1. The misrating of mortgage-backed securities by rating agencies contributed to the

financial crisis of 2007-2009. List some recommendations you would make to avoid

such mistakes in the future. (LO1)

Answer: In the run-up to the 2007-2009 crisis, the absence of data capturing a period

of falling house prices at a national level caused models to underestimate the default

accuracy of various bond rating firms in anticipating bond defaults also could

encourage more reliable ratings. Similarly, encouraging professional asset managers

can arise from payments by the bond issuers to the credit rating agencies in return for

having their bonds rated.

2. How do you think the abolition of investor protection laws would affect the risk

spread between corporate and government bonds? (LO1)

Answer: These laws were likely to be much more important in protecting purchasers

corporate and government bond yields.

3. You and a friend are reading The Wall Street Journal and notice that the Treasury

Assuming you are both believers in the liquidity premium theory, what might account

for your difference of opinion? (LO3, LO4)

Answer: The difference in opinion could reflect different views on the size of the risk

expectations that interest rates will rise and that the economy is expected to be

healthy.

4. Do you think the term spread was an effective predictor of the recession that started in

December 2007? Why or why not? (LO4)

Answer: An inverted yield curve (negative term spread) is often a sign that the

recession was not predicted by the yield curve.

5. *Given the data in the accompanying table, would you say that this economy is

heading for a boom or for a recession? Explain your choice. (LO4)

3-month

Treasury-bill

10-year

Treasury bond

Baa corporate

10-year bond

May 1.25% 4.5% 7.8%

Answer: The information in both the term structure and the risk structure point to a

that interest rates are expected to continue to rise in the future—a sign that the

economy is expected to do well.

The risk spread (the gap between the Treasury and corporate 10 year bonds) is

risk premium on corporate bonds.

6. Suppose recent regulatory reforms relating to credit rating agencies are perceived to

improve the reliability and accuracy of credit ratings of corporate bond issues.

Explain your answer. (LO1)

Answer: If, prior to the reforms, your bond issues enjoyed inflated credit ratings, you

are successful in bringing about more accurate ratings.

Core Principle 3 states that information is the basis for decisions. If, prior to the

issue new bonds at a reasonable price.

