Case 21 Teaching Note Mondelēz International

8

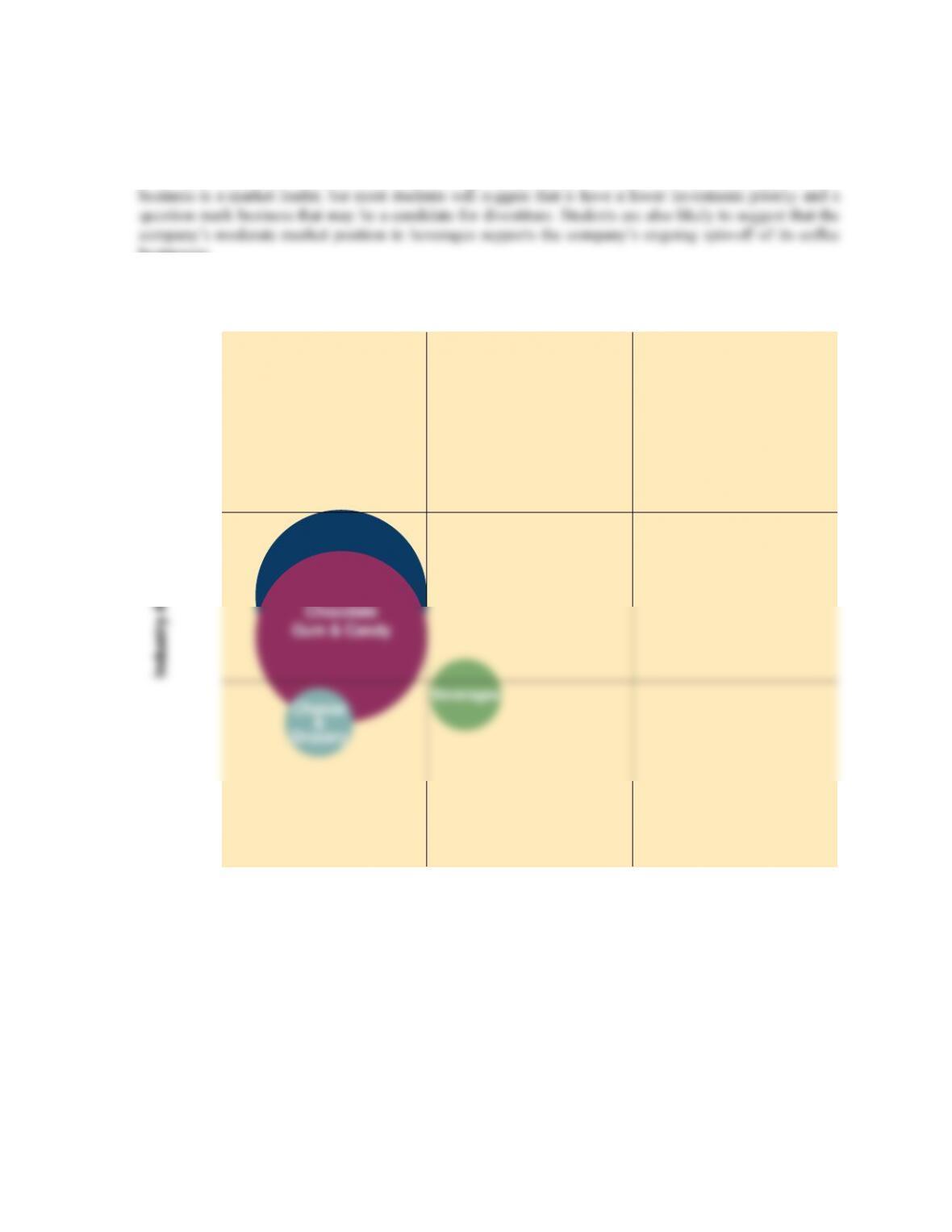

The 9-cell GE-style matrix analysis (Figure 1) indicates that Mondelēz International’s all compete in mature

industries and require modest reinvestments in the form of capital expenditures for new plant capacity.

However, the company’s Biscuits and Chocolate, Gum & Candy businesses are market leaders and continue

to be “grow and build” businesses that should be given a priority for investment. The Philadelphia cheese

businesses.

