Chapter 36 – Interest Rates and Monetary Policy

36-1

Chapter 36 – Interest Rates and Monetary Policy

McConnell Brue Flynn 21e

DISCUSSION QUESTIONS

1. What is the basic determinant of (a) the transactions demand and (b) the asset demand for

money? Explain how these two demands can be combined graphically to determine total money

demand. How is the equilibrium interest rate in the money market determined? Use a graph to

show the impact of an increase in the total demand for money on the equilibrium interest rate (no

change in money supply). Use your general knowledge of equilibrium prices to explain why the

previous interest rate is no longer sustainable. LO1

Chapter 36 – Interest Rates and Monetary Policy

36-2

2. What is the basic objective of monetary policy? What are the major strengths of monetary

policy? Why is monetary policy easier to conduct than fiscal policy? LO3

3. Distinguish between the federal funds rate and the prime interest rate. Why is one higher than

the other? Why do changes in the two rates closely track one another? LO4

Answer: The Federal funds interest rate is the interest rate banks charge one another on

overnight loans needed to meet the reserve requirement. The prime interest rate is the

interest rate banks charge on loans to their most creditworthy customers.

4. Distinguish between how the Fed would have to undertake restrictive monetary policy today

versus before the mortgage-debt crisis. What actions would it need to take in each case? LO4

Answer: Before 2008, short‐term interest rates were usually in the 3 to 10 percent range

and there was a lot of activity in the federal funds market. If the Fed wished to initiate a

Chapter 36 – Interest Rates and Monetary Policy

36-3

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

inflation.

5. Suppose that you are a member of the Board of Governors of the Federal Reserve System. The

post-2008 economy is experiencing a sharp rise in the inflation rate. What change in the federal

funds rate would you recommend? How would your recommended change get accomplished?

What impact would the actions have on the lending ability of the banking system, the real interest

rate, investment spending, aggregate demand, and inflation? LO5

6. Explain the links between changes in the nation’s money supply, the interest rate, investment

spending, aggregate demand, real GDP, and the price level. LO5

7. What do economists mean when they say that monetary policy can exhibit cyclical asymmetry?

How does the idea of a liquidity trap relate to cyclical asymmetry? Why is this possibility of a

liquidity trap significant to policymakers? LO6

Chapter 36 – Interest Rates and Monetary Policy

36-4

8. LAST WORD By what chain of causation does the ECB think negative interest rates will

stimulate the economy? If the Fed manages to raise interest rates up to historical levels before the

next recession, will it have to consider negative interest rates as a first course of action in terms of

stimulating the economy? Explain.

Answer: Starting in 2014, the ECB had set negative interest rates. By March 2016, the

ECB had set its version of the federal funds rate at negative 0.4 percent for the Eurozone

REVIEW QUESTIONS

1. When bond prices go up, interest rates go_______ . LO1

a. Up.

b. Down.

c. Nowhere.

Chapter 36 – Interest Rates and Monetary Policy

36-5

2. A commercial bank sells a Treasury bond to the Federal Reserve for $100,000. The money

supply: LO3

a. Increases by $100,000.

b. Decreases by $100,000.

c. Is unaffected by the transaction.

3. Use commercial bank and Federal Reserve Bank balance sheets to demonstrate the effect of

each of the following transactions on commercial bank reserves: LO3

a. Federal Reserve Banks purchase securities from banks.

b. Commercial banks borrow from Federal Reserve Banks at the discount rate.

c. The Fed reduces the reserve ratio.

d. Commercial banks increase their reserves after the Fed increases the interest rate that it pays on

reserves.

Chapter 36 – Interest Rates and Monetary Policy

36-6

Consolidated Balance Sheet: 12 Federal Reserve Banks

A

B

C

Assets:

Securities

$283

$

285

$

283

$

283

Loans to commercial banks

2

2

3

2

Liabilities and net worth:

Reserves of commercial banks

40

42

41

40

Treasury deposits

5

5

5

5

Federal Reserve Notes

225

225

225

225

Other liabilities and net worth

15

15

15

15

Feedback: In the tables above, columns A through C show the changes caused by the

answers to the questions. It is assumed the initial reserve ratio is 20 percent. Thus, as the

first column shows, the commercial banks are initially completely loaned up. The

answers are not cumulated: We return to the first column each time to show the resulting

change in columns A, B, or C.