Data Exploration

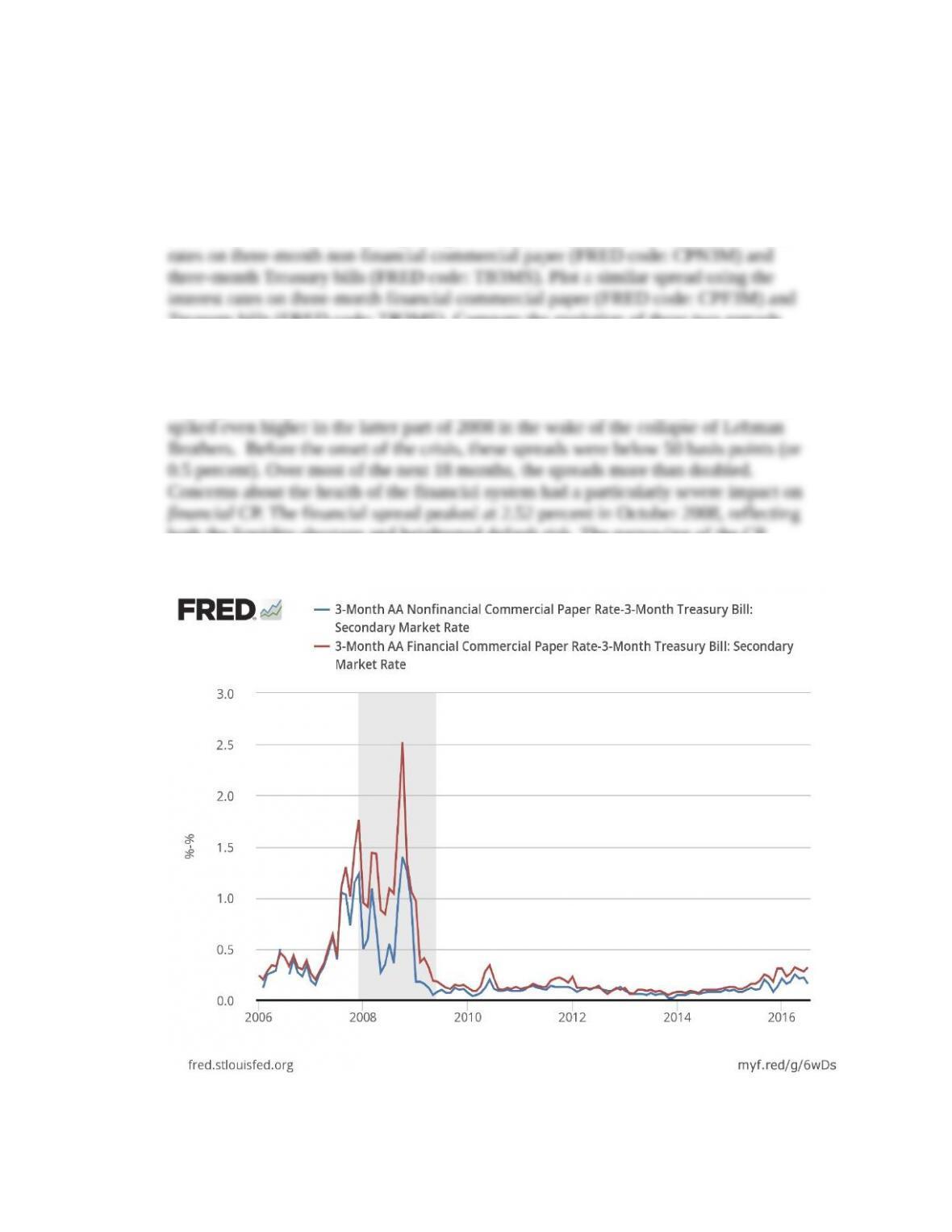

1. Did the financial crisis of 2007-2009 affect financial and nonfinancial firms to the

same extent? For the period beginning in 2006, plot the spread between the interest

Treasury bills (FRED code: TB3MS). Compare the evolution of these two spreads.

(LO1)

Answer: The spreads between commercial paper (CP) rates and the Treasury bill rate

rose significantly in the second half of 2007 as the financial crisis began to unfold and

both the liquidity shortage and heightened default risk. The narrowing of the CP

spreads in 2009 marked an important turning point in the crisis.