FIGURE 1. Sample Industry Attractiveness/Competitive Strength Matrix of Mondelēz

International’s Businesses

Beverages

Low

Business Strength

High

High

Low

Cheese

&

Grocery

Chocolate

Gum & Candy

Biscuits

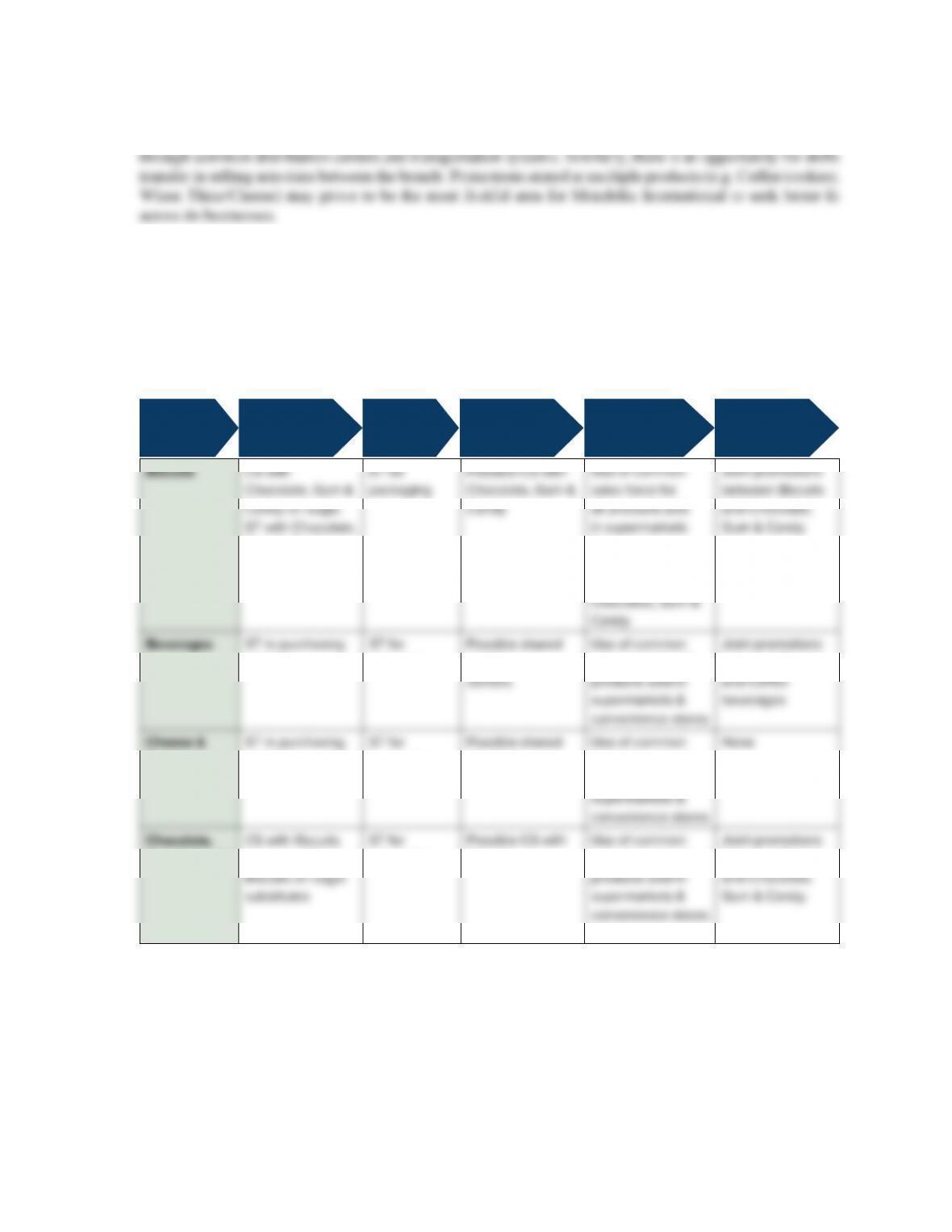

5. Does Mondelēz International’s portfolio exhibit good strategic fit? What value-chain match-

ups do you see? What opportunities for skills transfer, cost sharing, or brand sharing do you

see?

Students may initially suggest that substantial cost sharing opportunities exist between Mondelēz

International’s various businesses, but as was pointed out in the discussion to question 1 few such

opportunities exist beyond cross-selling and joint promotional activities. The purchasing and manufacture

of cheese, cookies, beverages, and gum are very different. The dissimilarity even limits cost sharing of

distribution of many of the brands produced by Mondelēz International.

Case 21 Teaching Note Mondelēz International

9

Perhaps the strongest strategic fit between businesses in Mondelēz International’s stable existed by geographic

distribution rather than business type. For the most part, Mondelēz International could distribute its products

Figure 2 provides a list of cost sharing, skills transfer, and brand sharing opportunities along the value chains

of Mondelēz International’s business units.

