Chapter 11 – Pure Competition in the Long Run

11-1

Chapter 11 – Pure Competition in the Long Run

McConnell Brue Flynn 21e

DISCUSSION QUESTIONS

1. Explain how the long run differs from the short run in pure competition. LO1

2. Relate opportunity costs to why profits encourage entry into purely competitive industries and

how losses encourage exit from purely competitive industries. L02

3. How do the entry and exit of firms in a purely competitive industry affect resource flows and

long-run profits and losses? LO2

4. In long-run equilibrium, P = minimum ATC = MC. Of what significance for economic

efficiency is the equality of P and minimum ATC? The equality of P and MC? Distinguish

between productive efficiency and allocative efficiency in your answer. LO4

Chapter 11 – Pure Competition in the Long Run

11-2

5. The basic model of pure competition reviewed in this chapter finds that in the long run all

firms in a purely competitive industry will earn normal profits. If all firms will only earn a normal

profit in the long run, why would any firms bother to develop new products or lower-cost

production methods? Explain. LO5

6. “Ninety percent of new products fail within two years—so you shouldn’t be so eager to

innovate.” Do you agree? Explain why or why not. LO5

7. LAST WORD How can patents speed up the process of creative destruction? How can

patents slow down the process of creative destruction? How do differences in manufacturing

costs affect which industries would be most likely to be affected by the removal of patents?

Chapter 11 – Pure Competition in the Long Run

11-3

REVIEW QUESTIONS

1. When discussing pure competition, the term long run refers to a period of time long enough to

allow: LO1

a. Firms already in an industry to either expand or contract their capacities.

b. New firms to enter or existing firms to leave.

c. Both a and b.

d. None of the above.

2. Suppose that the pen-making industry is perfectly competitive. Also suppose that each current

firm and any potential firms that might enter the industry all have identical cost curves, with

minimum ATC = $1.25 per pen. If the market equilibrium price of pens is currently $1.50, what

would you expect it to be in the long run? LO2

a. $0.25.

b. $1.00.

c. $1.25.

d. $1.50.

