Chapter 10 – Pure Competition in the Short Run

10-1

Chapter 10 – Pure Competition in the Short Run

McConnell Brue Flynn 21e

DISCUSSION QUESTIONS

1. Briefly state the basic characteristics of pure competition, pure monopoly, monopolistic

competition, and oligopoly. Under which of these market classifications does each of the

following most accurately fit? (a) a supermarket in your hometown; (b) the steel industry; (c) a

Kansas wheat farm; (d) the commercial bank in which you or your family has an account; (e) the

automobile industry. In each case justify your classification. LO1

Chapter 10 – Pure Competition in the Short Run

10-2

(e) Automobile industry: oligopoly. There are the Big Three automakers, so they are

2. Strictly speaking, pure competition is relatively rare. Then why study it? LO2

3. “Even if a firm is losing money, it may be better to stay in business in the short run.” Is this

statement ever true? Under what condition(s)? LO5

4. Consider a firm that has no fixed costs and that is currently losing money. Are there any

situations in which it would want to stay open for business in the short run? If a firm has no fixed

costs, is it sensible to speak of the firm distinguishing between the short run and the long run?

LO5

Chapter 10 – Pure Competition in the Short Run

10-3

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Answer: No, the firm will want to shut down. This follows because the firm is losing

money, but there are no fixed costs. Since there are no fixed costs, only variable cost,

revenue must be less than total variable cost or price is less than average variable cost

(the shut-down rule). In other words, the firm can shut down and lose nothing because

there are no fixed costs or it can keep producing and earn a negative profit.

In a more general sense, a firm with no fixed cost is really in the long run. By definition,

the short run implies there are fixed cost present that the firm cannot get of paying either

implicitly or explicitly. The long run implies all factors and costs can adjust to the

economy.

5. Why is the equality of marginal revenue and marginal cost essential for profit maximization in

all market structures? Explain why price can be substituted for marginal revenue in the MR = MC

rule when an industry is purely competitive. LO5

6. “That segment of a competitive firm’s marginal-cost curve that lies above its average-variable-

cost curve constitutes the short–run supply curve for the firm.” Explain using a graph and words.

LO6

7. LAST WORD If a firm’s current revenues are less than its current variable costs, when should

it shut down? If it decides to shut down, should we expect that decision to be final? Explain using

an example that is not in the book.

Chapter 10 – Pure Competition in the Short Run

10-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Answer: The firm should shut down immediately. If the firm were to continue

production in this case it would be adding to its losses. That is, not only would the firm

have to pay for its fixed cost it would also be paying more for the variable costs in excess

of revenue. In this case, it is best for the firm to just to shut down and take the loss on the

fixed cost (minimize losses).

However, this may only be a temporary case. If the price of the product were to rise then

the revenue may be sufficient to cover the variable costs. The firm will once again start

production because they can start to fill the financial hole generated by the fixed costs.

Examples will vary.

REVIEW QUESTIONS

1. Suppose that the paper clip industry is perfectly competitive. Also assume that the market

price for paper clips is 2 cents per paper clip. The demand curve faced by each firm in the

industry is: LO3

a. A horizontal line at 2 cents per paper clip.

b. A vertical line at 2 cents per paper clip.

c. The same as the market demand curve for paper clips.

d. Always higher than the firm’s MC curve.

