Chapter 14

Regulating the Financial System

Conceptual and Analytical Problems

1. Explain how a bank run can turn into a bank panic. (LO1)

Answer: Bank runs occur when people fear that their bank has become insolvent. Depositors

turn into system-wide bank panics because customers have a difficult time distinguishing

insolvent banks from solvent ones.

2. Current technology allows large bank depositors to withdraw their funds electronically at a

is called a silent run. When might a silent run happen, and why? (LO1)

Answer: Depositors may have their accounts set up so that funds are automatically

Depositors are likely to need to withdraw funds at the same time, leading to a silent run.

3. Explain why financial institutions such as pension funds and insurance companies are not as

Answer: Like deposit-taking institutions, money market mutual funds and securities dealers

though their assets tend to be illiquid, they are not as vulnerable to runs.

4. Explain the link between falling house prices and bank failures during the financial crisis of

2007-2009. (LO1)

Answer: Falling house prices led to a higher rate of mortgage defaults (as some customers

could not re-finance to a lower interest rate as they had planned, for example). These

wiped out and so the bank failed.

5. Discuss the regulations that are designed to reduce the moral hazard created by deposit

insurance. (LO3)

Answer: Regulators can restrict competition so that banks are not under as much pressure to

engage in risky investments. They can also prohibit banks from making certain types of

capital requirements.

6. During the financial crisis of 2007-2009, the Federal Reserve used its emergency authority to

function added to moral hazard. (LO2)

Answer: Nonbanks (including shadow banks) are subject to less oversight than the

7. *Why is the banking system much more heavily regulated than other areas of the economy?

(LO3)

Answer: The banking system, by its nature, is fragile, and banks play a crucial role in the

prevent bank managers from assuming excessive risk.

8. *Explain why, in seeking to avoid financial crises, the government’s role as regulator of the

financial system does not imply it should protect individual institutions from failure. (LO2)

Answer: Failure of less competitive, less efficient institutions or firms is part of the

efficiently run institutions.

9. Explain how macro-prudential regulations work to limit systemic risk in the financial system.

(LO3)

Answer: Macro-prudential regulations aim to safeguard the financial system by promoting

better risk management by firms and reducing the financial system’s vulnerability to the

borrowers in lean times. Regulators could also require banks to purchase catastrophe

insurance that would replenish its capital in times of crisis.

10. Why were runs during the financial crisis of 2007-2009 not limited to institutions with large

exposures to sub-prime mortgage lending? (LO1)

Answer: Banks and shadow banks are highly interconnected with one another and so

11. Suppose you have two deposits totaling $280,000 with a bank that has just been declared

insolvent. Would you prefer that the FDIC resolve the insolvency under the payoff method

or the purchase-and-assumption method? Explain your choice. (LO2)

Answer: You would prefer the purchase and assumption method, because under the payoff

method, you would lose any funds above the insurance limit. Currently, the limit is

ownership and depositors would not suffer a loss.

12. *How might the existence of the government safety net lead to increased concentration in the

banking industry? (LO2)

Answer: In an effort to avoid financial crisis, large institutions realize that the government

to an increase in concentration.

13. One goal of the Dodd-Frank Wall Street reform is to end the too-big-to-fail problem. How

does it propose to do so? Why might it fail? (LO3)

Answer: The government’s implicit willingness to bail out the creditors of a large

constrains Fed lending to individual nonbanks, limits the FDIC’s guarantee powers, subjects

large institutions to regular “stress tests,” requires systemically important financial

continued access to relatively low funding costs.

14. A government can overcome the challenge of time consistency only if it is both able and

procedures for bankruptcy affect the too-big-to-fail problem? (LO2)

Existing bankruptcy procedures are not designed for the speedy resolution of large, complex

financial intermediaries like SIFIs. If these procedures impede creditors from using their

would diminish SIFIs’ incentives to pursue risky strategies, making the financial system as a

whole less vulnerable. For these reasons, legal scholars and experts are exploring the creation

of a special U.S. bankruptcy code (sometimes called “Chapter 14”) for large intermediaries.

