Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Case 3 Teaching Note Amazon.com’s Business Model and Its Evolution

8

3. What does a competitive strength assessment reveal about Amazon’s e-commerce business,

as compared to the leaders in the discount retail industry? Use the methodology in Table 4.3

to support your answer.

Students should be able to prepare a competitive strength assessment for the major discount retailers.

Although the students’ strength measures, respective weightings, and ratings may vary, conclusions should

be consistent with Table 1.

TABLE 1. Competitive Strength Assessment for the Leading Rivals in the Discount Retail Industry

Rating Scale: 1 = very weak; 10 = very strong

Key Success Factors/

Strength Measures

Importance/

Weight

Amazon Walmart Costco

Rating

Weighted

Score Rating

Weighted

Score Rating

Weighted

Score

Customer service 0.20 81.60 61.20 61.20

Wide selection 0.10 90.90 80.80 70.70

Convenience 0.20 91.80 61.20 71.40

The table above indicates that Amazon is the strongest player in the discount retail market space, which

is supported by the market capitalization statistics presented in case Exhibit 1. Amazon’s competitive

strength is primarily a function of its superior customer service, distribution, and reputation for having a

wide selection of products and a convenient ordering system. Students are likely argue either way regarding

Amazon’s rating with respect to “low price,” as the case presents differing points of view on this category.

4. Does it appear that the company’s competitive positions in personal media players and

digital streaming are stronger or weaker than its position in e-commerce and cloud-based

computing services? What steps should it take to ensure that the digitally streamed media—

and mobile platforms to access that media—become a major contributor to the company’s

overall performance?

Based on the analyses above and a careful reading of the case, it should be quite obvious that Amazon is a

late entrant into the mobile device and digital streaming markets. Unlike Apple or Google, Amazon has not

yet enjoyed any experience curve benefits of being a late entrant into mobile phones, tablets, or streaming

Case 3 Teaching Note Amazon.com’s Business Model and Its Evolution

9

media. There was no apparent direct linkage between those devices and its e-commerce platform, nor is

proprietary software required for capturing the streaming content on those devices (or on any of its rivals’

devices, for that matter).

A good argument could thus be made for Amazon to entirely exit (or at least reduce its investments in) per-

sonal media players and other electronic devices such as the Fire TV or Amazon Dash that are not essential

to access the company’s commerce or web services ecosystems. The case states that, “in the third quarter of

5. Does it make good strategic sense for Amazon to be a competitor in the e-commerce,

cloud-based computing services, and personal media device industries? Which of its three

principal product lines—e-commerce, cloud computing services, personal media players—

do you think is most important to Amazon’s future growth and profitability? Why? Should

any of the product lines be discontinued?

Amazon has become the most disruptive force to emerge in retail in several decades. Its low-cost operations,

network effect, and laser focus on customer service provide it with sustainable competitive advantages that

traditional retailers cannot match; this should yield additional market share gains in the years to come.

So, the answer is yes and no, it does make good strategic sense for Amazon to remain a competitor in

the e-commerce and cloud-based computing services businesses, while the personal media player business

remains a strong question mark or perhaps even a candidate for divestment.

nOne of Amazon’s key advantages is its low-cost operations.

The cost to maintain its scalable fulfillment and distribution network is lower than having a large physical

retail presence, allowing Amazon to price below its brick-and-mortar peers while still generating excess

economic returns. Additionally, U.S. tax laws currently mandate that online retailers collect sales tax

in states where they have a physical presence, with the tax responsibility falling to the end consumers

themselves. As a result, Amazon currently collects sales tax in states where it maintains a physical

Case 3 Teaching Note Amazon.com’s Business Model and Its Evolution

10

nDespite ongoing large R&D investments in fulfillment, technology (hardware devices and AWS),

and content, we expect Amazon to continue generating positive cash flows, if not profits, for the

foreseeable future.

The shine may long be off its initial 2006 launch of the Kindle, which resulted in half a million devices

sold, and although the Fire Phone and Kindle Fire and other devices have met with limited market

acceptance to date, so Amazon should strongly consider abandoning the OEM business as it offsets

any profits from the current fulfillment and content streaming businesses that remain in high growth

markets.

6. What is your assessment of Amazon’s financial performance the past three years? (Use the

financial ratios in the Appendix of the text as a guide in doing your financial analysis.)

Students should be able to use the financial information provided in case Exhibit 3 and the financial ratios

provided in the Appendix of the text to make calculations similar to those shown in Table 2.

TABLE 2. Selected Financial Statistics and Ratios for Amazon Inc., 2010 – 2014

n/a = not applicable or impossible to calculate.