Chapter 10 – Pure Competition in the Short Run

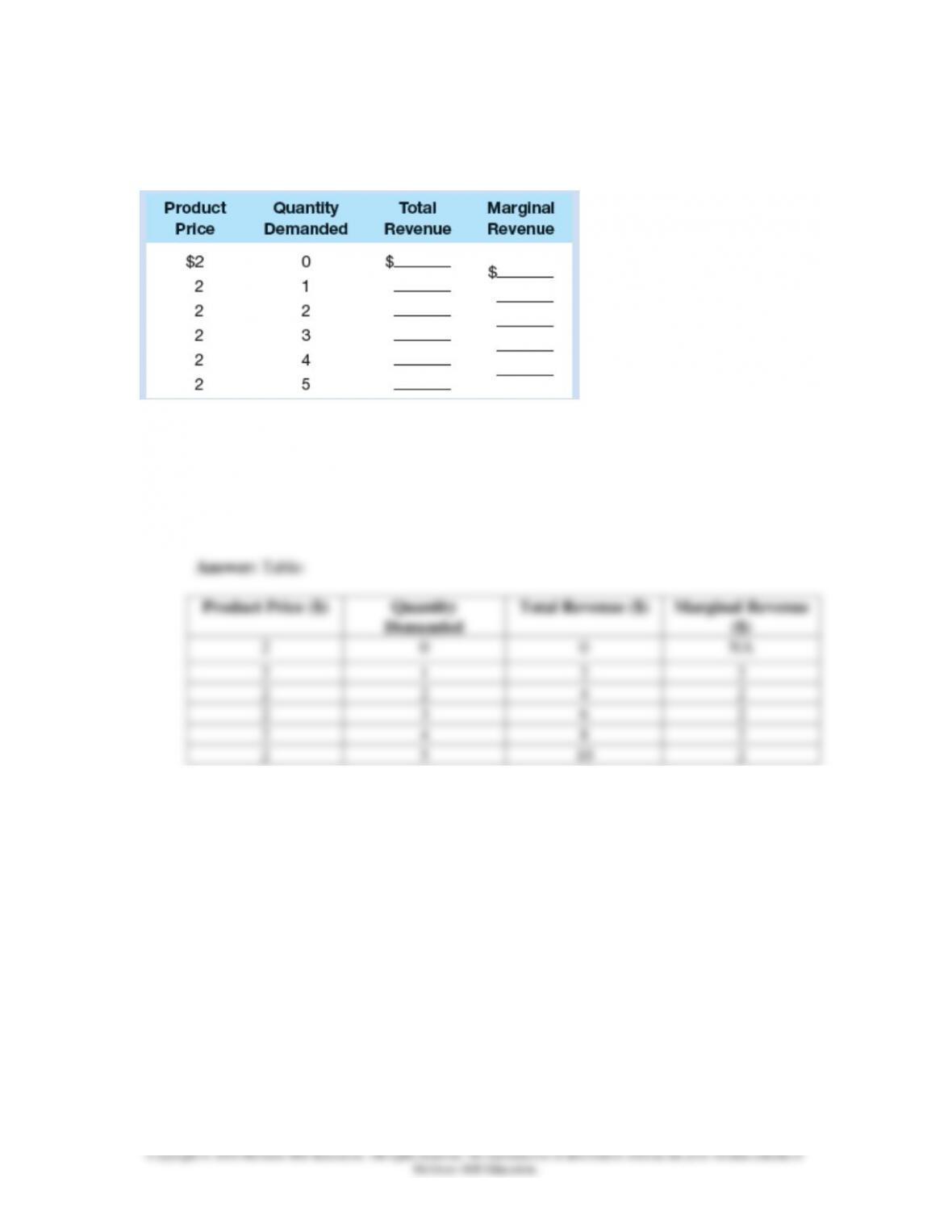

2. Use the following demand schedule to determine total revenue and marginal revenue for each

possible level of sales: LO3

a. What can you conclude about the structure of the industry in which this firm is operating?

Explain.

b. Graph the demand, total-revenue, and marginal-revenue curves for this firm.

c. Why do the demand and marginal-revenue curves coincide?

d. “Marginal revenue is the change in total revenue associated with additional units of output.”

Explain verbally and graphically, using the data in the table.

Chapter 10 – Pure Competition in the Short Run

10-6

a. The industry is purely competitive—this firm is a “price taker.” The firm is so small

3. A purely competitive firm whose goal is to maximize profit will choose to produce the amount

of output at which: LO4

a. TR and TC are equal.

b. TR exceeds TC by as much as possible.

c. TC exceeds TR by as much as possible.

d. None of the above.