15. If banks’ fragility arises from the fact that they provide liquidity to depositors, as a bank

manager, how might you reduce the fragility of your institution? (LO1)

Answer: You could reduce the risk of large-scale unexpected withdrawals by increasing the

portion of assets in the form of liquid securities that could be sold easily to meet withdrawals.

16. *Why do you think bank managers are not always willing to pursue strategies to reduce the

fragility of their institutions? (LO1)

Answer: In Problem 16, we identified ways to reduce a bank’s vulnerability to sudden

reserves or liquid assets that pay relatively low rates of interest are also likely to reduce profit

margins.

17. Regulators have traditionally required banks to maintain capital-asset ratios of a certain level

balance sheet. Why might such capital adequacy requirements not be effective? (LO3)

Answer: The importance of off-balance sheet activities of banks has been increasing and the

high ratings and thus lowered the banks’ risk-weighted capital requirements.

18. You are the lender of last resort and an institution approaches you for a loan. You assess that

deposits and is requesting a loan to tide it over. Would you grant the loan? (LO2)

Answer: Based on the information given, you should grant the loan. The institution has

institution from failing.

19. You are a bank examiner and have concerns that the bank you are examining may have a

What do you think might be going on and what should you do about it? (LO3)

Answer: This may be a case where the bank has a large portion of non-performing loans.

and which should be written off and to assess the impact on the solvency of the institution.

20. In the period since the financial crisis of 2007-2009, several countries experienced very low

concern to someone managing a bank? (LO1)

Answer: Deflation is associated with falling net worth of borrowers, as the nominal value of

of the bank’s balance sheet and may eventually lead to insolvency.

