Chapter 35 – Money Creation

35-1

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 35 – Money Creation

McConnell Brue Flynn 21e

DISCUSSION QUESTIONS

1. Explain why merchants accepted gold receipts as a means of payment even though the receipts

were issued by goldsmiths, not the government. What risk did goldsmiths introduce into the

payments system by issuing loans in the form of gold receipts? LO1

2. Why is the banking system in the United States referred to as a fractional reserve bank system?

What is the role of deposit insurance in a fractional reserve system? LO1

3. What is the difference between an asset and a liability on a bank’s balance sheet? How does net

worth relate to each? Why must a balance sheet always balance? What are the major assets and

claims on a commercial bank’s balance sheet? LO2

Chapter 35 – Money Creation

35-2

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Answer: An asset of a commercial bank is something owned by the bank or owed to the

bank (cash, securities, loans, etc…). A liability of the bank is a claim against the bank by

non-owners (checkable deposits, etc…) and the owners of the bank. This last liability is

the net worth of the bank. The balance sheet must balance by definition. That is, the sum

of assets must equal the sum of liabilities plus net worth for the bank to ensure

appropriate accounting of transactions.

The major assets of a bank are reserves, securities, loans, and vault cash (this last one is

relatively small when compared to the others). The major claim on the bank is checkable

deposits.

4. Why does the Federal Reserve require commercial banks to have reserves? Explain why

reserves are an asset to commercial banks but a liability to the Federal Reserve Banks. What are

excess reserves? How do you calculate the amount of excess reserves held by a bank? What is the

significance of excess reserves? LO2

5. “Whenever currency is deposited in a commercial bank, cash goes out of circulation and, as a

result, the supply of money is reduced.” Do you agree? Explain why or why not. LO2

6. “When a commercial bank makes loans, it creates money; when loans are repaid, money is

destroyed.” Explain. LO3

35-3

7. Suppose that Mountain Star Bank discovers that its reserves will temporarily fall slightly below

those legally required. How might it temporarily remedy this situation through the Federal funds

market? Now assume Mountain Star finds that its reserves will be substantially and permanently

deficient. What remedy is available to this bank? (Hint: Recall your answer to question 6.) LO3

8. Explain why a single commercial bank can safely lend only an amount equal to its excess

reserves but the commercial banking system as a whole can lend by a multiple of its excess

reserves. What is the monetary multiplier, and how does it relate to the reserve ratio? LO4, LO5

Chapter 35 – Money Creation

35-4

9. How would a decrease in the reserve requirement affect the (a) size of the money multiplier,

(b) amount of excess reserves in the banking system, and (c) extent to which the system could

expand the money supply through the creation of checkable deposits via loans? LO5

10. LAST WORD Does leverage increase the total size of the gain or loss from an investment, or

just the percentage rate of return on the part of the investment amount that was not borrowed?

How would lowering leverage make the financial system more stable?

Chapter 35 – Money Creation

35-5

REVIEW QUESTIONS

1. A goldsmith has $2 million of gold in his vaults. He issues $5 million in gold receipts. His gold

holdings are what fraction of the paper money (gold receipts) he has issued? LO1

a. 1/10.

b. 1/5.

c. 2/5.

d. 5/5.

2. A commercial bank has $100 million in checkable-deposit liabilities and $12 million in actual

reserves. The required reserve ratio is 10 percent. How big are the bank’s excess reserves? LO2

a. $100 million.

b. $88 million.

c. $12 million.

d. $2 million.

Chapter 35 – Money Creation

35-6

3. The actual reason that banks must hold required reserves is: LO2

a. To enhance liquidity and deter bank runs.

b. To help fund the Federal Deposit Insurance Corporation, which insures bank deposits.

c. To give the Fed control over the lending ability of commercial banks.

d. To help increase the number of bank loans.

4. A single commercial bank in a multibank banking system can lend only an amount equal to its

initial preloan _________________. LO3

a. Total reserves.

b. Excess reserves.

c. Total deposits.

d. Excess deposits.