10-7

4. If it is possible for a perfectly competitive firm to do better financially by producing rather than

shutting down, then it should produce the amount of output at which: LO5

a. MR < MC.

b. MR = MC.

c. MR > MC.

d. none of the above.

5. A perfectly competitive firm that makes car batteries has a fixed cost of $10,000 per month.

The market price at which it can sell its output is $100 per battery. The firm’s minimum AVC is

$105 per battery. The firm is currently producing 500 batteries a month (the output level at which

MR = MC). This firm is making a _____________ and should _______________ production.

LO5

a. profit; increase

b. profit; shut down

c. loss; increase

d. loss; shut down

Chapter 10 – Pure Competition in the Short Run

10-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Answer: d. loss; shut down.

This firm is making a loss and should shut down production. We know that it is making a

loss because the market price at which it can sell its batteries is less than the minimum

AVC. That implies that its revenue per battery is not even high enough to cover the

variable cost of producing its output. But the situation is even worse because each month

the firm has $10,000 in fixed costs. So if the firm produces output, not only will it be

failing to cover the variable cost of producing output, it will also be failing to cover its

fixed cost of producing output.

The firm should shut down immediately and produce nothing because producing nothing

will minimize the size of its loss. That is because if it produces nothing, it will only lose

$10,000 per month, the value of its fixed cost. By contrast, if it continues to produce

output, it will lose not only its fixed cost but also an additional amount because its

revenues are not even high enough to cover the variable cost of producing output. Thus, it

would lose less money if it shut down production than if it continued producing output.

Better to lose just the fixed-cost amount of $10,000 per month rather than an even larger

amount!

6. Consider a profit-maximizing firm in a competitive industry. For each of the following

situations, indicate whether the firm should shut down production or produce where MR = MC.

LO5

a. P < minimum AVC.

b. P > minimum ATC.

c. Minimum AVC < P < minimum ATC.

Chapter 10 – Pure Competition in the Short Run

10-9

PROBLEMS

1. A purely competitive firm finds that the market price for its product is $20. It has a fixed cost

of $100 and a variable cost of $10 per unit for the first 50 units and then $25 per unit for all

successive units. Does price exceed average variable cost for the first 50 units? What about for

the first 100 units? What is the marginal cost per unit for the first 50 units? What about for units

51 and higher? For each of the first 50 units, does MR exceed MC? What about for units 51 and

higher? What output level will yield the largest possible profit for this purely competitive firm?

(Hint: Draw a graph similar to Figure 10.2 using data for this firm.) LO5

2. A purely competitive wheat farmer can sell any wheat he grows for $10 per bushel. His five

acres of land show diminishing returns because some are better suited for wheat production than

others. The first acre can produce 1,000 bushels of wheat, the second acre 900, the third 800, and

so on. Draw a table with multiple columns to help you answer the following questions. How

many bushels will each of the farmer’s five acres produce? How much revenue will each acre

generate? What are the TR and MR for each acre? If the marginal cost of planting and harvesting

an acre is $7,000 per acre for each of the five acres, how many acres should the farmer plant and

harvest? LO5

Chapter 10 – Pure Competition in the Short Run

10–10

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Answers: The student should end up constructing a table similar to the following.

The farmer should plant and harvest four acres.

Feedback: Consider the following example. A purely competitive wheat farmer can sell

any wheat he grows for $10 per bushel. His five acres of land show diminishing returns

because some are better suited for wheat production than others. The first acre can

produce 1,000 bushels of wheat, the second acre 900, the third 800, and so on. Also

assume the marginal cost of planting and harvesting an acre is $7,000 per acre for each of

the five acres.

