Structure of the Case

As the case begins, Dr. Richard Scheller, EVP of Research and Early Development at Genentech, is

preparing for a meeting with Roche executives. Roche completed its acquisition of Genentech in 2009,

counting on the biotechnology company to advance its efforts in personalized medicine. Both firms

had high hopes that Genentech’s antiangio-genesis agent, Avastin, would become a blockbuster treat-

ment for a variety of early- and late-stage cancers. Since then, a Phase III trial in early-stage colon can-

cer has failed and an advisory panel voted to revoke Avastin’s approval for the treatment of advanced

breast cancer. Consequently, Scheller finds himself under significant pressure to accelerate other Phase

III projects in order to bring more products to market. At the same time, he is afraid that reallocating too

many resources to late-stage drug development risks neglecting Genentech’s core capability in early

drug discovery.

development and marketing. The result was an explosion of biotech startups and double-digit growth

in biotech revenues. Pharmaceutical firms readily established strategic alliances or acquired their bio-

tech partners in order to bring their innovative capabilities and new-product pipelines in-house. Case

Exhibits2-9 provide rich material for students to conduct an in-depth industry analysis.

The next section presents the legendary founding and growth of Genentech, the creator of the bio-

as those related to Genentech’s strategic goals. Their “creativity and initiative” led to the development

of more than 100 projects across multiple therapeutic areas, as detailed in Case Exhibits 13 and 14.

Nevertheless, Genentech remains vulnerable in two main respects: an insufficient quantity of original

drugs in its pipeline and an overreliance on the cancer market for a majority of its revenues.

Genentech: After the Acquisition by Roche

TEACHING NOTE

MHE-FTR-014

1259420477

REV: JANuARy 6, 2012

Teaching Note — Genentech: After the Acquisition by Roche

The section entitled “Buyout by Roche” describes the development of the Roche-Genentech relation-

ship leading up to the 2009 acquisition (see Case Exhibit 18). Roche has decided to maintain Genentech

as a wholly owned subsidiary, which means that it will continue operations as an independent research

and development center within the Roche Group. Nevertheless, there have been considerable struc-

tural and leadership changes made in anticipation of scale benefits and operational synergies. It is also

cutting costs and improving health care effectiveness. Genentech is particularly concerned because

close to 70 percent of its sales come from patent-protected cancer drugs, which sell at a premium but

provide minimal benefit in terms of survival time. Meanwhile, Genentech is facing increased competi-

tion from established pharmaceutical companies, who view investments in biotechnology as a means

to offset stagnating sales of new chemical entities. Genentech is also in danger of self-cannibalization

The case concludes by describing the difficult balancing act faced by Scheller: how best to allocate

resources between basic research (exploration) and the development (exploitation) of existing thera-

pies. Research is the fuel that keeps the product pipeline full, but late-stage development translates

Genentech’s medical advances into useful therapeutics for patients. Finding the right trade-off is neces-

sary if Genentech is to gain a sustainable competitive advantage over its competition.

Suggested Questions

AnAlysis: Focus on internAl And externAl environment

1. Perform a VRIO analysis. What is Genentech’s competitive advantage, if any?

2. Apply a PESTEL analysis. What impact will changes in health care and biogenerics regulation

have on Genentech? Why?

3. Apply a five forces analysis. How would you describe Genentech’s competitive position?

4. Perform a SWOT analysis.

Teaching Note —Genentech: After the Acquisition by Roche

FormulAtion: Focus on Business, corporAte or GloBAl

strAteGy

5. What impact will the Roche buyout have on Genentech? Will it be possible for Roche to own

Genentech without destroying its ability to innovate?