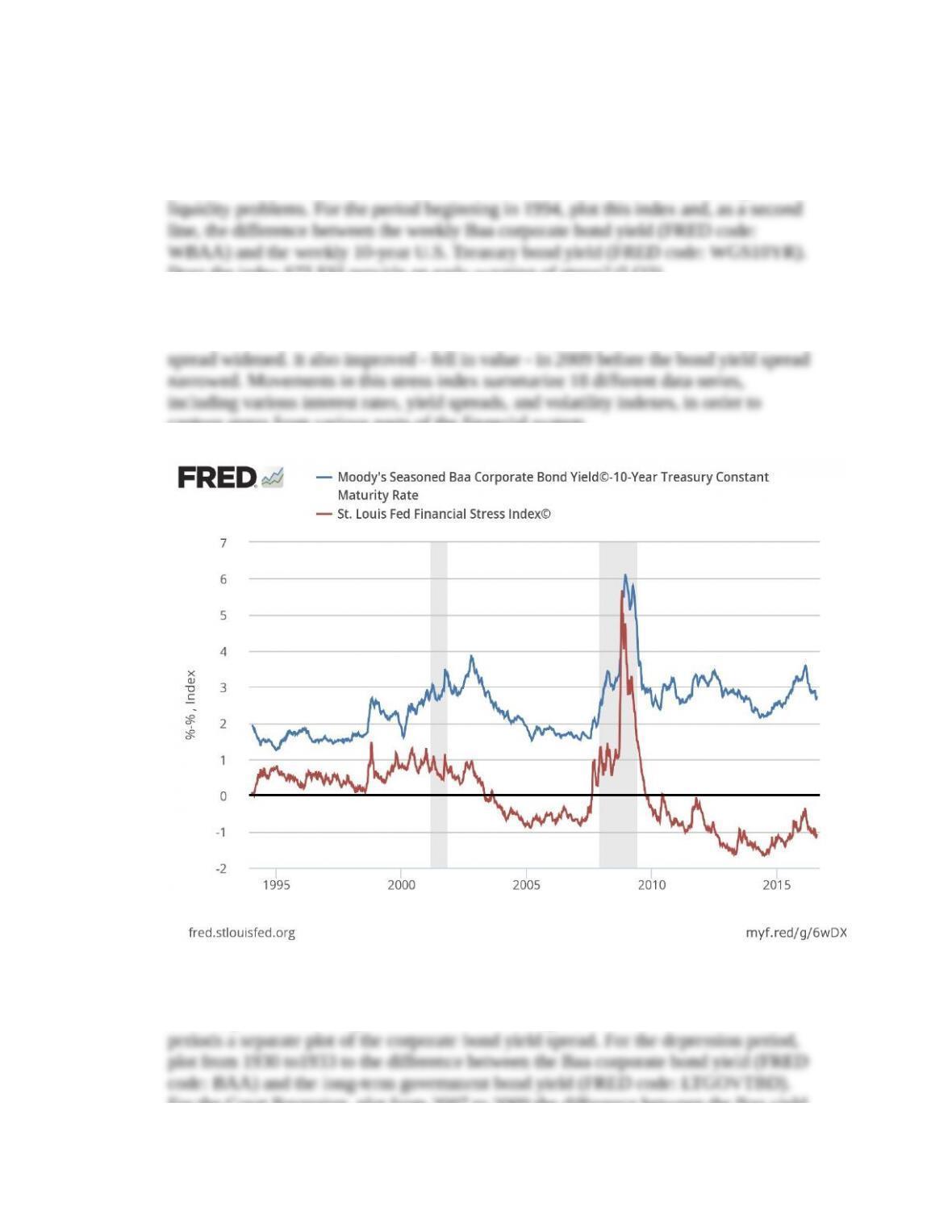

2. The Federal Reserve Bank of St. Louis publishes a weekly index of financial stress

(FRED code: STLFSI) that summarizes strains in financial markets, including

Does the index STLFSI provide an early warning of stress? (LO3)

Answer: The stress index deteriorated – rose in value – in 2007 before the bond yield

capture stress from various parts of the financial system.