a. It is assumed the Fed buys $2 billion worth of securities. This should increase

commercial bank reserves by $2 billion and reduce securities by $2 billion. This is the

immediate effect to the consolidated balance sheet. With demand deposits of $200

billion, required reserves are $40 billion (= 20 percent of $200 billion). Therefore, excess

reserves are $2 billion (= $42 billion – $40 billion) and the banking system can increase

the money supply (by making loans) by $10 billion more (= $2 billion × 5) in the longer

term.

b. It is assumed the commercial banks borrow $1 billion from the Fed. The immediate

effect to the commercial banks’ consolidated balance sheet is to increase reserves by $1

billion on the asset side and increase loans from the Federal Reserve banks by $1 billion

on the liabilities side. In the longer term, the commercial banks may now increase the

money supply (through making loans) by $5 billion (= $1 billion × 5).

c. Changing the reserve ratio in itself does not change the balance sheets. However, in the

longer term, if we assume the reserve ratio has been decreased from 20 percent to 19

percent, required reserves are now $38 billion (= 19 percent of $200 billion) and the

commercial banks can now increase the money supply (through making loans) by $10.53

billion (= $2 billion × (1/0.19)). Proof: 19 percent of $210.53 billion is $40 billion.

d. Both columns A and B show an increase in commercial bank reserves. However,

column A is the better answer because it shows that the increase in reserves came from

selling securities, whereas the increase in reserves in column B came from loans from the

Federal Reserve Banks. It is unlikely that the Federal Reserve Banks would lend money

to commercial banks at an interest rate lower than the rate the Federal Reserve Banks pay

commercial banks on their reserves. The more likely scenario (which is not shown in the

balance sheets above) is that the commercial banks would increase their reserves by

decreasing loans to their customers.

Chapter 36 – Interest Rates and Monetary Policy

36-7

4. A bank currently has $100,000 in checkable deposits and $15,000 in actual reserves. If the

reserve ratio is 20 percent, the bank has ___________ in money-creating potential. If the reserve

ratio is 14 percent, the bank has ___________ in money-creating potential. LO3

a. $20,000; $14,000.

b. $3,000; $2,100.

c. -$5,000; $1,000.

d. $5,000; $1,000.

Answer: c. – $5,000, $1,000

5. A bank borrows $100,000 from the Fed, leaving a $100,000 Treasury bond on deposit with the

Fed to serve as collateral for the loan. The discount rate that applies to the loan is 4 percent and

the Fed is currently mandating a reserve ratio of 10 percent. How much of the $100,000 borrowed

by the bank must it keep as required reserves? LO3

a. $0.

b. $4,000.

c. $10,000.

d. $100,000.

Chapter 36 – Interest Rates and Monetary Policy

36-8

6. Which of the following Fed actions will increase bank lending? LO3

Select one or more answers from the choices shown.

a. The Fed raises the discount rate from 5 percent to 6 percent.

b. The Fed raises the reserve ratio from 10 percent to 11 percent.

c. The Fed buys $400 million worth of Treasury bonds from commercial banks.

d. The Fed lowers the discount rate from 4 percent to 2 percent.

7. If the Federal Reserve wants to increase the federal funds rate using open-market operations, it

should _____________bonds. LO4

a. Buy.

b. Sell.

Chapter 36 – Interest Rates and Monetary Policy

36-9

8. True or False: A liquidity trap occurs when expansionary monetary policy fails to work

because an increase in bank reserves by the Fed does not lead to an increase in bank lending.

LO6

9. True or False: In the United States, monetary policy has two key advantages over fiscal policy:

(1) isolation from political pressure and (2) speed and flexibility. LO6

Chapter 36 – Interest Rates and Monetary Policy

36-10

PROBLEMS

1. Assume that the following data characterize the hypothetical economy of Trance: money

supply = $200 billion; quantity of money demanded for transactions = $150 billion; quantity of

money demanded as an asset = $10 billion at 12 percent interest, increasing by $10 billion for

each 2-percentage-point fall in the interest rate. LO1

a. What is the equilibrium interest rate in Trance?

b. At the equilibrium interest rate, what are the quantity of money supplied, the total quantity of

money demanded, the amount of money demanded for transactions, and the amount of money

demanded as an asset in Trance?

