17. The central bank of a country facing economic and financial market difficulties asks for your

during the financial crisis of 2007-2009, what might you advise this central bank to do?

(LO4)

Answer: You should advise the central bank to use unconventional monetary policy tools.

This could include expanding its balance sheet significantly, providing aggregate reserves

intermediaries (targeted asset purchases). It could also inform markets of its commitment to

keep interest rates low (forward guidance).

18. *Suppose ECB officials ask your opinion about their operational framework for monetary

managing the supply of reserves. What specific changes would you suggest the ECB should

make to its system in the future? (LO3)

Answer: As national markets become more integrated, and the euro-area financial crisis

recedes, you might suggest that the ECB concentrate its operations in Frankfurt instead of

for such changes will become more urgent as more countries join EMU.

19. In June 2014, the European Central Bank (ECB) cut the interest rate it pays on excess

reserves below zero. What was the rationale for this move and why would banks be willing

to pay to keep deposits with the ECB? (LO1)

Answer: The ECB cut the rate in an effort to provide further monetary accommodation. The

their vaults also is costly. The transactions costs of using cash include storage, transport and

insurance.

20. Inflation, rather than the price level or nominal GDP, is the policy target of choice for many

of the world’s central banks. Provide a reason why you think this is the case. (LO2)

businesses to make decisions about the future.

