1. Do you think, in the interest of transparency, the Chair of the Federal Reserve

or why not? (LO2)

Answer: Since 2012, the Fed Chair has conducted quarterly press conferences

following those FOMC meetings where members’ quantitative economic and

policy rate forecasts are published. This practice mirrors the communications

can lead to confusion and uncertainty when the decisions themselves are unclear

or contentious.

2. Suppose a fellow student in your money and banking class made the following

On what basis could you disagree with this student? (LO1, LO3)

Answer: Expressing a numerical target for inflation but not for the maximum

employment element of the mandate does not imply that greater importance is

conflict, it will take a “balanced approach”, emphasizing the equal standing of

both parts of the mandate.

3. Compare the communication strategies of the Federal Reserve and the ECB. In

justified in omitting each of them. (LO1, LO3)

Answer: The communication strategies of the Fed and the ECB share many

common elements: they both immediately release the target interest rate with a

research.

In contrast to the ECB, the Fed makes public the votes of individual votes of the

publishes transcripts of its meetings after a five-year lag.

Not publishing votes of Governing Council members can be justified on the basis

that it makes it more feasible for members who represent individual countries to

published with a long lag.

4. During the euro-area crisis, interest-rate spreads between the sovereign debt of

pattern?

Data Exploration

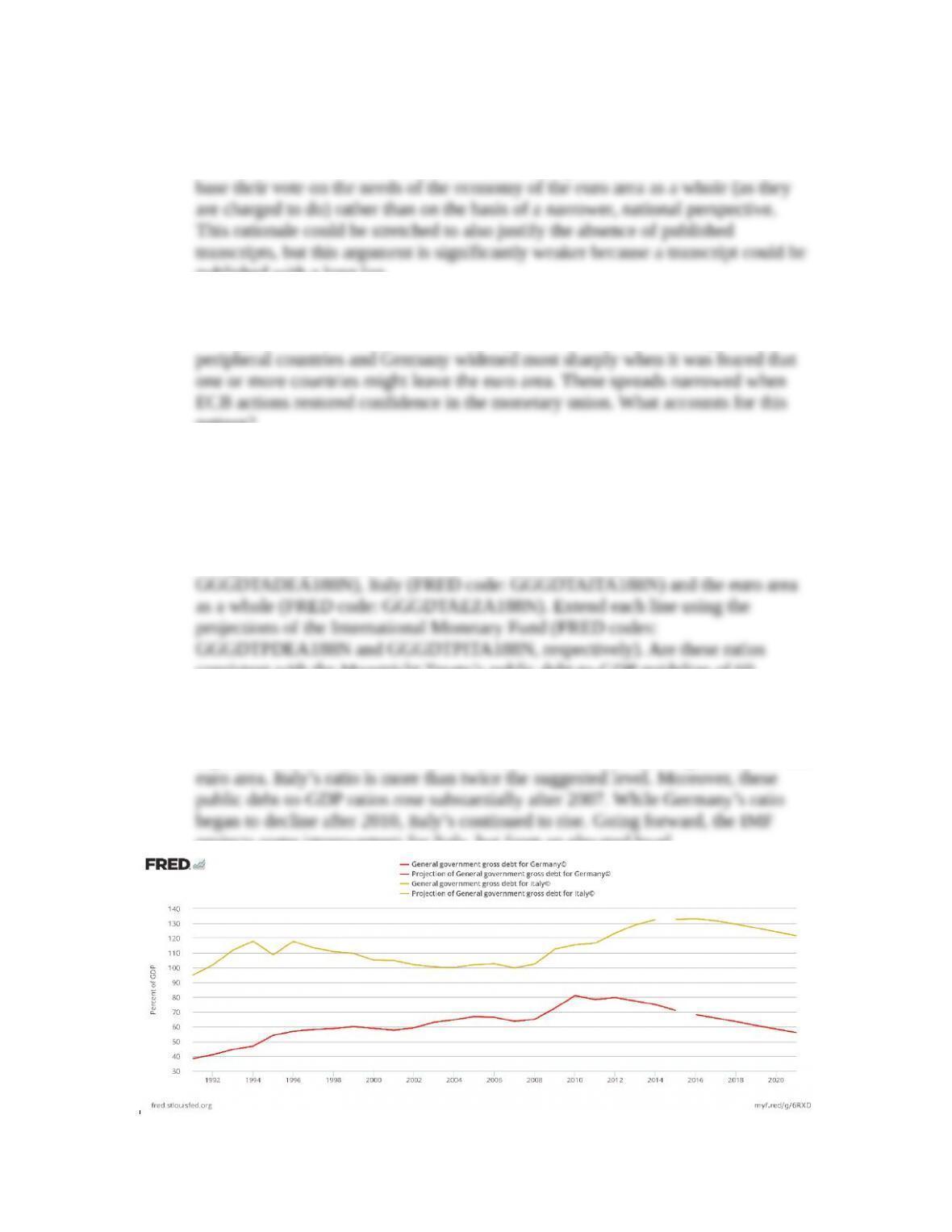

1. How large are the public debt burdens of key euro-area economies? Are they

rising or falling? Plot the debt-to-GDP ratios of Germany (FRED code:

consistent with the Maastricht Treaty’s public debt-to-GDP guideline of 60

percent? (LO4)

Answer: As of 2015, even Germany, the largest and perhaps the healthiest of the

big euro-area economies, has a debt-to-GDP ratio above the 60% guideline for the

projects some improvement for Italy, but from an elevated level.

International Monetary Fund, General government gross debt for Germany© [GGGDTADEA188N], retrieved from

FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/GGGDTADEA188N.

International Monetary Fund, Projection of General government gross debt for Germany© [GGGDTPDEA188N],

retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/GGGDTPDEA188N.

International Monetary Fund, General government gross debt for Italy© [GGGDTAITA188N], retrieved from FRED,

Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/GGGDTAITA188N,

International Monetary Fund, Projection of General government gross debt for Italy© [GGGDTPITA188N], retrieved

from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/GGGDTPITA188N.