Chapter 36 – Interest Rates and Monetary Policy

36-11

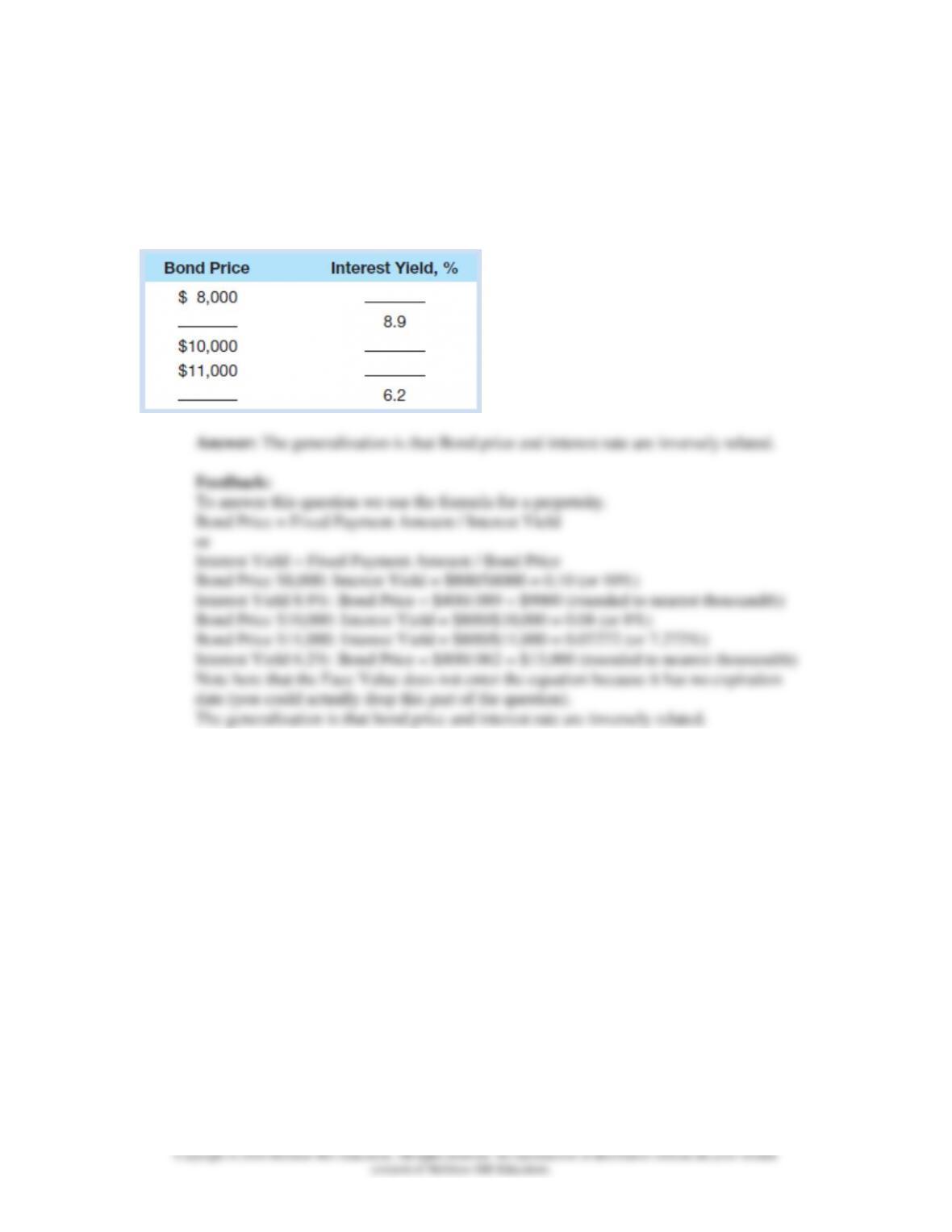

2. Suppose a bond with no expiration date has a face value of $10,000 and annually pays a fixed

amount of interest of $800. In the table provided, calculate and enter either the interest rate that

the bond would yield to a bond buyer at each of the bond prices listed or the bond price at each of

the interest yields shown. Round your answer to the nearest thousandth. What generalization can

