3. *Monetary policymakers observe an increase in output in the economy and

believe it is a result of an increase in potential output. If they were correct, what

would the appropriate policy response be to maintain the existing inflation target?

If they were incorrect and the increase in output resulted simply from a positive

supply shock, what would the long-run impact be of their policy response? (LO3)

Answer: To maintain the existing inflation target, monetary policymakers should

shift their MPRC to the right, shifting the AD to the right. This would restore

If, however, the increase in output resulted simply from a positive supply shock,

the expansionary monetary policy would increase the expansionary gap. In the

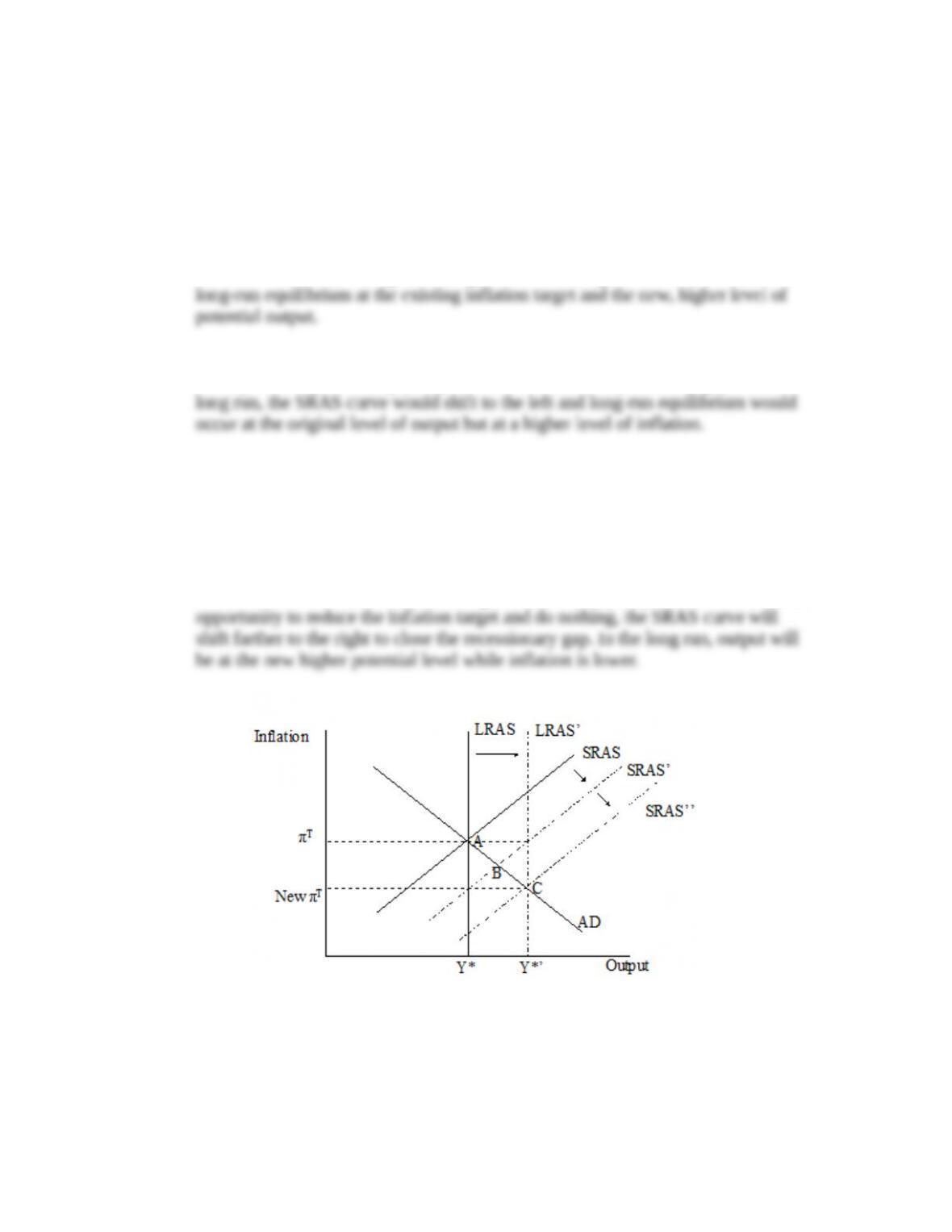

4. *Consider a previously closed economy that opens up to international trade. Use

the aggregate demand–aggregate supply framework to illustrate a situation where

this would lead to lower inflation in the long run. (LO2)

