Chapter 15 – Technology, R&D, and Efficiency

15-1

Chapter 15 – Technology, R&D, and Efficiency

McConnell Brue Flynn 21e

DISCUSSION QUESTIONS

1. What is meant by technological advance, as broadly defined? How does technological advance

enter into the definition of the very long run? Which of the following are examples of

technological advance, and which are not: an improved production process; entry of a firm into a

profitable purely competitive industry; the imitation of a new production process by another firm;

an increase in a firm’s advertising expenditures? LO1

2. Contrast the older and the modern views of technological advance as they relate to the

economy. What is the role of entrepreneurs and other innovators in technological advance? How

does research by universities and government affect innovators and technological advance? Why

do you think some university researchers are becoming more like entrepreneurs and less like

“pure scientists”? LO2

Chapter 15 – Technology, R&D, and Efficiency

15-2

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

An entrepreneur is an initiator, innovator, and risk bearer—the catalyst who combines,

land, labor and capital resources in new and unique ways to produce new goods and

services. Historically, these were individuals. In today’s more technologically complex

economy, this role is just as likely to be carried out by entrepreneurial teams. Unlike

entrepreneurs, other innovators do not bear personal financial risk. These people include

key executives, scientists, and other salaried employees engaged in commercial R&D

activities.

New scientific knowledge is highly important to technological advance, but

scientific principles, as such, cannot be patented. For this reason entrepreneurs

actively study the scientific output of university and government laboratories to

find discoveries with commercial applications, obtaining information without

paying for its development. Although, firms increasingly help fund university

research that relates to their products, scientists increasingly realize their work

may have commercial value.