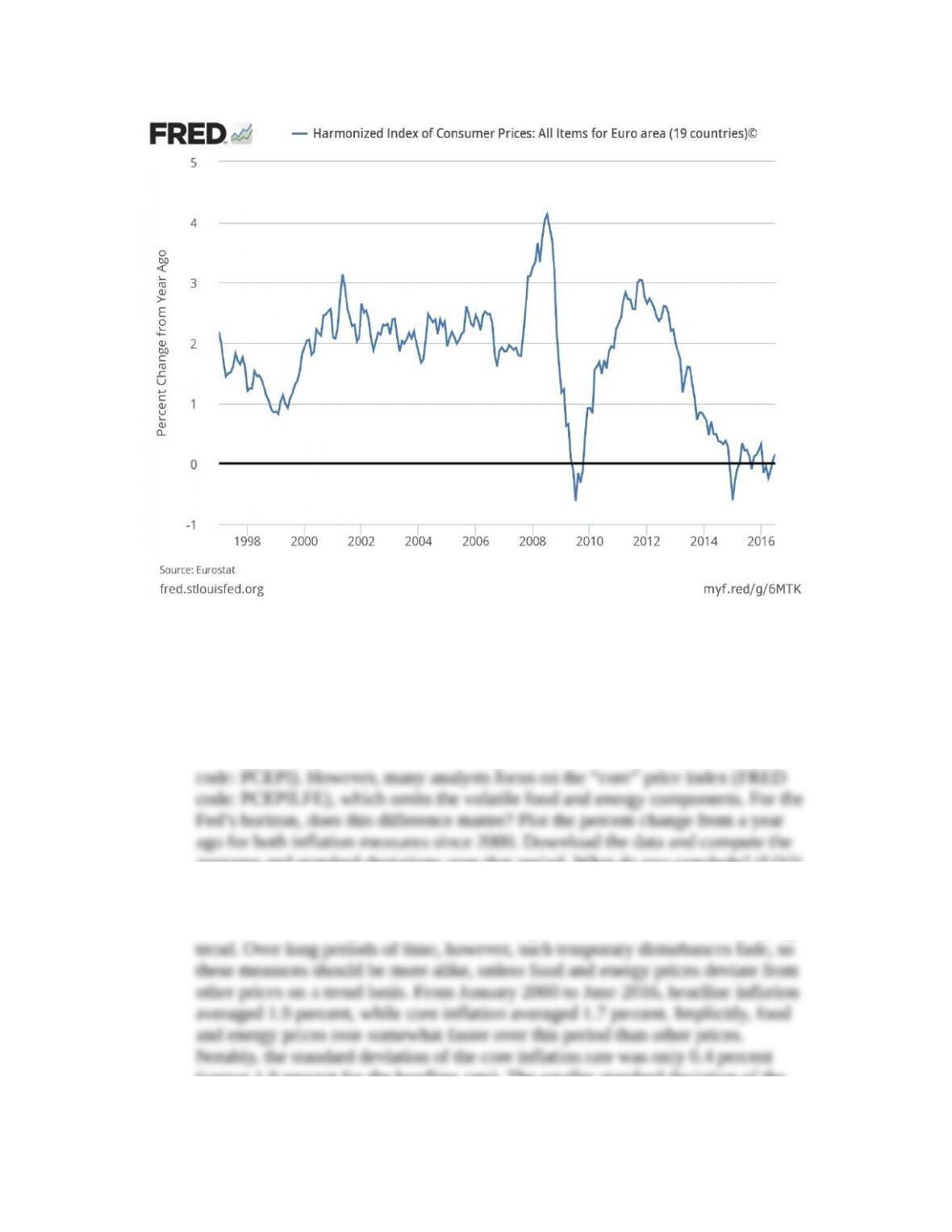

2. The European Central Bank (ECB) has translated its primary objective of price

stability into an explicit, quantitative goal of keeping euro-area annual inflation

compute the average inflation rate for the full period and for the periods

2008-2009, 2010-2011, and 2012-present. (LO4)

Answer: The plot is shown below. Over short periods, measured inflation varies

significantly as a result of temporary price disturbances that do not affect the trend

of inflation. Moreover, monetary policy changes influence inflation only with a

the ECB is pursuing expansionary policies to raise the euro-area inflation rate

toward its goal of just below 2 percent.

Eurostat, Harmonized Index of Consumer Prices: All Items for Euro area (19 countries)© [CP0000EZ19M086NEST],

retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CP0000EZ19M086NEST.