Chapter 35 – Money Creation

35-7

5. The two conflicting goals facing commercial banks are: LO3

a. Profit and liquidity.

b. Profit and loss.

c. Deposits and withdrawals.

d. Assets and liabilities.

6. Suppose that the banking system in Canada has a required reserve ratio of 10 percent while the

banking system in the United States has a required reserve ratio of twenty percent. In which

country would $100 of initial excess reserves be able to cause a larger total amount of money

creation? LO4

a. Canada.

b. United States.

Chapter 35 – Money Creation

35-8

7. Suppose that the Fed has set the reserve ratio at 10 percent and that banks collectively have $2

billion in excess reserves. What is the maximum amount of new checkable-deposit money that

can be created by the banking system? LO5

a. $0.

b. $200 million.

c. $2 billion.

d. $20 billion.

8. Suppose that last year $30 billion in new loans were extended by banks while $50 billion in old

loans were paid off by borrowers. What happened to the money supply? LO5

a. Increased.

b. Decreased.

c. Stayed the same.

Chapter 35 – Money Creation

35-9

PROBLEMS

1. Suppose the assets of the Silver Lode Bank are $100,000 higher than on the previous day and

its net worth is up $20,000. By how much and in what direction must its liabilities have changed

from the day before? LO2

2. Suppose that Serendipity Bank has excess reserves of $8,000 and checkable deposits of

$150,000. If the reserve ratio is 20 percent, what is the size of the bank’s actual reserves? LO2

3. The Third National Bank has reserves of $20,000 and checkable deposits of $100,000. The

reserve ratio is 20 percent. Households deposit $5000 in currency into the bank and that currency

is added to reserves. What level of excess reserves does the bank now have? LO3

Chapter 35 – Money Creation

35-10

4. Suppose again that the Third National Bank has reserves of $20,000 and checkable deposits of

$100,000. The reserve ratio is 20 percent. The bank now sells $5,000 in securities to the Federal

Reserve Bank in its district, receiving a $5,000 increase in reserves in return. What level of

excess reserves does the bank now have? By what amount does your answer differ (yes, it does!)