Answer: Opening up to international trade increases potential output and the

SRAS and LRAS curves shift to the right. If monetary policymakers use this as an

5. *How could you use the aggregate demand–aggregate supply (AD/AS)

framework to explain the impact of the financial crisis of 2007–2009 on inflation

and output in the economy? (LO2, LO3)

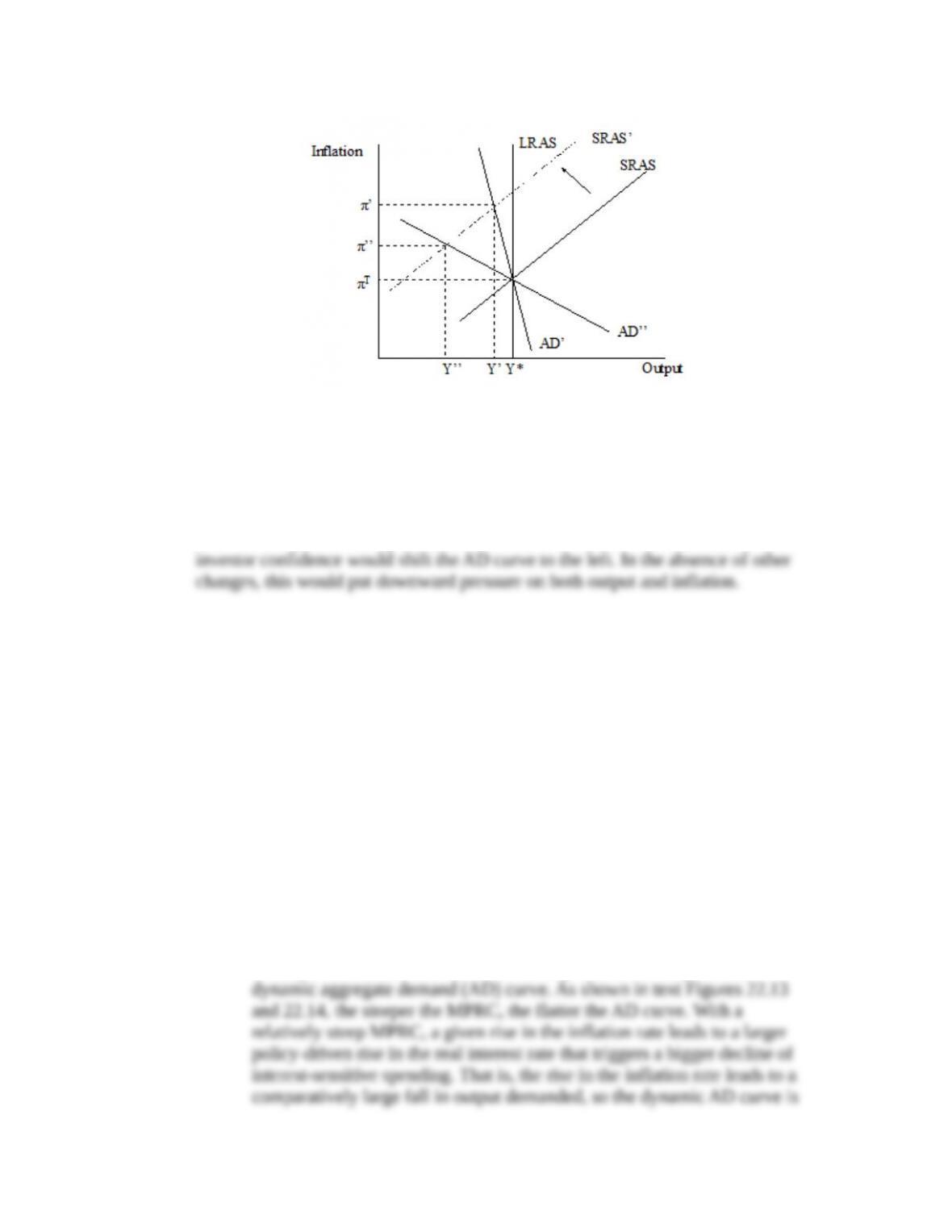

Answer: You can think of the disruption in financial markets as an AD shock.