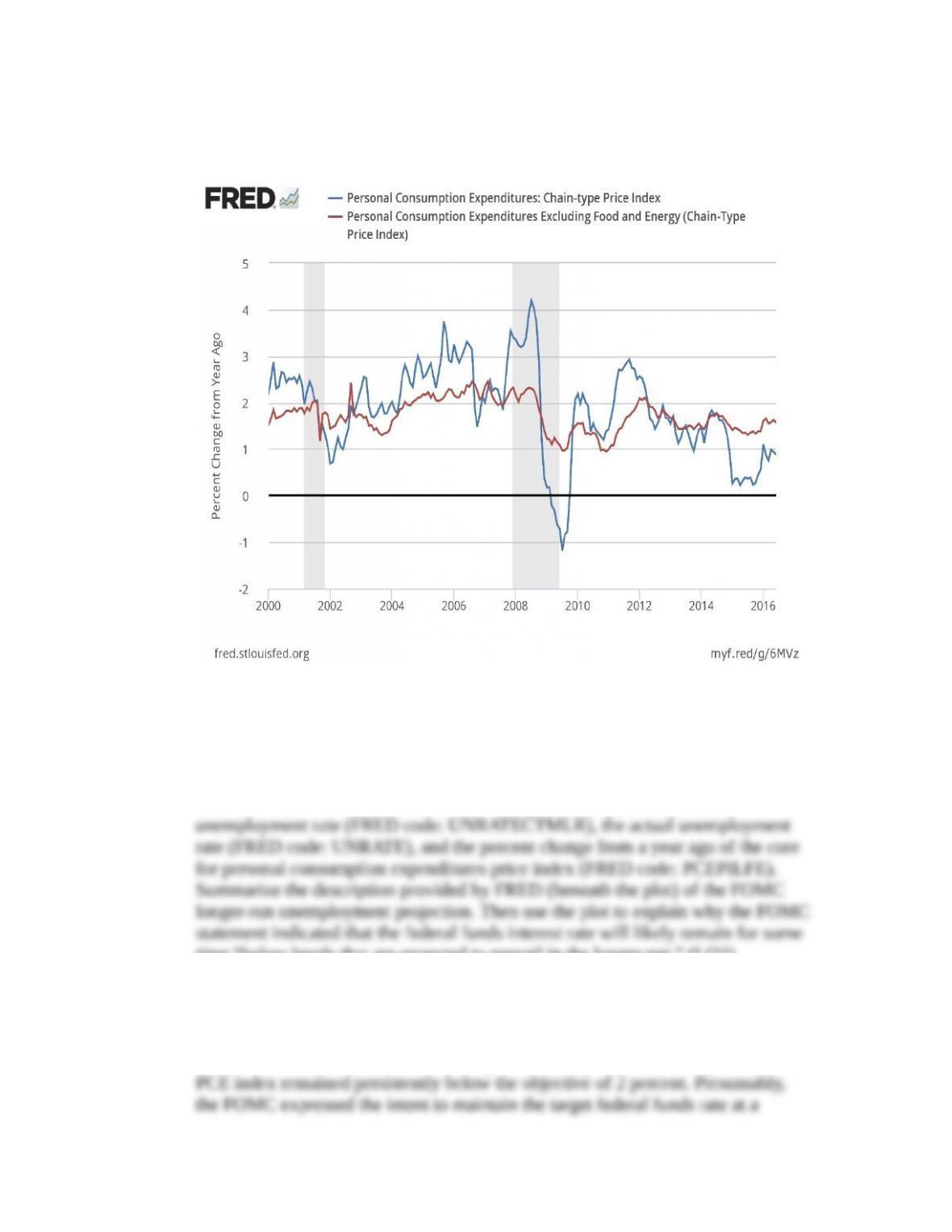

3. In 2012, the Federal Reserve announced an inflation objective of 2 percent “over

the longer run” for the personal consumption expenditures price index (FRED

averages and standard deviations over that period. What do you conclude? (LO2)

Answer: The core index is relatively useful for examining the trend of inflation,

because volatile components of the headline price index can mask its underlying

(versus 1.0 percent for the headline rate). The smaller standard deviation of the

core measure means that it is usually a more reliable signal of the underlying

inflation trend.

4. Its statement of July 27, 2016, indicated that the FOMC it would pursue policies

to meet its “objectives of maximum employment and 2 percent inflation.” Plot

since 2009 the evolution of the FOMC’s longer-run projection for the

time “below levels that are expected to prevail in the longer run.” (LO2)

Answer: The midpoint of the projections of members of the FOMC reflects the

