1

What is the economic rationale for the cost approach? Under what conditions would the cost approach tend to

give the best value estimate?

Question 10-2

What is the economic rationale for the sales comparison approach? What information is necessary to use this

approach? What does it mean for a property to be comparable?

Question 10-3

What is a capitalization rate? What are the different ways of arriving at an overall rate to use for an appraisal?

Question 10-4

If investors buy properties based on expected future benefits, what is the rationale for appraising a property

without making any income or resale price projections?

Question 10-5

What is the relationship between a discount rate and a capitalization rate?

Question 10-6

What is meant by a unit of comparison? Why is it important?

Question 10-7

Why do you think appraisers usually use three different approaches when estimating value?

Question 10-8

Under what conditions should financing be explicitly considered when estimating the value of a property?

Question 10-9

What is meant by depreciation for the cost approach?

Question 10-10

When may a “terminal” cap rate be lower than a “going in” cap rate? When may it be higher?

Question 10-11

In general, what effect would a reduction in risk have on “going in” cap rates? What would this effect have if it

occurred at the same time as an unexpected increase in demand? What would be the effect on property values?

Question 10-12

What are some of the potential problems with using a “going in” capitalization rate that is obtained from previous

property sales transactions to value a property being offered for sale today?

Question 10-13

When estimating the reversion value in the year of sale, why is the terminal cap rate applied to NOI for the year

after the holding period?

Question 10-14

Is a cap rate the same as an IRR? Which is generally greater? Why?

Question 10-15

Discuss the differences between using (1) a terminal cap rate and (2) an appreciation rate in property value when

estimating revision values.

Solution to Problems – Chapter 10

Valuation of Income Properties: Appraisal and the Market for Capital

INTRODUCTION

The homework problems in this chapter provide practice in application of all three of the appraisal approaches. The required

solution procedure follows the examples in the text. However, the problems purposely do not indicate exactly which

approach to use. Students should learn to determine which approach is appropriate given the information available, which is,

of course, the way it works in practice.

Problem 10-1

Part (a)

(1) The goal is to find the present value of NOI from year 1-7 and

Problem 10-2

(a) The property value is $22,222,222

Solution:

Property Value = NOI Next Year / (Discount Rate – Growth Rate)

Problem 10-3

Office is the highest and best use of this site.

The analysis for the Baker Tract is as follows:

Problem 10-4

Step 1, Calculate the NOI for the Office Building

Solution:

Rents $6,000,000

PGI or EGI 6,000,000

0.50 = ( 15,000,000 – 10,000,000 ) / 10,000,000

(c) The Land Value would be $2,727,273

Solution:

-0.7273 = ( 2,727,273 – 10,000,000 ) / 10,000,000

1. Expected Return on the Investment could to increase to 12.7% from 12%

Solution:

0.0857 = 3,600,000 / 42,000,000

2. Expected growth (g) in NOI would increase from 0.03 to 0.0343

Solution:

0.0857 = 3,600,000 / 42,000,000

Expected Growth (g) = Expected Return (r) – Required Return (R)

3. Building Costs would have to decrease by $2,000,000, or by $6.67 per sq. ft. and the investor will earn 12%.

Solution:

4. Rents would have to increase from $6,000,000 to $6,300,000 or average rent per square foot from $20 to $21

and the investor would still earn 12%.

Solution:

Problem 10-5

(a) The present value of the property would be $588,235.

Problem 10-6

(a)The estimated value of this property is $1,172,457

Solution:

End of (a) (b) (c) (d) (e)

Year NOI PV at 11% REV PVREV at 11% Total PV

0.0816 = $100,000 / $1,224,809

(c) The difference between the cap rate in (b) and the .10 terminal cap rate is caused by the fact that as properties age and

