Data Exploration

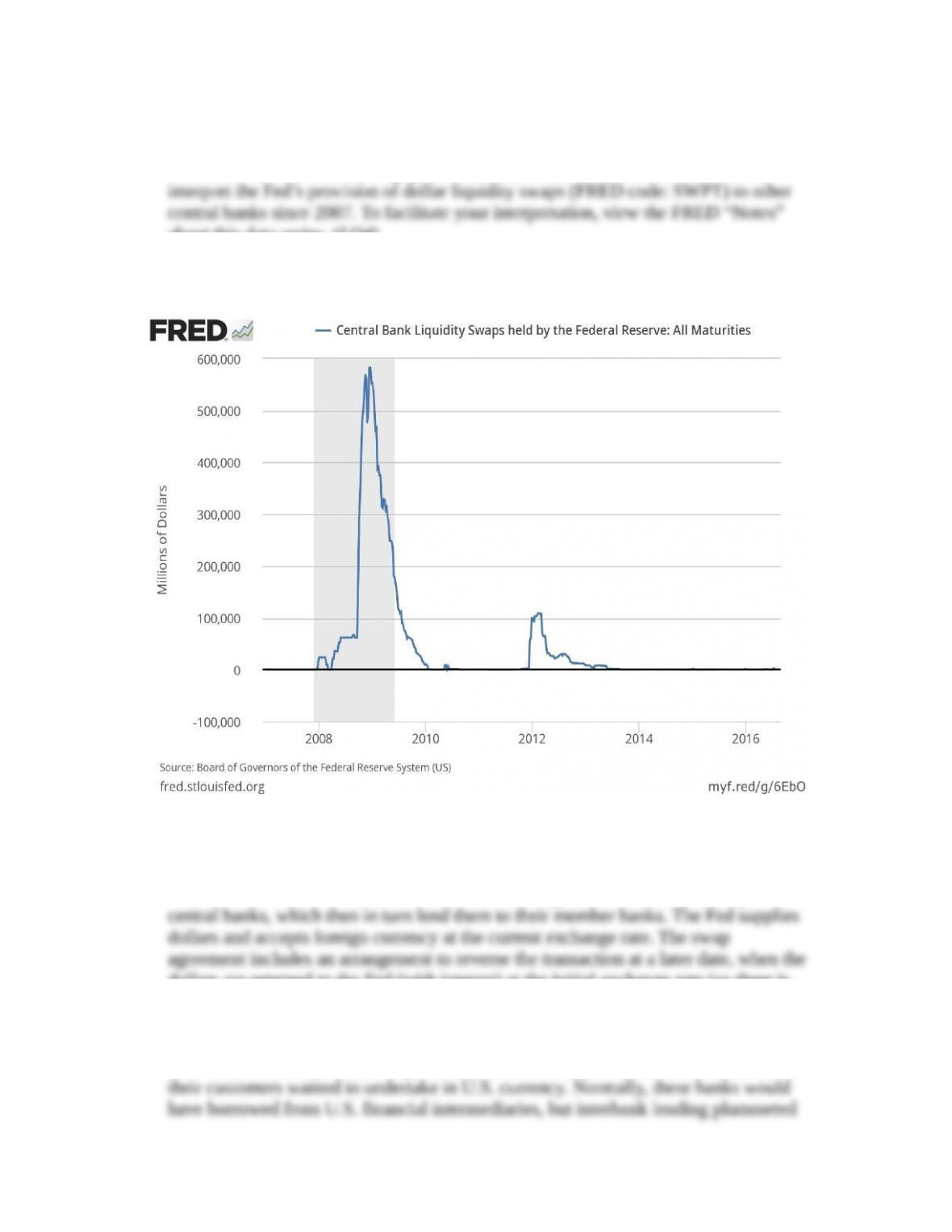

1. Central banks occasionally engage in “liquidity swaps” with each other. Plot and

about this data series. (LO4)

Answer: The data plot is:

These liquidity swaps occur when foreign banks need additional U.S. dollars to fund

their dollar-denominated activities. The Fed exchanges dollars with the foreign

dollars are returned to the Fed (with interest) at the initial exchange rate (so there is

no currency risk to the Fed).

The data plot shows that these swaps occurred first in the financial crisis of

2007-2009. In that period, foreign commercial banks needed dollars for transactions

central banks occurred in 2012 at an acute stage of the sovereign and banking crisis in

the euro area (see Chapter 16). In both cases, once the function of private markets

improved, central bank liquidity swaps virtually disappeared.