Lack of access to credit by consumers and businesses and loss of consumer and

6. Changes in oil prices shift the short-run aggregate supply curve (SRAS). Consider

how volatility in oil prices may influence the economy’s short-run equilibrium,

which occurs at the intersection of the dynamic aggregate demand (AD) curve and

the SRAS curve. (LO3)

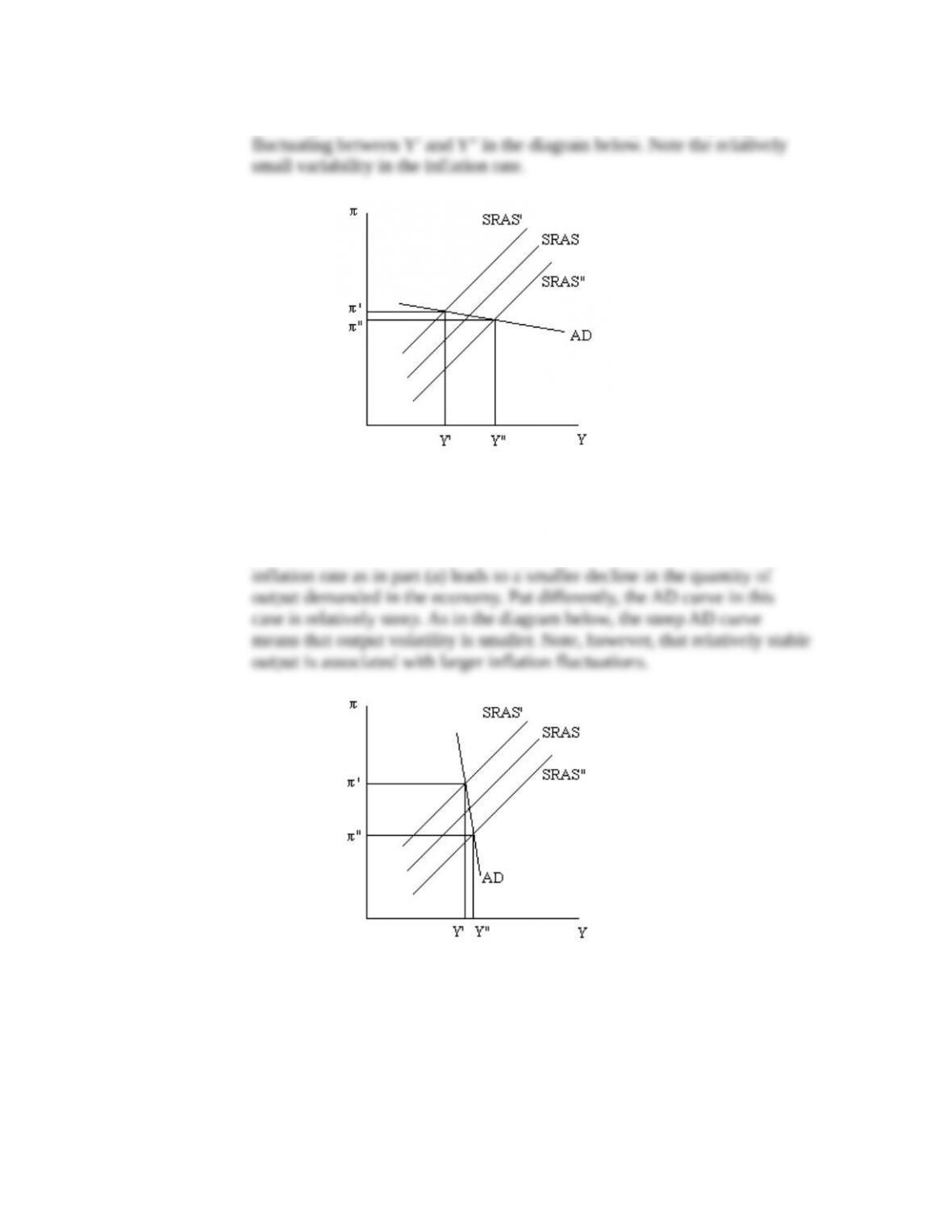

. Suppose the monetary policy reaction curve is relatively steep. What does

this imply about the slope of the AD curve? What does it imply about the

variability of output and inflation when the SRAS curve shifts? Explain.

. Suppose the monetary policy reaction curve is relatively flat. What does

this imply about the slope of the AD curve? What does it imply about the

variability of output and inflation when the SRAS curve shifts? Explain.