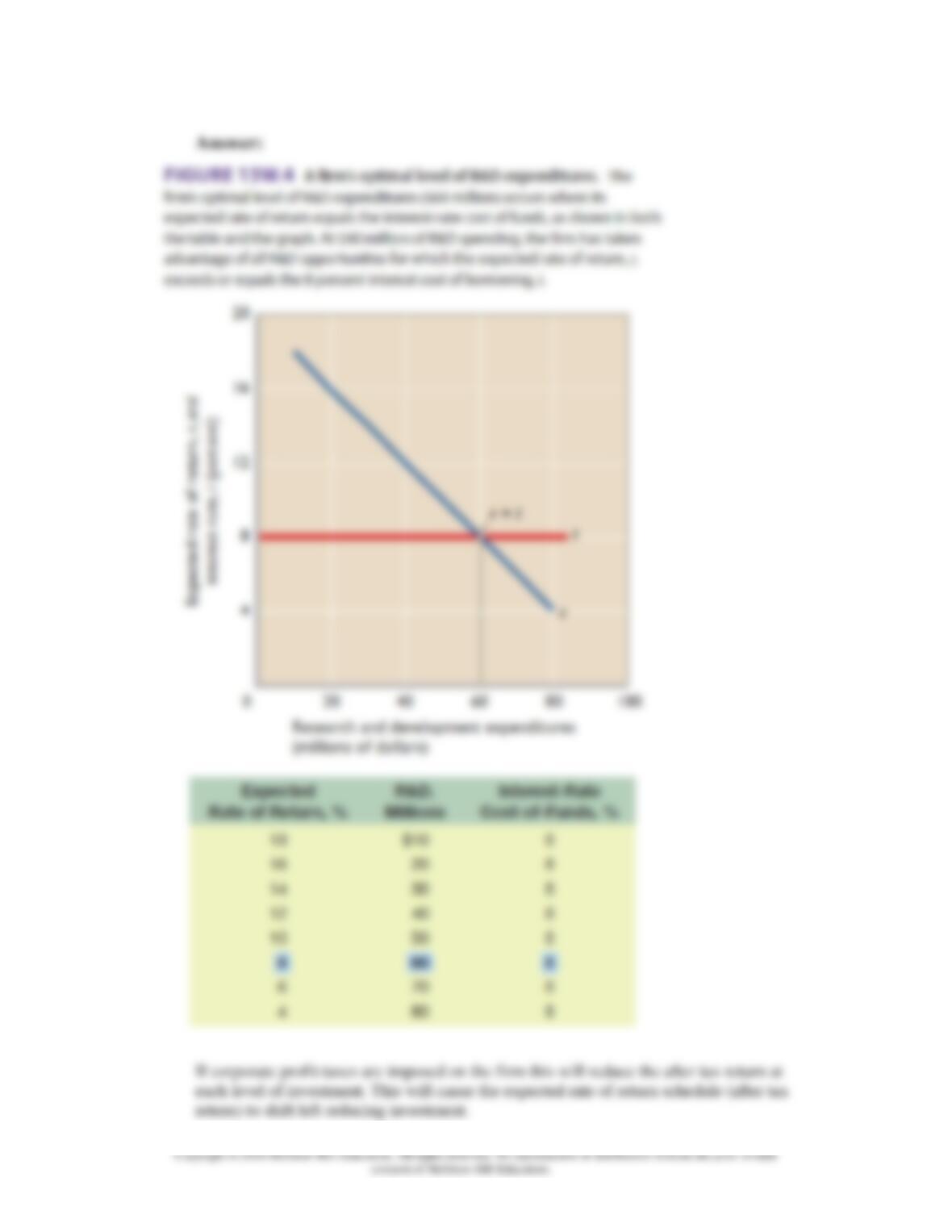

3. Consider the effect that corporate profit taxes have on investing. Look back at Figure 15.4.

Suppose that the r line is the rate of return a firm earns before taxes. If corporate profit taxes are

imposed, the firm’s after-tax returns will be lower (and the higher the tax rate, the lower the after-

tax returns). If the firm’s decisions about R&D spending are based on comparing after-tax returns

with the interest-rate costs of funds, how will increased corporate profit taxes affect R&D

spending? Does this effect modify your views on corporate profit taxes? Discuss. LO3

Chapter 15 – Technology, R&D, and Efficiency

15-3

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Answer:

If corporate profit taxes are imposed on the firm this will reduce the after tax return at

each level of investment. This will cause the expected rate of return schedule (after tax

return) to shift left reducing investment.

Chapter 15 – Technology, R&D, and Efficiency

15-4

For example, if the tax rate is 50% the firm only keeps 50% of the before tax return. In

the diagram above the equilibrium level of R&D expenditure (investment) is $60 million

4. Answer the following lettered questions on the basis of the information in this table: LO3

a. If the interest-rate cost of funds is 8 percent, what will be the optimal amount of R&D spending

for this firm?

b. Explain why $20 million of R&D spending will not be optimal.

c. Why won’t $60 million be optimal either?

Chapter 15 – Technology, R&D, and Efficiency

15-5

5. Explain: “The success of a new product depends not only on its marginal utility but also on its

price.” LO4

6. Learning how to use software takes time. So once customers have learned to use a particular

software package, it is easier to sell them software upgrades than to convince them to switch to

new software. What implications does this have for expected rates of return on R&D spending for

software firms developing upgrades versus firms developing imitative products? LO5

15-6

7. Why might a firm making a large economic profit from its existing product employ a fast–

second strategy in relationship to new or improved products? What risks does it run in pursuing

this strategy? What incentive does a firm have to engage in R&D when rivals can imitate its new

product? LO5

8. Do you think the overall level of R&D would increase or decrease over the next 20 to 30 years

if the lengths of new patents were extended from 20 years to, say, “forever”? What if the duration

were reduced from 20 years to, say, 3 years? LO5

9. Make a case that neither pure competition nor pure monopoly is conducive to a great deal of

R&D spending and innovation. Why might oligopoly be more favorable to R&D spending and

innovation than either pure competition or pure monopoly? What is the inverted-U theory of

R&D, and how does it relate to your answers to these questions? LO6

Chapter 15 – Technology, R&D, and Efficiency

15-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

expensive R&D costs associated with major product or process innovation. The typical

firm in oligopoly is likely to realize ongoing economic profits, which provides a ready

source of funds. The existence of barriers to entry gives some assurance that any

economic profits earned from innovation can be maintained. The large volume of sales

allows the firm to spread the cost of R&D over a great many units of output. The large

size of the firms in oligopoly also makes it easier to absorb the inevitable losses from

“misses” while waiting for compensation from the “hits.”

The inverted-U theory suggests that R&D expenditures as a percentage of sales rise with

industry concentration until the four-firm concentration ratio reaches about 50%. Further

increases in industry concentrations are associated with lower relative R&D expenditures.

(See figure 31W-7) The inverted-U theory reiterates the assessment made above

regarding likely R&D spending and market structure.

10. Evaluate: “Society does not need laws outlawing monopolization and monopoly. Inevitably,

monopoly causes its own self-destruction since its high profit is the lure for other firms or

entrepreneurs to develop substitute products.” LO7

11. LAST WORD How could spending less on Social Security now lead to an ability to

increase Social Security in the future? Why don’t businesses devote more of their R&D

spending toward basic scientific research?

Chapter 15 – Technology, R&D, and Efficiency

15-8

REVIEW QUESTIONS

1. Listed below are several possible actions by firms. Write “INV” beside those that reflect

invention, “INN” beside those that reflect innovation, and “DIF” beside those that reflect

diffusion. LO1

a. An auto manufacturer adds “heated seats” as a standard feature in its luxury cars to keep pace

with a rival firm whose luxury cars already have this feature.

b. A television production company pioneers the first music video channel.

c. A firm develops and patents a working model of a self-erasing whiteboard for classrooms.

d. A light bulb firm is the first to produce and market lighting fixtures with LEDs (light emitting

diodes).

e. A rival toy maker introduces a new Jezebel doll to compete with Mattel’s Barbie doll.