implementAtion: Focus on recommendAtions And How to

execute tHem

6. What is the major dilemma that Mr. Scheller faces in the case? What should he do?

Suggested Answers

AnAlysis: Focus on internAl And externAl environment

1. Perform a VRIO analysis. What is Genentech’s competitive advantage, if any?

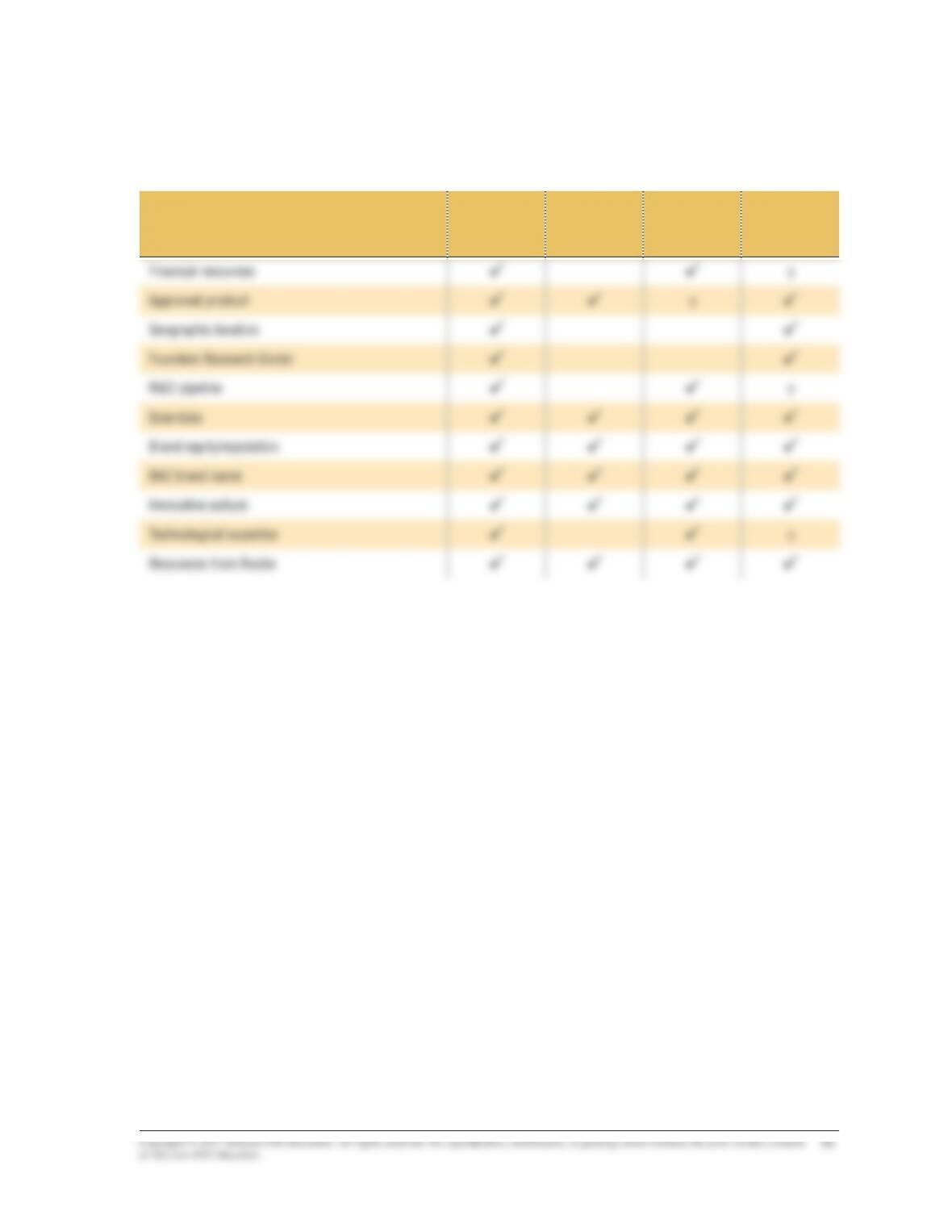

As in any knowledge-intensive industry, Genentech’s intangible resources and capabilities are more

important than its tangible assets when it comes to creating and sustaining a competitive advantage.