Performance Ratios 2014 2013 2012 2011 2010

Net sales growth % 19.5% 21.9% 27.1% 40.6% n/a

Sales growth, products % 15.1% 17.7% 23.2% 36.4% n/a

Sales growth, services % 39.6% 44.8% 54.0% 78.1% n/a

Gross margin, % 29.5% 27.2% 24.8% 22.4% 22.3%

Case 3 Teaching Note Amazon.com’s Business Model and Its Evolution

11

Students are likely to suggest that that the strength of Amazon’s strategy and products allowed it to withstand

the effects of the recession much easier than competing bricks-and-mortar retailers.

Students should quickly recognize that, although Amazon’s performance between 2010 and 2011 had been

exceptionally strong with net sales revenues growing by 41%, the growth rate in that category weakened

considerably in the succeeding years out to 2014. For purposes of comparison, revenue growth in services

remained robust relative to revenue growth in products during that four-year period. As a result, gross mar-

gins widened considerably, from 22% to nearly 30%.

7. What strategic issues confront Amazon in 2015? What market or internal circumstances

should most concern Je Bezos and the company’s senior leadership team?

We think it is always a good idea to push the class for their assessment of what issues management needs

to address before proceeding to ask for action recommendations. Issue identification (or compilation of a

“what I’d do if I were in her/his shoes” list) is a way for students to draw conclusions from all the preceding

analyses, plus it sets the stage for what actions need to be taken.

In Amazon’s case, we see several high-priority issues meriting priority consideration:

nHow best to sustain long-term growth and profitability

nDespite apparent reductions in general and administrative overhead, how to stem the declines in

operating profit as a percentage of total revenues

Case 3 Teaching Note Amazon.com’s Business Model and Its Evolution

12

8. What recommendations would you make to Amazon to address the strategic issues confron-

ting it in 2015 and sustain its impressive growth in revenues and maintain its profitability?

Although the major societal trends towards replacement of analogue media by digital media and the

replacement of computers by larger-format smart phones are likely to continue unabated, Amazon

must be more selective with its capital allocation into any OEM personal devices.

nThat is, we believe the lack of consumer interest in the Fire Phone was a wakeup call for management’s

future capital decisions, as the company runs the risk of losing key personnel without stronger returns

on invested capital, owing to the equity component of many employees’ compensation structure.

However, the company should continue on its recent path with respect to acquisitions and investments in

fulfillment and streaming content.

nThese investments have been more directly aligned with Amazon’s stable growth core e-commerce and

higher growth AWS platforms.

TABLE 3. Selected Strategic Options for Amazon Inc.

Option Pros Cons

Continue Preserves entrepreneurial can-do spirit, company

culture, and investments in information technology

and operating systems

Rival firms such as Google or Facebook

may catch Amazon by developing similar

or stronger data analytics, customer

service & IT capabilities

Expand via JV

or acquisition

Could involve strategic alliance with — or acquisition

of — a large social media company with billions

of users e.g. Facebook or Snapchat or LinkedIn,

it may be able to achieve economies of scope

Requires massive amounts of capital &

cooperation to achieve

Potential dilution of ownership & control

Potential diminution of customer service &

Case 3 Teaching Note Amazon.com’s Business Model and Its Evolution

13

Wrapping Up The Class

The Amazon case can provide instructors with an important “bridge” to strategy execution concepts covered in

later chapters, or it can even be paired with those chapters. We would encourage you to conclude by foreshadowing

the material in those chapters and by making the following points:

nDisruptive companies like Amazon that have superior competitive strength in one or two arenas—

such as e-commerce or web service—typically have prioritized a few key success factors (KSF) that

are necessary for industry dominance: (covered in Chapter 5):

• Develop a capability and a corporate culture to support superior customer service

• Make massive investments in logistics and fulfillment, often to the detriment of profits

• Adopt a virtuous circle that puts customers at the center, via a friendly, easy-to-use interface and policies

that reward rather than punish customers

nAmazon’s high performance, innovative culture is an excellent example of how companies get an

important boost from a culture that promotes superior strategy execution and operating excellence:

(covered in Chapter 12)

• Company strategies cannot be executed well unless you have inculcated a culture like Amazon’s, that is,

one highly conducive to adaptation and change.

