1. If the Federal Reserve decides to sterilize the foreign exchange market intervention described

should assume that the intervention took place in a deep, well-functioning foreign exchange

market. (LO2)

Answer: If the Fed decides to sterilize the FX market intervention, it will carry out an open

market operation to offset the impact of the FX intervention on the monetary base. In this

case, it will carry out an open market operation where it purchases $1,000 of U.S. securities.

This will increase U.S. securities by $1,000 on the asset side of the balance sheet and

reserves.

The overall impact on the balance sheet is shown below. On the asset side, there is a

compositional change between FX and domestic securities while on the liability side

intervention itself is tiny relative to the overall volume traded in the market. It is through

changes in the domestic interest rate that foreign exchange market interventions affect the

exchange rate.

2. Use a supply-and-demand diagram for dollars to show the impact of an increase in U.S.

market intervention by the Federal Reserve. (LO2)

Answer: If the U.S. interest rate rises as a result of a purchase of dollars from the market by

in the supply of dollars from U.S. investors wishing to purchase foreign assets. The overall

3. Do you think the U.S. dollar is more likely to strengthen or weaken over the next few

months? Explain your reasoning. (LO1)

Answer: Shorter-term movements in floating exchange rates, like other asset prices, are

typically unpredictable, with the current exchange rate usually being the best predictor of the

conditions, this would contribute to dollar strength.

On the other hand, concern about the path of U.S. fiscal policy and related concerns that the

central bank may tolerate faster inflation could lead to a decline in the dollar.

4. *Consider a small open economy with a wide array of trading partners all operating in

different currencies. The economy’s business cycles are not well synchronized with any of

economy adopt a fixed exchange-rate regime? (LO3)

Answer: In this situation, fixing the exchange rate does not look like a good idea. Given that

the country’s trading partners operate in different currencies, fixing against one currency

Fixing your exchange rate to another currency involves adopting the other country’s interest

economies, the monetary policy decisions of the large country could exacerbate business

cycle fluctuations.

Quantity of dollars traded

D0

D1

S1

Fixing the exchange rate ties the hands of local policymakers who can often help to gain

discipline doesn’t appear to be necessary in this country.

5. A small Eastern European economy asks your opinion about whether it should pursue the

(LO4)

Answer: Joining the EMU has many advantages over “euroization”. The economy would

resort in making euro loans.

21. In the face of increased short-run synchronization of global stock markets, what

strategies could you employ to continue to benefit from international diversification? (LO1)

If you have a shorter-term investment horizon, you could invest in a portfolio of stocks