FIGURE 2. Assessment of Strategic Fit Potentials Between Mondelēz International’s Business

Units

CS = cost sharing benefits ST = skills transfer opportunities

Value Chain Activities

Business Unit Purchasing Operations Distribution Sales & Marketing Advertising/

Promotion

Gum & Candy on

sugar substitutes

& convenience

stores; Cross

selling with

activities.

packaging

distribution

sales force for all

between Biscuits

Grocery

activities.

packaging

distribution

centers

sales force for all

products sold in

Gum & Candy

on sugar. ST with

packaging

Biscuits

sales force for all

stores

between Biscuits

6. What is your overall evaluation of Mondelēz International’s corporate strategy and

restructuring since 2012? What evidence and/or reasons support a conclusion that

Mondelēz International’s shareholders have benefitted from the spino of the company’s

North American grocery business?

Students may be divided over the effectiveness of Mondelēz International’s corporate strategy with those

who are more enthusiastic pointing to the company’s 7 $1 billion brands. Students point out that it seems

hard to fault businesses that are number 1 in their respective markets just because the industries they are

mature.

Case 21 Teaching Note Mondelēz International

10

A review of the company’s financial performance since the spinoff of Kraft Foods slower growth businesses

should lead students to the conclusion that the focus on snack brands has done little to bring about sustained

growth in shareholder value.