Answer:

a. In the diagram below, suppose that SRAS fluctuates between SRAS’ and

SRAS”, with a typical position at SRAS. The impact of these fluctuations

on output and inflation in the short run depends on the slope of the

relatively flat. With a flat AD, the variability in output is fairly large,

b. If the MPRC is relatively flat, a given rise in the inflation rate leads to a

smaller policy-driven increase in the real interest rate, resulting in a

smaller decline of interest-sensitive purchases. So, the same increase in the

7. You are asked to advise a central bank of an advanced economy that is about to

set an inflation target for the first time. Officials are leaning toward adopting a 2

percent target, in line with the practice in many other countries. Suggest two

factors that the central bank should consider before settling on 2 percent. (LO3)

Answer: You might suggest the central bank officials consider: 1) estimates of the

neutral real interest rate in their economy; and 2) the historical depths of

recessions in their economy. In a situation where the neutral real interest rate is

8. Suppose that a government imposes trade barriers that raise the domestic cost of

production and lower potential output. What would you expect to happen to

inflation and output in the short run and the long run, assuming monetary

policymakers only recognize the fall in potential output with a lag and keep their

inflation target unchanged? (LO1)

Answer: The fall in potential output would be reflected in a shift to the left of both

the SRAS and LRAS curves. In the short run, before policymakers realize that

potential output has fallen, inflation will rise and output will fall as the economy

In the long run, the overall impact of the protectionist policies would be to lower

9. High debt ratios led many countries in recent years to reduce government

spending. Suppose the cut in spending started from a point with the economy at

long-run equilibrium. How might monetary policymakers react, assuming their

inflation target remained unchanged? (LO1)

Answer: The cut in government spending shifts the AD curve to the left, reducing

inflation below expected inflation and below the inflation target and also lowering

output below potential output. Realizing that the long-run real interest rate had