Data Exploration

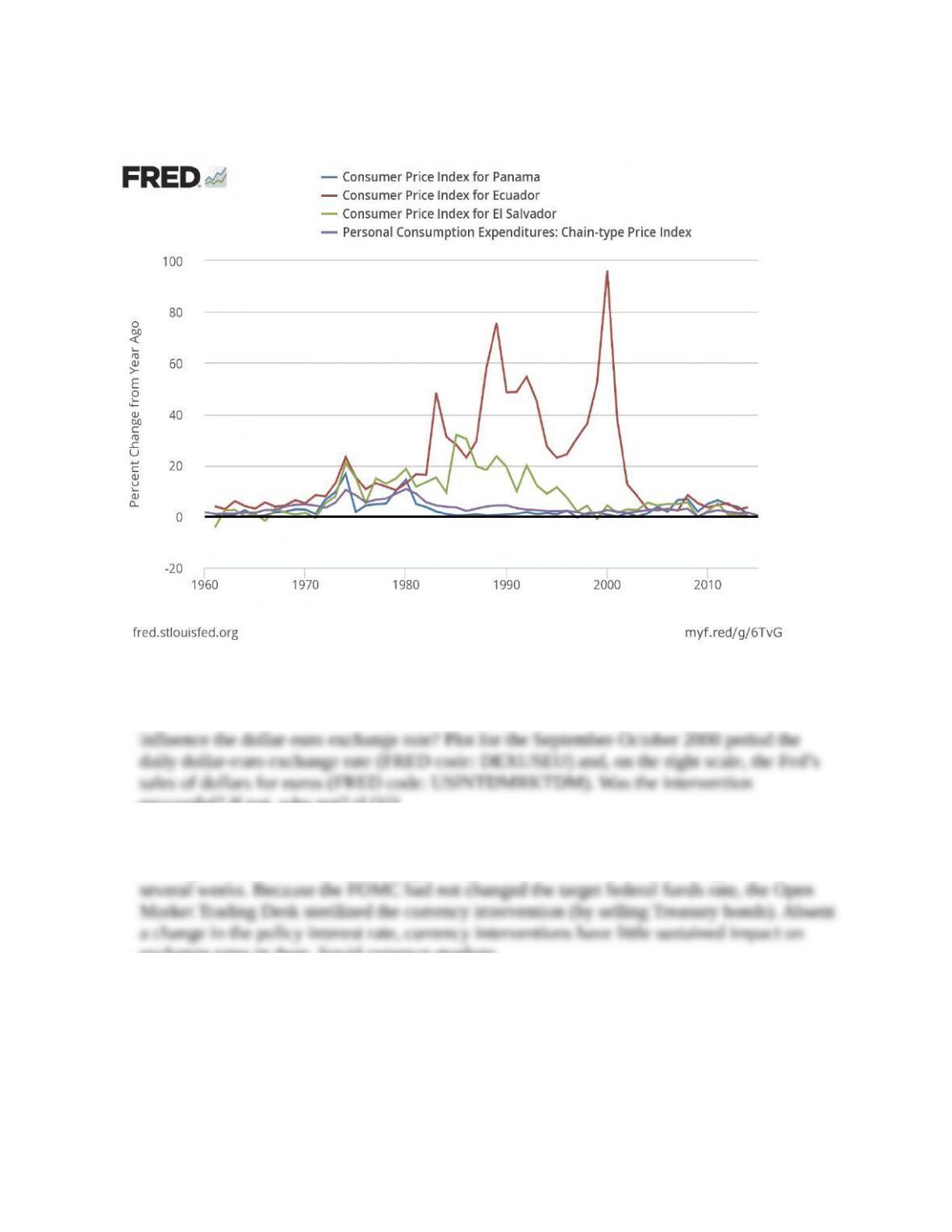

1. Panama, Ecuador, and El Salvador began using the U.S. dollar as their domestic currency in

1904, 2000, and 2001, respectively. How do you expect their inflation rates to compare with

date of dollarization), compare the average inflation rate in each country with U.S. inflation.

(LO4)

Answer: The data is plotted below. Broadly speaking, the inflation rates of these countries

percent in 2000 to 12 percent in 2002, and has averaged 4.3 percent thereafter. El Salvador

experienced average inflation of 3.0 percent after 2000.