Problem 10–7

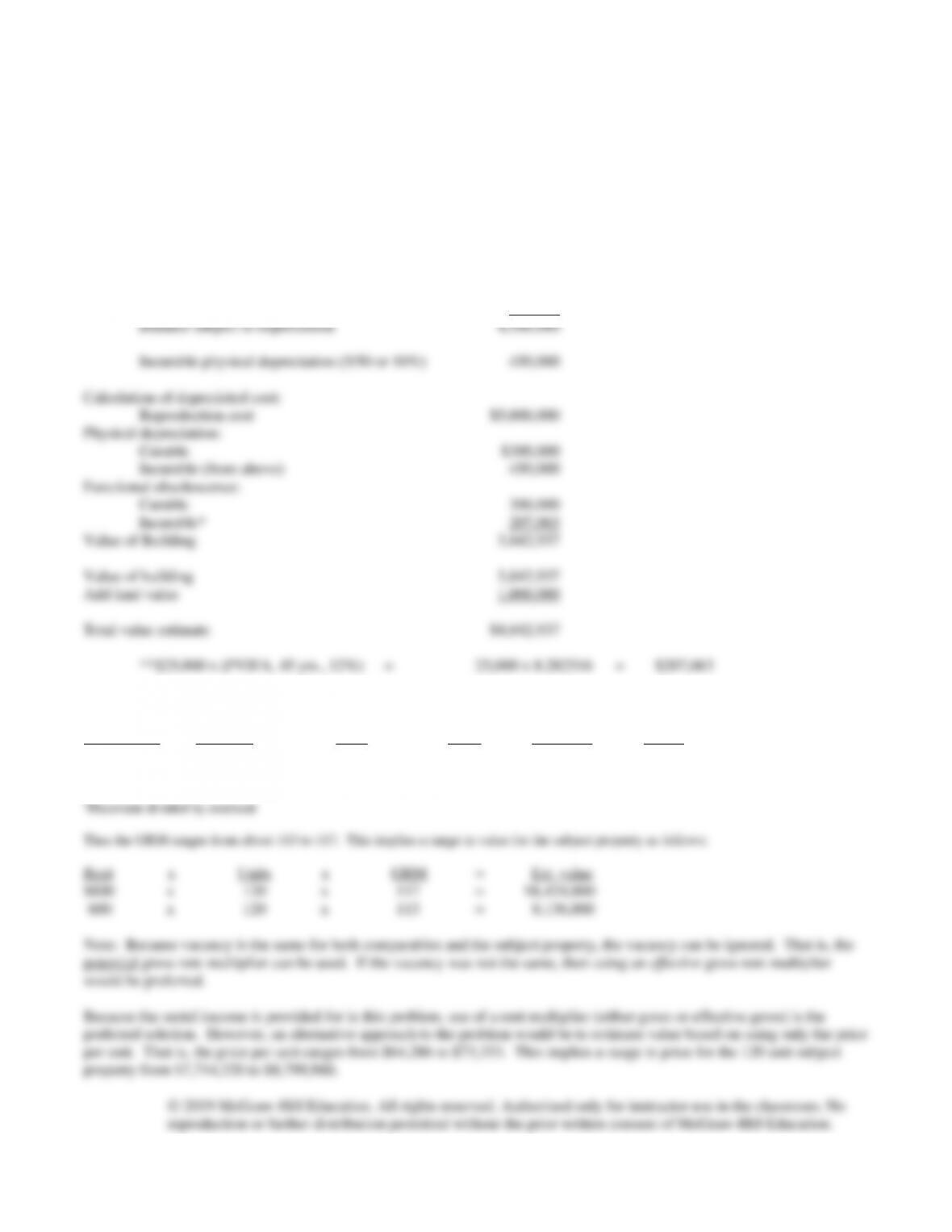

Calculation of incurable physical depreciation:

Reproduction cost $5,000,000

Less: curable physical depreciation 300,000

Less: curable functional obsolescence 200,000

Problem 10-8

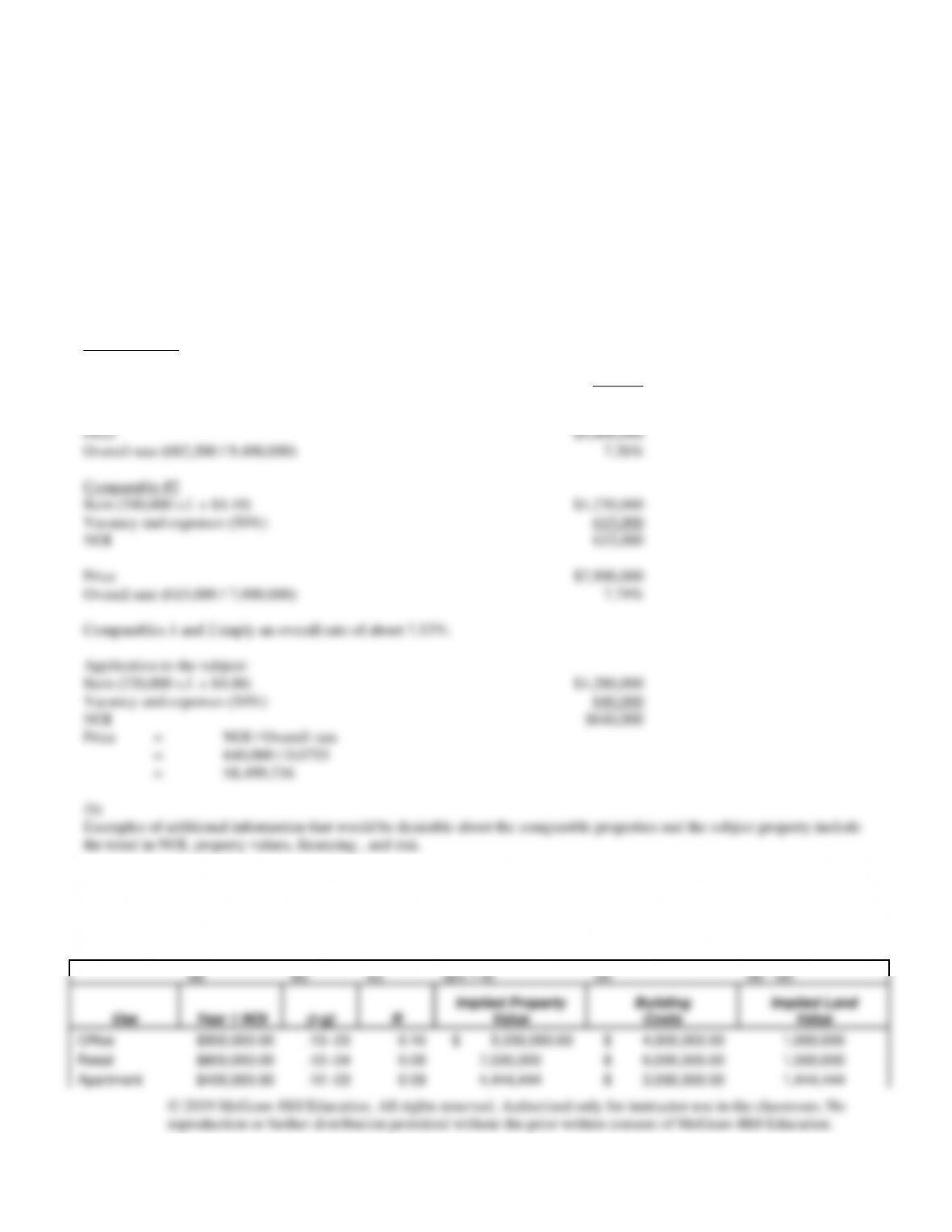

(a)

Comparable Rent/unit Price Units Price/unit GRM*

#1 $550 $9,000,000 140 $64,286 117

#2 650 6,600,000 90 73,333 113

Problem 10-9

(a) Loan payment (PMT) = NOI / DCR = $150,000 / 1.2 = $125,000

Loan amount (using a financial calculator):

PMT = $125,000; i = 10/12%, n = 20×12; FV = 0;

Solve for PV

Resale = 173,891 / .09 = $1,932,123

Loan balance = 969,348

Problem 10-10

(a)