median estimate of the “normal” unemployment rate consistent with “maximum

employment.” By mid-2016, the actual unemployment rate had reached that level.

However, inflation as measured by the percent change from a year ago of the core

that its inflation target is symmetric, meaning that it is not biased in favor of

inflation that is somewhat above 2 percent or somewhat below 2 percent.

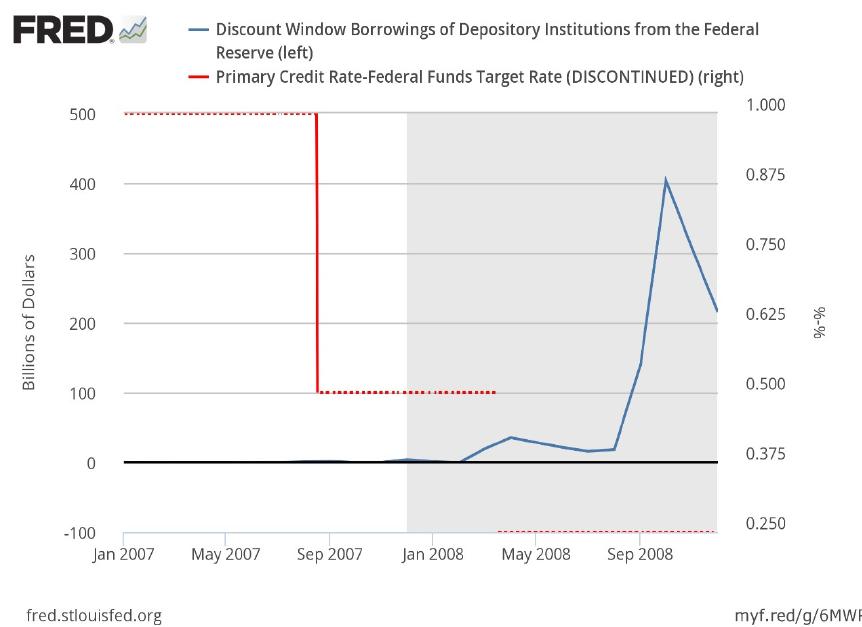

5. In August 2007 and in March 2008, the Federal Reserve Board reduced the

discount rate to ease liquidity conditions for banks. Plot discount window

funds target rate trigger the borrowing surge in September-October 2008? (LO2)

Answer: The data plot is below. The data show no immediate effect from the

discount rate cut in August 2007 (that narrowed the spread to 50 basis points) and

(see Chapter 3 Lessons from the Crisis: Interbank Lending), not the March change

in the discount rate.

* indicates more difficult problems