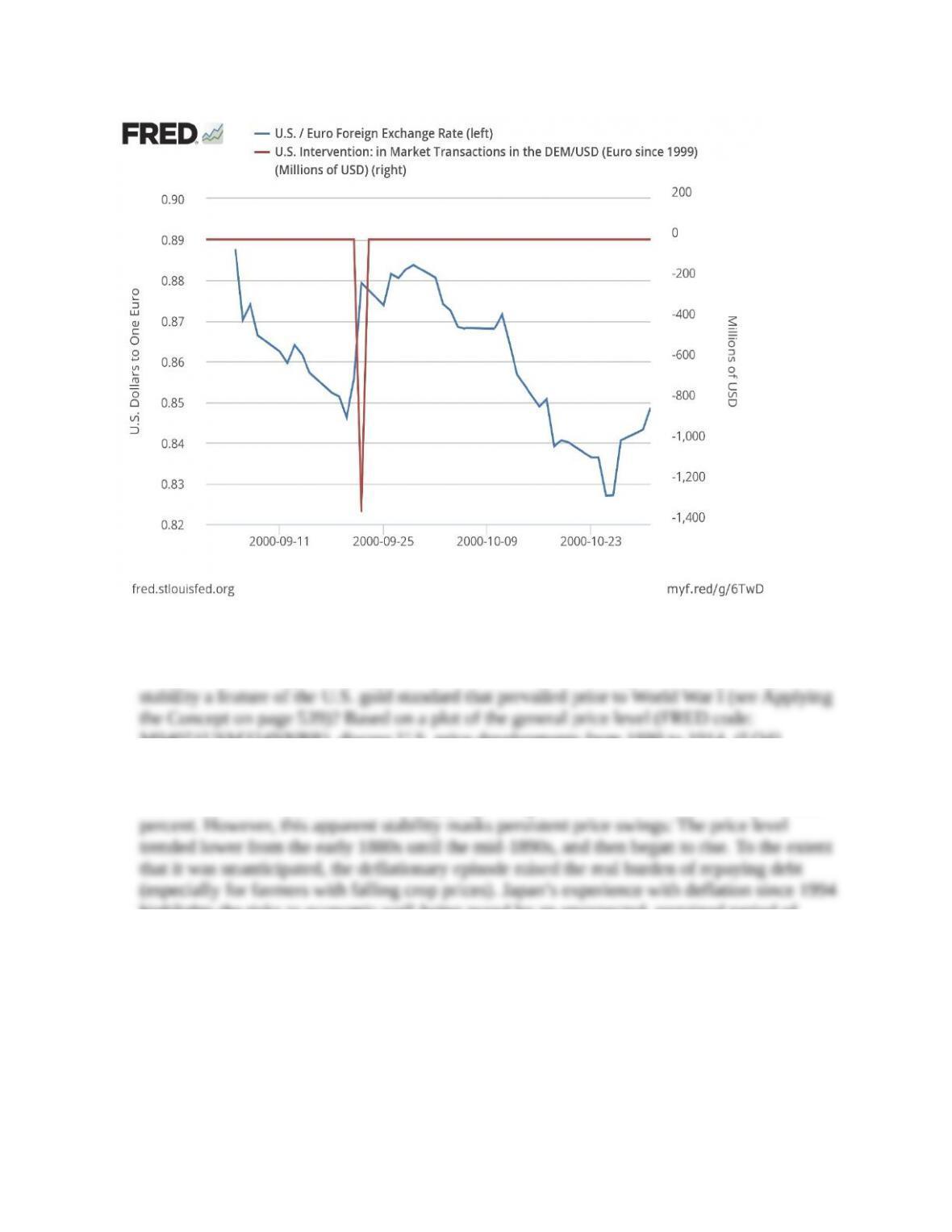

2. Did the September 2000, currency intervention by the United States and other countries

successful? If not, why not? (LO2)

Answer: The data is plot is below. The intervention appears to have boosted the euro only for

a brief period, with the euro returning to its pre-intervention value and sinking further after

exchange rates in deep, liquid currency markets.