Data Exploration

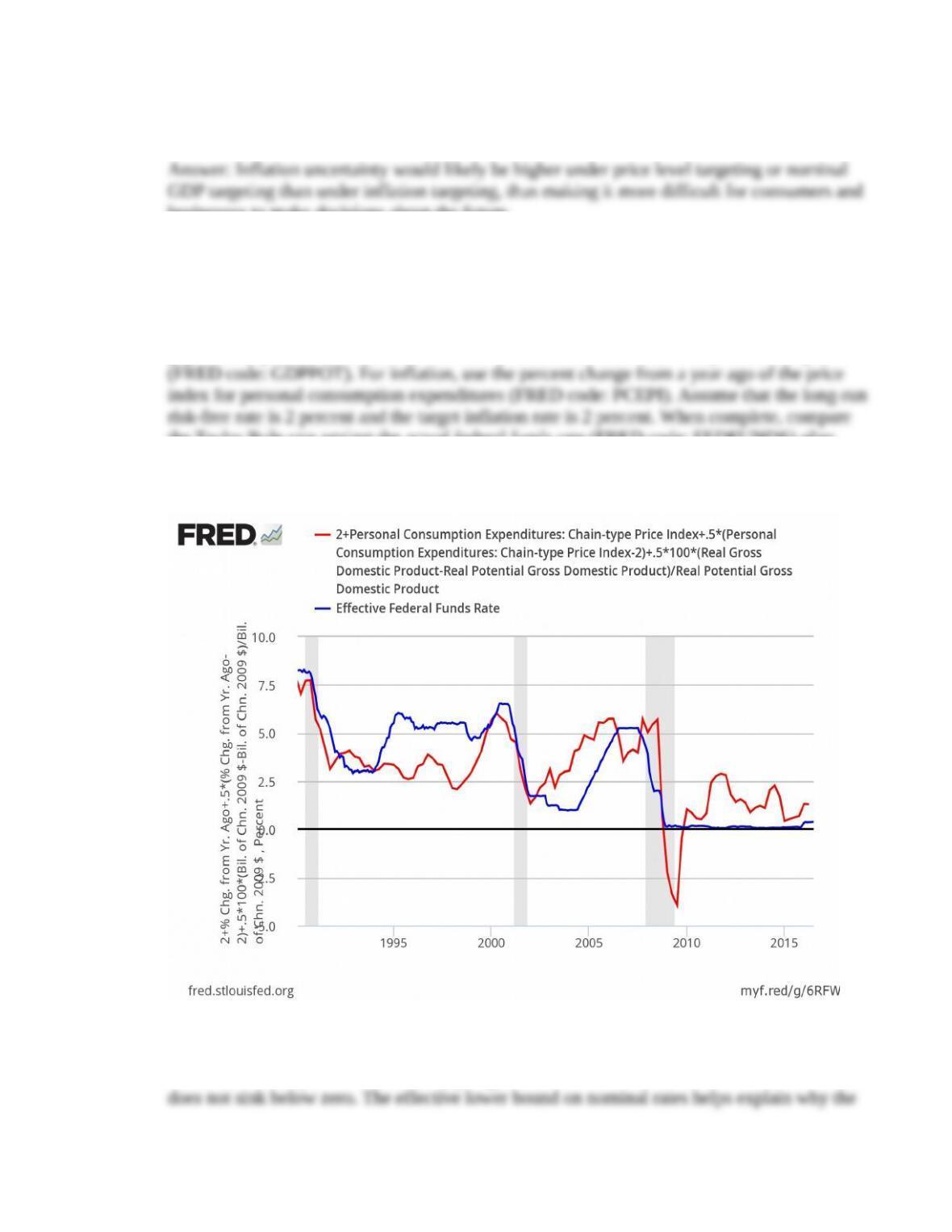

1. Plot the Taylor Rule since 1990 on a quarterly basis (similar to Figure 18.7). For the output

gap, use the percent deviations of real GDP (FRED code: GDPC1) from potential output

the Taylor Rule rate against the actual federal funds rate (FRED code: FEDFUNDS) after

2007. (LO3)

Answer: The data plot is:

Notice that the Taylor rule turns sharply negative in 2009 and 2010, but the federal funds rate

guidance, quantitative easing and targeted asset purchases.

2. On December 15, 2015, the FOMC raised the target range for the market federal funds rate

by 25 basis points (bp) to a range of ¼ to ½ percent. It also instructed the Open Market Desk

FF). Explain the plot, noting the impact of the FOMC decision on these two interest rates as

well as the implicit role played by the offering rate on ON RRPs. (LO4)

Answer: The data are plotted below. No bank will lend below the IOER rate when it can earn

the risk-free IOER rate by making deposits at the Fed. However, some financial

intermediaries like government-sponsored enterprises (GSEs) are not eligible to earn interest

from the Fed. These institutions lend in the federal funds market to earn positive interest

rate. Thus, in practice, when the Fed offers ON RRPs in sufficient quantity, the offering rate

sets a floor on the funds rate, as the experience after the FOMC meeting indicates.