Data Exploration

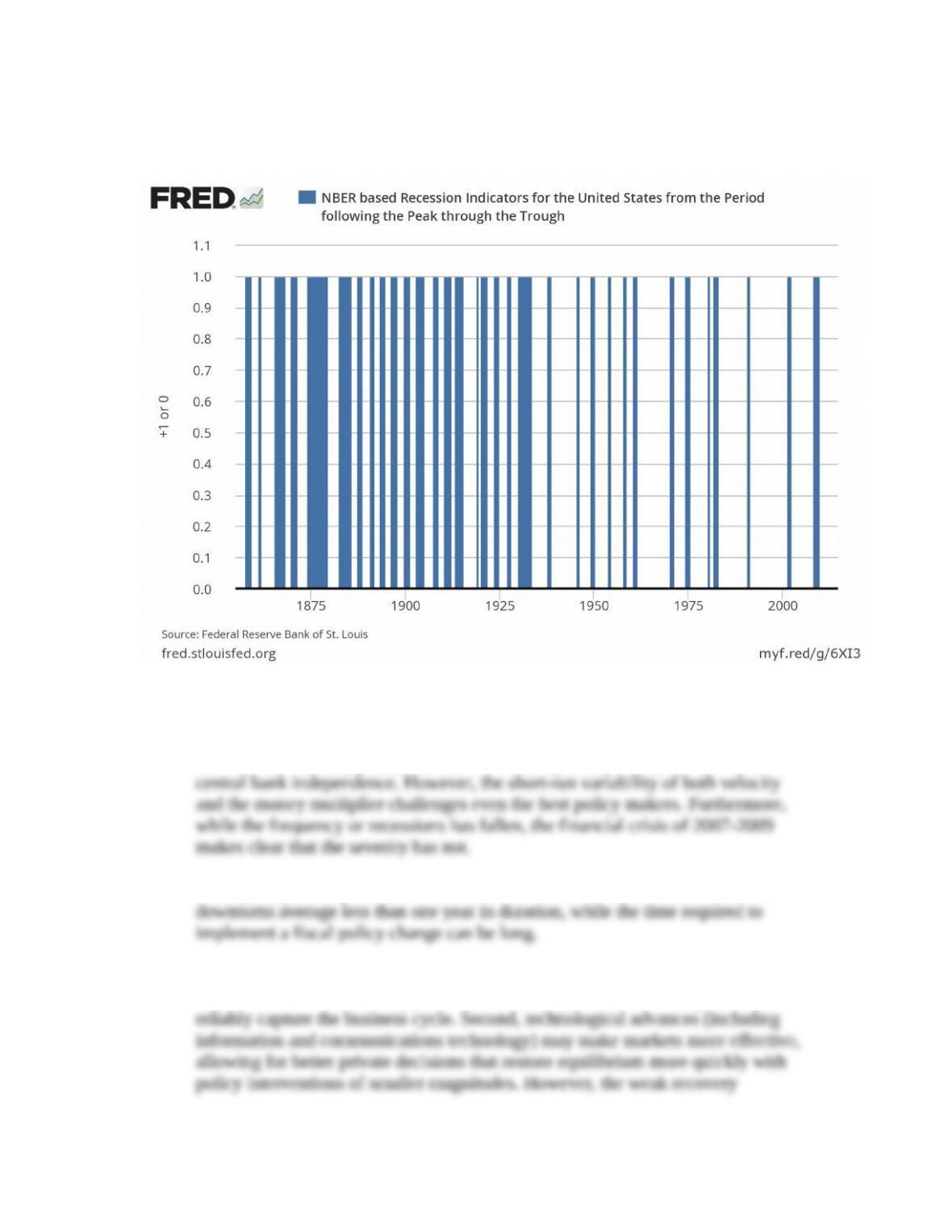

1. Display as a bar chart the periods since 1854 that are designated as U.S.

recessions by the National Bureau of Economic Research (FRED code: USREC).

Why has the frequency of recessions declined over time? Could improvements in

monetary policy have played a role? Improvements in fiscal policy? Can you

think of any other causes? (LO1)

Answer: The frequency of recessions has notably diminished, especially after the

Great Depression. Monetary policy has improved over time, especially with the

advent of a monetary policy framework stressing transparency, credibility and

Fiscal policy usually is more difficult to use to counter recessions because these

At least two other possibilities exist. First, one hypothesis is that the data prior to

World War II, and especially prior to World War I, is not sufficiently accurate to

following the 2007-2009 recovery highlights the limits of the economy’s

self-correcting forces.