Table:

The first step is to calculate the revenue generated by each acre (column 3). Each entry,

the acre’s revenue, is found by multiplying the price per bushel by the acre’s yield. The

revenue generated by the first acre is $10,000 (=$10 x 1,000), the second acre $9,000

(=$10 x 900), the third acre $8,000 (=$10 x 800), etc…

The next step is to calculate total revenue (column 4). Total revenue equals the sum of

revenue generated by each successive acre being cultivated. Total revenue for the first

acre is $10,000, total revenue for first and second acre is $19,000 (=$10,000 + $9,000),

total revenue for the first, second, and third acre is $27,000 (= $10,000 +$ 9,000 +

$8,000), etc…

The final step is to calculate marginal revenue (column 5). Marginal revenue equals the

change in total revenue as each successive acre is cultivated. Marginal revenue for the

first unit is $10,000 because as we move from cultivating zero acres to one acre out total

revenue changes by $10,000. The marginal revenue for the second acre equals $9,000,

which is the total revenue of the second acre minus the revenue generated by the first acre

(=$19,000 – $10,000). etc…

Using our MC=MR rule, the farmer should plant and harvest 4 acres. Marginal revenue

for the fourth acre equals $7,000 and the marginal cost equals $7,000.

Chapter 10 – Pure Competition in the Short Run

3. Karen runs a print shop that makes posters for large companies. It is a very competitive

business. The market price is currently $1 per poster. She has fixed costs of $250. Her variable

costs are $1,000 for the first thousand posters, $800 for the second thousand, and then $750 for

each additional thousand posters. What is her AFC per poster (not per thousand!) if she prints

1,000 posters? 2,000? 10,000? What is her ATC per poster if she prints 1,000? 2,000? 10,000? If

the market price fell to 70 cents per poster, would there be any output level at which Karen would