Comparable #1

Rent (350,000 s.f. x $3.90) $1,365,000

Vacancy and expenses (50%) 682,500

NOI $682,500

Problem 10-11

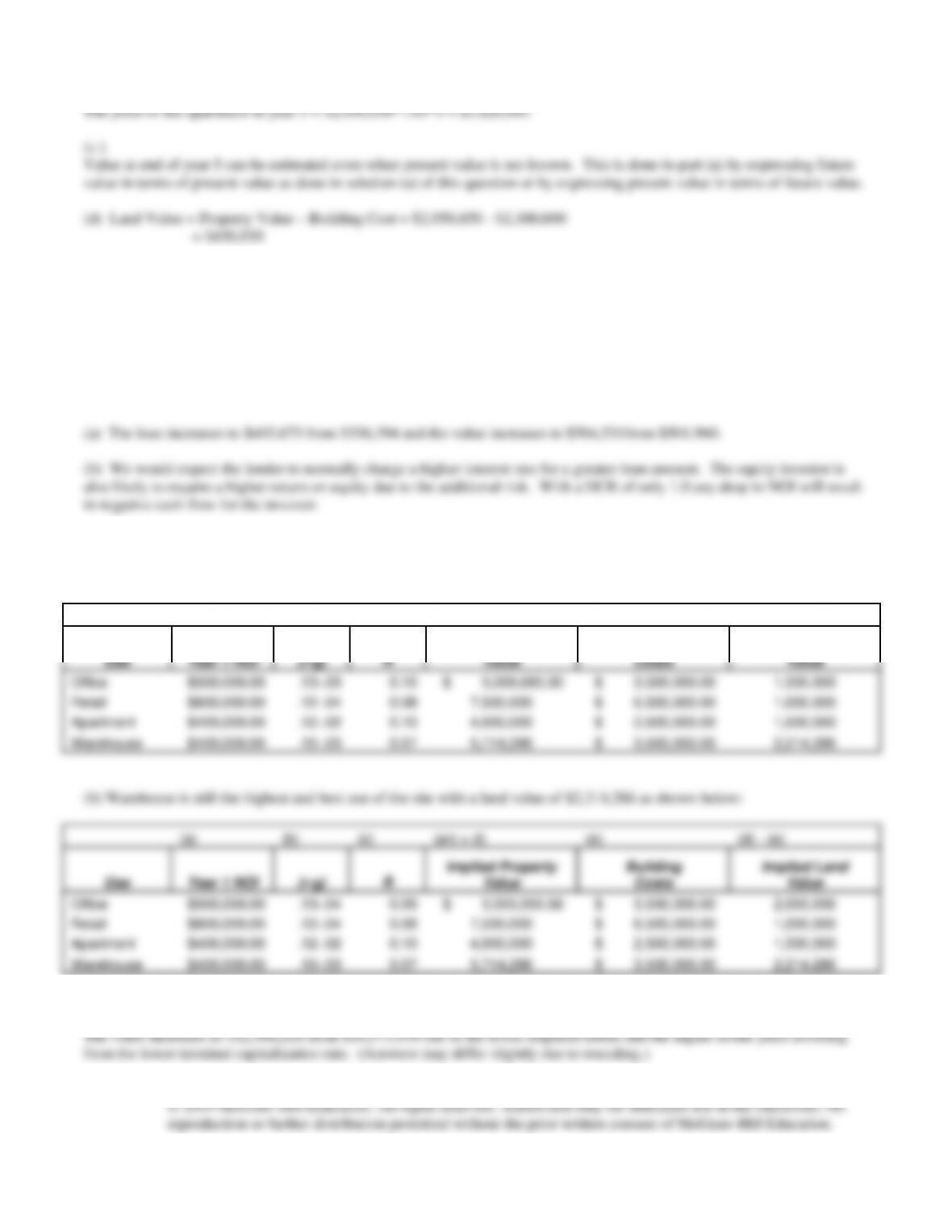

Refer to table below, the highest land value is now $1,714,286 with a highest and best use of warehouse. The higher growth

rate for warehouse was enough to change the highest and best use.

(a)

(b)

(c)

(a/c = d)

(e)

(d) – (e)

Implied Property

Value

Building

Costs

Implied Land

Value

Use

Year 1 NOI

(r-g)

R

Office

$500,000.00

.13-.03

0.10

$ 5,000,000.00

$ 4,000,000.00

1,000,000

Retail

$600,000.00

.12-.04

0.08

7,500,000

$ 6,000,000.00

1,500,000

Apartment

$400,000.00

.12-.03

0.09

4,444,444

$ 3,000,000.00

1,444,444

Warehouse

$400,000.00

.10-.03

0.07

5,714,286

$ 4,000,000.00

1,714,286

Problem 10-12

(a)

Rose garden has a better quality and location then other comparables. It offers all the amenities offered by other apartments

and has more parking space. In sum, Rose garden should have lower going-in cap rate then all other comparables.

Problem 10-13

(a)

The price of the apartment can be calculated by solving the following equation

PV= 200,000/(1.1)^1 +210,000/(1.1)^2+ 220,000/(1.1)^3+ 230,000/(1.1)^4+ 240,000/(1.1)^5+ PV*1.03^5 /(1.1)^5

This produces:

(b)

Problem 10-14

Problem 10-15

(a) Warehouse is now the highest and best use with a land value of $2,214,286 as shown below:

(a)

(b)

(c)

(a/c = d)

(e)

(d) – (e)

Implied Property

Value

Building

Costs

Implied Land

Value

Use

Year 1 NOI

(r-g)

R

Office

$500,000.00

.13-.03

0.10

$ 5,000,000.00

$ 3,500,000.00

1,500,000

Retail

$600,000.00

.12-.04

0.08

7,500,000

$ 6,500,000.00

1,000,000

Apartment

$400,000.00

.12-.02

0.10

4,000,000

$ 2,500,000.00

1,500,000

Warehouse

$400,000.00

.10-.03

0.07

5,714,286

$ 3,500,000.00

2,214,286

(b) Warehouse is still the highest and best use of the site with a land value of $2,214,286 as shown below:

(a)

(b)

(c)

(a/c = d)

(e)

(d) – (e)

Implied Property

Value

Building

Costs

Implied Land

Value

Use

Year 1 NOI

(r-g)

R

Office

$500,000.00

.13-.04

0.09

$ 5,555,555.56

$ 3,500,000.00

2,055,556

Retail

$600,000.00

.12-.04

0.08

7,500,000

$ 6,500,000.00

1,000,000

Apartment

$400,000.00

.12-.02

0.10

4,000,000

$ 2,500,000.00

1,500,000

Warehouse

$400,000.00

.10-.03

0.07

5,714,286

$ 3,500,000.00

2,214,286

Problem 10-16