Certainly, Genentech has solid financial resources as a result of its approved product portfolio, but both

of these are a function of Genentech’s underlying technological expertise and its ability to leverage its

knowledge and reputation to create novel biotech therapies. Similarly, Genentech’s location in the San

2. Apply a PESTEL analysis. What impact will health care and biogenerics regulation have on

Genentech? Why?

This question is ideal for a PESTEL analysis, which will show that health care regulation is a critical

external (political/legal) force that can have great impact on biopharmaceutical companies, including

Genentech. Recent health care reform in the united States impacts the biopharmaceutical industry

in at least two ways. First, the Patient Protection and Affordable Care Act and the Health Care and

Teaching Note — Genentech: After the Acquisition by Roche

of McGraw-Hill Education.

estimated 16 percent of the population, or 47 million people. With the new law, more people in the

united States will have health insurance, which translates to broader coverage for insurance compa-

nies. This is good news for biopharmaceutical companies like Roche and Genentech since more people

will have insurance to pay for prescription drugs. What is not clear is how drug coverage rates might

change, as many of these people will be from lower income brackets.

Second, a key part of health care reform includes cost-saving measures. Government payers (such

as Medicare and Medicaid) will likely rely more on comparative effectiveness research (CER) to deter–

mine what drugs will receive coverage. As noted in the case, Genentech has had a recent spate of dis-

appointing results from CER studies, making its products likely targets to be removed from eligibility

for insurance coverage. This is especially true in light of the high prices of most cancer drugs ($25,000

have the same effect of limiting biotechnology companies’ period of market exclusivity.

Perhaps the next most important PESTEL sector is the sociocultural, as a result of demographic changes

in the world’s population. Roche’s 2010 Annual Report (page 16) describes the trends and resulting

impact as follows (emphasis added):

The world’s population continues to expand, and people are living longer on average. Greater life expectancy means

a rise in age-related diseases such as cancer, diabetes, rheumatoid arthritis, Parkinson’s and Alzheimer’s. This

is true not only of the industrialised world but increasingly of developing countries and emerging markets

third largest pharmaceutical market after the united States and Japan in 2010.

