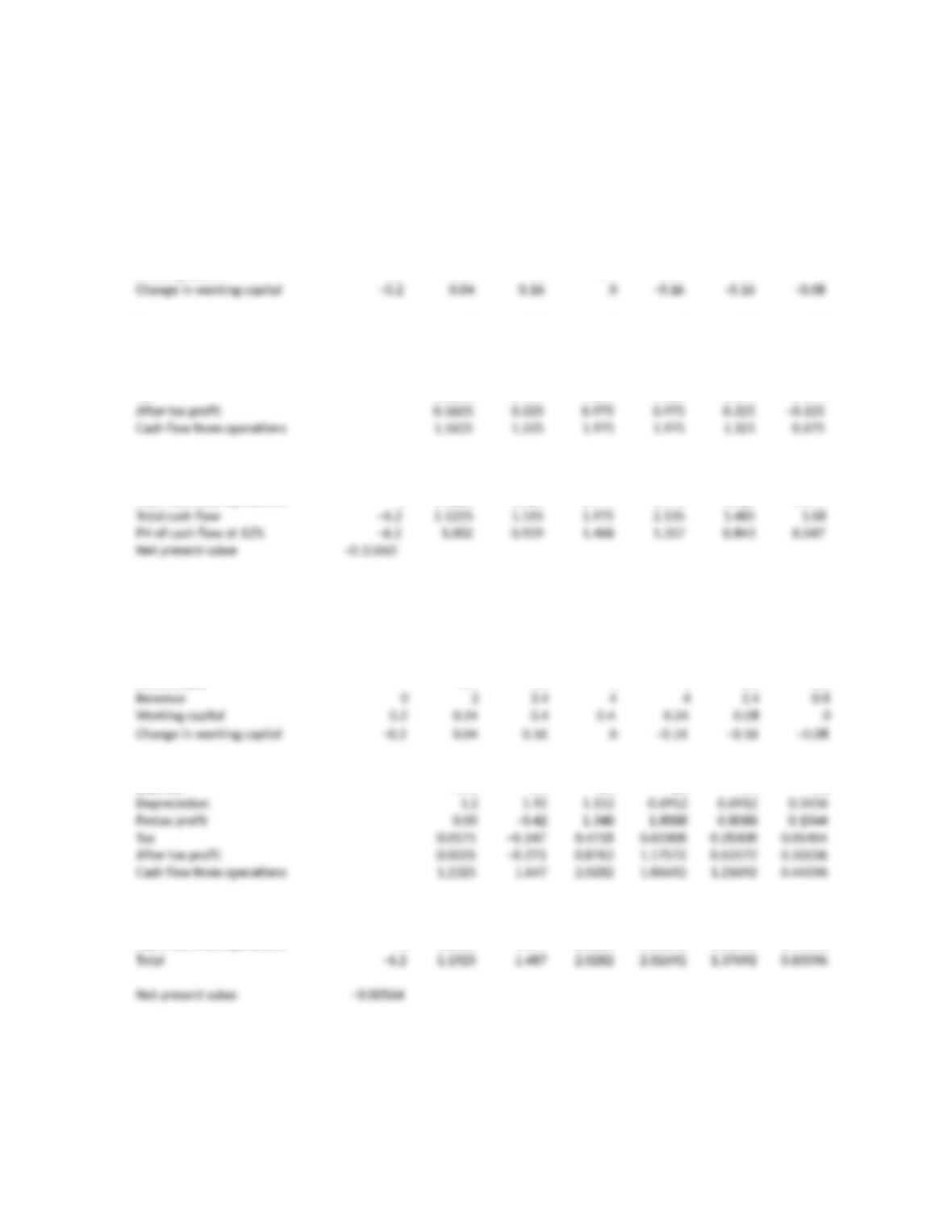

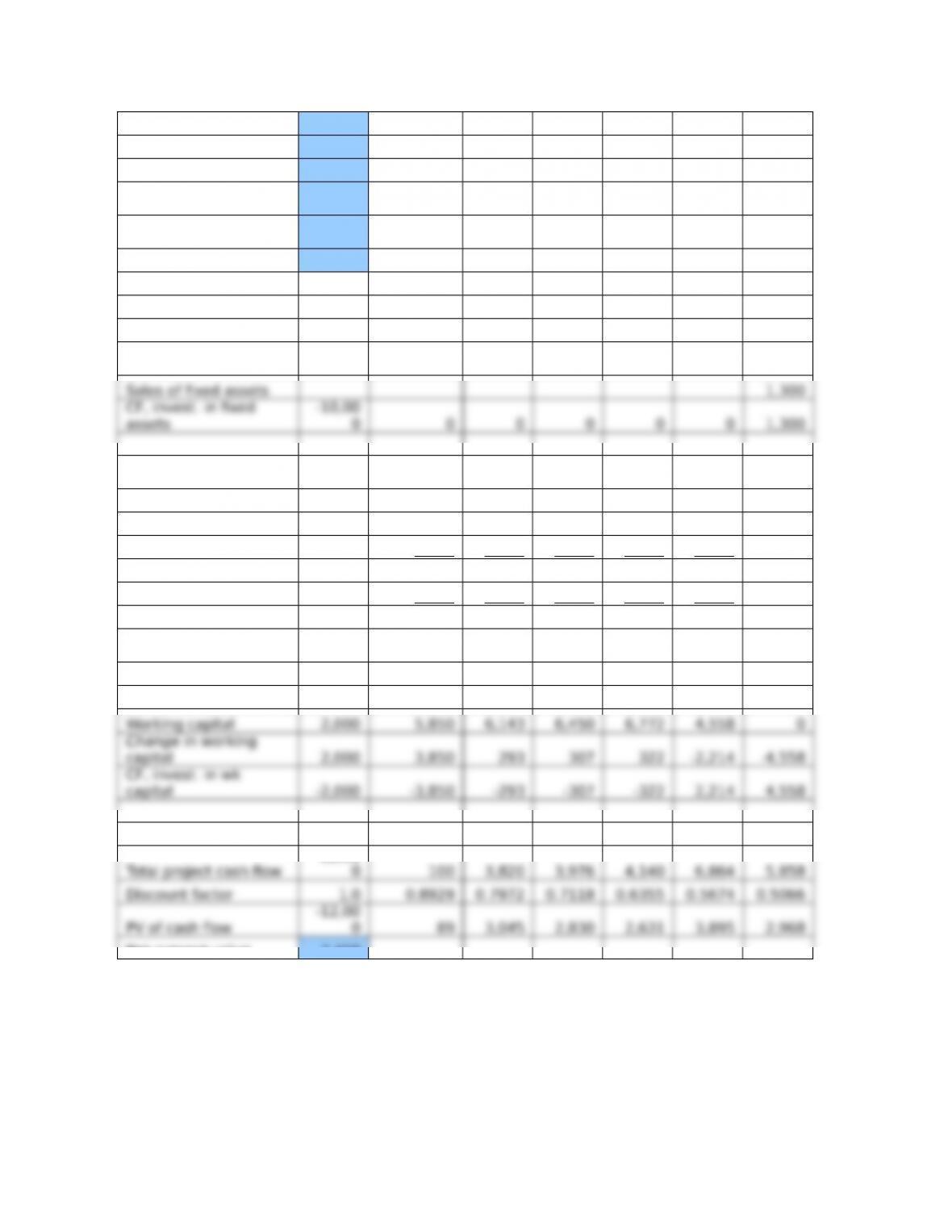

Year 0 1 2 3 4 5 6

Sales (traps) 0.5 0.6 1 1 0.6 0.2

Revenue 0 2 2.4 4 4 2.4 0.8

Working capital 0.2 0.24 0.4 0.4 0.24 0.08 0

Revenues 2 2.4 4 4 2.4 0.8

Expense 0.75 0.9 1.5 1.5 0.9 0.3

depreciation 1 1 1 1 1 1

Pretax profit 0.25 0.5 1.5 1.5 0.5 –0.5

Tax 0.0875 0.175 0.525 0.525 0.175 –0.175

Cash 0ow: capital invest. –6 0.325

Cash 0ow from WC –0.2 –0.04 –0.16 0 0.16 0.16 0.08

Cash 0ow from operation 0 1.1625 1.325 1.975 1.975 1.325 0.675

Year 0 1 2 3 4 5 6

Sales (traps) 0.5 0.6 1 1 0.6 0.2

Revenues 2 2.4 4 4 2.4 0.8

Expense 0.75 0.9 1.5 1.5 0.9 0.3

Cash 0ow: capital invest. –6 0.325

Cash 0ow from WC –0.2 –0.04 –0.16 0 0.16 0.16 0.08

Cash 0ow from operation 0 1.2325 1.647 2.0282 1.86692 1.21692 0.44596

1. All cash flows are in millions of dollars. Sales price of machinery in year 6 is shown on

an after-tax basis as a positive cash flow on the capital investment line.

a.

…

b. ….

….