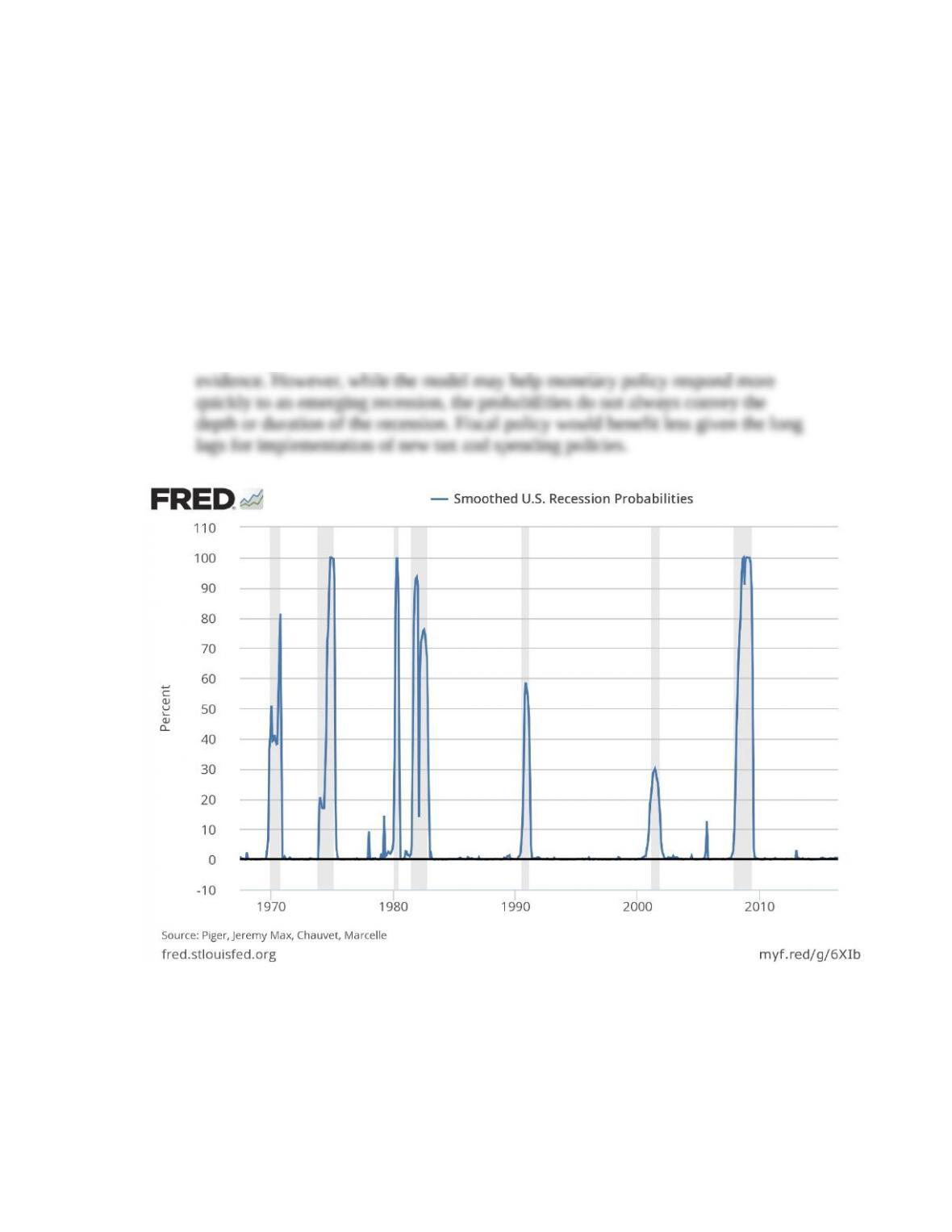

2. In the past, policymakers occasionally became aware of a recession only well

after it began. Can they do better? Plot the probability of a recession from a

statistical model (FRED code: RECPROUSM156N). To what extent could the

model help improve monetary or fiscal policy or both? (LO3)

