Chapter 12 – Pure Monopoly

PROBLEMS

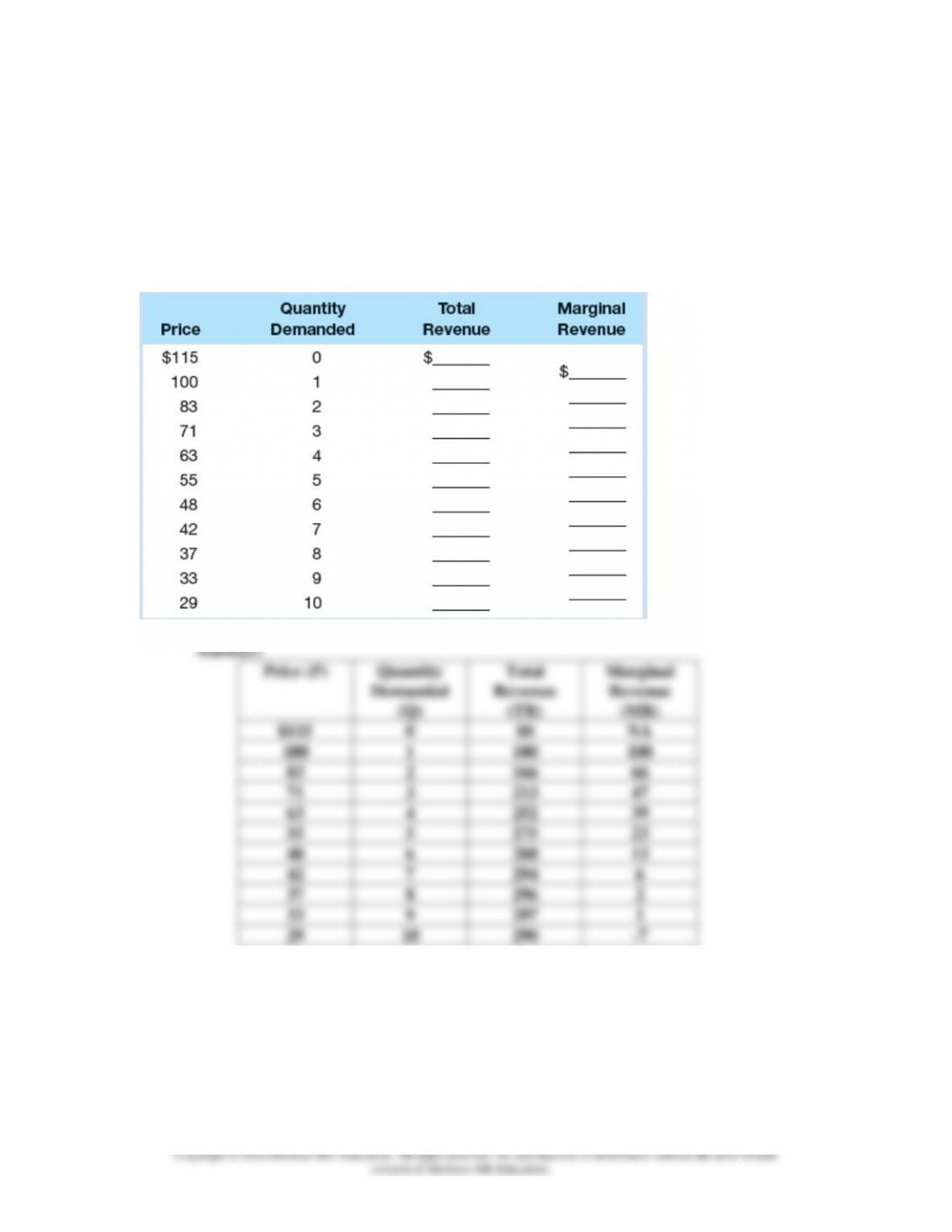

1. Suppose a pure monopolist is faced with the demand schedule shown below and the same cost

data as the competitive producer discussed in problem 4 at the end of Chapter 10. Calculate the

missing total-revenue and marginal-revenue amounts, and determine the profit-maximizing price

and profit-maximizing output for this monopolist. What is the monopolist’s profit? Verify your