be drawn from the completed table? LO1

Chapter 36 – Interest Rates and Monetary Policy

36-12

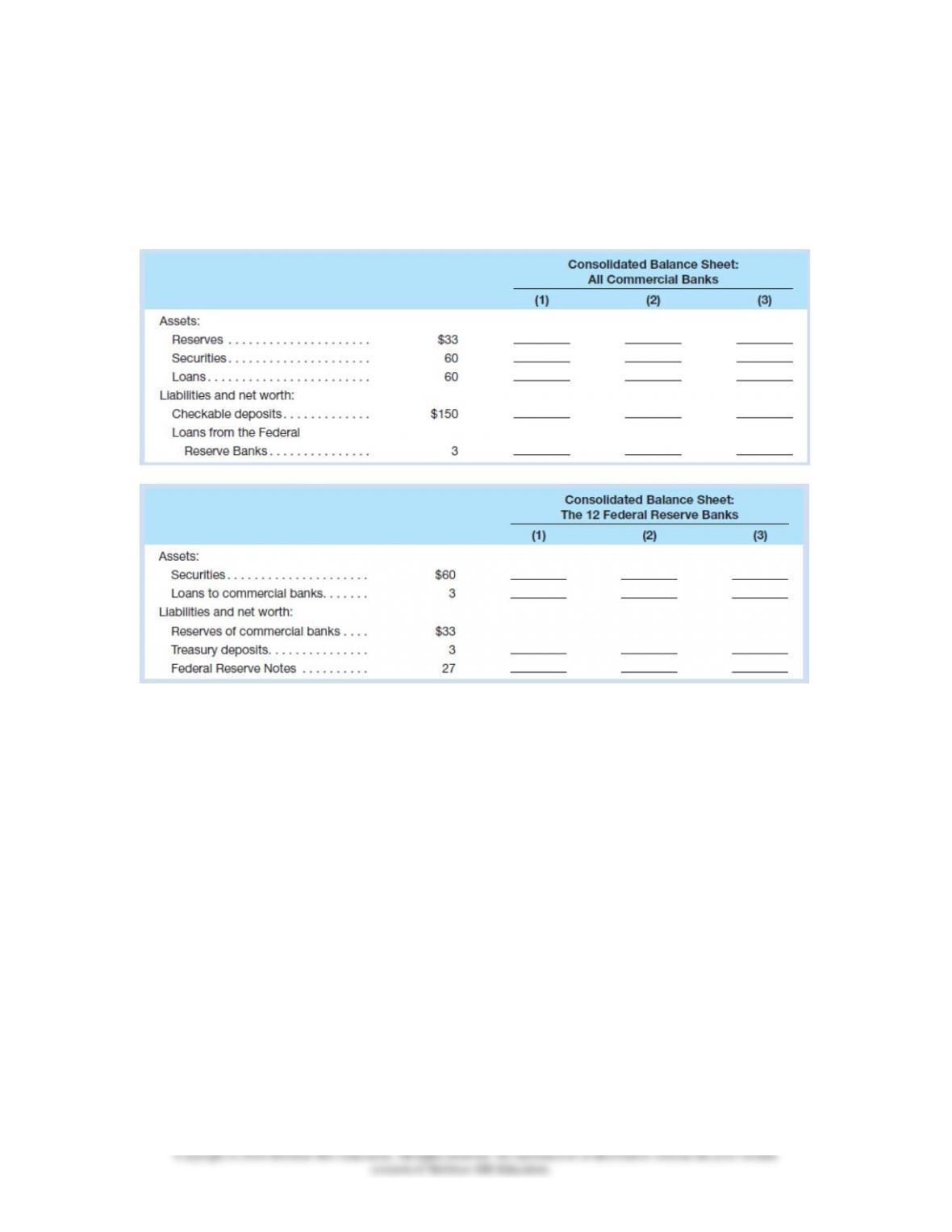

3. In the accompanying tables you will find consolidated balance sheets for the commercial

banking system and the 12 Federal Reserve Banks. Use columns 1 through 3 to indicate how the

balance sheets would read after each of transactions a to c is completed. Do not cumulate your

answers; that is, analyze each transaction separately, starting in each case from the numbers

provided. All accounts are in billions of dollars. LO3

a. A decline in the discount rate prompts commercial banks to borrow an additional $1 billion

from the Federal Reserve Banks. Show the new balance-sheet numbers in column 1 of each table.

b. The Federal Reserve Banks sell $3 billion in securities to members of the public, who pay for

the bonds with checks. Show the new balance-sheet numbers in column 2 of each table.

c. The Federal Reserve Banks buy $2 billion of securities from commercial banks. Show the new

balance-sheet numbers in column 3 of each table.

d. Now review each of the above three transactions, asking yourself these three questions: (1)

What change, if any, took place in the money supply as a direct and immediate result of each

transaction? (2) What increase or decrease in the commercial banks’ reserves took place in each

transaction? (3) Assuming a reserve ratio of 20 percent, what change in the money-creating

potential of the commercial banking system occurred as a result of each transaction?