not shut down production immediately? LO5

10–12

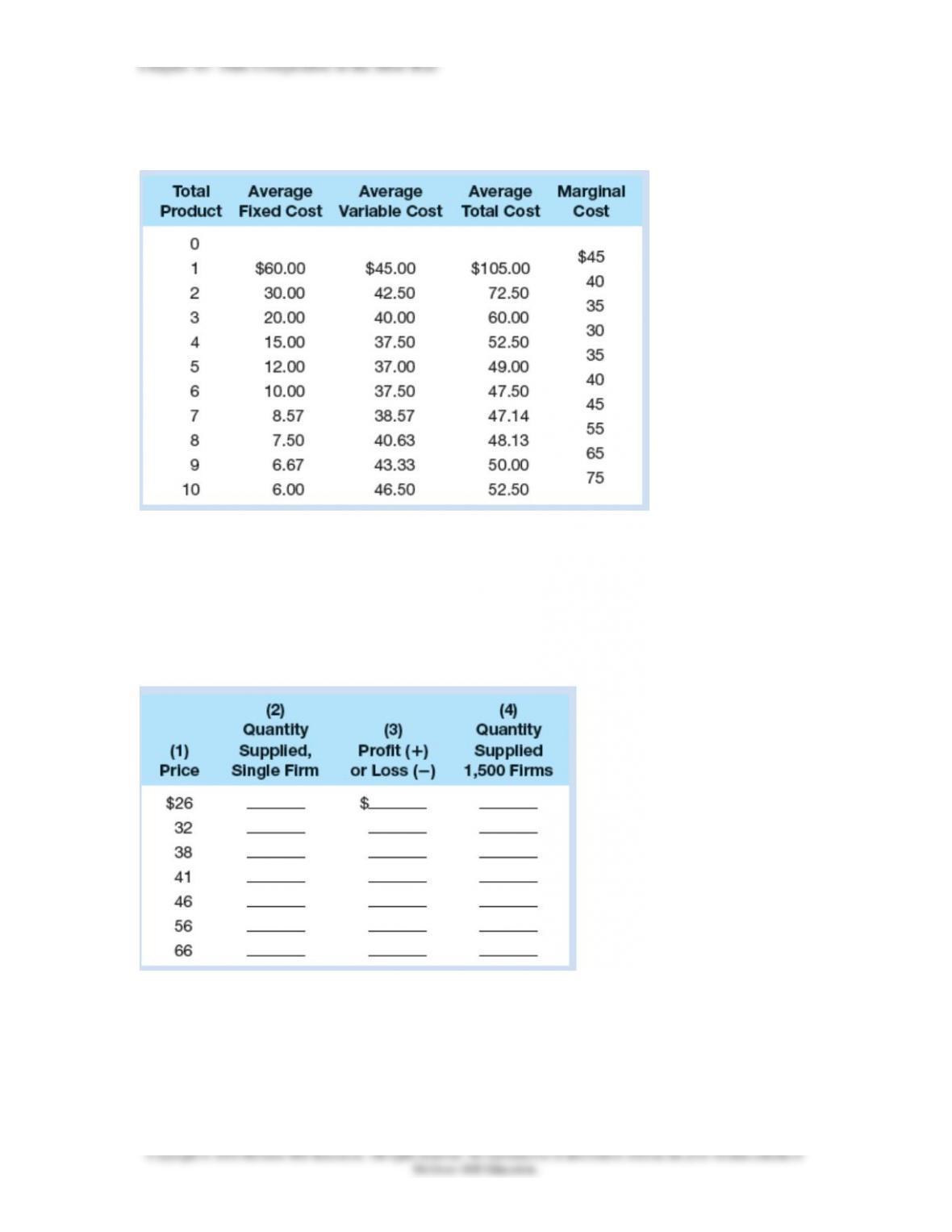

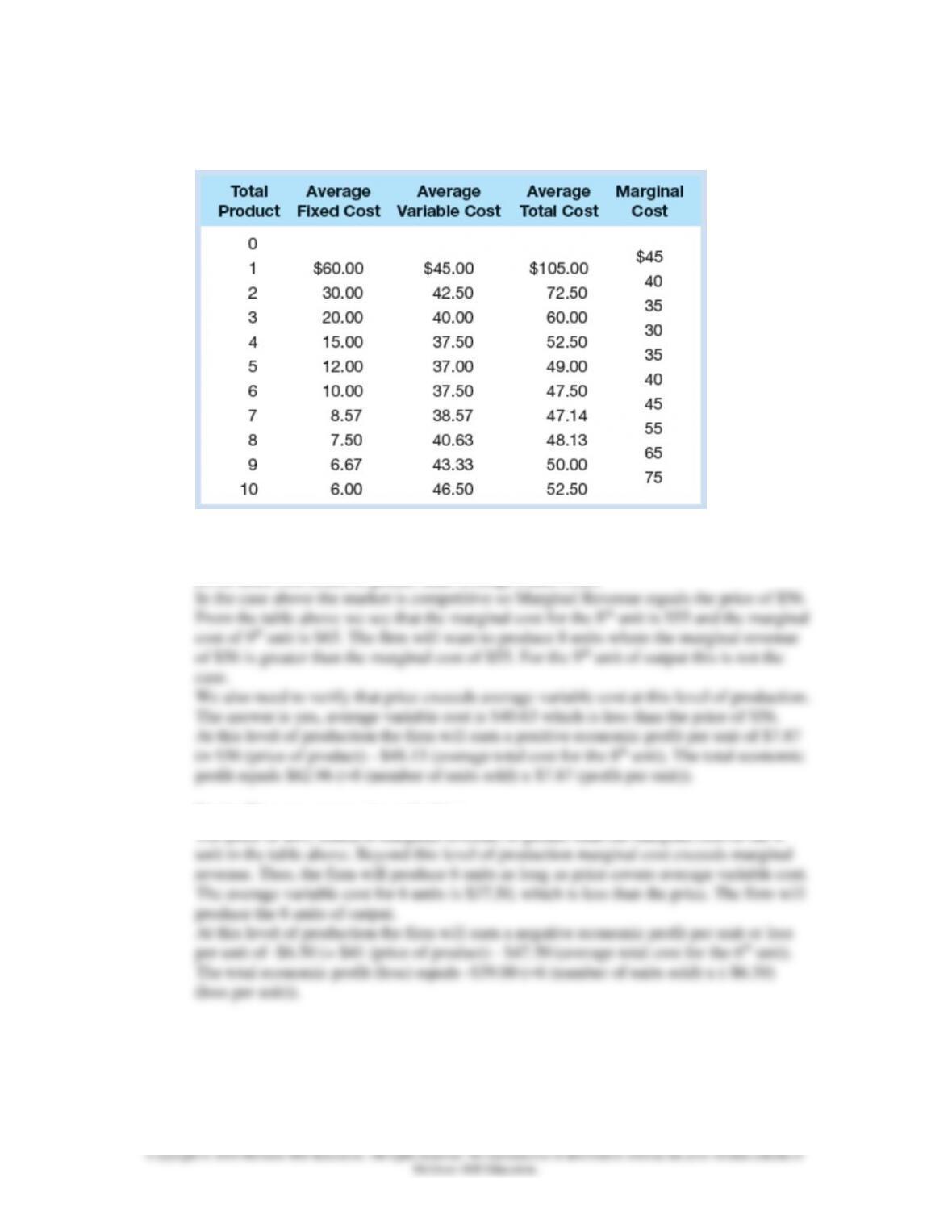

4. Assume the following cost data are for a purely competitive producer: LO5

a. At a product price of $56, will this firm produce in the short run? If it is preferable to produce,

what will be the profit-maximizing or loss-minimizing output? What economic profit or loss will

the firm realize per unit of output?

b. Answer the questions of 4a assuming product price is $41.

c. Answer the questions of 4a assuming product price is $32.

d. In the table below, complete the short-run supply schedule for the firm (columns 1 and 2) and

indicate the profit or loss incurred at each output (column 3).

e. Now assume that there are 1,500 identical firms in this competitive industry; that is, there are

1,500 firms, each of which has the cost data shown in the table. Complete the industry supply

schedule (column 4).