3. Apply a five forces analysis. How would you describe Genentech’s competitive position?

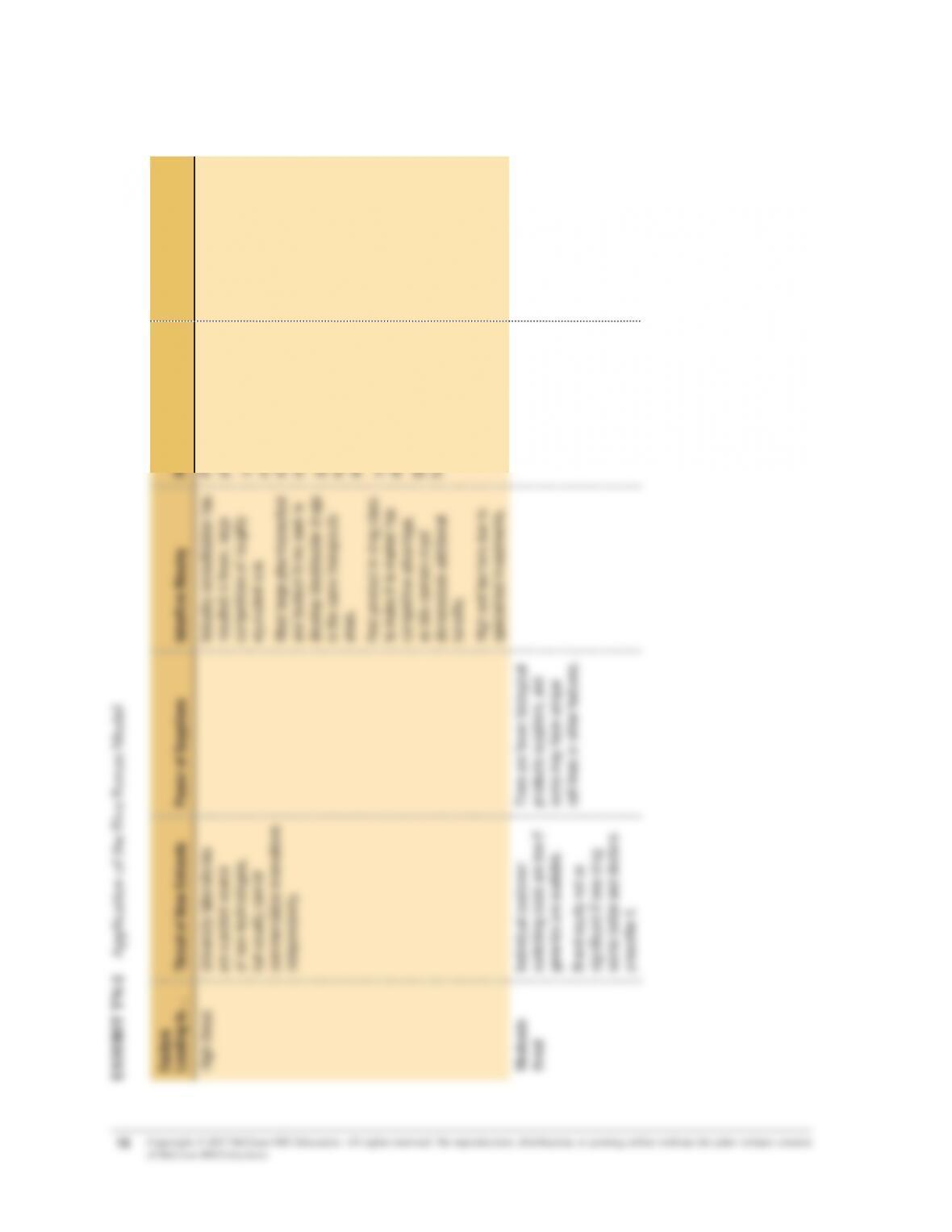

Applying the five forces model (see the Exhibit TN-2 at the end of this teaching note), we can see

that Genentech is in a relatively attractive industry with significant profit potential. Entry barriers to

the biopharmaceutical industry are high because it takes years for any new entrant to build a core

Teaching Note —Genentech: After the Acquisition by Roche

The threat of substitutes is greater than the threat of entry. Generics are already a major threat to phar–

maceuticals, and are an emerging threat to biotechnology products with the approval of the Biologics

Rivalry tends to be high, as most large drug companies compete in the same therapeutic areas,

seeking to develop the next blockbuster medication for the major diseases/disorders that affect the

population of the developed world. In other words, they go after the (same) largest markets in terms

of size and profitability. For example, Avastin’s competitor drugs include Erbitux by ImClone/Bristol-

The power of suppliers is relatively low in this industry because there are many biochemical manu-

facturers available to choose from, switching costs are low, and suppliers pose a low threat of forward

integration. The drug manufacturing process and quality of inputs is highly regulated by the FDA,

4. Perform a SWOT analysis.

A SWOT analysis is a helpful tool for integrating the results from internal (VRIO) and external

(PESTEL and five forces) analysis.

strengths—Genentech’s core competency is its technological expertise in genetic engineering, which

enables it to innovate multiple novel therapeutic agents. Its strong commitment to basic research has

been a powerful engine that has propelled the company forward, making it one of the few profitable

Teaching Note — Genentech: After the Acquisition by Roche

of McGraw-Hill Education.