Chapter 36 – Interest Rates and Monetary Policy

36-13

Chapter 36 – Interest Rates and Monetary Policy

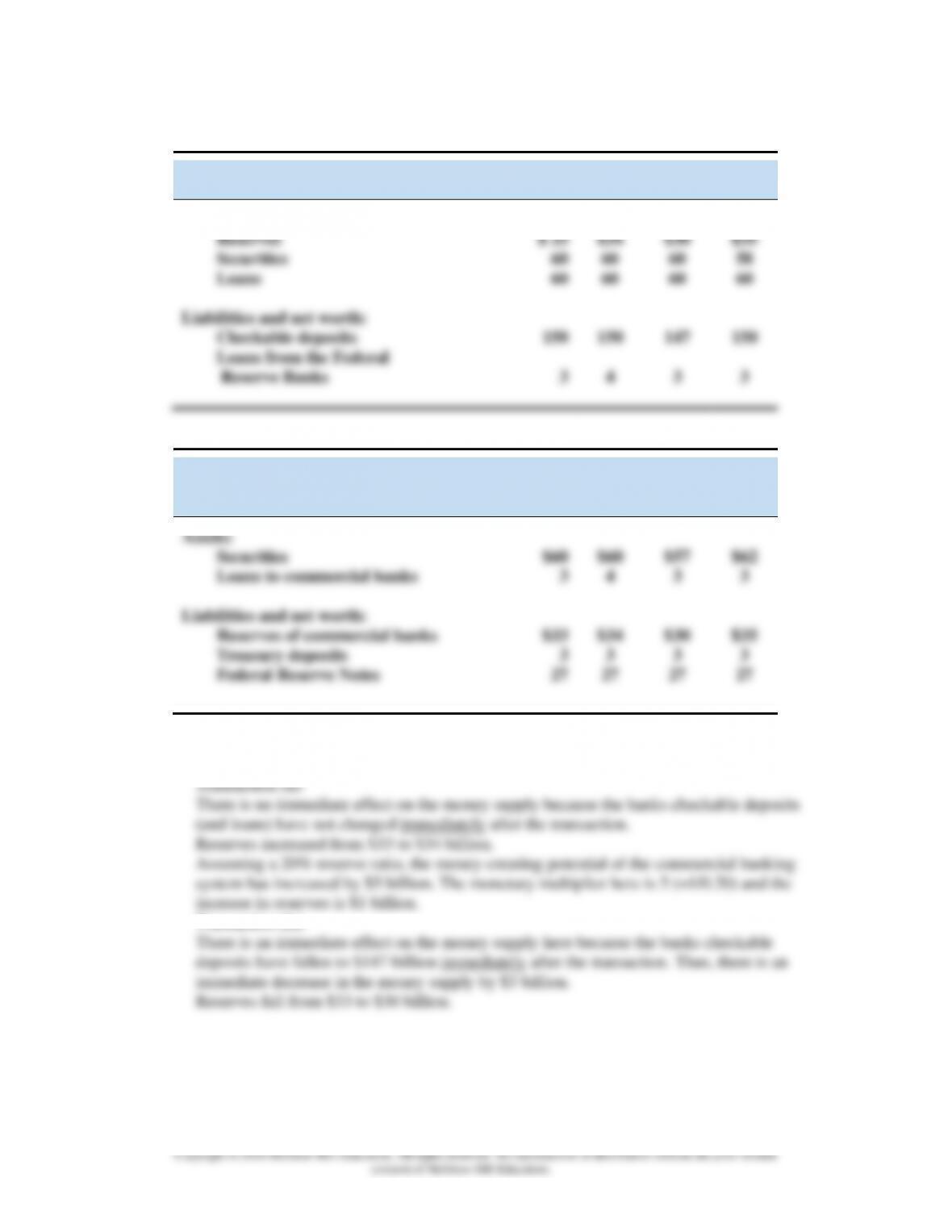

CONSOLIDATED BALANCE SHEET: ALL COMMERCIAL BANKS

(1)