from the answer to question 3? LO3

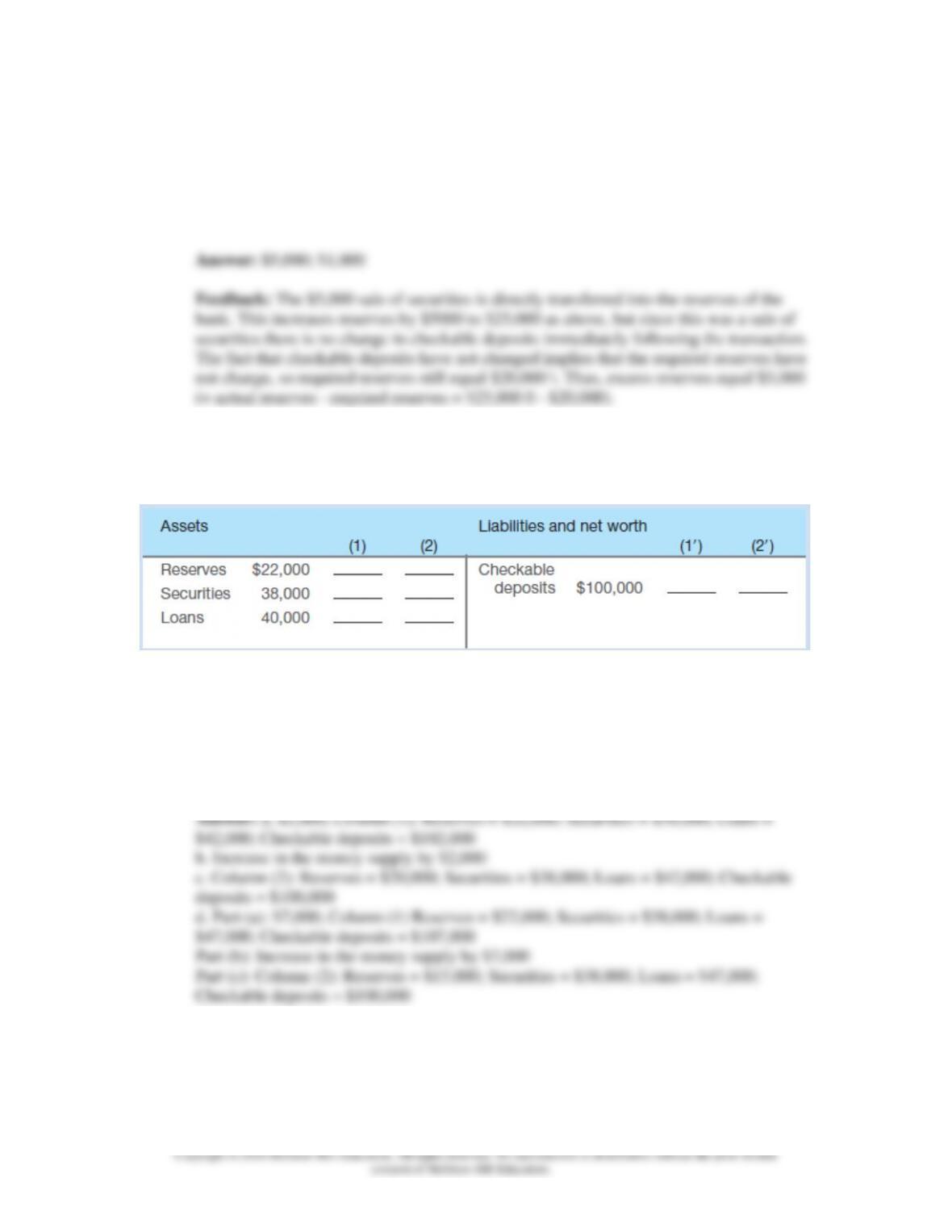

5. The balance sheet at the top of the next page is for Big Bucks Bank. The reserve ratio is 20

percent. LO3

a. What is the maximum amount of new loans that Big Bucks Bank can make? Show in columns

1 and 1′ how the bank’s balance sheet will appear after the bank has lent this additional amount.

b. By how much has the supply of money changed?

c. How will the bank’s balance sheet appear after checks drawn for the entire amount of the new

loans have been cleared against the bank? Show the new balance sheet in columns 2 and 2′.

d. Answer questions a, b, and c on the assumption that the reserve ratio is 15 percent.