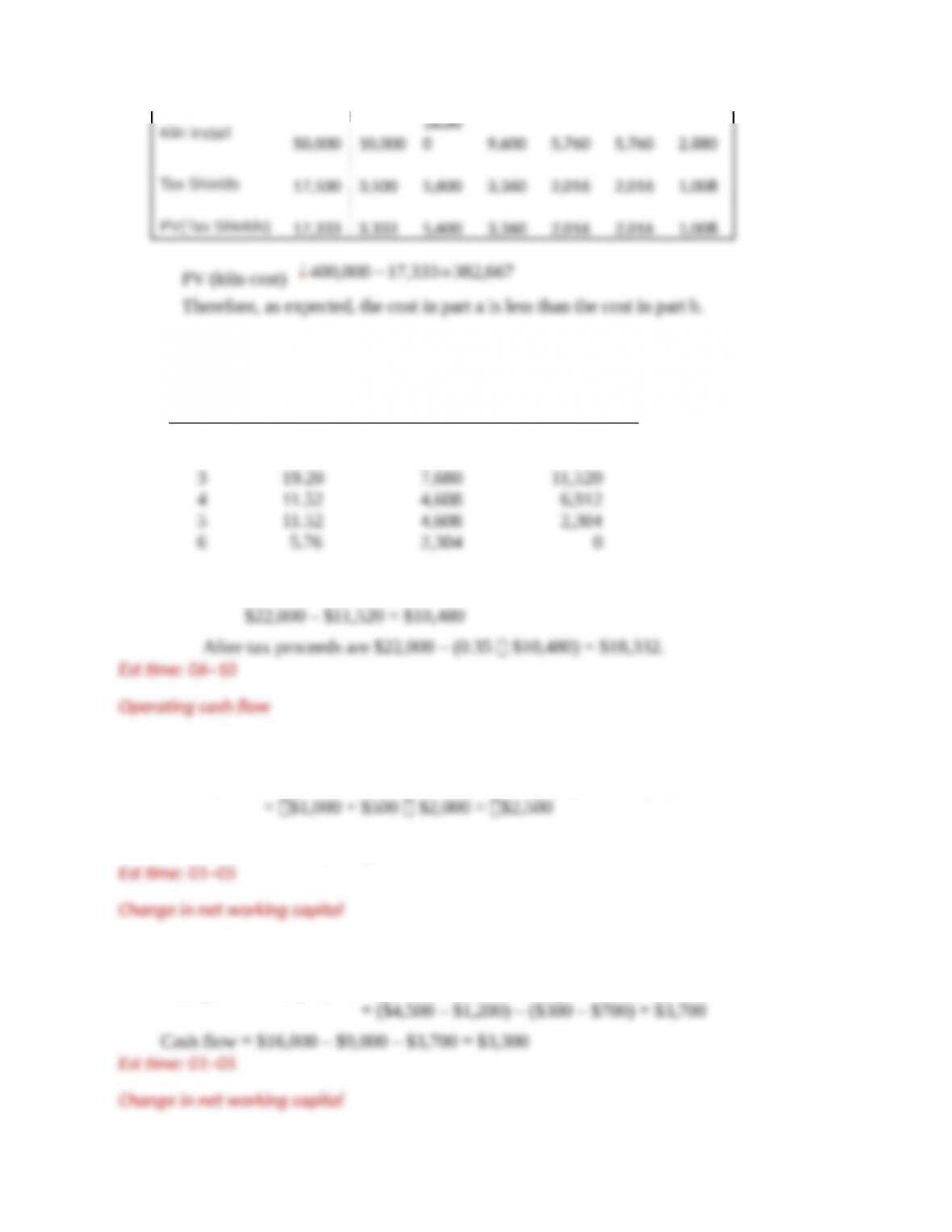

Using the 5-year MACRS schedule, the net present value increases by $111,010 (=

116,650 – 5,640).

Est time: 11–15

9–