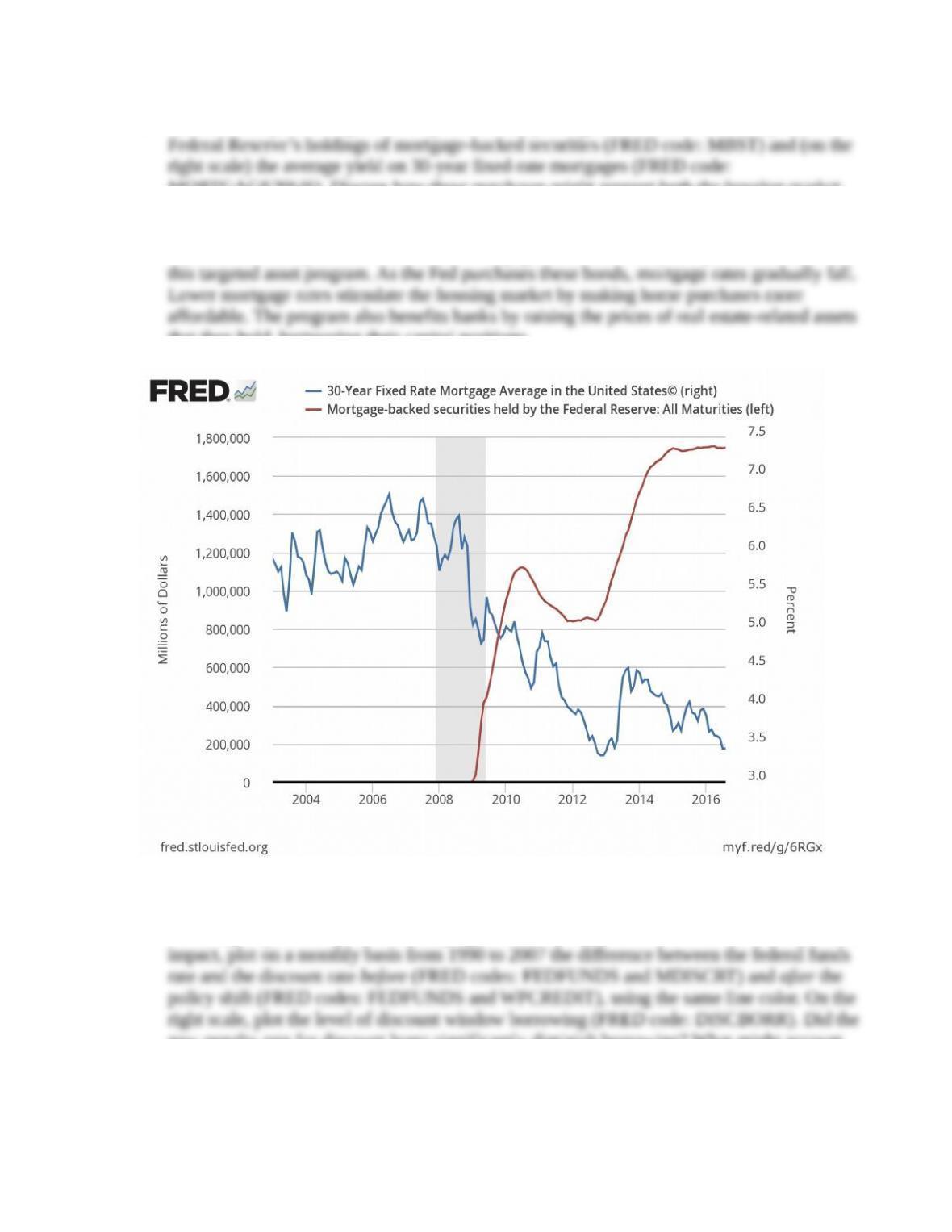

3. Assess the impact of targeted asset purchases by plotting since 2003 on a monthly basis the

MORTGAGE30US). Discuss how these purchases might support both the housing market

and the banking system. (LO4)

Answer: The data plot below shows the mortgage rate for several years prior to the onset of

that they hold, buttressing their capital positions.