Data Exploration

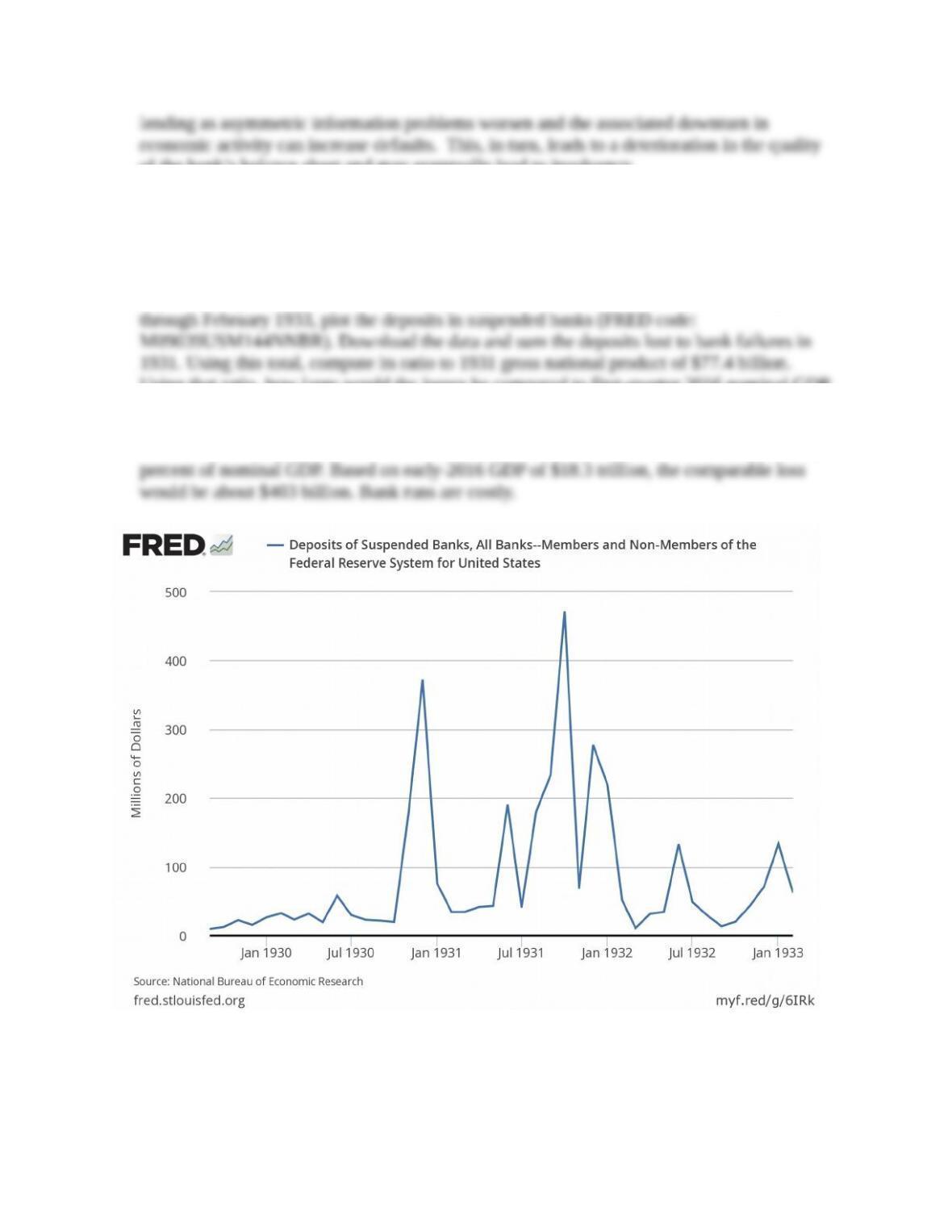

1. When banks failed in the 1929-1933 period, the lack of deposit insurance meant that

depositors experienced sizable losses. How big were these losses? For September 1929

Using that ratio, how large would the losses be compared to first-quarter 2016 nominal GDP

of $18.3 trillion. (LO1)

Answer: The data plot is below. In 1931, the cumulative loss was $1,690 million, about 2.2