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

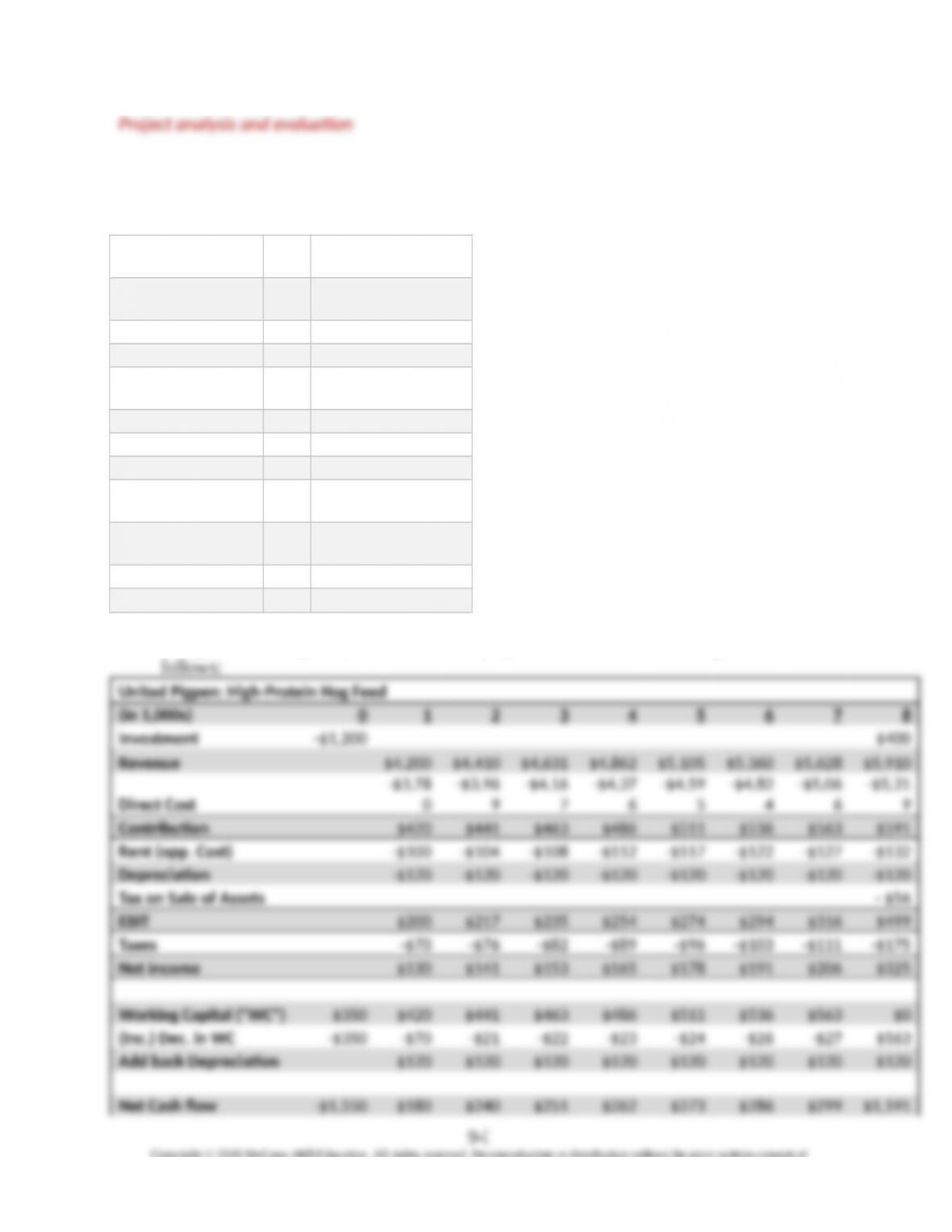

2. The assumptions for the Pigpen project are laid out in the table below:

Investment $1.