Chapter 11 – Pure Competition in the Long Run

11-4

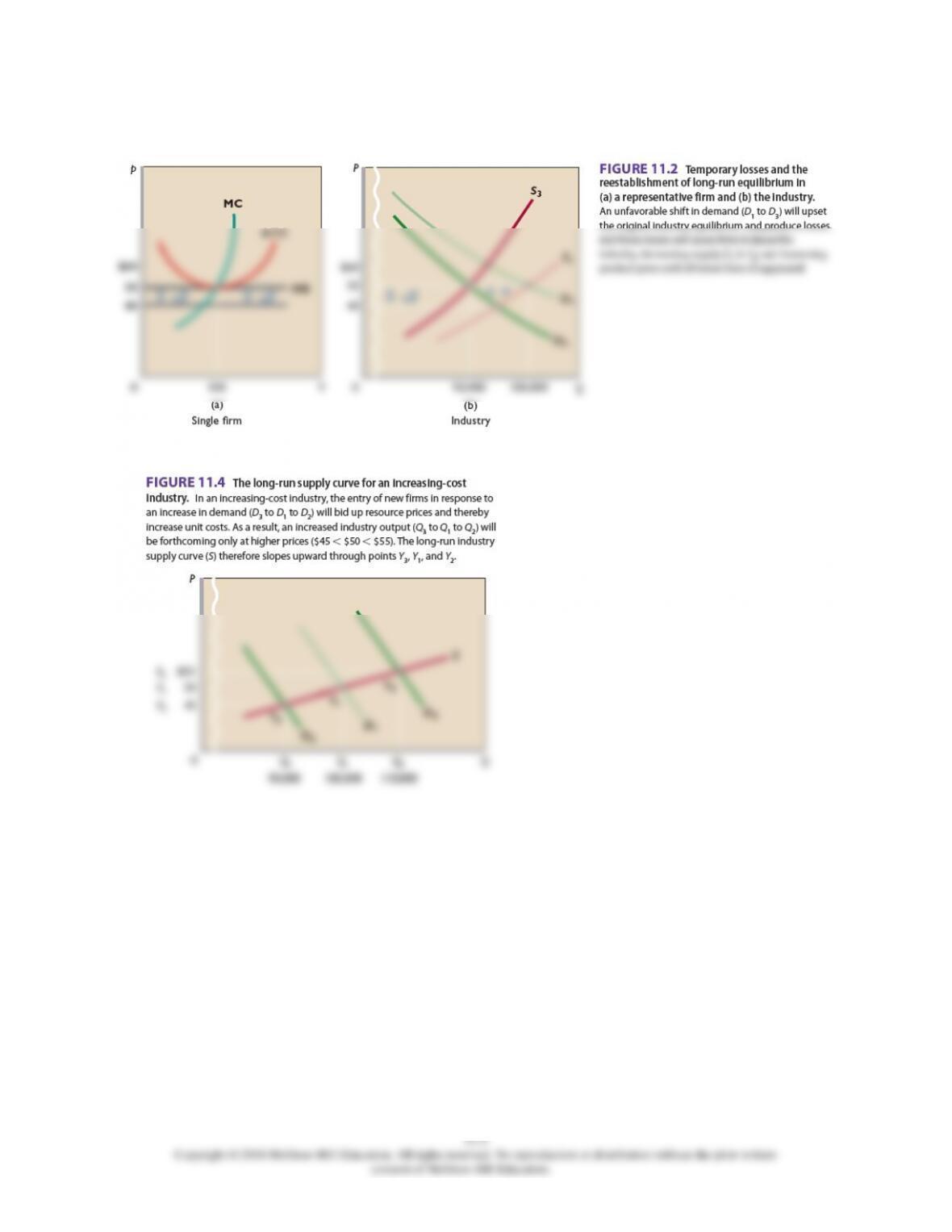

3. Suppose that as the output of mobile phones increases, the cost of touch screens and other

component parts decreases. If the mobile phone industry features pure competition, we would

expect the long-run supply curve for mobile phones to be: LO3

a. Upward sloping.

b. Downward sloping.

c. Horizontal.

d. U-shaped.