2. A firm is considering three possible one-year investments, which we will name X, Y, and Z.

• Investment X would cost $10 million now and would return $11 million next year, for a

net gain of $1 million.

• Investment Y would cost $100 million now and would return $105 million next year, for

a net gain of $5 million.

• Investment Z would cost $1 million now and would return $1.2 million next year, for a

net gain of $200,000.

The firm currently has $150 million of cash on hand that it can loan out at 15 percent interest.

Which of the three possible investments should it undertake? LO3

a. X only.

b. Y only.

c. Z only.

d. X and Y.

e. X and Z.

f. X, Y, and Z.

Chapter 15 – Technology, R&D, and Efficiency

15-9

3. An additional unit of Old Product X will bring Cindy an MU of 15 utils; an additional unit of

New Product Y will bring Cindy an MU of 30 utils; and an additional unit of New Product Z will

bring Cindy an MU of 40 utils. If a unit of Old Product X costs $10, a until of New Product Y

costs $30, and a unit of New Product Z costs $20, which product will Cindy prefer to spend her

money on? LO4

a. Old Product X.

b. New Product Y.

c. New Product Z.

d. More information is required.

4. The inverted-U theory suggests that R&D expenditures as a percentage of sales __________

with industry concentration after the four-firm concentration ratio exceeds about 50 percent. LO6

a. Rise.

b. Fall.

c. Fluctuate.

d. Flat-line.

Chapter 15 – Technology, R&D, and Efficiency

15–10

5. Which statement about market structure and innovation is true? LO7

a. Innovation helps only dominant firms.

b. Innovation keeps new firms from ever catching up with leading firms.

c. Innovation often leads to creative destruction and the replacement of

established firms by new firms.

d. Innovation always leads to entrenched monopoly power.

PROBLEMS

1. Suppose a firm expects that a $20 million expenditure on R&D this year will result in a new

product that will increase its profit next year by $1 million. LO3

a. What is the expected rate of return on this R&D expenditure?

b. Suppose the firm can get a bank loan at 6 percent interest to finance its $20 million R&D

project. Will the firm undertake the project?

c. Now suppose the interest-rate cost of borrowing, in effect, falls to 4 percent because the firm

decides to use its own retained earnings to finance the R&D. Will this lower interest rate change

the firm’s R&D decision?

d. Now suppose that the firm has savings of $20 million—enough money to fund the R&D

expenditure without borrowing. If the firm has the chance to invest this money either in the R&D

project or in government bonds that pay 3.5 percent per year, which should it do?

e. What if the government bonds were paying 6.5 percent per year?

Feedback:

a. The expected rate of return equals the (expected) profit from the R&D divided the

expenditure.

b. The firm will not borrow at a rate greater than the expected rate of return. Since the

Chapter 15 – Technology, R&D, and Efficiency

15–11

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

c. The firm will borrow at a rate less than the expected rate of return. Since the bank loan

now has a 4% rate of interest, which is less than the expected rate of return, the firm will

undertake this project.

d. The firm will invest its savings where the return is the highest. Since government

bonds pay 3.5% per year and the expected rate of return on the R&D project is 5%, the

firm should invest in the R&D project.

e. If government bonds pay 6.5% per year and the expected rate of return on the R&D

project is 5%, the firm should invest in government bonds (not undertake the project).

2. A firm faces the following costs. Its total cost of capital = $1,000; its price paid for labor = $12

per labor unit; and its price paid for raw materials = $4 per raw-material unit. LO4

a. Suppose the firm can produce 5,000 units of output this year by combining its fixed capital

with 100 units of labor and 450 units of raw materials. What are the total cost and average total

cost of producing the 5,000 units of output?

b. Now assume the firm improves its production process so that it can produce 6,000 units of

output this year by combining its fixed capital with 100 units of labor and 450 units of raw

materials. What are the total cost and average total cost of producing the 6000 units of output?

c. If units of output can always be sold for $1 each, then by how much does the firm’s profit

increase after it improves its production process?

d. Suppose that implementing the improved production process would require a one-time-only

cost of $1,100. If the firm only considers this year’s profit, would the firm implement the

improved production process? What if the firm considers its profit not just this year but in future

years as well?

Chapter 15 – Technology, R&D, and Efficiency

c. The firm’s profit equals total revenue (price x units produced and sold) minus total

d. If the firm only considers this year’s profit, the firm would choose not to implement

the improved production process. The firm will only increase profit by $1,000 for the