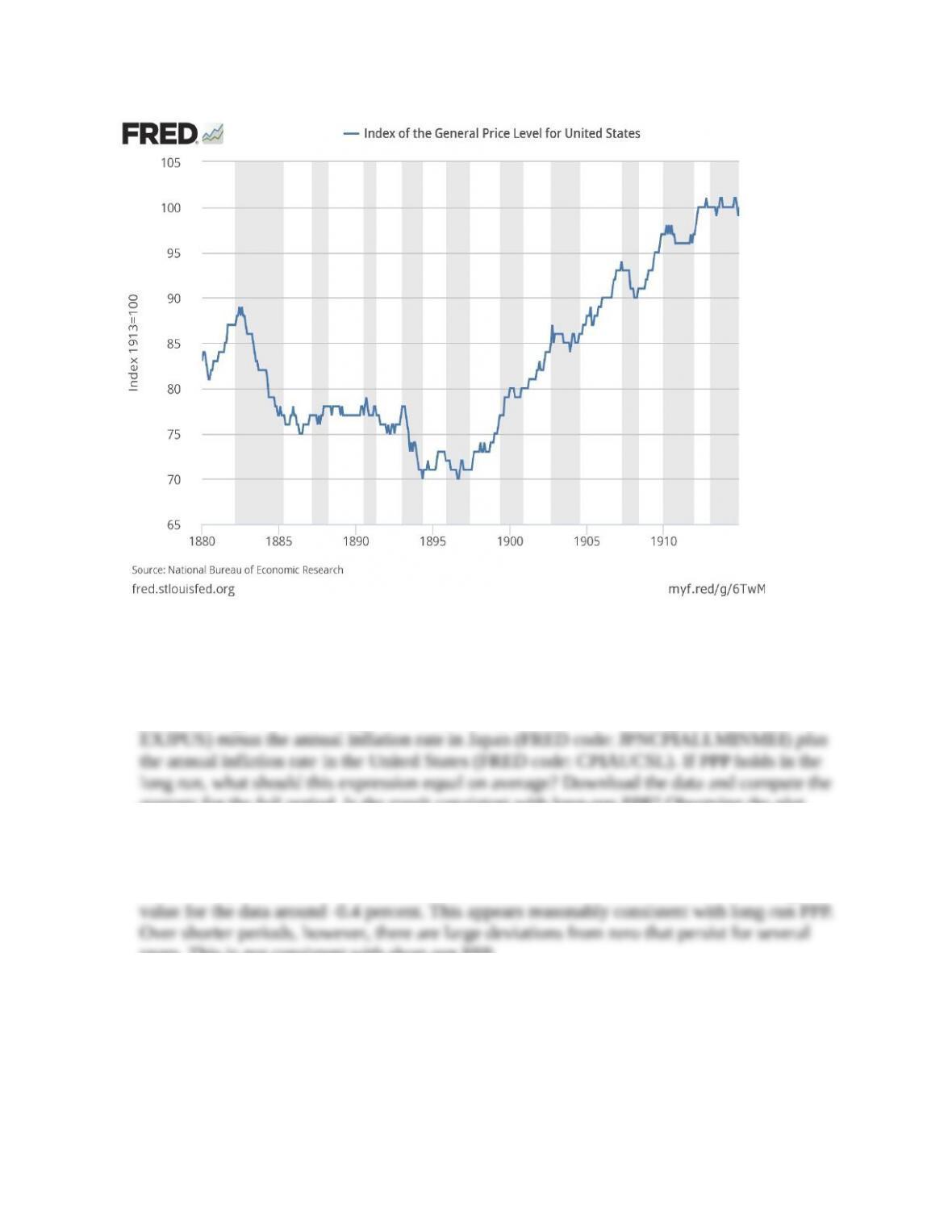

3. Some claim that adoption of a gold standard would contribute to price stability. Was price

M04051USM324NNBR), discuss U.S. price developments from 1880 to 1914. (LO4)

Answer: The data plot is below. Over the 30-year period from 1882 to 1914, the price level

increased from a value of 87 to 100, implying average annual inflation of less than one-half

highlights the risks to economic well-being posed by an unexpected, sustained period of

falling prices.