2

million

Revenue $4.

2

million

Rev growth 5% per annum

Manufacture costs 90% of sales

Rent (opp. Cost) $10

0

thousand

Rent Growth 4% per annum

Dep’n Life 10 years

Tax Rate 35% marginal

Plant Salet=8 $40

0

thousand

WC investment $35

0

thousand

WC ongoing 10% of sales

Cost of Capital 12%

Using these assumptions, we can schedule project cash flows across the 8 year horizon as

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Est time: 11–15

Project analysis and evaluation

3. While depreciation is a noncash expense, it has an impact on net cash flow because of its

impact on taxes. Every dollar of depreciation expense reduces taxable income by one

4. Depreciation expense per year = $40/5 = $8 million

5. Using the 7-year MACRS depreciation schedule, after 5 years the machinery will be

written down to 22.30% of its original value: 0.2230 $10 million = $2.230 million

If the machinery is sold for $4.5 million, the sale generates a taxable gain of $2.270

million.

6. a. All values should be interpreted as incremental results from making the purchase.

Earnings before depreciation $1,500

9–

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

b. NPV = –$4,800 + [$1,300 annuity factor (16%, 6 years)]

7. a. If Ideal China expenses the installation costs immediately, then the present value of the

16,00

8. a.

Year MACRS (%) Depreciation Book Value

(end of year)

1

20.00

$ 8,000

$32,000

2 32.00 12,800 19,200

b. If the machine is sold for $22,000 after 3 years, sales price exceeds book value by:

9. a. NWC = accounts receivable + inventory accounts payable

b. Cash flow = $36,000 $24,000 + $2,500 = $14,500

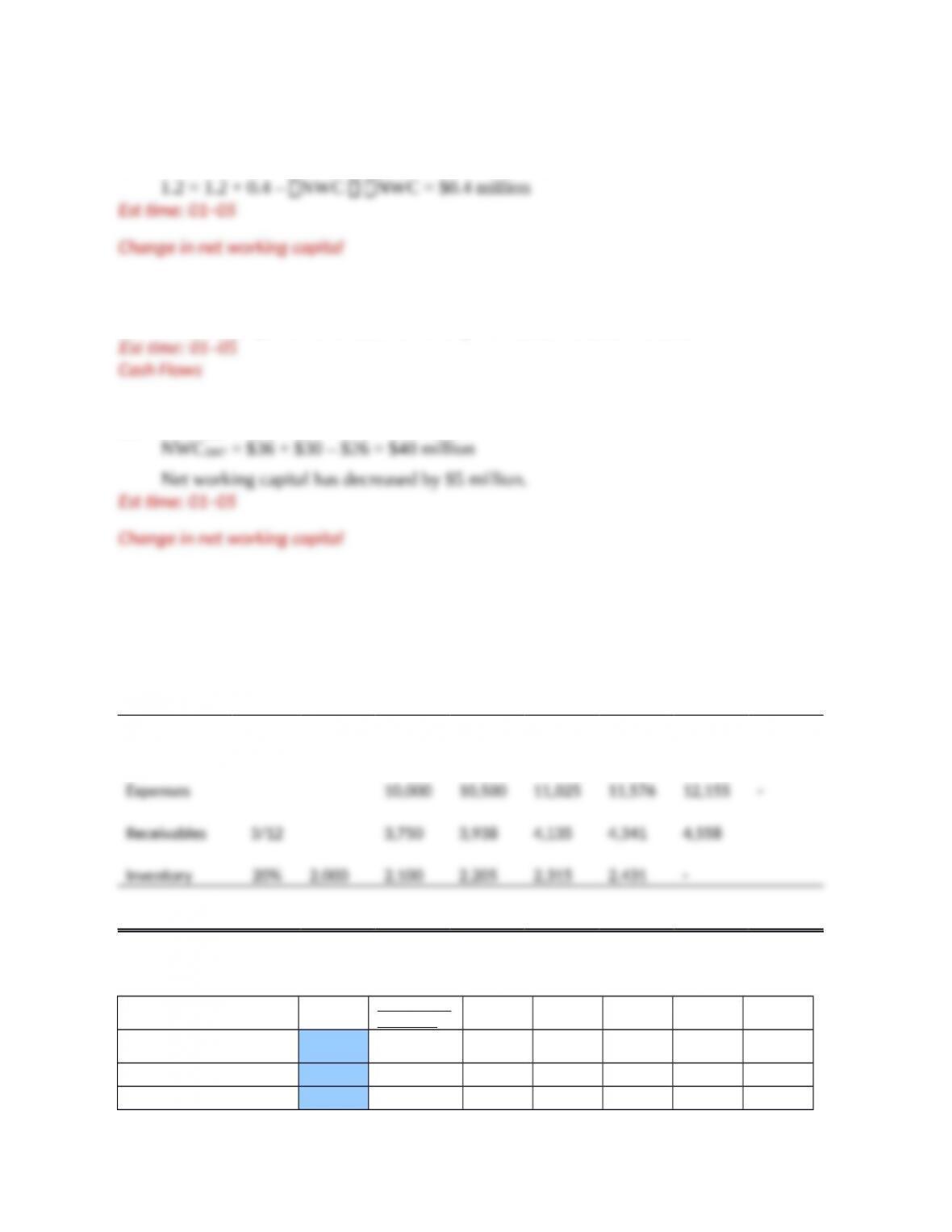

10. Change in working capital = accounts receivable – accounts payable

9–

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

11. Cash flow = net income + depreciation – increase in NWC

12. Cash flow = profit – increase in inventory = $10,000 – $1,000 = $9,000

13. NWC2016 = $32 + $25 – $12 = $45 million

14.

a. Lower. The NPV decreases from $4,223 to $3,458. See the valuation used in part c.

b.

0 1 2 3 4 5 6

Revenue

15,000

15,750

16,538

17,364

18,233

–

Working Capital

2,000

5,850

6,143

6,450

6,772

4,558

A. Inputs

Spreadshe

et Name

Initial Investment 10,000

Investmen

t

Salvage value 2,000 Salvage

Initial revenue 15,000 Initial_rev

9–

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Initial expenses 10,000 Intial_exp