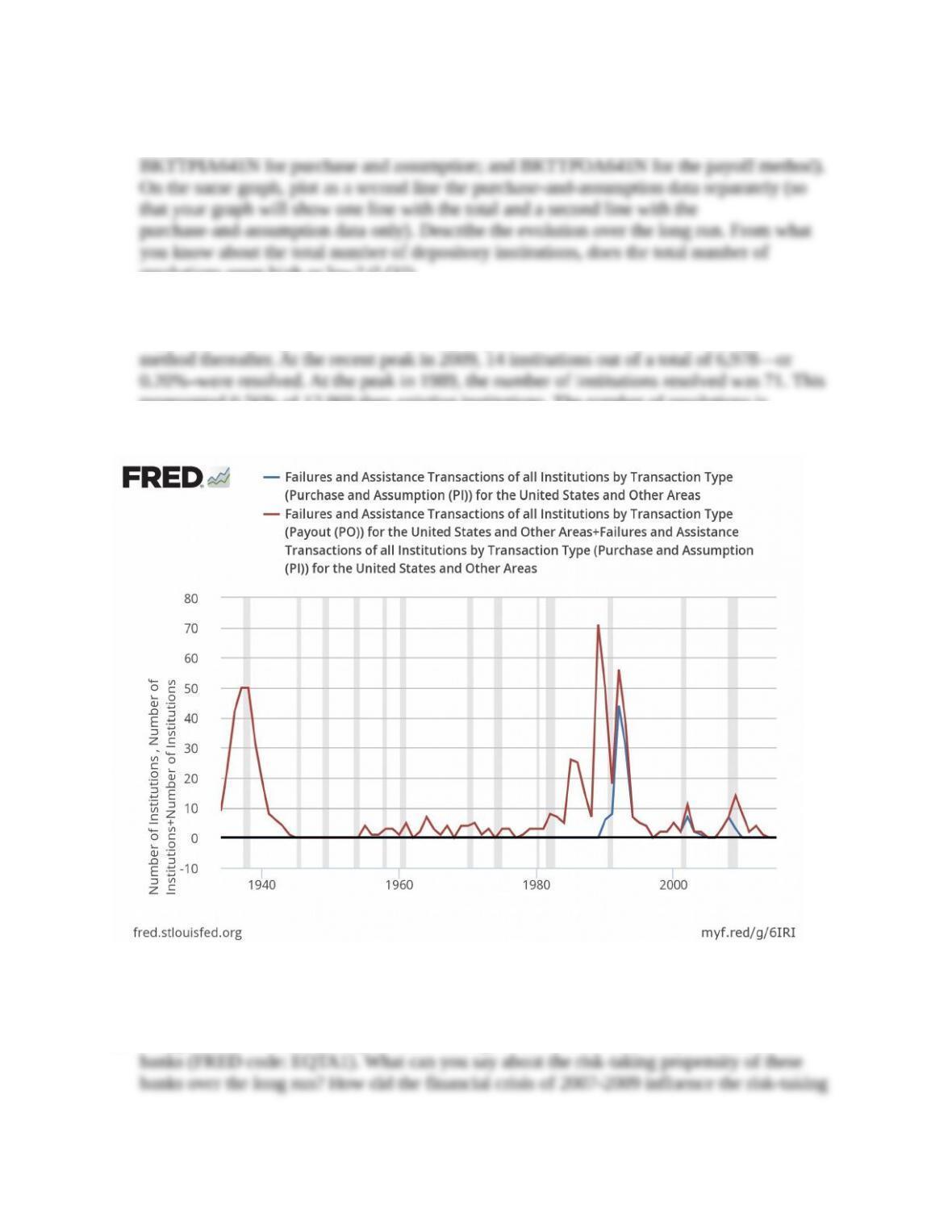

2. How frequently are the payoff and the purchase-and-assumption methods used by the FDIC?

Using FRED, plot the total number of institutions receiving such assistance (FRED codes:

resolutions seem high or low? (LO2)

Answer: Until the late 1980s, the payoff method was used to restore the balances to

depositors at failing banks. The FDIC only began to use the purchase-and-assumption

represented 0.56% of 12,869 then-existing institutions. The number of resolutions is

relatively low.