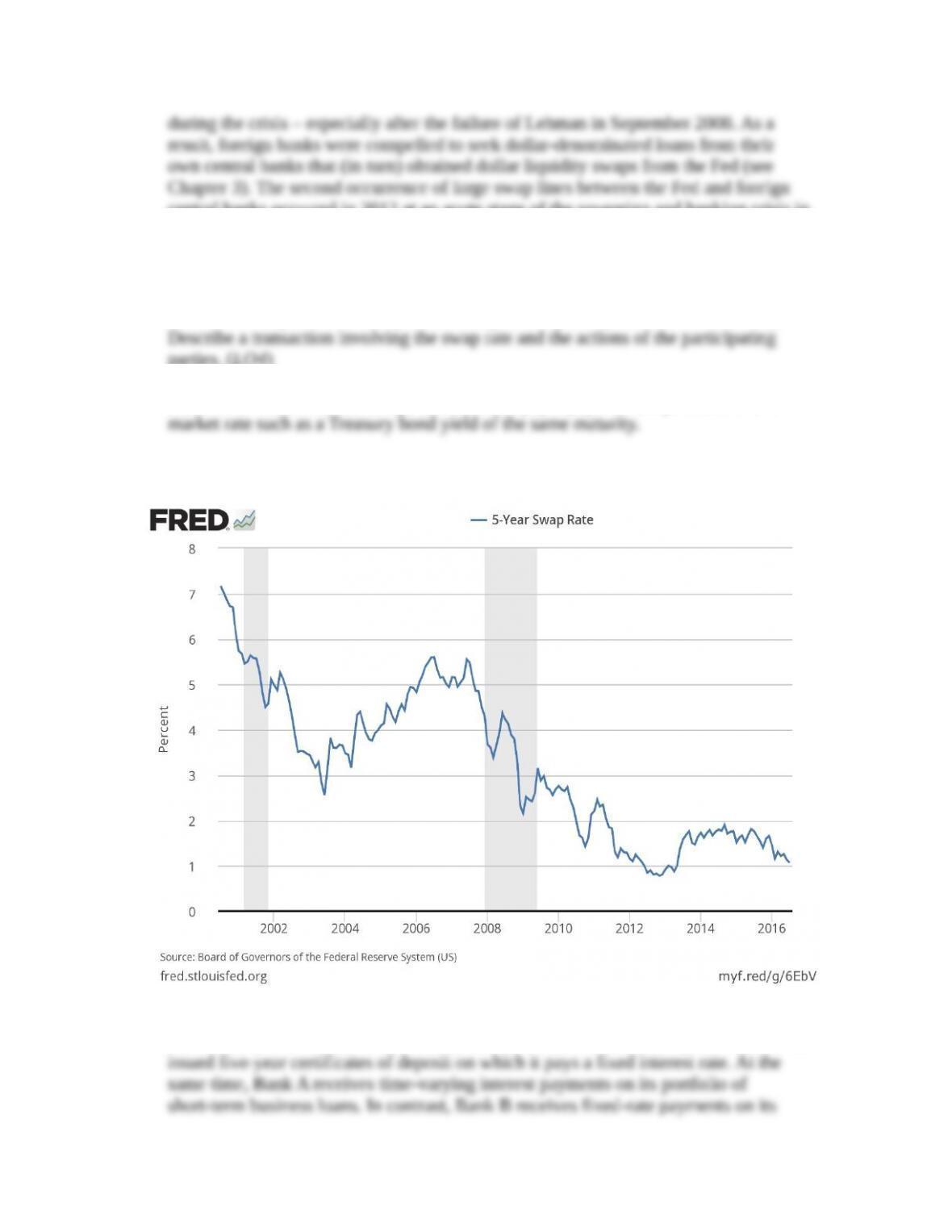

2. Define the swap rate and then plot the five-year swap rate (FRED code: MSWP5).

parties. (LO4)

Answer: In an interest rate swap, the fixed-rate payer pays the swap rate, tied to a

The data plot is:

As an example of an interest rate swap, consider a commercial bank (Bank A) that has

payment stream. Bank B will then have fixed income from its mortgages and fixed

expenses on the CDs, stabilizing profits. Bank A will have variable interest income