Answer: The probabilities are plotted below. With the exception of the mild

downturn in 2001, a recession occurs whenever the statistical probability rises

above 50 percent. Furthermore, there are no “false signals” with the available

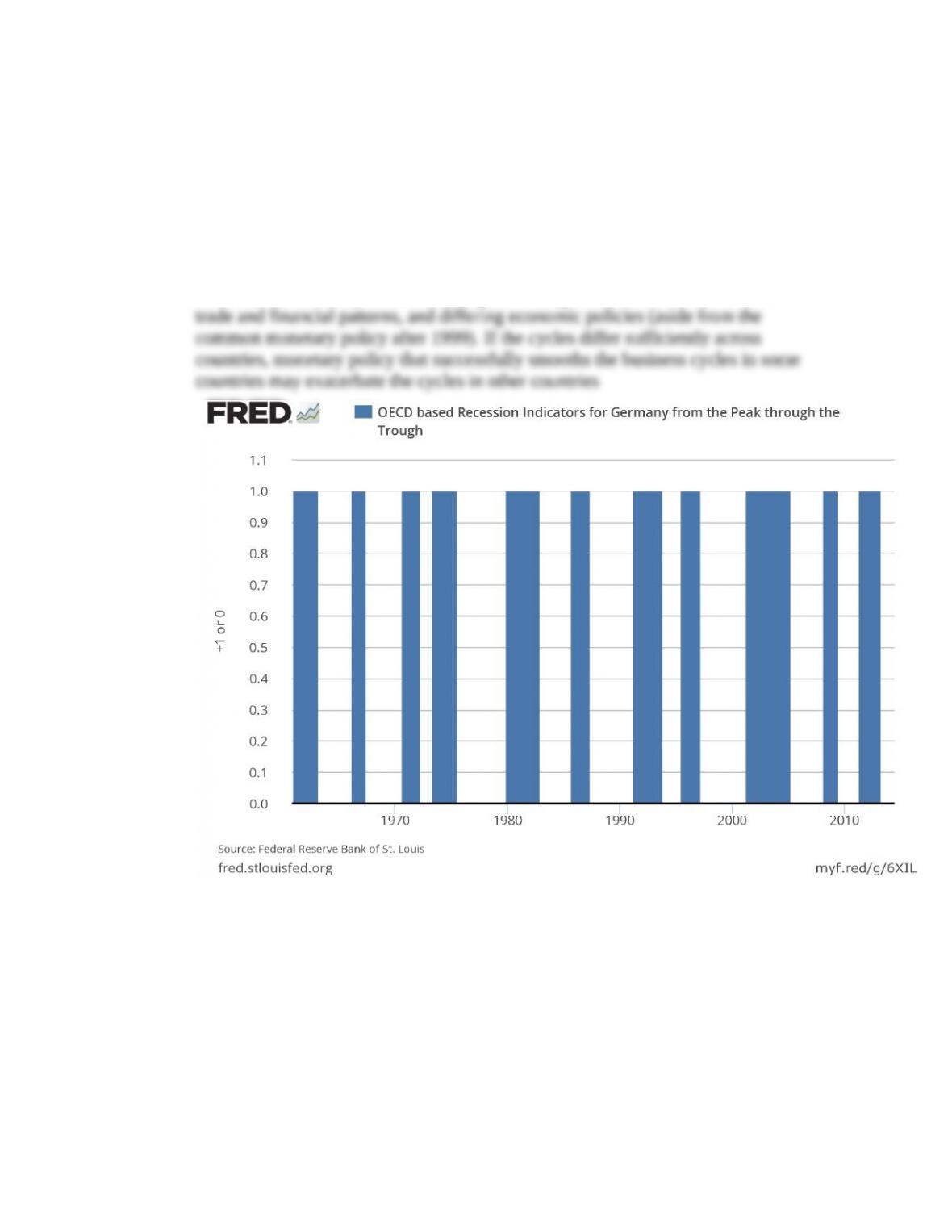

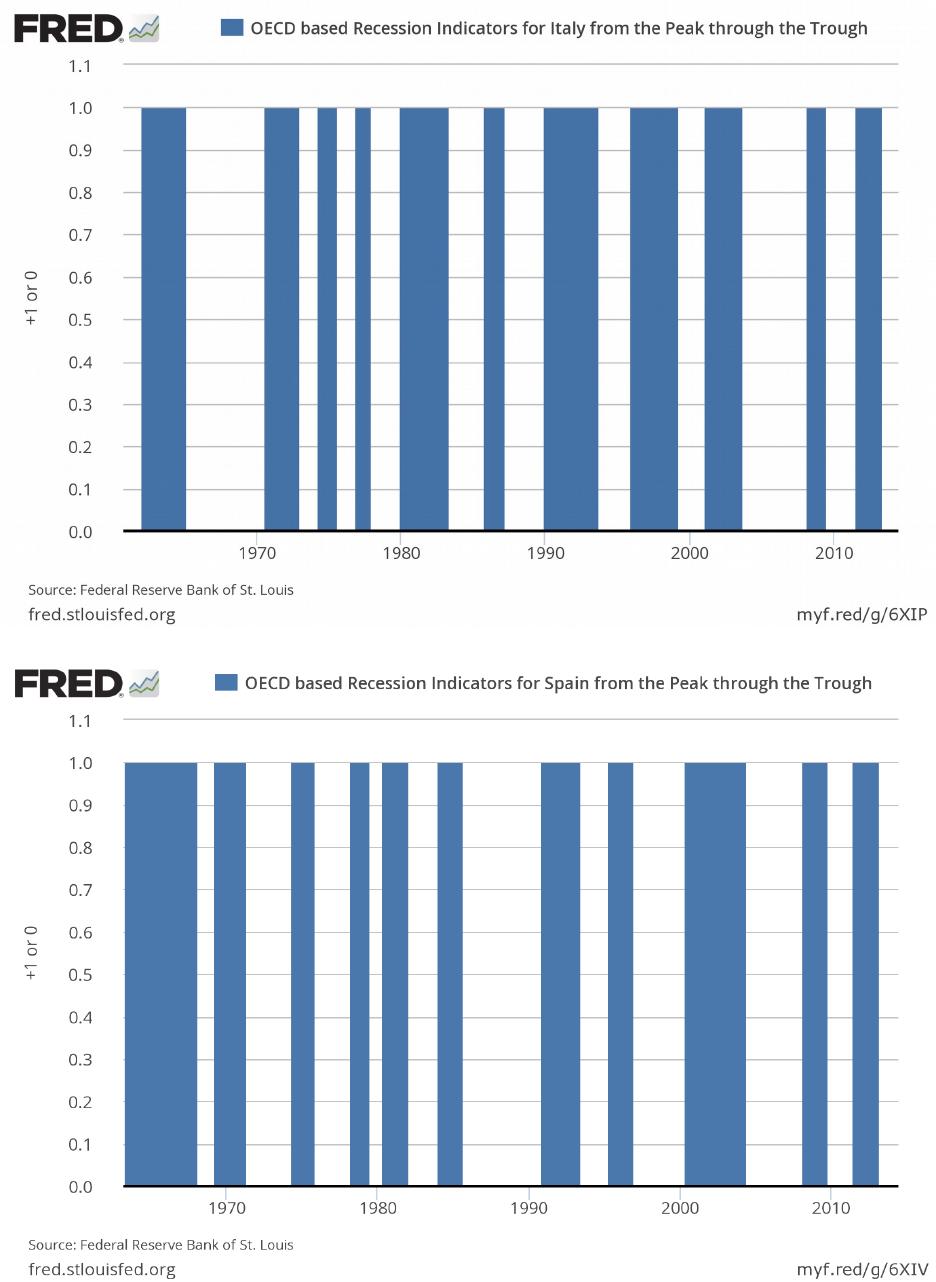

3. Compare the frequency and timing of recessions in key European economies

since 1960. Make separate bar charts for Germany (FRED code: DEURECM),

Italy (FRED code: ITARECM), and Spain (FRED code: ESPRECM). Do their

business cycles appear sufficiently well-aligned to make them operate easily in a

single currency area with a common monetary policy? (LO3)

Answer: The plots are below. While there appears to be some overlap, the timing

and duration of recessions in the European countries are not identical.