answer graphically and by comparing total revenue and total cost. LO4

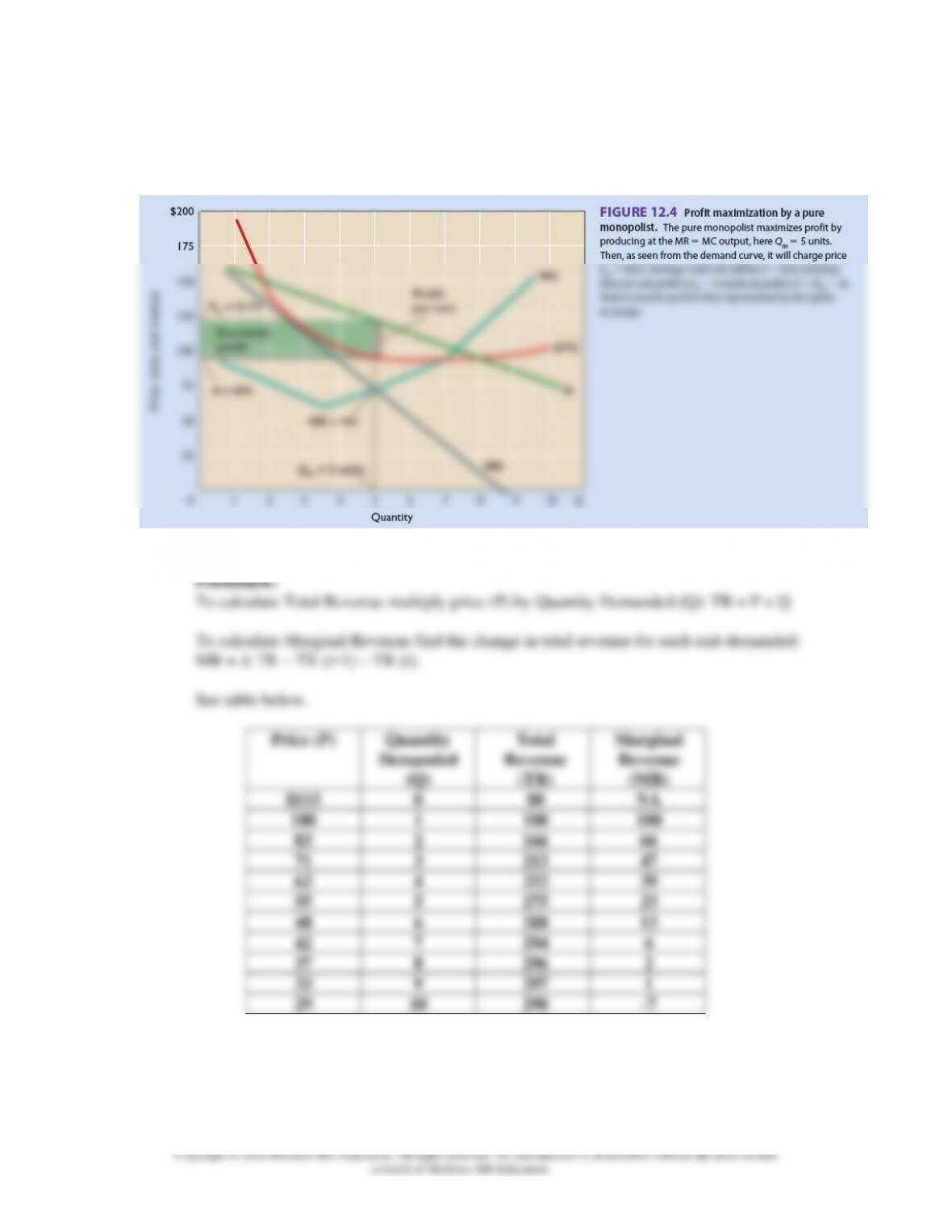

Chapter 12 – Pure Monopoly

Profit-maximizing price = $63; profit-maximizing quantity = 4 units;

monopolist’s profit = $42.

The graph should have the general shape of Figure 12.4.

Chapter 12 – Pure Monopoly

12–15

To determine profit-maximizing price and profit-maximizing output for this monopolist

use the cost data in the table below.