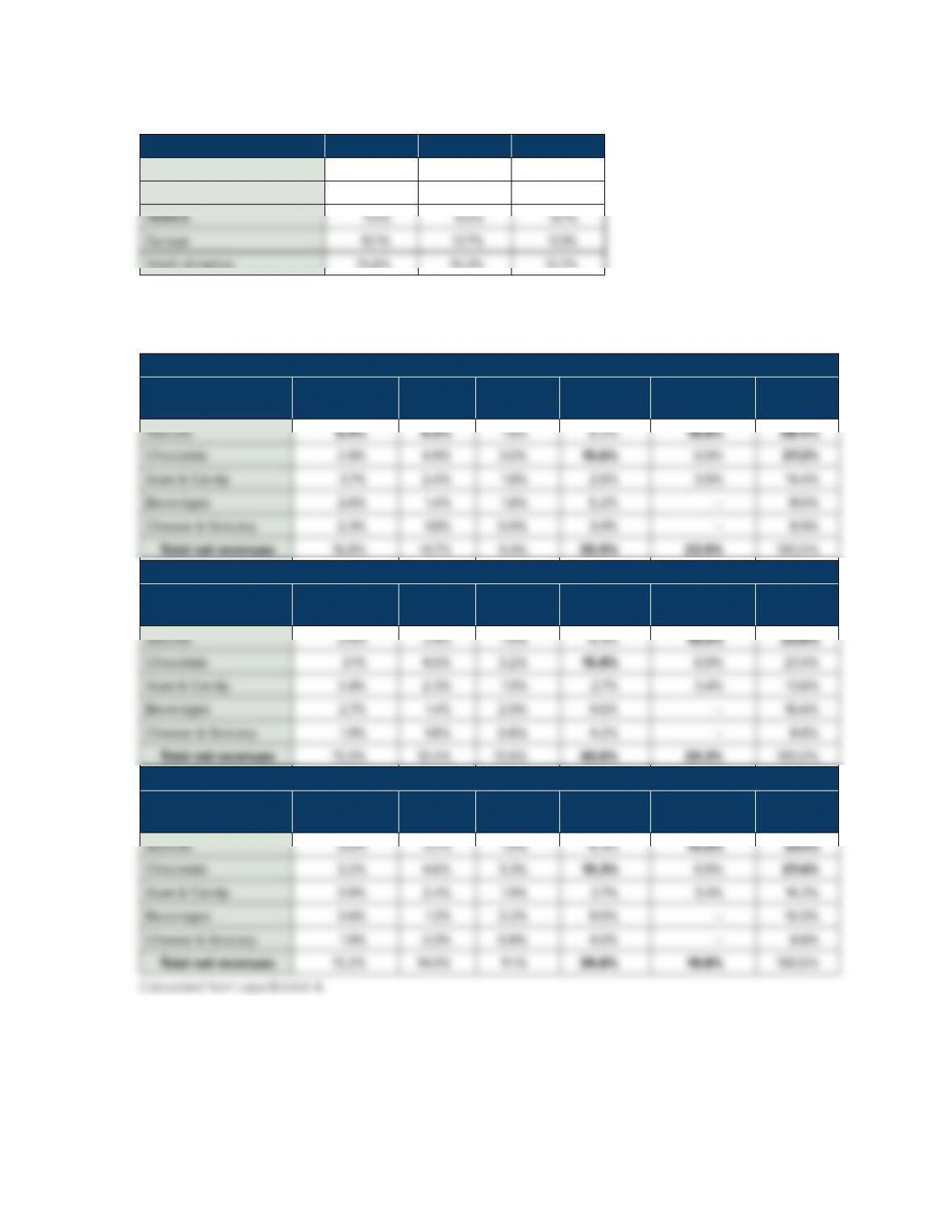

Table 4 below shows that while of Mondelēz International management has been effective in boosting gross

Students should conclude that the general direction of the company’s profitability ratios signals a weak or

awed corporate level strategy.

TABLE 4. Select Financial Ratios for Mondelēz International, 2013-2015

2015 2015* 2014 2013

Gross profit margin 38.8% 38.8% 36.8% 37.1%

2015* Excluding extraordinary items

n.a. Not available

Calculated from case Exhibits 5 and 6.

A review of operating profit margins by geographic region should allow students to recognize that the

company’s North American and European operations comprise a sizeable portion of the company’s operating

income, even though sales in other international markets are increasing. Case Exhibit 3 and Table 5 indicates

that the company’s operations outside North America and Europe are struggling and contribute little to

shareholder value. Some students may recognize that price increases bore by consumers in North America

and Europe are critical to any stability in profitability at the company. Eventual resistance to price increases

by North American and European consumers will threaten of Mondelēz International’s margins.

A review of the company’s revenue contribution by product category and geographic region should allow

students to develop a keener understanding of the drivers of shareholder value at of Mondelēz International.

Table 6 indicates that chocolate sales in Europe and snack or biscuit sales in North America are the major

Case 21 Teaching Note Mondelēz International

11

TABLE 5. Operating Margins by Mondelēz International Geographic Segment, 2013 – 2015

2015 2014 2013

Latin America 9.7% 9.2% 10.6%

Asia Pacific 6.1% 8.4% 10.3%

North America 15.8% 13.3% 12.7%

Calculated from case Exhibit 3.

TABLE 6. Revenue Contribution by Mondelēz International Product Category and Geographic