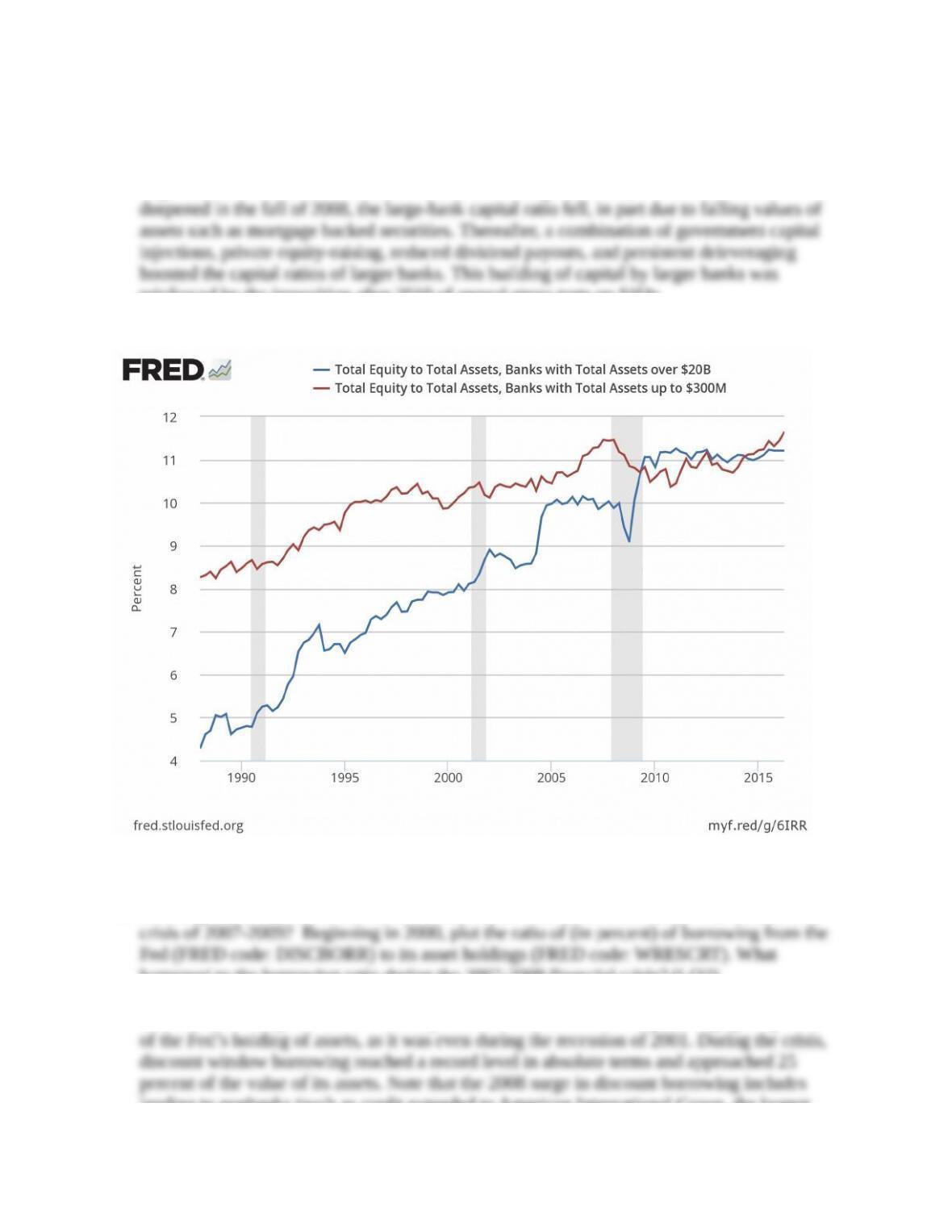

3. Using FRED, examine the capital ratios of large banks (FRED code: EQTA5) and small

behavior of large banks? (LO3)

Answer: Historically, small banks have had higher capital ratios than large banks. That is,

large banks have been more inclined to take on leverage (and risk). As the final crisis

reinforced by the imposition after 2010 of annual stress tests on SIFIs.