Genentech’s top four selling products (Avastin, Rituxan, Herceptin, and Lucentis) have achieved

constant growth. Meanwhile, the company has been actively pursuing new indications of existing

products, as well as identifying new molecular entities in order to move them into development. As a

result of Genentech’s strong brand equity in the North American market, Roche has decided to place

all of its u.S. commercial operations in pharmaceuticals under the Genentech name. under Roche’s

ownership, Genentech will benefit from the companies’ combined u.S. sales organizations to maintain

strong performance in its specialty areas.

weaknesses—Paradoxically, Genentech’s dependence on the oncology market is also one of the com-

pany’s biggest weaknesses (close to 70 percent of Genentech’s 2008 sales came from cancer drugs).

Growing governmental concern over health care expenses has led to more careful scrutiny of the cost/

benefit ratio of high-priced cancer treatments. With several therapies showing minimal survival ben-

is mid-2012. Genentech does have a few more new products in Phases I and II of development; how-

ever, it will be years before Genentech can reap financial benefits from its research efforts. (Postscript:

Genentech did not get another drug approved until Actemra [toclizumab], a treatment for rheumatoid

arthritis, in 2010).

opportunities—Genentech currently has the leading position in the u.S. oncology drug market,

which is expected to grow quickly. According to MarketResearch, cancer is the second-leading cause

of death in the united States. The world market for cancer therapeutics is growing at a brisk double-

digit pace, with revenues surpassing $40 billion in 2010. This increased demand for oncology drugs is

threats—Recent health care reform will likely place an increasing emphasis on comparative effec-

tiveness research as a means of reducing health care expenses. This could pose a serious threat to

Genentech, which is highly dependent on the expensive (and lucrative) oncology market. If studies

continue to demonstrate that Genentech’s oncology products confer minimal survival benefits, the

products are likely to lose insurance coverage, forcing Genentech to lower its prices.

Teaching Note —Genentech: After the Acquisition by Roche

7

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction, distribution, or posting online without the prior written consent

of McGraw-Hill Education.

Generic drug competition has been a serious problem for many large pharmaceutical companies,

but was not an issue for biotechnology firms until the passage of the Biologics Price Competition and

Innovation Act in 2010. While the FDA has yet to develop a full implementation plan, the new legis-

lation allows for an abbreviated approval pathway for biosimilars. unlike pharmaceutical generics

(which must only demonstrate “pharmaceutical equivalence” to the patented compound), biogeneric

sponsors will be required to provide data from analytical, animal, and clinical studies, significantly

increasing the time and expense of getting a biosimilar approved. Nevertheless, the future prospect of

biogenerics is a serious threat looming on Genentech’s horizon.

FormulAtion: Focus on Business, corporAte or GloBAl

strAteGy

5. What impact will the Roche buyout have on Genentech? Will it be possible for Roche to own

Genentech without destroying its ability to innovate?

Evidence suggests that Roche had long been planning to buy the remaining shares of Genentech,

and that the equity alliance was merely a precursor to an eventual acquisition. By developing an early

relationship with Genentech, Roche preempted competitors and also reserved the future option of

unfortunately, empirical research indicates that most M&A deals turn out to be unsuccessful, and

ultimately destroy shareholder value, despite their high price tags. An important question for both

companies, therefore, is whether Roche will be able to avoid the M&A curse and realize the anticipated

synergies from this acquisition. Of course, the outcome of the Roche–Genentech integration depends

on multiple factors.

continuity between Genentech’s independent past and future as part of the Roche Group. He was

promoted to Executive Vice President of Research and Early Development, reporting directly to Roche

CEO, Severin Schwan.

Teaching Note — Genentech: After the Acquisition by Roche

A bigger concern in M&A deals is cultural collision, and Roche’s acquisition of Genentech is no excep-

tion. Themost profound impact will come from whether or not Roche’s seniorpharmaceutical man-

agement will support Genentech’s culture and nurture its continuation. Genentech’s academic and

innovative culture has been the dynamic engine that has propelled the company forward and kept

implementAtion: Focus on recommendAtions And How to

execute tHem

6. What is the major dilemma that Mr. Scheller faces in the case? What should he do?

The key problem Dr. Scheller faces is managing the trade-off between exploitation (defined as apply-

ing current knowledge to enhance firm performance in the short term) and exploration (defined as

searching for new knowledge that may enhance a firm’s long-term performance). Empirical studies

have shown that an ambidextrous organization—an organization that can balance exploitation with

and development in 2008, which was approximately 21 percent of its operating revenues, and signifi-

cantly more than the pharmaceutical industry average. Much of this was directed toward expanding

Genentech’s biotech capabilities into two new therapeutic areas—neuroscience and infectious diseases.