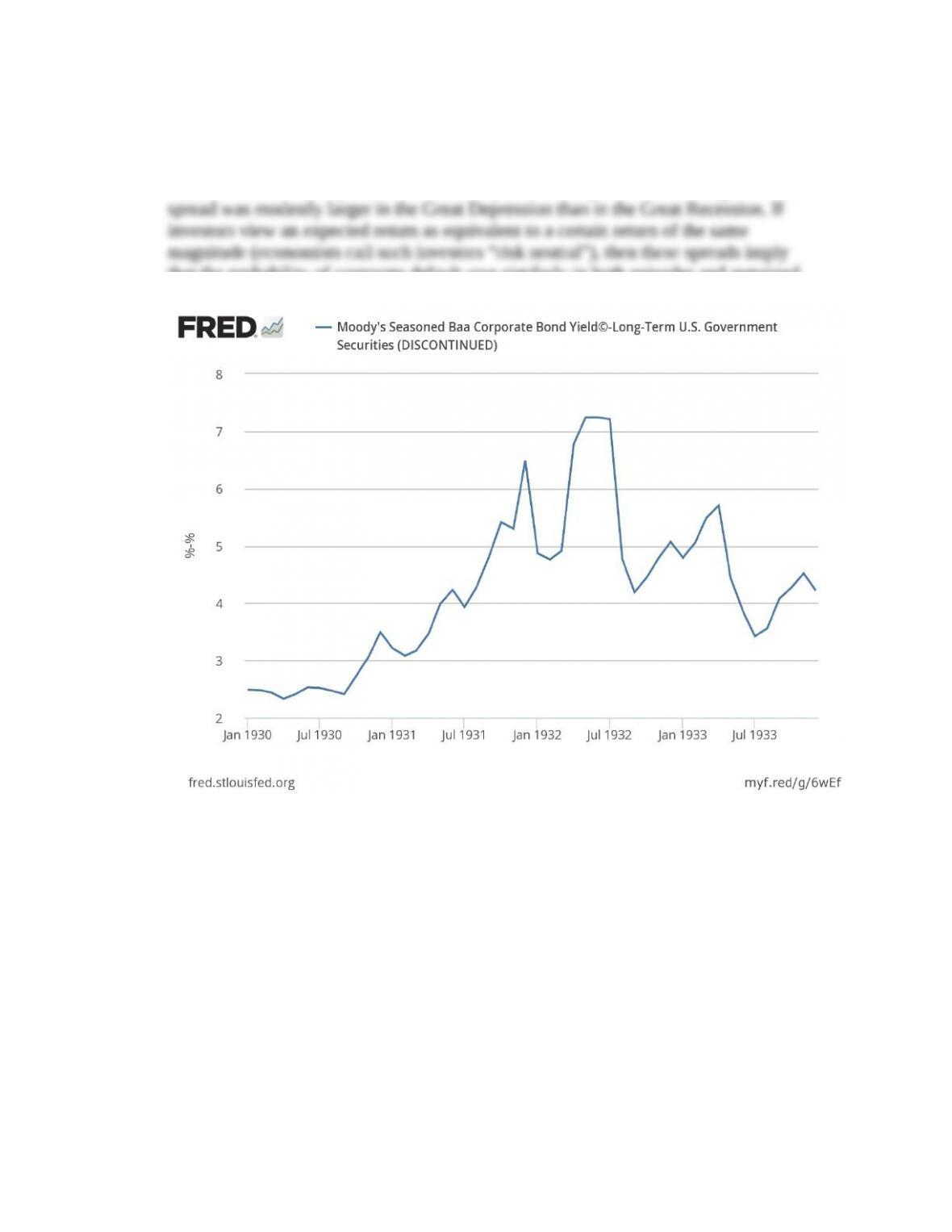

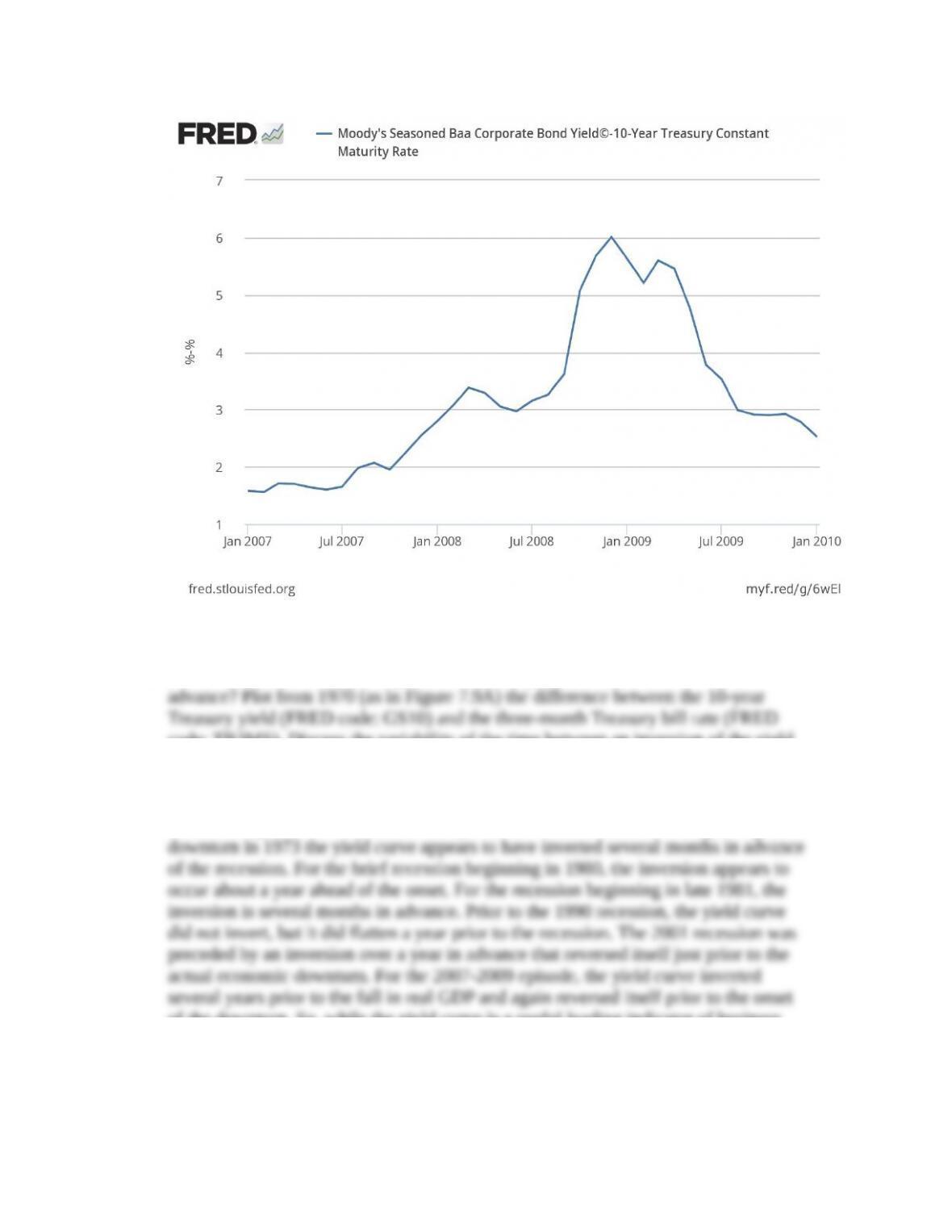

3. How did the Great Depression (1930-33) and the Great Recession of 2007-2009

affect expectations of corporate default? To investigate, construct for each of those

For the Great Recession, plot from 2007 to 2009 the difference between the Baa yield

(FRED code: Baa) and the 10-year Treasury bond yield (FRED code: GS10).