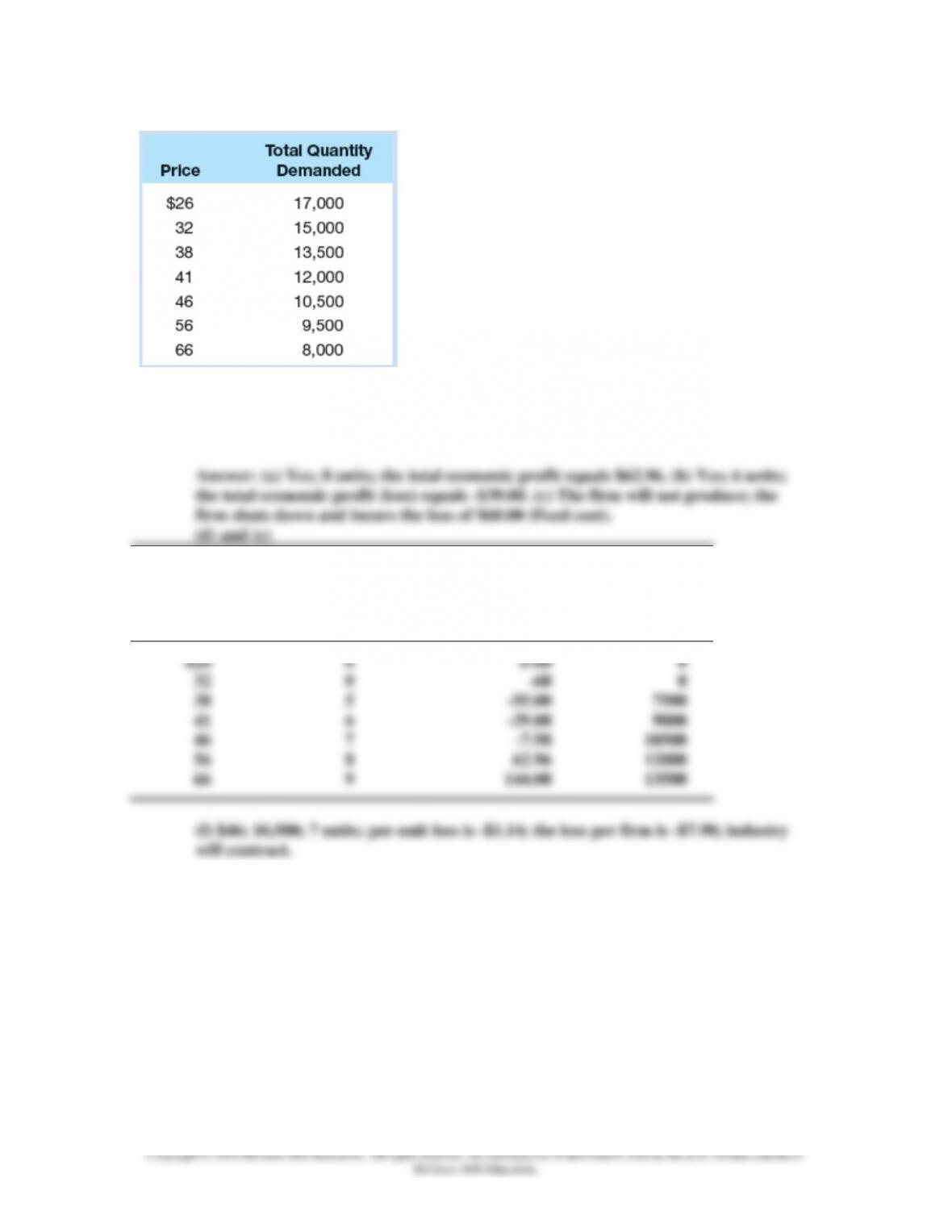

f. Suppose the market demand data for the product are as follows:

Chapter 10 – Pure Competition in the Short Run

10–13

What will be the equilibrium price? What will be the equilibrium output for the industry? For

each firm? What will profit or loss be per unit? Per firm? Will this industry expand or contract in

the long run?

(1)

Price

(2)

Quantity

supplied,

single firm

(3)

Profit (+)

or loss (-)

(4)

Quantity

supplied,

1500 firms

$26

32

38

41

46

56

66

0

0

5

6

7

8

9

$-60

–60

-55.00

-39.00

-7.98

62.96

144.00

0

0

7500

9000

10500

12000

13500

Chapter 10 – Pure Competition in the Short Run

10–14

Feedback:

Part a: The rule is to produce at the level of output where Marginal Revenue equals (or is

greater than if we are using integers) Marginal Cost as long as revenue is sufficient to

cover fixed cost (Price is greater than Average Fixed Cost).

Part b: The same process is applied here.

The price of $41, which is marginal revenue, is greater than the marginal cost of the 6th

Chapter 10 – Pure Competition in the Short Run

Part c: We could go through the same exercise here. However, by recognizing that the

price of $32 is below average variable cost at all levels of production the firm will not

produce. Thus, the firm shuts down and incurs the loss of $60.00 (fixed cost).

Part d and e:

(1)

Price

(2)

Quantity

supplied,

single firm

(3)

Profit (+)

or loss (-)

(4)

Quantity

supplied,

1500 firms

$26

32

38

41

46

56

66

0

0

5

6

7

8

9

$-60

–60

-55.00

-39.00

-7.98

62.96

144.00

0

0

7500

9000

10500

12000

13500

Part f: To determine the equilibrium price we look at the total quantity demanded

schedule and the total quantity supplied schedule (for the 1,500 firms above) to find the

price where quantity demanded equals quantity supplied.