Chapter 35 – Money Creation

35-11

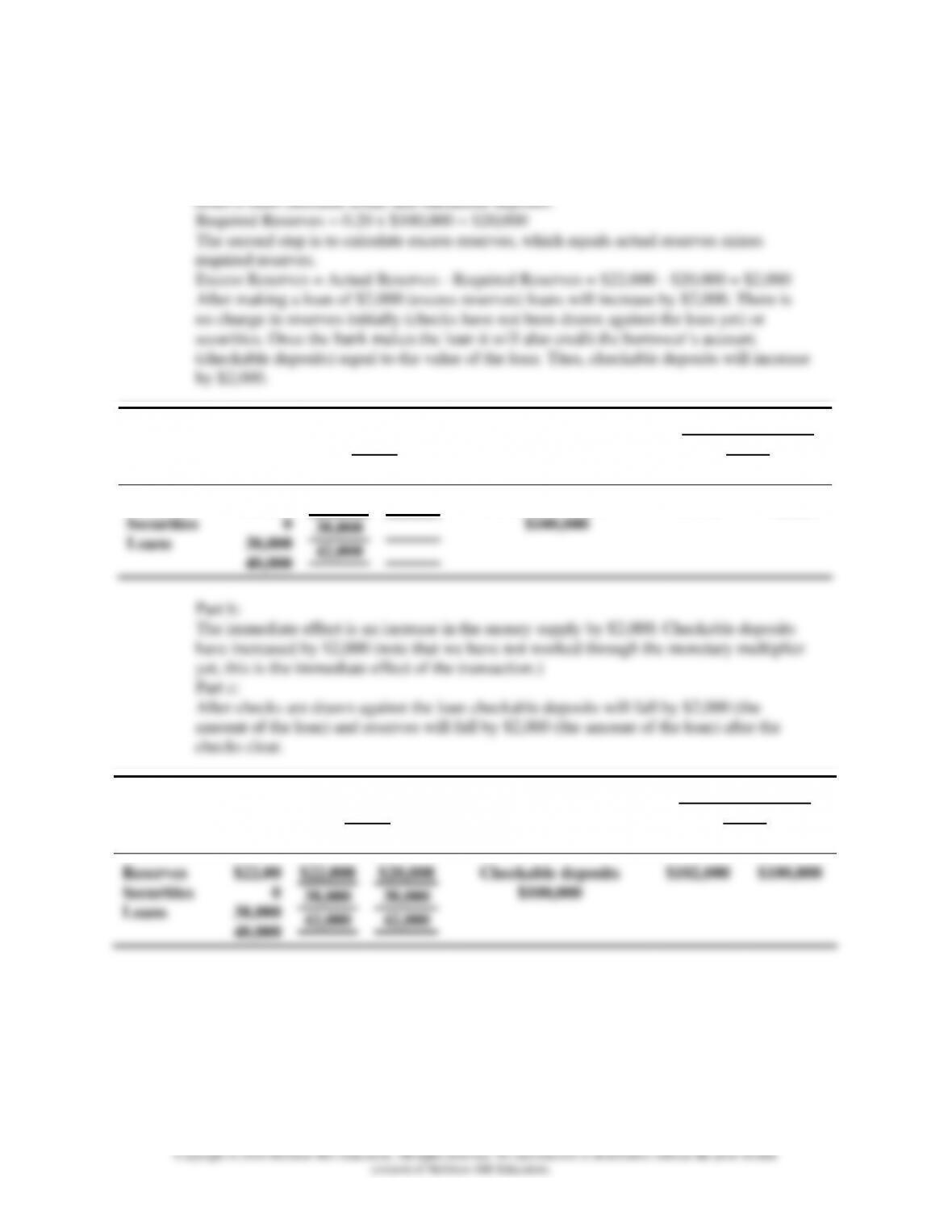

Feedback:

Part a:

The first step is to calculate required reserves, which equals the product of the required

Assets

(1) (2)

Liabilities and net

worth

(1) (2)

Reserves

Securities

Loans

$22,00

0

38,000

40,000

$22,000

38,000

42,000

Checkable deposits

$100,000

$102,000

_____

Assets

(1) (2)

Liabilities and net

worth

(1) (2)

Reserves

Securities

Loans

$22,00

0

38,000

40,000

$22,000

38,000

42,000

$20,000

38,000

42,000

Checkable deposits

$100,000

$102,000

$100,000

Chapter 35 – Money Creation

Part d:

Part a:

Chapter 35 – Money Creation

6. Suppose the simplified consolidated balance sheet shown below is for the entire commercial

banking system and that all figures are in billions of dollars. The reserve ratio is 25 percent. LO5

a. What is the amount of excess reserves in this commercial banking system? What is the

maximum amount the banking system might lend? Show in columns 1 and 1′ how the

consolidated balance sheet would look after this amount has been lent. What is the size of the

monetary multiplier?

b. Answer the questions in part a assuming the reserve ratio is 20 percent. What is the resulting

difference in the amount that the commercial banking system can lend?

Chapter 35 – Money Creation

Two things to note here: (1) The banking system does not lose reserves (2) checkable

deposits increase by the amount of the loans (money creation through the fractional

reserve banking system).