• Strategy-supportive cultures like Amazon’s not only enable better execution, but also strengthen organi-

zational capabilities, enough, in certain industries at least, to provide a substantial competitive edge over

rivals

Case 3 Teaching Note Amazon.com’s Business Model and Its Evolution

14

Epilogue

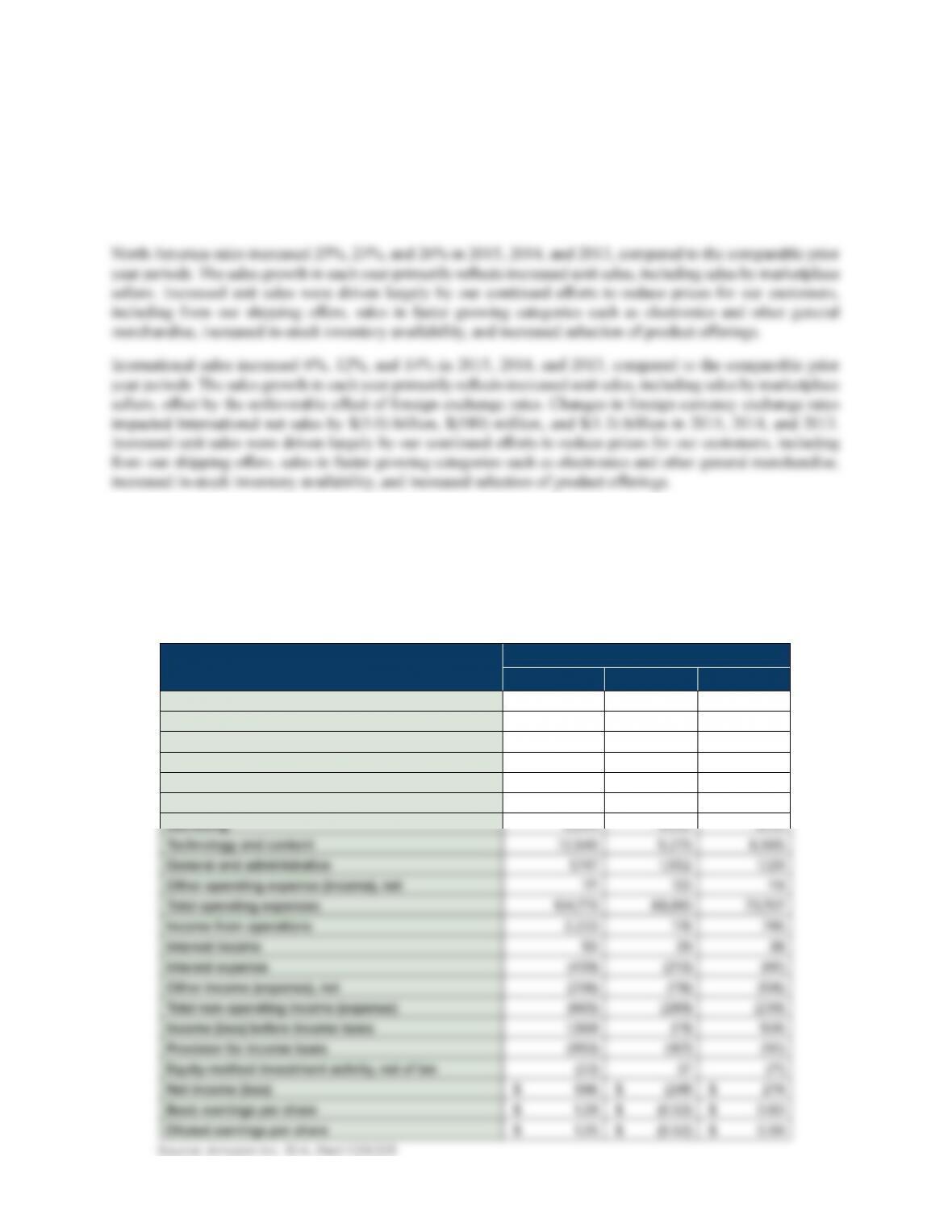

Sales increased 20%, 20%, and 22% in 2015, 2014, and 2013, compared to the comparable prior year periods.

Changes in foreign currency exchange rates impacted net sales by $(5.2) billion, $(636) million, and $(1.3)

billion for 2015, 2014, and 2013. For a discussion of the effect on sales growth of foreign exchange rates, see

“Effect of Foreign Exchange Rates” below.

AWS sales increased 70%, 49%, and 69% in 2015, 2014, and 2013, compared to the comparable prior year

periods. The sales growth primarily reflects increased customer usage, partially offset by pricing changes. Pricing

changes were driven largely by our continued efforts to reduce prices for our customers.

AMAZON.COM, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS, 2013 – 2015

(in millions, except per share data)

Year Ended December 31

2015 2014 2013

Net product sales $79,268 $70,080 $60,903

Net service sales 27,738 18,908 13,549

Total net sales 107,006 88,988 74,452

Operating expenses:

Cost of sales 71,651 62,752 54,181

Fulfillment 13,410 10,766 8,585