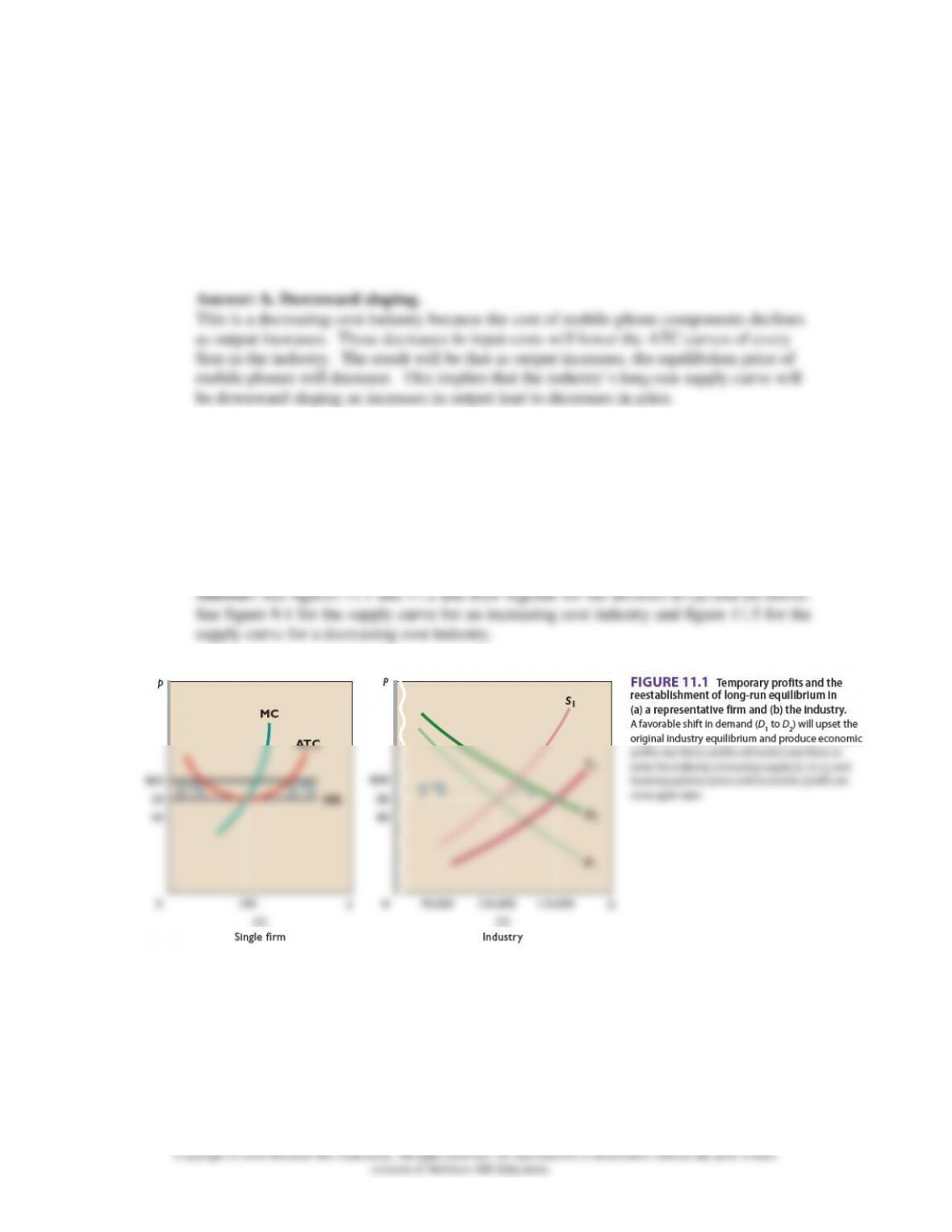

4. Using diagrams for both the industry and a representative firm, illustrate competitive long-run

equilibrium. Assuming constant costs, employ these diagrams to show how (a) an increase and

(b) a decrease in market demand will upset that long-run equilibrium. Trace graphically and

describe verbally the adjustment processes by which long-run equilibrium is restored. Now

rework your analysis for increasing– and decreasing-cost industries and compare the three long-

run supply curves. LO3

Chapter 11 – Pure Competition in the Long Run

11-6

5. Suppose that purely competitive firms producing cashews discover that P exceeds MC. Will

their combined output of cashews be too little, too much, or just right to achieve allocative

efficiency? In the long run, what will happen to the supply of cashews and the price of cashews?

Use a supply and demand diagram to show how that response will change the combined amount

of consumer surplus and producer surplus in the market for cashews. LO4

Chapter 11 – Pure Competition in the Long Run

11-7

PROBLEMS

1. A firm in a purely competitive industry has a typical cost structure. The normal rate of profit in

the economy is 5 percent. This firm is earning $5.50 on every $50 invested by its founders. What

is its percentage rate of return? Is the firm earning an economic profit? If so, how large? Will this

industry see entry or exit? What will be the rate of return earned by firms in this industry once the

industry reaches long-run equilibrium? LO2

2. A firm in a purely competitive industry is currently producing 1,000 units per day at a total cost

of $450. If the firm produced 800 units per day, its total cost would be $300, and if it produced

500 units per day, its total cost would be $275. What are the firm’s ATC per unit at these three

levels of production? If every firm in this industry has the same cost structure, is the industry in

long-run competitive equilibrium? From what you know about these firms’ cost structures, what

is the highest possible price per unit that could exist as the market price in long-run equilibrium?

If that price ends up being the market price and if the normal rate of profit is 10 percent, then how

big will each firm’s accounting profit per unit be? LO4

Answers: The firms’ ATC per unit at 1,000 units per day is $0.45 (= $450/1,000); at

Chapter 11 – Pure Competition in the Long Run

11-8

Feedback: The average total cost (ATC) is found by dividing total cost by the number of

units being produced. ATC for 1,000 units is $0.45 (=$450 / 1,000). ATC for 800 units

3. There are 300 purely competitive farms in the local dairy market. Of the 300 dairy farms, 298

have a cost structure that generates profits of $24 for every $300 invested. What is their

percentage rate of return? The other two dairies have a cost structure that generates profits of $22

for every $200 invested. What is their percentage rate of return? Assuming that the normal rate of

profit in the economy is 10 percent; will there be entry or exit? Will the change in the number of

firms affect the two that earn $22 for every $200 invested? What will be the rate of return earned

by most firms in the industry in long–run equilibrium? If firms can copy each other’s technology,

what will be the rate of return eventually earned by all firms? LO4

Feedback: The percentage rate of return for the firms is found by dividing profits by the

amount invested. This is multiplied by 100 to convert into percentage form. The