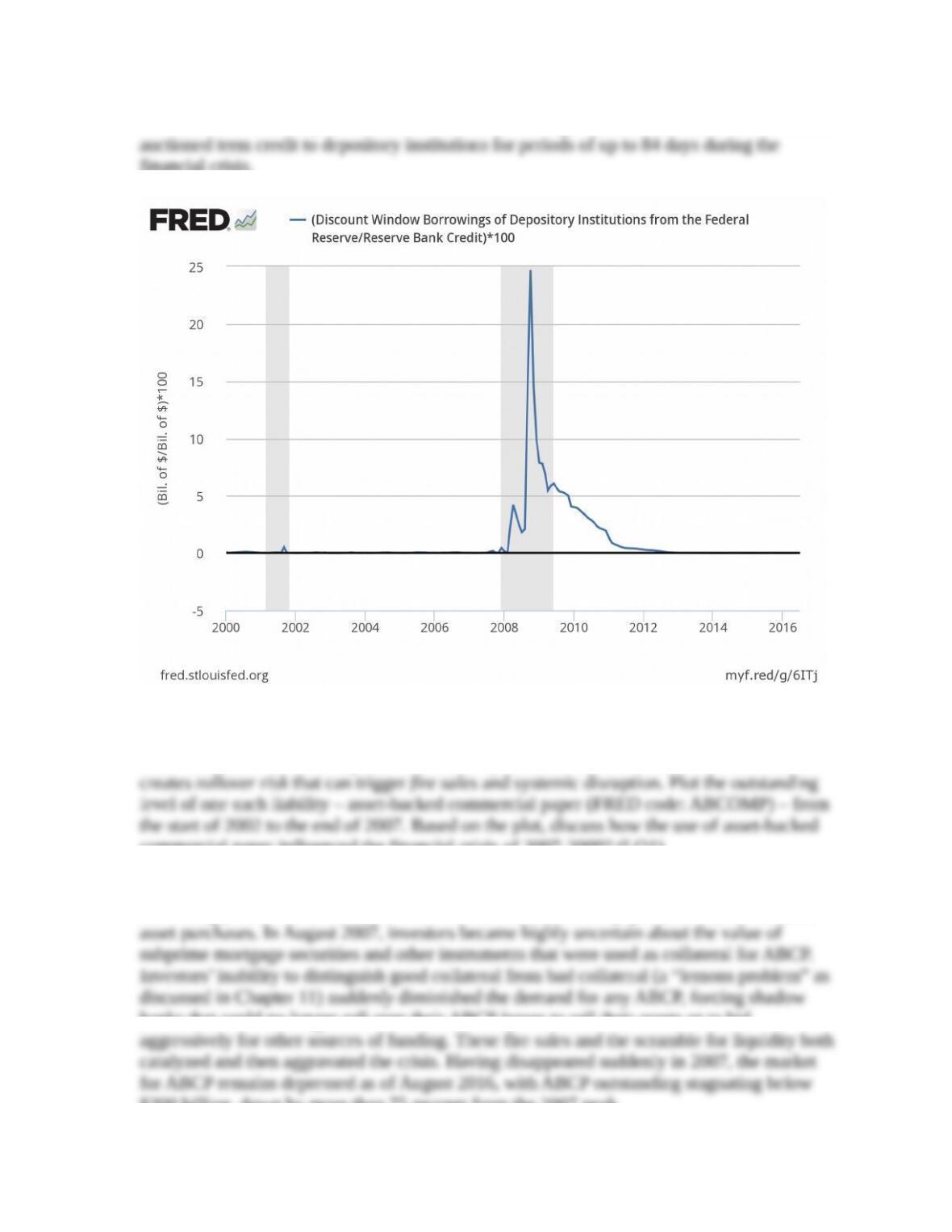

4. How important was the lender-of-last-resort function of the Federal Reserve in the financial

happened to the borrowing ratio during the 2007-2009 financial crisis? (LO2)

Answer: The data plot is below. Usually, discount window borrowing is a negligible portion

lending to nonbanks (such as credit extended to American International Group, the largest

U.S. insurer at the time). In addition to these loans through the discount window, the Fed also

financial crisis.

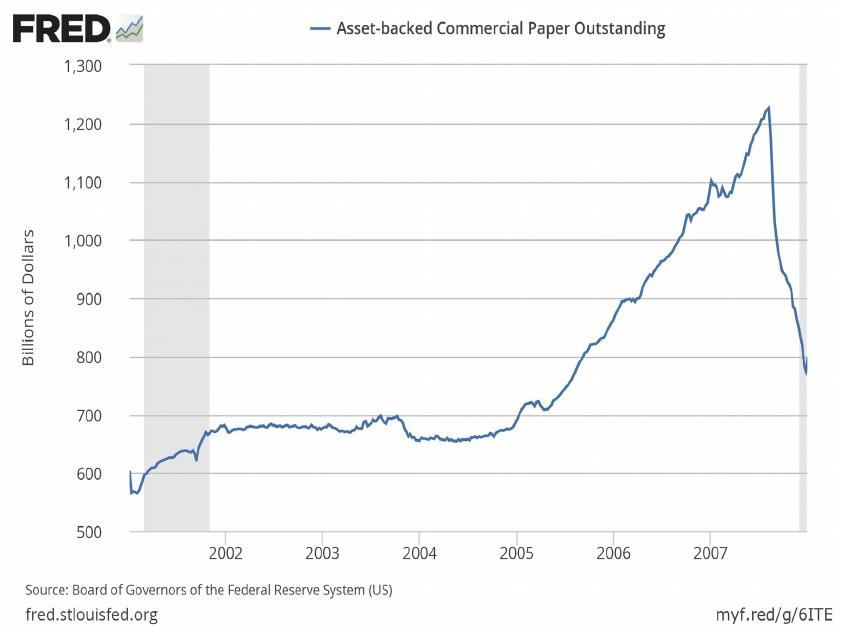

5. Shadow banks typically fund their assets by issuing liabilities of shorter maturity that are

close substitutes for bank deposits. The maturity mismatch between their assets and liabilities

commercial paper influenced the financial crisis of 2007-2009? (LO1)

Answer: The plot appears below. From 2005 to the summer of 2007, shadow banks

increasingly relied on the issuance of asset-backed commercial paper (ABCP) to fund their

banks that could no longer roll over their ABCP issues to sell their assets or to bid

$300 billion, down by more than 75 percent from the 2007 peak.

* indicates more difficult problems