To find the profit maximizing quantity compare marginal revenue from the first table

Chapter 12 – Pure Monopoly

12–16

The profit maximizing quantity produced is 4 units.

The profit maximizing price is the price associated with the profit maximizing quantity, 4

units. Thus, the profit maximizing price is $63.

12–17

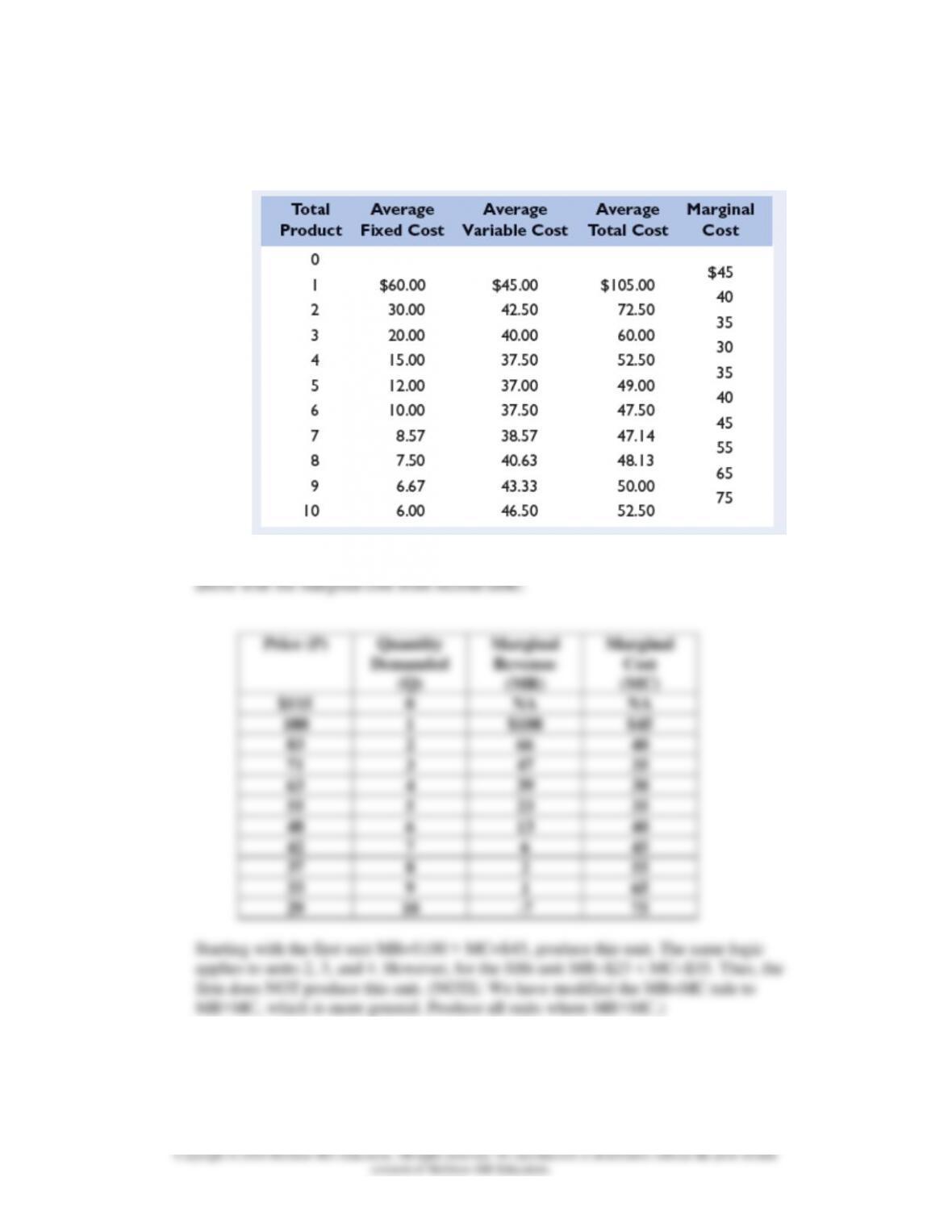

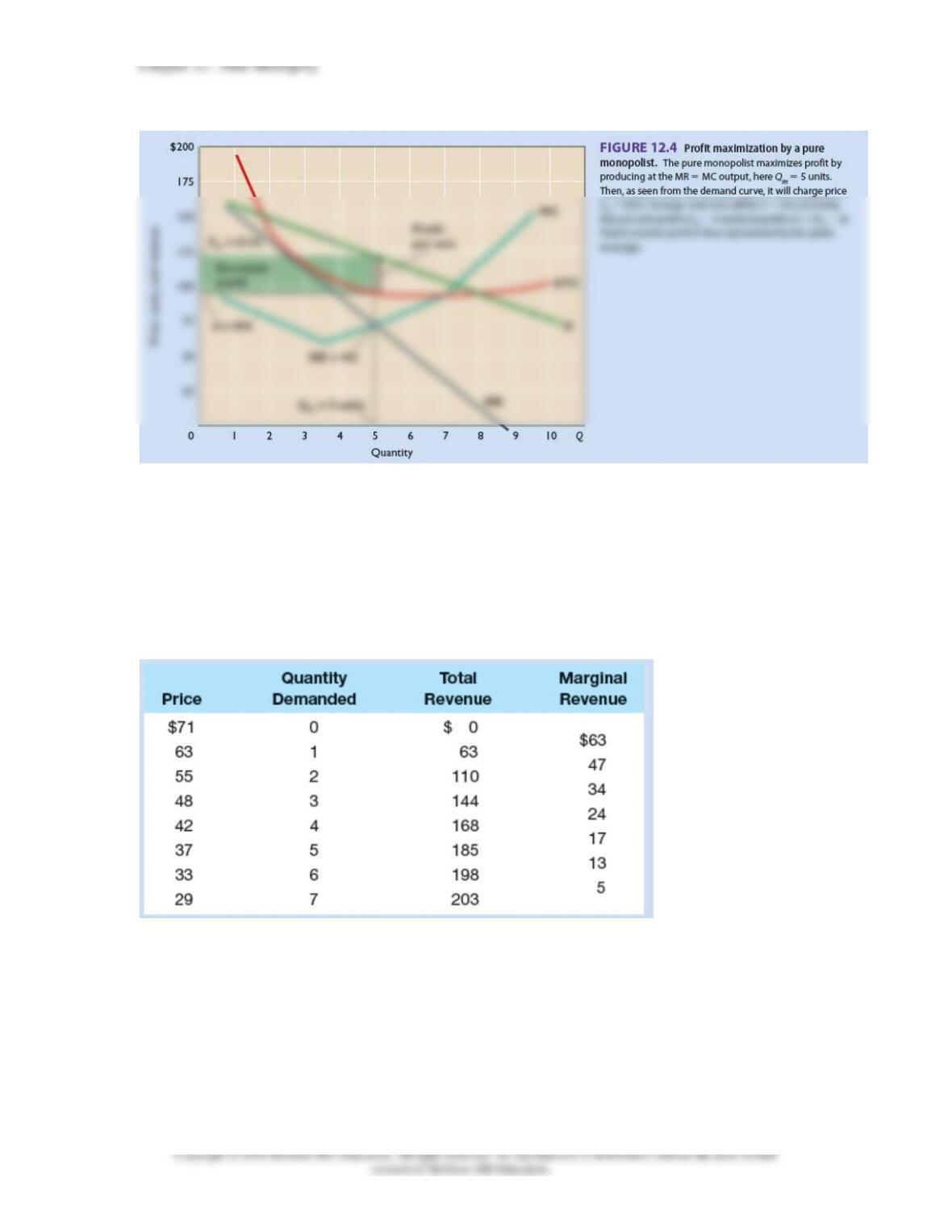

2. Suppose that a price-discriminating monopolist has segregated its market into two groups of

buyers. The first group described by the demand and revenue data that you developed for

problem 1. The demand and revenue data for the second group of buyers is shown in the

accompanying table. Assume that MC is $13 in both markets and MC = ATC at all output levels.

What price will the firm charge in each market? Based solely on these two prices, which market

has the higher price elasticity of demand? What will be this monopolist’s total economic profit?