(2)

(3)

Assets:

Reserves

Securities

Loans

Liabilities and net worth:

Checkable deposits

Loans from the Federal

Reserve Banks

$ 33

60

60

150

3

$34

60

60

150

4

$30

60

60

147

3

$35

58

60

150

3

CONSOLIDATED BALANCE SHEET:

TWELVE FEDERAL RESERVE BANKS

(1)

(2)

(3)

Assets:

Securities

Loans to commercial banks

Liabilities and net worth:

Reserves of commercial banks

Treasury deposits

Federal Reserve Notes

$60

3

$33

3

27

$60

4

$34

3

27

$57

3

$30

3

27

$62

3

$35

3

27

Part d:

Transaction (b):

Chapter 36 – Interest Rates and Monetary Policy

36-15

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Assuming a 20% reserve ratio, the money-creating potential of the commercial banking

system has decreased by $12 billion. This one takes a little more thought. Reserves have

fallen by $3 billion. Given the monetary multiplier is 5 (=1/0.20) this results in a decrease

in money-creating potential of $15 billion (=5 x $3 billion). However, checkable deposits

have also fallen by $3 billion. This implies that the bank has additional excess reserves of

$0.6 billion (= .20 (required reserve ratio) x $3 billion (decrease in checkable deposits))

relative to reserves prior to the transaction. The bank can lend out these additional excess

reserves. Again, given the monetary multiplier is 5 (=1/0.20) this results in an increase in

money-creating potential of $3 billion (=5 x $.06 billion).

Combining these two effects the money-creating potential of the commercial banking

system has decreased by $12 billion as stated above (= decrease of $15 billion due to the

direct fall in reserves minus the $3 billion increase resulting from the decrease of

checkable deposits and reduced need for required reserves.)

Transaction (c):

There is no immediate effect on the money supply because the banks checkable deposits

(and loans) have not changed immediately after the transaction.

Reserves increased from $33 to $35 billion.

Assuming a 20% reserve ratio, the money-creating potential of the commercial banking

system has increased by $10 billion. The monetary multiplier here is 5 (=1/0.20) and the

increase in reserves is $2 billion.

4. Refer to Table 36.2 and assume that the Fed’s reserve ratio is 10 percent and the economy is in

a severe recession. Also suppose that the commercial banks are hoarding all excess reserves (not

lending them out) because of their fear of loan defaults. Finally, suppose that the Fed is highly

concerned that the banks will suddenly lend out these excess reserves and possibly contribute to

inflation once the economy begins to recover and confidence is restored. By how many

percentage points would the Fed need to increase the reserve ratio to eliminate one-third of the

excess reserves? What would be the size of the monetary multiplier before and after the change in

the reserve ratio? By how much would the lending potential of the banks decline as a result of the

increase in the reserve ratio? LO3

Chapter 36 – Interest Rates and Monetary Policy

36-16

5. Suppose that the target range for the federal funds rate is 1.5 to 2.0 percent but that the

equilibrium federal funds rate is currently 1.70 percent. Assume that the equilibrium federal funds

rate falls (rises) by 1 percent for each $120 billion in repo (reverse repo) bond transactions the

Fed undertakes. If the Fed wishes to raise the equilibrium federal funds rate up to the top end of

the target range, will it initiate repos or reverse repos of bonds to nonbank financial firms? How

much will it have to repo or reverse repo? LO4

6. Suppose that inflation is 2 percent, the Federal funds rate is 4 percent, and real GDP falls 2

percent below potential GDP. According to the Taylor rule, in what direction and by how much

should the Fed change the real Federal funds rate? LO4

Chapter 36 – Interest Rates and Monetary Policy

36-17

7. Refer to the accompanying table for Moola to answer the following questions. LO5

What is the equilibrium interest rate in Moola? What is the level of investment at the equilibrium

interest rate? Is there either a recessionary output gap (negative GDP gap) or an inflationary

output gap (positive GDP gap) at the equilibrium interest rate, and, if either, what is the amount?

Given money demand, by how much would the Moola central bank need to change the money

supply to close the output gap? What is the expenditure multiplier in Moola?