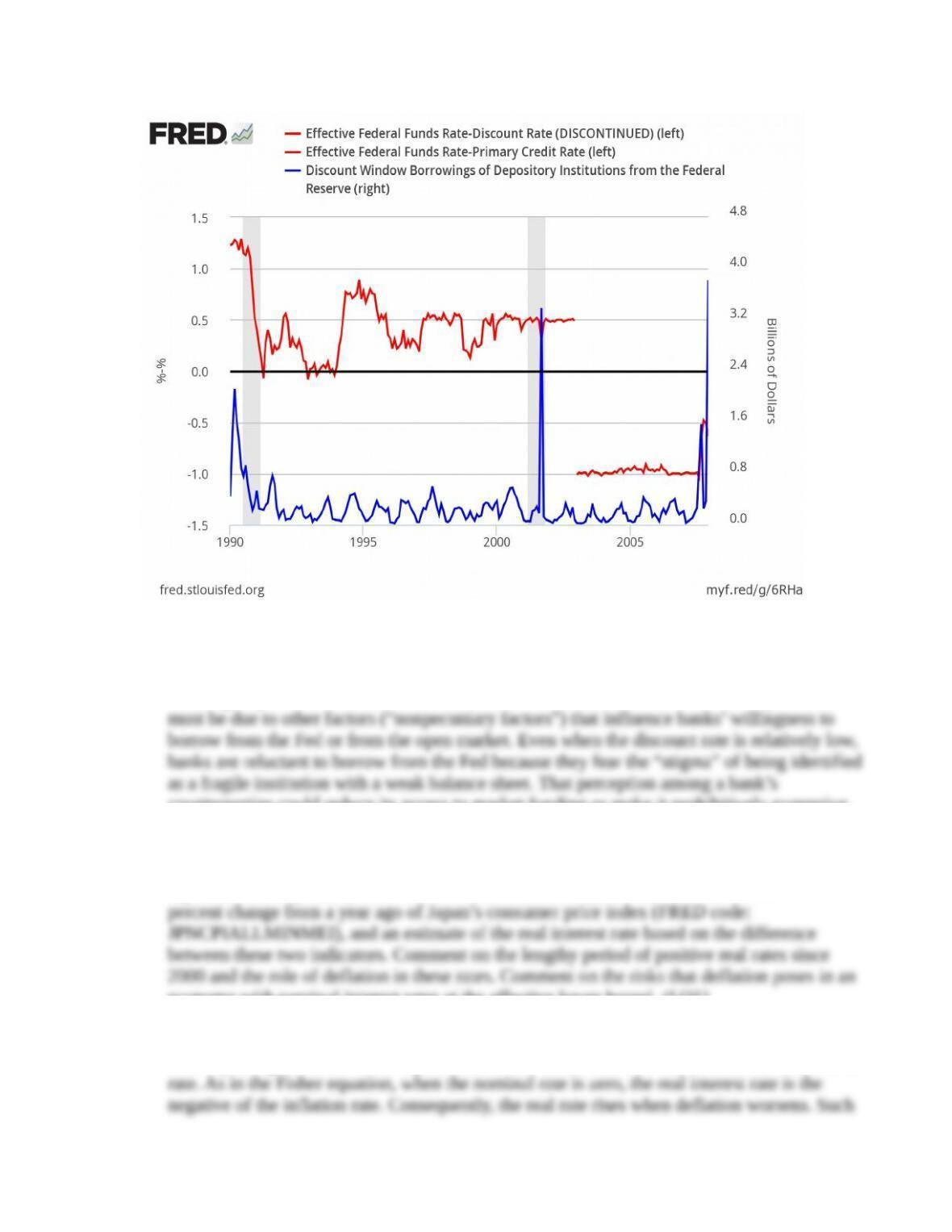

4. In 2002, the Federal Reserve began to set the discount rate above the federal funds rate,

reversing its previous practice of keeping the discount rate below the funds rate. To assess the

new penalty rate for discount loans significantly diminish borrowing? What might account

for the behavior of discount window borrowing? (LO1)

Answer: Prior to 2002, the federal funds rate was above the discount rate, but banks

borrowed relatively little from the Fed. Moreover, the volume of borrowing did not change

meaningfully after the discount rate was set above the federal funds rate. The explanation

counterparties could reduce its access to market funding or make it prohibitively expensive.