The challenge Dr. Scheller faces is to convince Roche’s senior leaders of the value of basic research and

gain their support for continued investment in Genentech’s exploratory activities. This will not be an

easy job, however. To Roche, “only an approved drug is a good drug.” Roche’s expectations for Avastin

Teaching Note —Genentech: After the Acquisition by Roche

9

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction, distribution, or posting online without the prior written consent

of McGraw-Hill Education.

breast cancer in the united States. Prior to these disappointments, Avastin was predicted to become the

world’s biggest-selling prescription medicine by 2014, and it is still Genentech and Roche’s top-selling

product. Roche is therefore eager to counteract criticisms that the drug is overpriced (at $50,000 per

patient per year) and shows minimal benefits in survival time. After all, Avastin targets cancer patients

who face high mortality risks. Any extension of their survival, even by days, is invaluable to them and

their loved ones.

Changes in Genentech’s organizational structure following the Roche takeover may also push

Genentech more toward exploitation and efficiency. Dr. Scheller fears these changes might alienate

Genentech’s legendary scientists, who have been asking if the acquisition marks “the end of Genentech

as we know it.” Somehow, Dr. Scheller needs to make a compelling case to Roche’s top management

and convince them that increasing resource allocations to scientific exploration is the most sustainable

route to achieving competitive advantage.

Recent Updates

2011 NDA activity. In August 2011, the FDA approved Zelboraf (vemurafenib) for the treatment of

BRAF V600E mutation-positive, inoperable or metastatic melanoma, along with the cobas 4800 BRAF

V600 Mutation Test used to determine patient eligibility for treatment with Zelboraf. The approval

provides proof-of-concept for Roche’s personalized approaches to medicine. Additionally, Genentech

submitted an NDA for vismodegib for the treatment of inoperable, basal cell carcinoma in November

2011. The application is undergoing priority review with an action date of March 8, 2012. For ongoing

updates, please visit Genentech’s press release archives at http://www.gene.com/gene/news/press-

releases/display.do?method=archive&year=2011.

Avastin approval revoked. The FDA issued a final ruling revoking Avastin’s approval for the treat-

Additional Resources

1. Additional information on the company is available at the corporate website at http://www.gene.

com/gene/index.jsp.

2. For an updated version of Genentech’s clinical development pipeline (Case Exhibit 13), please see

the following web page: http://www.gene.com/gene/gred/science/pipeline/.

3. Case Exhibit 16 is provided as an interactive timeline at http://www.gene.com/gene/products/

approvals-timeline.html. Click the product logos for more information on approved indications

and safety profiles.

4. Datamonitor 360 (a resource available through most academic libraries) published an updated

profile of the u.S. biotechnology industry in August 2011:

Teaching Note — Genentech: After the Acquisition by Roche

“Biotechnology in the united States,” datamonitor, Reference code: 0072-0695, August 2011. www.

datamonitor.com.

5. http://www.blinkx.com/watch-video/genentech-driven-by-science/aqp_F_ j4lx1ubdQfMsFBMQ

(17:35). Genentech: driven by science (June 12, 2007). A PharmaTV interview with Joseph McCracken,

Genentech’s VP of Business Development. McCracken describes the firm’s approach to scientific

discovery and alliance management, prior to the completion of the Roche acquisition.

6. http://www.pharmatelevision.com/Video/332-Genentech-Marc-Tessier-Lavigne.aspx (13:11).