Compare the plots. (LO1)

Answer: The two data plots are below. The patterns are quite similar, though the risk

that the probability of corporate default rose similarly in both episodes and remained

above pre-crisis levels several years later.

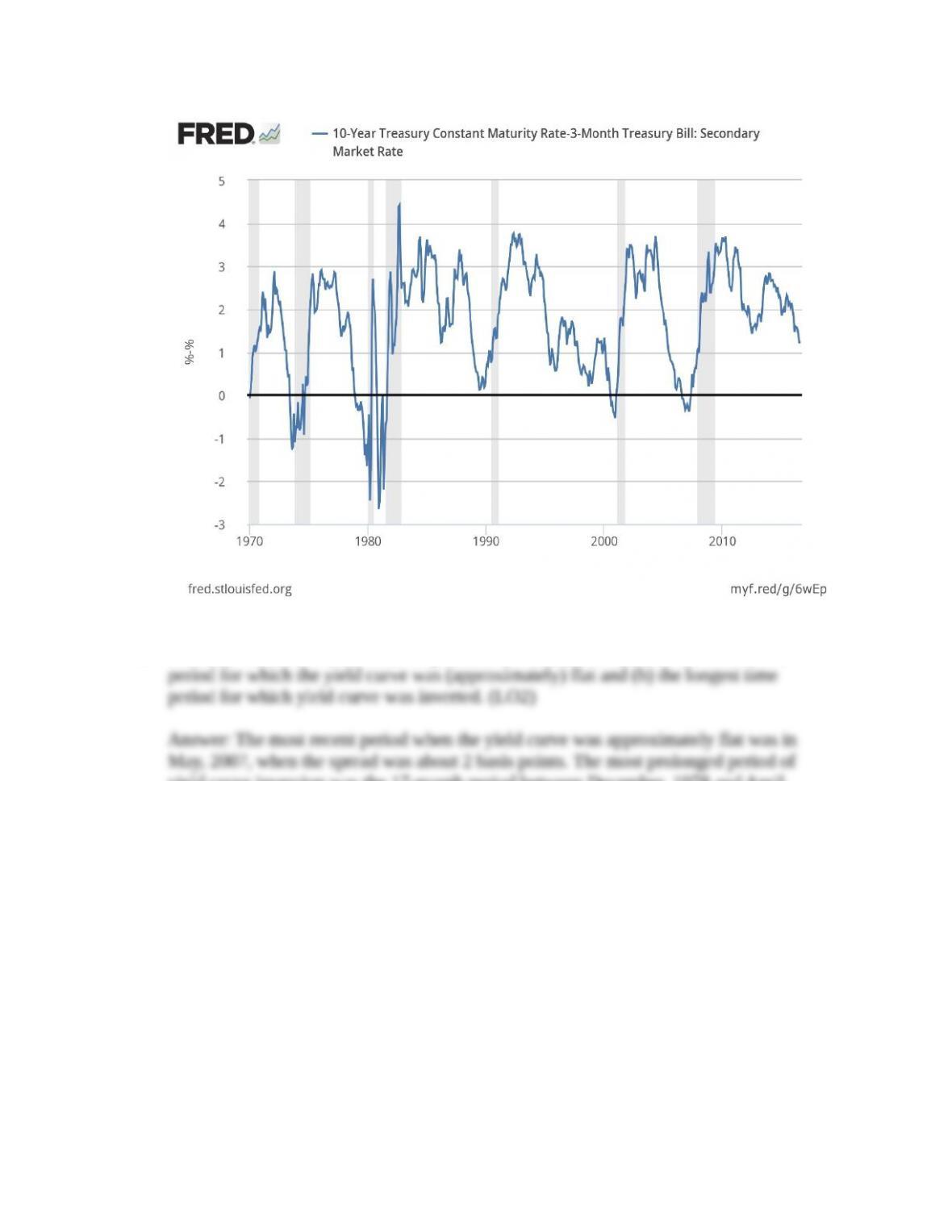

4. How reliably does an inverted yield curve anticipate a recession? How far in

code: TB3MS). Discuss the variability of the time between an inversion of the yield

curve and the subsequent recession. (LO3)

Answer: The data plot is below. The yield curve inverts when the term spread

becomes negative, so we examine the spread for values around zero. Regarding the

of the downturn. So, while the yield curve is a useful leading indicator of business

cycles, this variability in timing makes it an imperfect one.

5. Download the data used in Data Exploration Problem 4 and (a) find the most recent

yield curve inversion was the 17-month period between December, 1978 and April,

1980.

* indicates more difficult problems