LO6

Chapter 12 – Pure Monopoly

12–18

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Answer: Price in market 1 = $48; price in market 2 = $33; the second market has

the higher price elasticity of demand; total economic profit = $330.

Feedback: Let’s start with the second market. Marginal cost is $13 for all output levels.

The marginal revenue from producing the 6th unit is $13 (=$198- $185), so this is the last

unit produced by the firm for this market.

The first market is found in problem 1 (Table reproduced below):

Price (P)

Quantity

Demanded

(Q)

Total

Revenue

(TR)

Marginal

Revenue

(MR)

$115

0

$0

NA

100

1

100

100

83

2

166

66

71

3

213

47

63

4

252

39

55

5

275

23

48

6

288

13

42

7

294

6

37

8

296

2

33

9

297

1

29

10

290

-7

Chapter 12 – Pure Monopoly

12–19

Again, marginal cost is $13 for all output levels.

The marginal revenue equals marginal cost rule results in 6 units being produced in this

market as well (MR=MC=$13 at 6 units in this market).

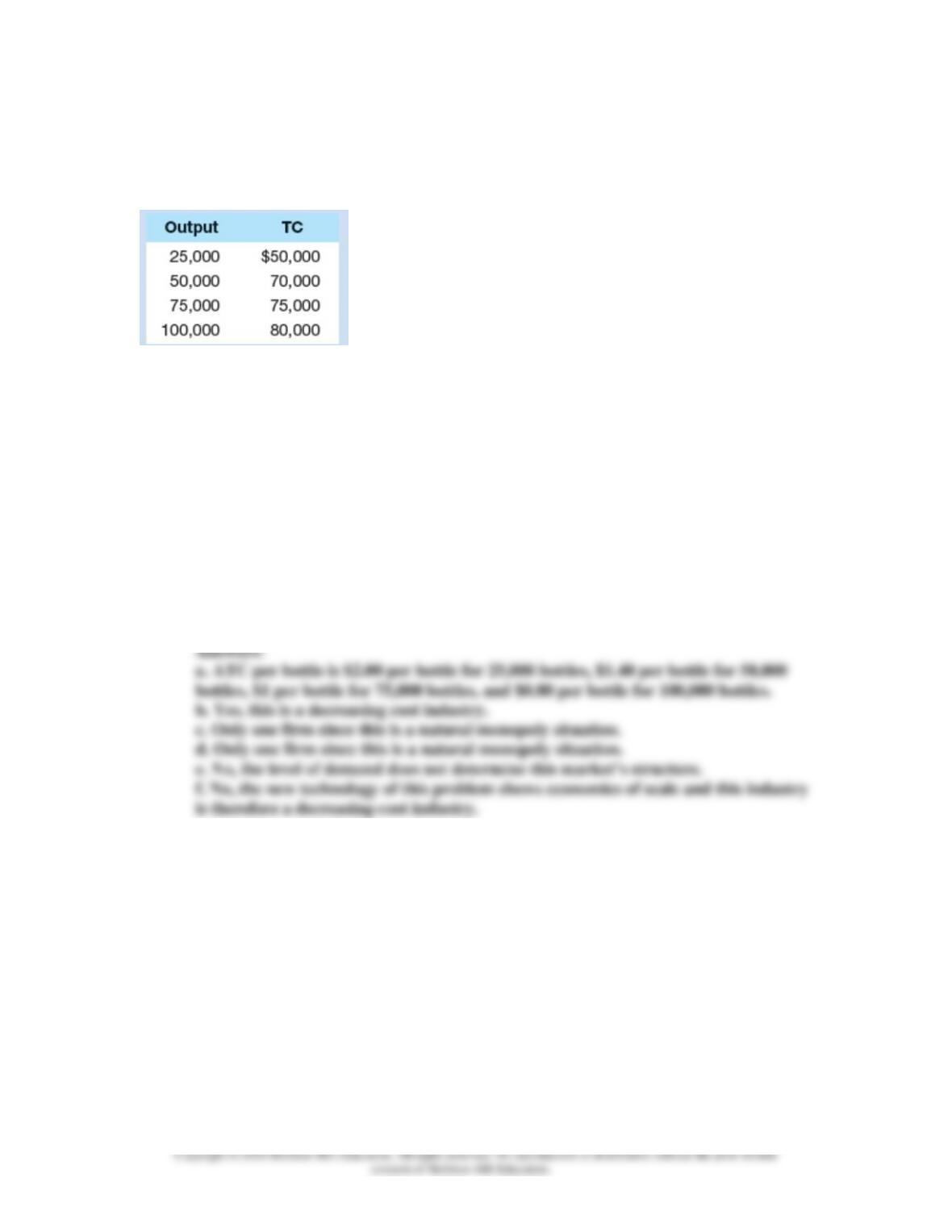

3. Assume that the most efficient production technology available for making vitamin pills has

the cost structure given in the following table. Note that output is measured as the number of

bottles of vitamins produced per day and that costs include a normal profit. LO6

a. What is ATC per unit for each level of output listed in the table?

b. Is this a decreasing-cost industry? (Answer yes or no).

c. Suppose that the market price for a bottle of vitamins is $2.50 and that at that price the total

market quantity demanded is 75,000,000 bottles. How many firms will there be in this industry?

d. Suppose that instead the market quantity demanded at a price of $2.50 is only 75,000. How

many firms do you expect there to be in this industry?

e. Review your answers to parts b, c, and d. Does the level of demand determine this industry’s

market structure?

Chapter 12 – Pure Monopoly

Feedback:

a. To find Average Total Cost (ATC) divide Total Cost by Output (Quantity).

Chapter 12 – Pure Monopoly

12–21

4. A new production technology for making vitamins is invented by a college professor who

decides not to patent it. Thus, it is available for anybody to copy and put into use. The TC per

bottle for production up to 100,000 bottles per day is given in the following table. LO6

a. What is ATC for each level of output listed in the table?

b. Suppose that for each 25,000-bottle per day increase in production above