Genentech: Becoming part of roche (October 13, 2009). A PharmaTV interview with Marc Tessier-

Lavigne, Chief Scientific Officer and Executive Vice President of Genentech after the Roche acqui-

sition. Tessier-Lavigne talks about Genentech’s position within the larger Roche organization and

how they have sought to protect Genentech’s unique scientific culture. Note: The first five minutes

are available for free, but a subscription is required to view the episode in its entirety.

Teaching Note —Genentech: After the Acquisition by Roche

ExHIbIT TN-1 A VRIO Analysis of Genetech

Genentech’s Resources and Capabilities

… are they?

Valuable

V

Rare

R

Costly to

Imitate

I

Organized to

capture value

O

Teaching Note — Genentech: After the Acquisition by Roche

of McGraw-Hill Education.

ExHIbIT TN-2 Application of the Five Forces Model

(continued)

Factors

Leading to… Threat of New Entrants Power of Suppliers Interfirm Rivalry Power of Buyers Threat of Substitutes

High threat University laboratories

are a potent source

of new technologies,

but usually cannot

commercialize innovations

independently.

Industry consolidation has

resulted in fewer, large

competitors of roughly

equivalent size.

Most large pharmaceutical

and biotech firms seek to

develop blockbuster drugs

in the same therapeutic

areas.

First product in drug class

to make it to market has

competitive advantage,

as late comers must

demonstrate additional

benefits.

High exit barriers due to

specialized investments.

Physicians decide what to

prescribe to patients.

Insurers and policy

makers decide which

drugs receive insurance

coverage.

Strong political pressure

to lower health care

expenses.

Increased comparative

effectiveness research.

Drug effectiveness trumps

brand loyalty.

Generics are major threat

for pharmaceuticals

and emerging threat for

biologics.

Biotech and

pharmaceutical products

may be substitutes for

one another.

Drugs may work for

more than one indication,

cannibalizing existing

products.

Moderate

threat

Individual customer

switching costs are low if

generics are available.

Brand equity not as

significant if new drug

works better and doctors

prescribe it.

There are fewer biological

products suppliers, and

some may have unique

cell lines or other features.

For some indications,

diet and exercise may be

viable alternatives.

Neutraceuticals may

be available for some

indications.

Teaching Note —Genentech: After the Acquisition by Roche

13

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction, distribution, or posting online without the prior written consent

of McGraw-Hill Education.

and money to develop

proprietary technology

through R&D.

High capital requirements

for manufacturing

facilities.

Building sophisticated

sales force requires

significant capital

investment.

Industry is highly

regulated by FDA.

Many biochemical

materials suppliers are

available.

Highly regulated industry,

so minimal opportunities

for differentiation.

Low switching costs for

large drug companies.

Many biotech companies

produce their own

biomolecules in-house.

Suppliers do not have

technology or knowledge

to forward integrate.

Demand for product is

increasing with aging of

baby boomers.

Emerging economies

are relatively untapped

markets.

Consolidation has lowered

intensity of rivalry in

developed markets.

Low threat of backward

integration.

Nature of threat

depends on comparative

effectiveness.