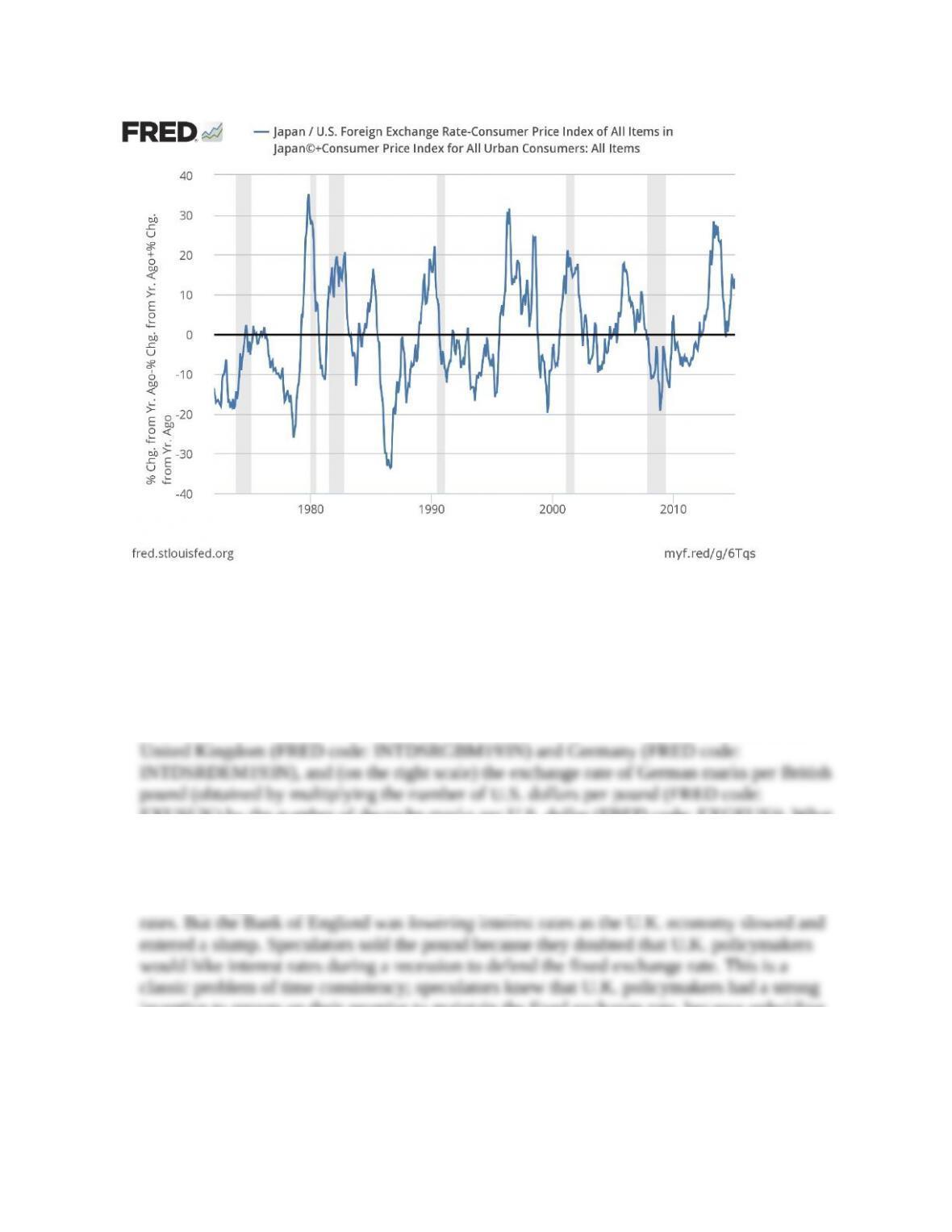

4. Does purchasing power parity (PPP) hold in the long run? Does it hold in the short run?

Following text equation (3), plot for Japan and the United States beginning in 1972 the

percent change from a year ago of the Japanese yen/U.S. dollar exchange rate (FRED code:

average for the full period. Is the result consistent with long-run PPP? Observing the plot,

does PPP seem to hold in the short run? (LO1)

Answer: The data is plotted below. If PPP holds, the computed expression should average to

zero. For Japan and the United States, the data do fluctuate around zero, with the average

years. This is not consistent with short-run PPP.

Organization for Economic Co-operation and Development, Consumer Price Index of All Items in Japan©

[JPNCPIALLMINMEI], retrieved from FRED, Federal Reserve Bank of St. Louis;

https://fred.stlouisfed.org/series/JPNCPIALLMINMEI.

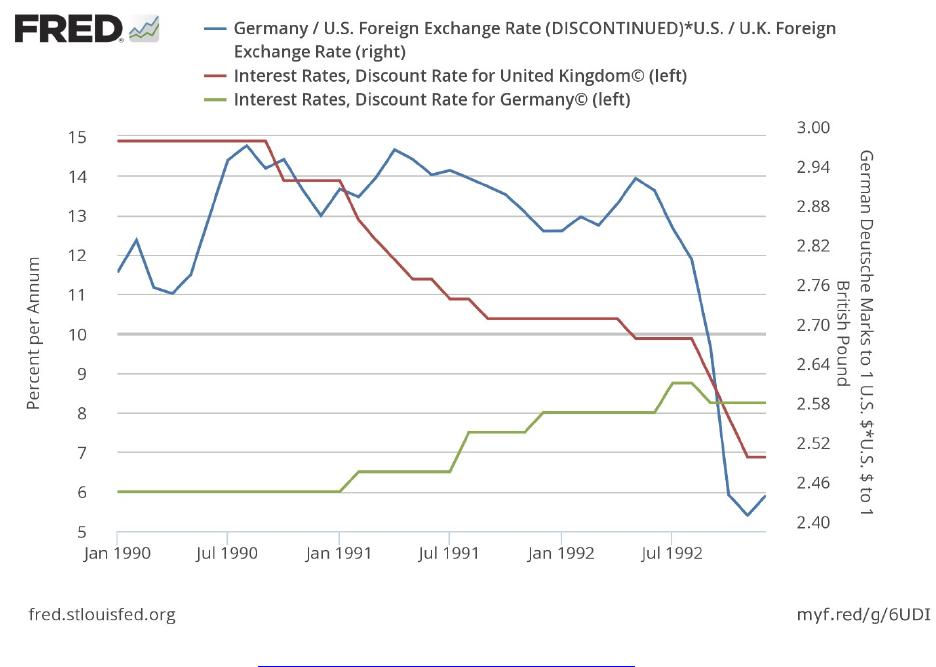

5. In September 1992, a speculative attack compelled the United Kingdom to devalue the

British pound versus the German currency (the deutsche mark). How did monetary policies

in both countries influence this outcome? Plot from 1990 to 1992 the discount rates in the

EXUSUK) by the number of deutsche marks per U.S. dollar (FRED code: EXGEUS)). What

do you conclude? (LO3)

Answer: The plot appears below. In the early 1990s, the re-unification of west and east

Germany triggered an economic boom, prompting the German central bank to raise interest

incentive to renege on their promise to maintain the fixed exchange rate, because upholding

that promise could trigger a deeper recession.

International Monetary Fund, Interest Rates, Discount Rate for Germany© [INTDSRDEM193N], retrieved from FRED,

Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/INTDSRDEM193N. International Monetary Fund,

Interest Rates, Discount Rate for United Kingdom© [INTDSRGBM193N], retrieved from FRED, Federal Reserve Bank of

St. Louis; https://fred.stlouisfed.org/series/INTDSRGBM193N.

* indicates more difficult problems