Region, 2013 – 2015

2015

Latin

America

Asia

Pacific EEMEA Europe

North

America Total

2014

Latin

America

Asia

Pacific EEMEA Europe

North

America Total

2013

Latin

America

Asia

Pacific EEMEA Europe

North

America Total

Case 21 Teaching Note Mondelēz International

12

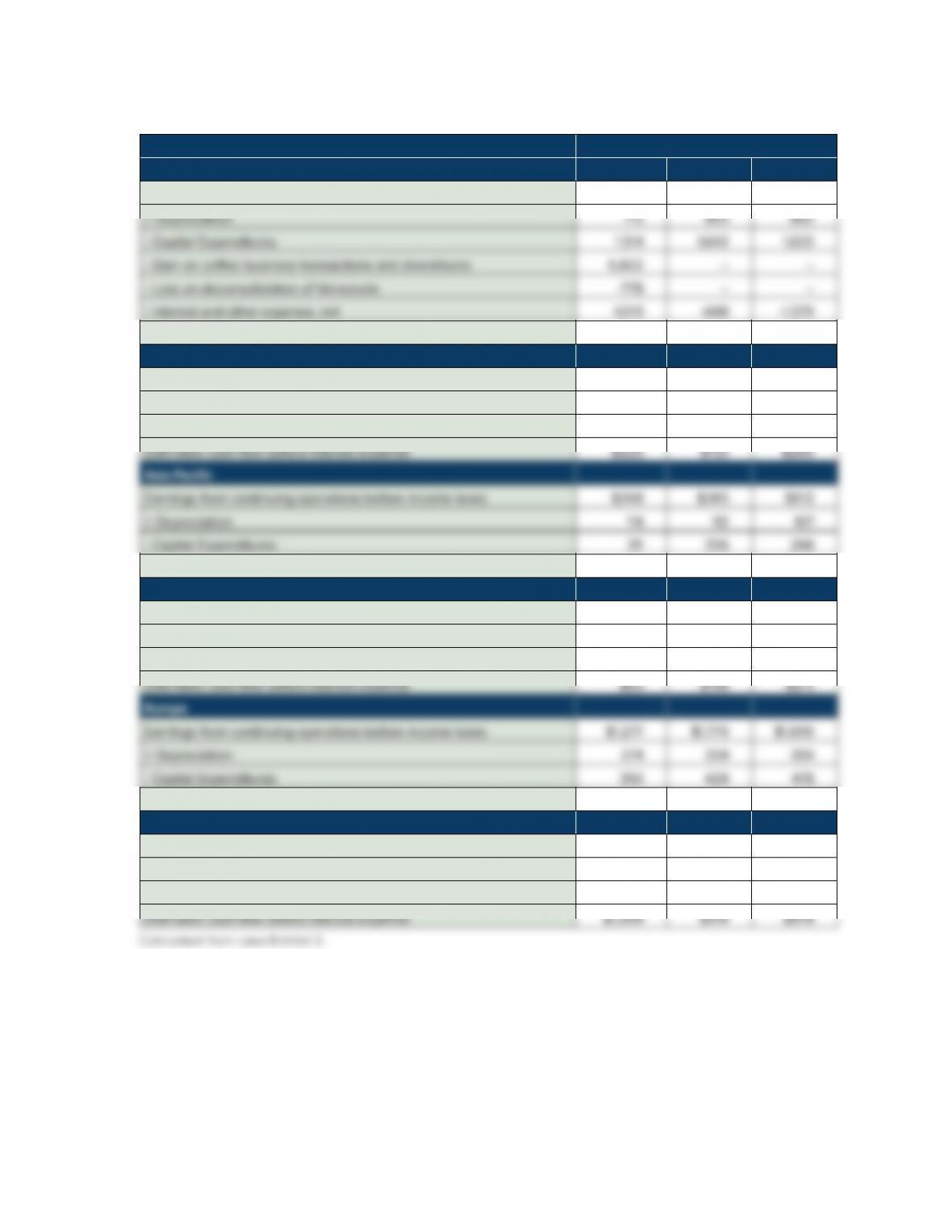

TABLE 7. Estimated Cash Flow by Mondelēz International Geographic Region, 2013 – 2015

Estimated Cash Flow

Companywide 2015 2014 2013

Earnings from continuing operations before income taxes $7,884 $2,554 $2,392

Estimated cash flow from continuing operations $26 $1,077 $51

Latin America

Earnings from continuing operations before income taxes $485 $475 $570

+ Depreciation 94 118 107

– Capital Expenditures 354 460 412

Estimated cash flow before interest expense $71 $141 $351

EEMEA

Earnings from continuing operations before income taxes $194 $327 $379

+ Depreciation 66 90 88

– Capital Expenditures 197 219 254

Estimated cash flow before interest expense $1,161 $1,700 $1,580

North America

Earnings from continuing operations before income taxes $1,105 $922 $889

+ Depreciation 165 174 199

– Capital Expenditures 262 178 210

Case 21 Teaching Note Mondelēz International

13

7. What actions do you recommend that Mondelēz International management take to improve

the company’s performance and boost shareholder value? Your recommended actions must

be supported with convincing, analysis-based arguments.

Students should identify the following challenges to increasing shareholder value at Mondelēz International.

Business lineup overreliance on slow growth product categories

Declining sales in core chocolate business

Student recommendations to improve the company’s performance should address the strategic issues listed

above and may include some of the following points.

Mondelēz International faces threats from industry maturity which may be linked to health concerns

(obesity) for many of its brands. Students are likely to suggest that the company develop healthier

formulations of its products and seek out acquisitions in healthy snack categories. The company’s

restructuring and continued focus on snack foods and chocolates has failed to bring about increases in

shareholder value. Mondelēz International must move into star product categories that offer stronger

grow and build opportunities that line extensions of its well-known snack brands.

Actions must be taken to reverse the company’s decline in chocolate sales in North America and Europe.