These differences may reflect differing mixes of goods and services, different

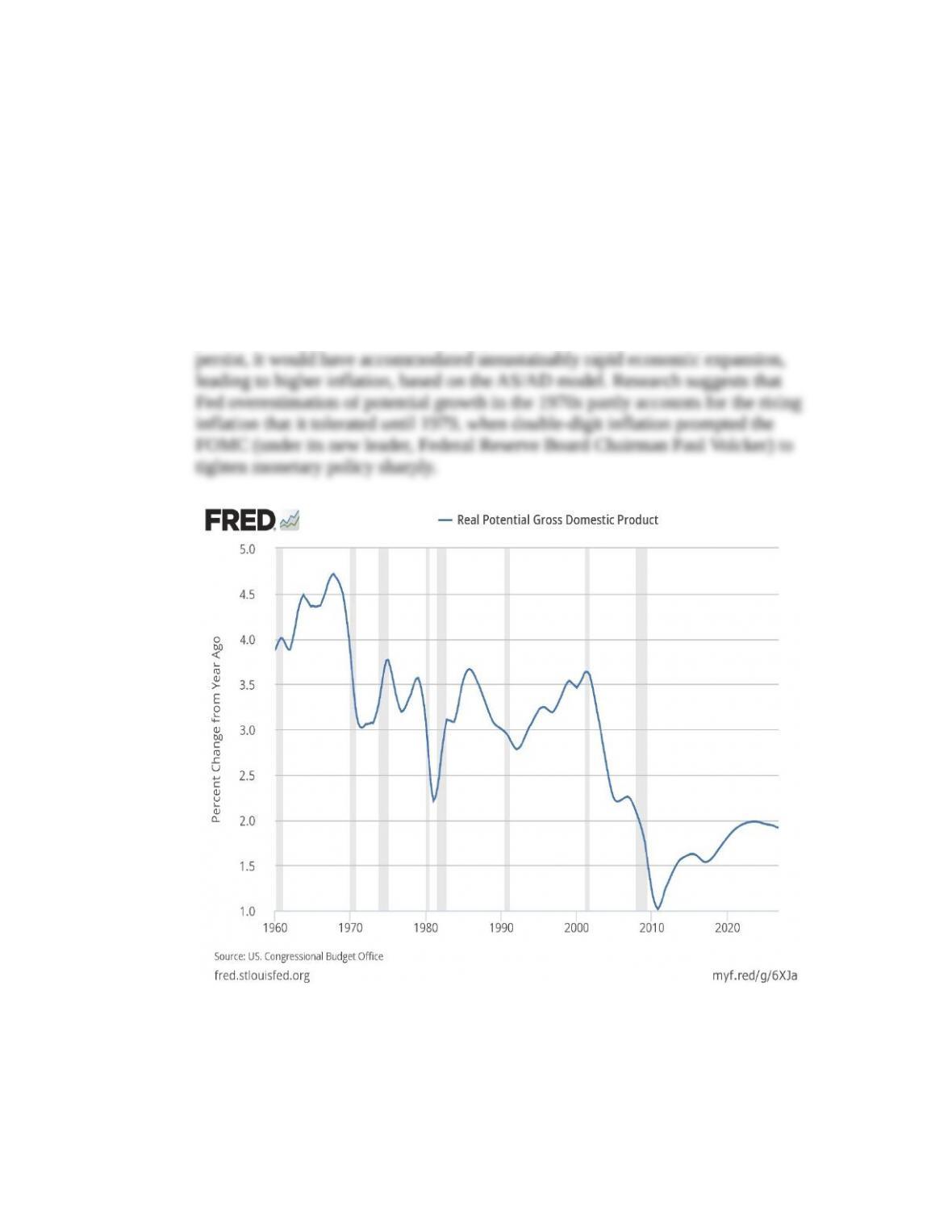

4. To keep inflation low and steady, central banks would like to keep output

reasonably close to its potential level, but can they anticipate changes in potential

GDP? Plot since 1960 the percent change from a year ago of the Congressional

Budget Office’s estimate of potential GDP (FRED code: GDPPOT). Suppose that

the FOMC assumed that the growth rate of potential GDP remained permanently

at its 1960s average. What would you expect to happen to inflation? Why? (LO1)

Answer: The plot appears below. According to the CBO, potential GDP growth

averaged 4.3 percent in the 1960s. From 1970 to mid-2016, it averaged 2.8

percent. Had the FOMC assumed that potential GDP growth of 4.3 percent would

* indicates more difficult problems