100,000 bottles per day, TC increases by $5,000 (so that, for instance, 125,000 bottles per day

would generate total costs of $85,000 and 150,000 bottles per day would generate total costs of

$90,000). Is this a decreasing-cost industry?

c. Suppose that the price of a bottle of vitamins is $1.33 and that at that price the total quantity

demanded by consumers is 75,000,000 bottles. How many firms will there be in this industry?

d. Suppose that instead the market quantity demanded at a price of $1.33 is only 75,000. How

many firms do you expect there to be in this industry?

e. Review your answers to parts b, c, and d. Does the level of demand determine this industry’s

market structure?

f. Compare your answer to part d of this question with your answer to part d of problem 3. Do

both production technologies show constant returns to scale?

Chapter 12 – Pure Monopoly

Feedback:

a. To find Average Total Cost (ATC) divide Total Cost by Output (Quantity).

ATC = Total Cost / Output

Chapter 12 – Pure Monopoly

12–23

5. Suppose you have been tasked with regulating a single monopoly firm that sells 50-pound bags

of concrete. The firm has fixed costs of $10 million per year and a variable cost of $1 per bag no

matter how many bags are produced. LO7

a. If this firm kept on increasing its output level, would ATC per bag ever increase? Is this a

decreasing-cost industry?

b. If you wished to regulate this monopoly by charging the socially optimal price, what price

would you charge? At that price, what would be the size of the firm’s profit or loss? Would the

firm want to exit the industry?

c. You find out that if you set the price at $2 per bag, consumers will demand 10 million bags.

How big will the firm’s profit or loss be at that price?

d. If consumers instead demanded 20 million bags at a price of $2 per bag, how big would the

firm’s profit or loss be?

e. Suppose that demand is perfectly inelastic at 20 million bags, so that consumers demand 20

million bags no matter what the price is. What price should you charge if you want the firm to

earn only fair rate of return? Assume as always that TC includes a normal profit.

Chapter 12 – Pure Monopoly

12–24

Feedback:

a. ATC will never increase. This is a decreasing cost industry. The intuition is that FC get

c. The firm’s revenue equals $20,000,000 ( = $2 (price) x 10,000,000 (quantity)).

e. The fair rate of return is where economic profit is zero (Total Cost above includes

normal profit).