Students are also likely to suggest that the company must discontinue its reliance on price increases paid

The company’s “venerable brands” are dear to aging baby boomers and the company can utilize its

marketing expertise to make these products appealing to younger generations. Similarly, students may

Students are also likely to recommend that the company develop new strategic approaches in developing

As was discussed in the answers to Question 5 above, the key to unlocking value in mature markets is

finding synergies across the various holdings of the company. Otherwise, the parent company is just a

Case 21 Teaching Note Mondelēz International

14

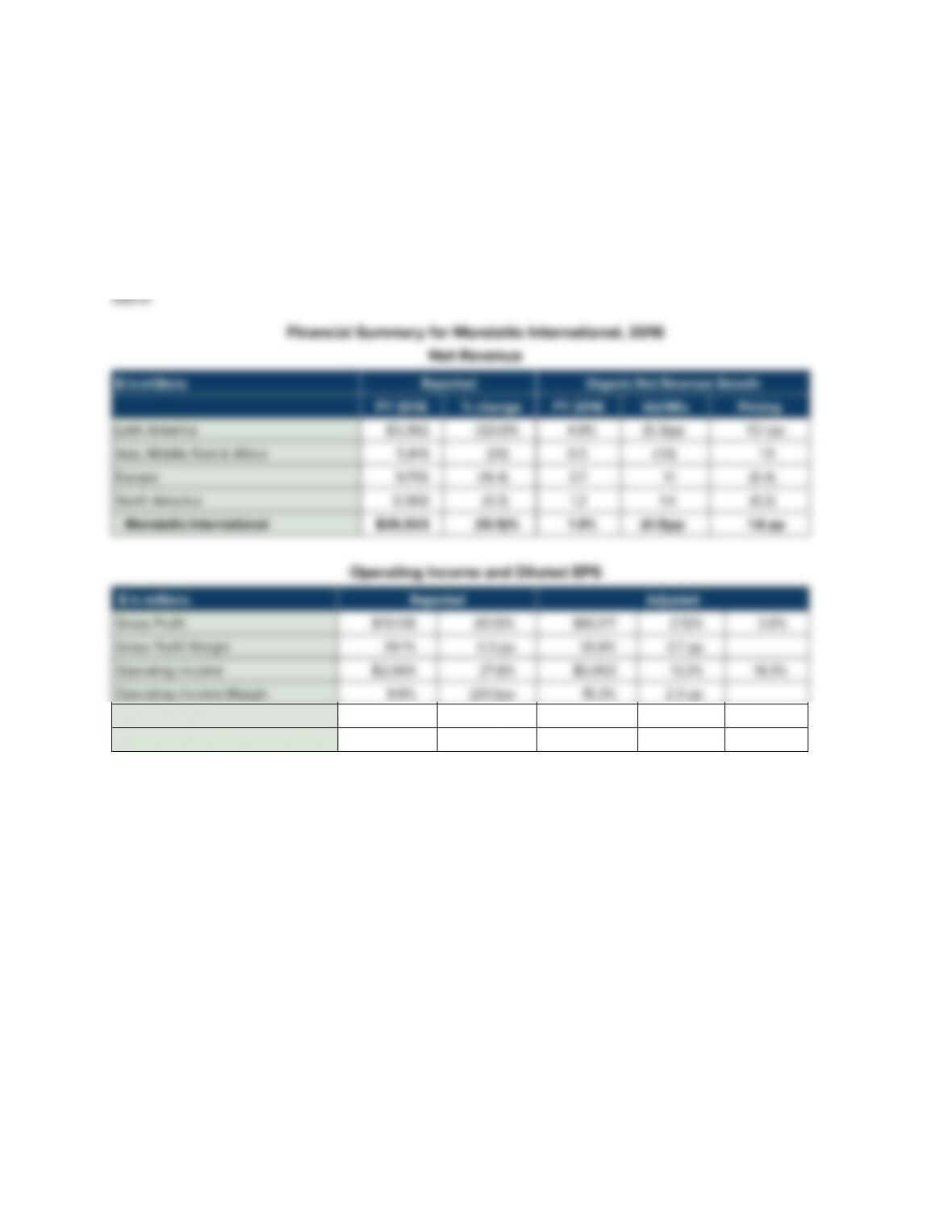

Epilogue

Mondelēz International’s poor financial performance continued through year-end 2016 with revenues declining

by 12.5 percent from year-end 2015 and gross profit declining by 12 percent between 2015 and 2016. The

company’s operating profit margin and EPS declined by 20.1 percent and 76 percent, respectively, between 2015

and 2016. Much of the decreases in profit indicators was a result of the effect of extraordinary items in 2016, but

the company’s organic net revenues declined overall with the greatest declines occurring in Latin America. The

company reported that adjusted operating income and net income increased by 13.3 percent and 14.9 percent,

respectively between 2015 and 2016. A summary of the company’s 2016 financial performance is presented

Net Earnings $1,659 (77.2)% $3,046 14.9% 19.0%

Diluted EPS $1.05 (76.4)% $1.94 19.8% 24.1%

Source: “Mondelēz International Reports 2016 Results,” Global Newswire, February 7, 2017.