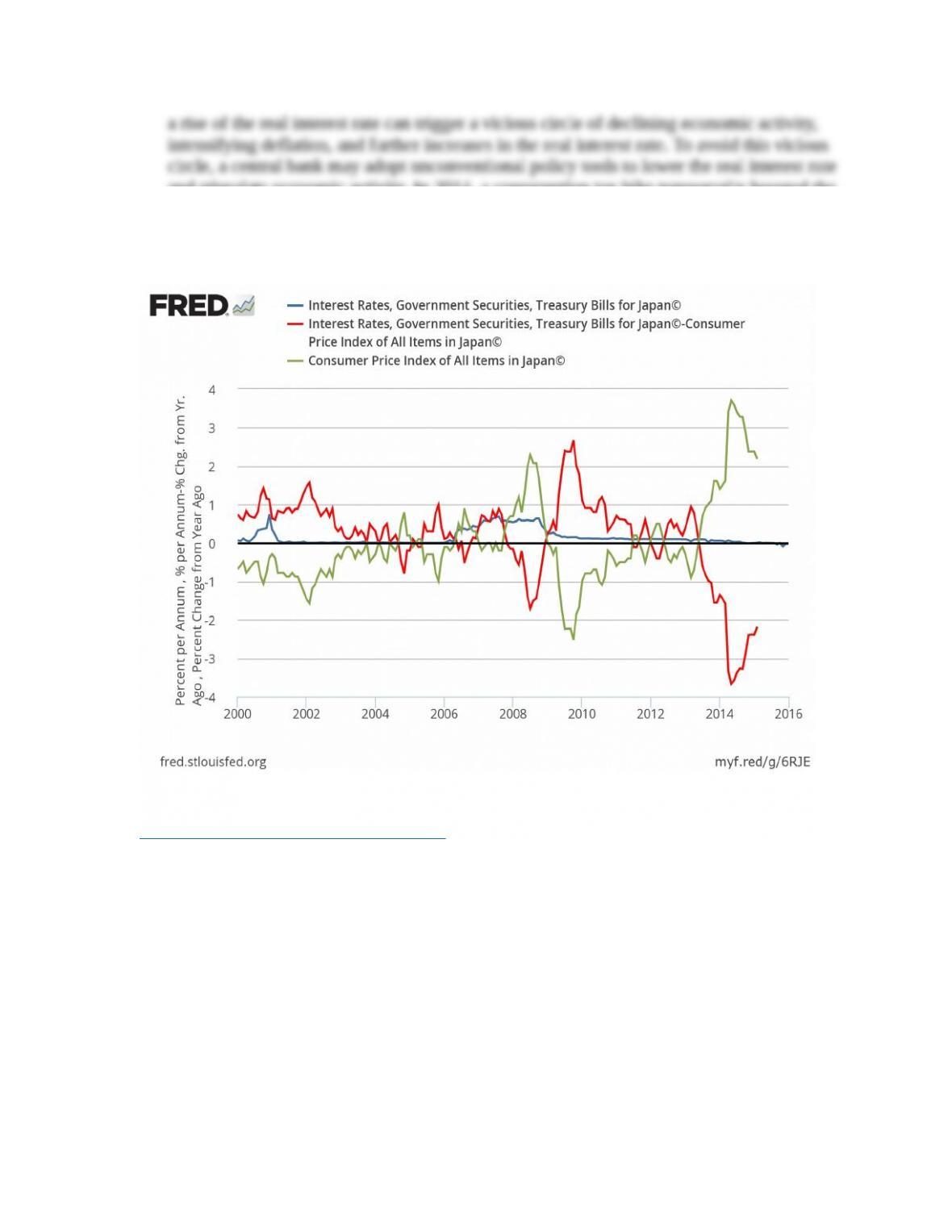

5. Examine the real interest rate in Japan, plotting since 2000 the nominal interest rate on

Japanese Treasury bills (FRED code: INTGSTJPM193N), the inflation rate based on the

economy with nominal interest rates at the effective lower bound. (LO1)

Answer: If expected inflation is equal to the inflation rate measured as the percentage change

from a year ago of the consumer price index, then the red line is a measure of the real interest

and stimulate economic activity. In 2014, a consumption tax hike temporarily boosted the

measured inflation rate in Japan; as a result, with nominal rates continuing at zero, the

measured real rate appeared very negative. However, as of 2016, CPI inflation again

subsided, raising the measured real interest rate.

Organization for Economic Co-operation and Development, Consumer Price Index of All Items in Japan©

[JPNCPIALLMINMEI], retrieved from FRED, Federal Reserve Bank of St. Louis;

https://fred.stlouisfed.org/series/JPNCPIALLMINMEI.

International Monetary Fund, Interest Rates, Government Securities, Treasury Bills for Japan© [INTGSTJPM193N], retrieved

from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/INTGSTJPM193N.

* indicates more difficult problems