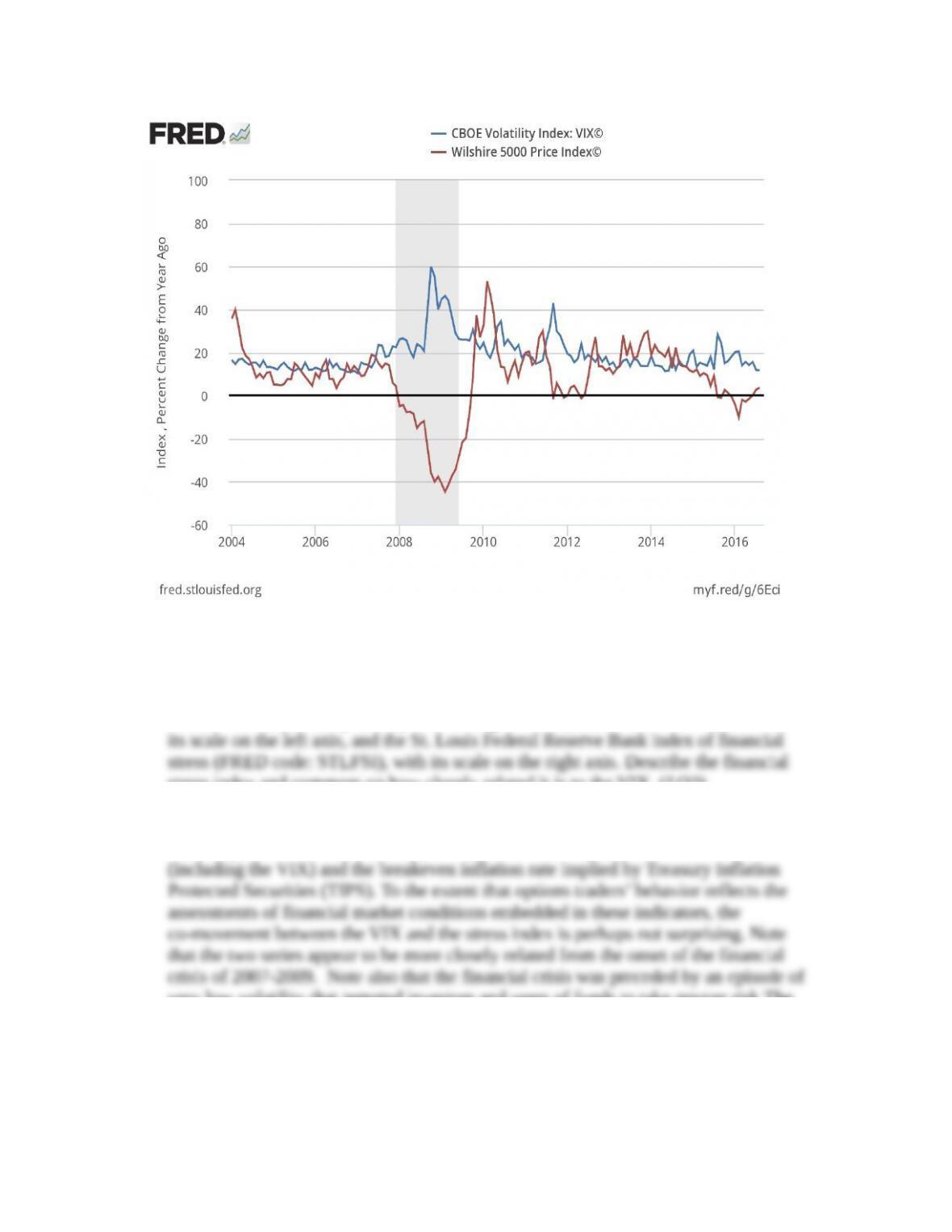

3. Risk-averse investors care greatly about asset price volatility. Using the FRED

and the percent change from a year ago of the Wilshire 5000 stock market index

(FRED code:WILL5000PR). Interpret the graph (LO3)

Answer: The VIX infers stock market participants’ collective expectation of stock

price volatility from options prices. Because the price of an option increases as the

related to the performance of the equity market index: expected volatility is low when

the stock market rises (and vice versa). The VIX spike in 2008 followed the collapse

of Lehman.

The data plot is:

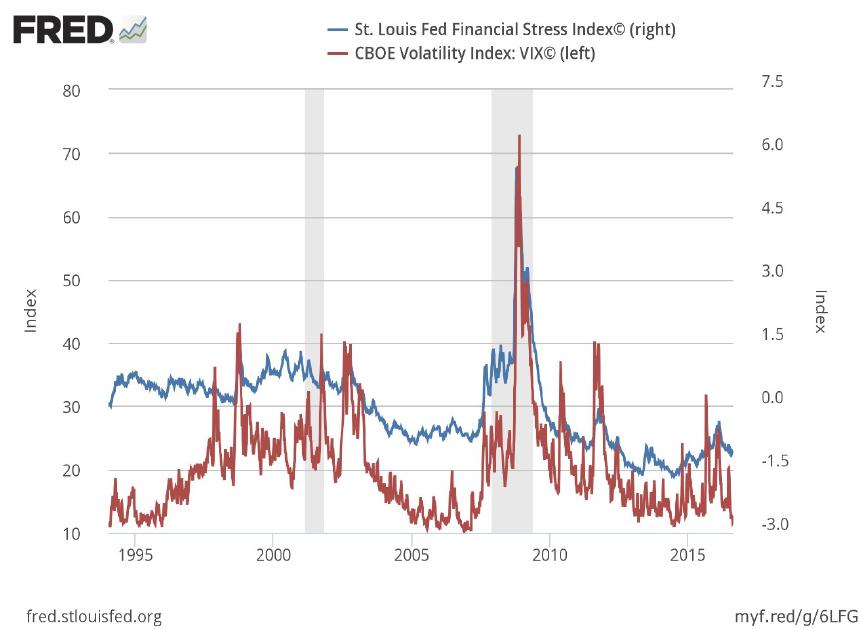

4. Is the VIX volatility index (FRED code: VIXCSL) an indicator of broader financial

market volatility? Using weekly data ending on Fridays, plot from 1994 the VIX, with

stress index and comment on how closely related it is to the VIX. (LO3)

Answer: The St. Louis Fed’s financial stress index is based on eighteen data series,

including seven interest rates, six yield spreads, volatility indexes of stocks and bonds

very low volatility that tempted investors and users of funds to take greater risk The

VIX has become a major focus of attention because it is, arguably, the single most

important (and timely) indicator of financial stress.

* indicates more difficult problems