Teaching Note — Genentech: After the Acquisition by Roche

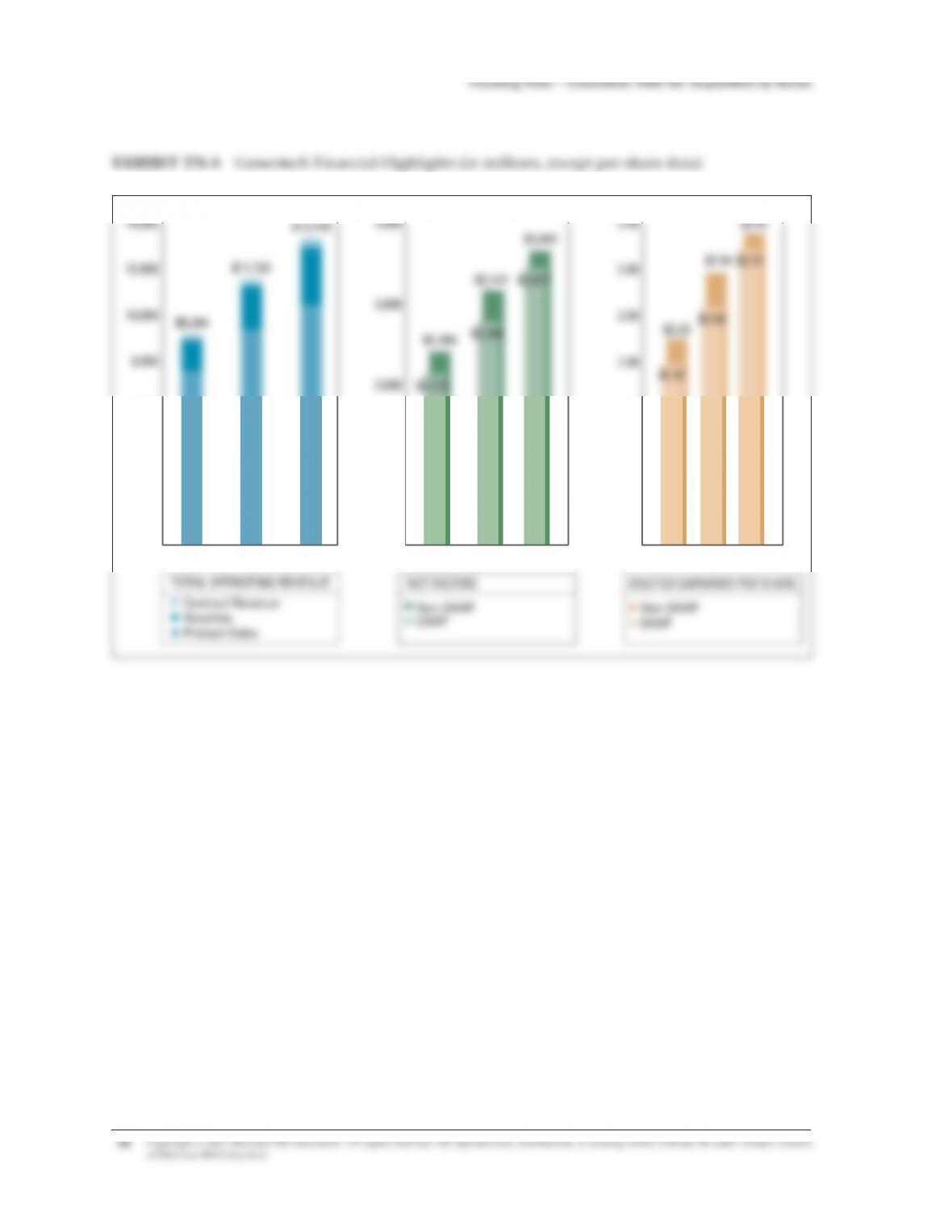

ExHIbIT TN-3 Genentech Financial Highlights (in millions, except per-share data)

20072006 2008

6,000

4,000

2,000

0

8,000

10,000

12,000

14,000

$9,284

$13,418

$11,724

20072006 2008

3,000

2,000

1,000

0

4,000

$2,113

$2,769

$3,427

$3,643

$3,142

$2,390

20072006 2008

1.50

1.00

0.50

0.00

2.00

2.50

3.00

3.50

$1.97

$2.59

$2.94

$3.42

$3.21

$2.23

TOTAL OPERATING REVENUE

Contract Revenue

Royalties

Product Sales

NET INCOME

Non-GAAP

GAAP

DILUTED EARNINGS PER SHARE

Non-GAAP

GAAP

Source: Genentech 2008 Annual Report, p. 13. See the 2008 Annual Report for more details.