Inflation rate 0.05 Inflation

Discount rate 0.12 Disc_rate

Acct receiv. as % of

sales 1/4 A_R

Inven. as % of

expenses 0.2 Inv_pct

Tax rate 0.35 Tax_rate

Year: 0 1 2 3 4 5 6

B. Fixed assets

Investments in fixed

assets 10,000

C. Operating cash

ow

Revenues 15,000 15,750 16,538 17,364 18,233

Expenses 10,000 10,500 11,025 11,576 12,155

Depreciation 2,000 2,000 2,000 2,000 2,000

Pretax pro)t 3,000 3,250 3,513 3,788 4,078

Tax 1,050 1,138 1,229 1,326 1,427

profit after tax 1,950 2,113 2,283 2,462 2,650

Cash flow from

operations 3,950 4,113 4,283 4,462 4,650

D. Working capital

E. Project valuation

-12,00

Net present value 3,458

Est time: 06–10

Net Present Value

9–

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

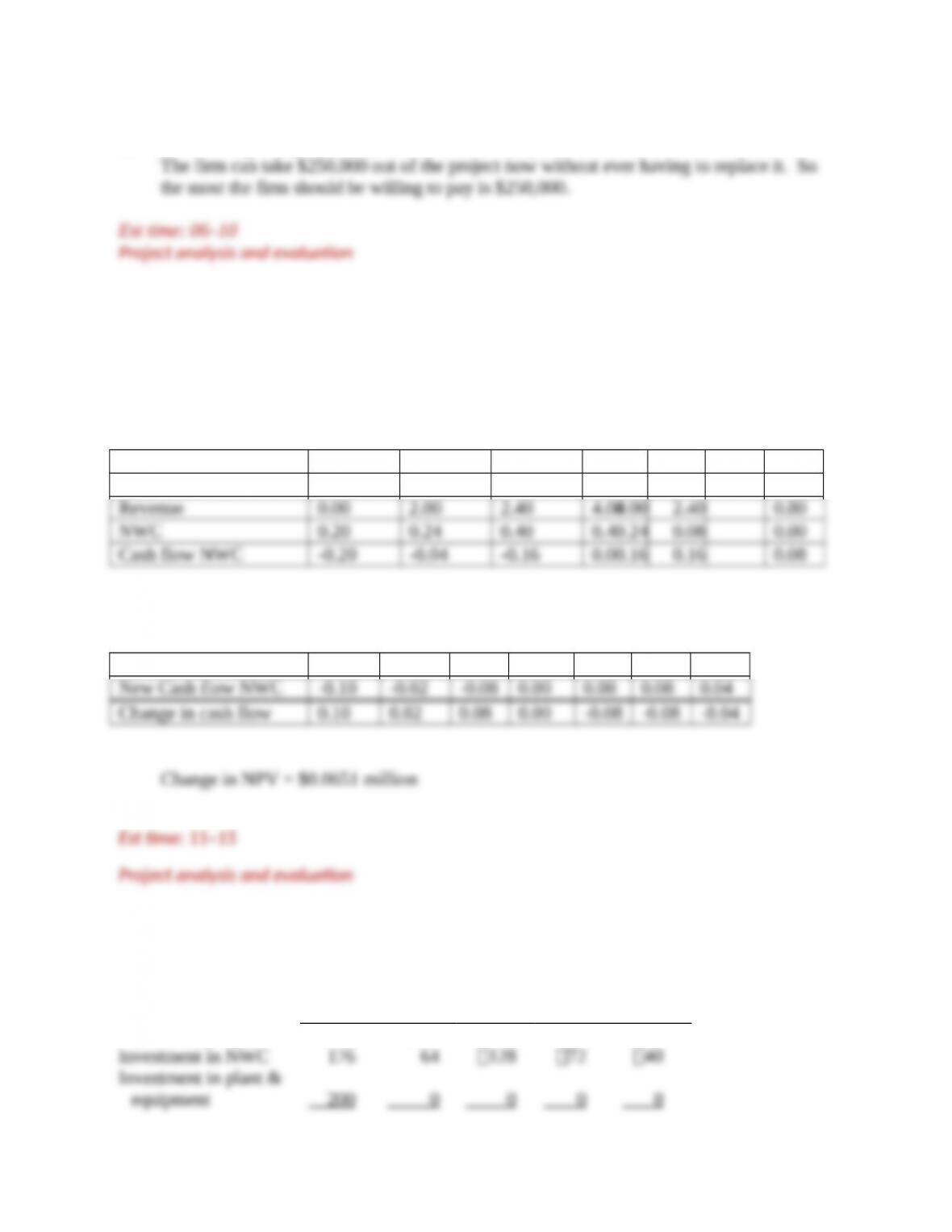

15. If the savings are permanent, then the inventory system is worth $250,000 to the firm.

16. Some values below may show as rounded for display purposes, though unrounded

numbers should be used for actual calculations.

All cash flows are in millions of dollars. Sales price of machinery in year 6 is shown on an

after-tax basis as a positive cash flow on the capital investment line.

Year 0 1 2 3 6

Sales units 0.00 0.50 0.60 1.001.00 0.60 0.20

If working capital requirements were only one-half of the expected amount, then the

working capital cash-flow forecasts would change as follows:

New NWC 0.10 0.12 0.20 0.20 0.12 0.04 0.00

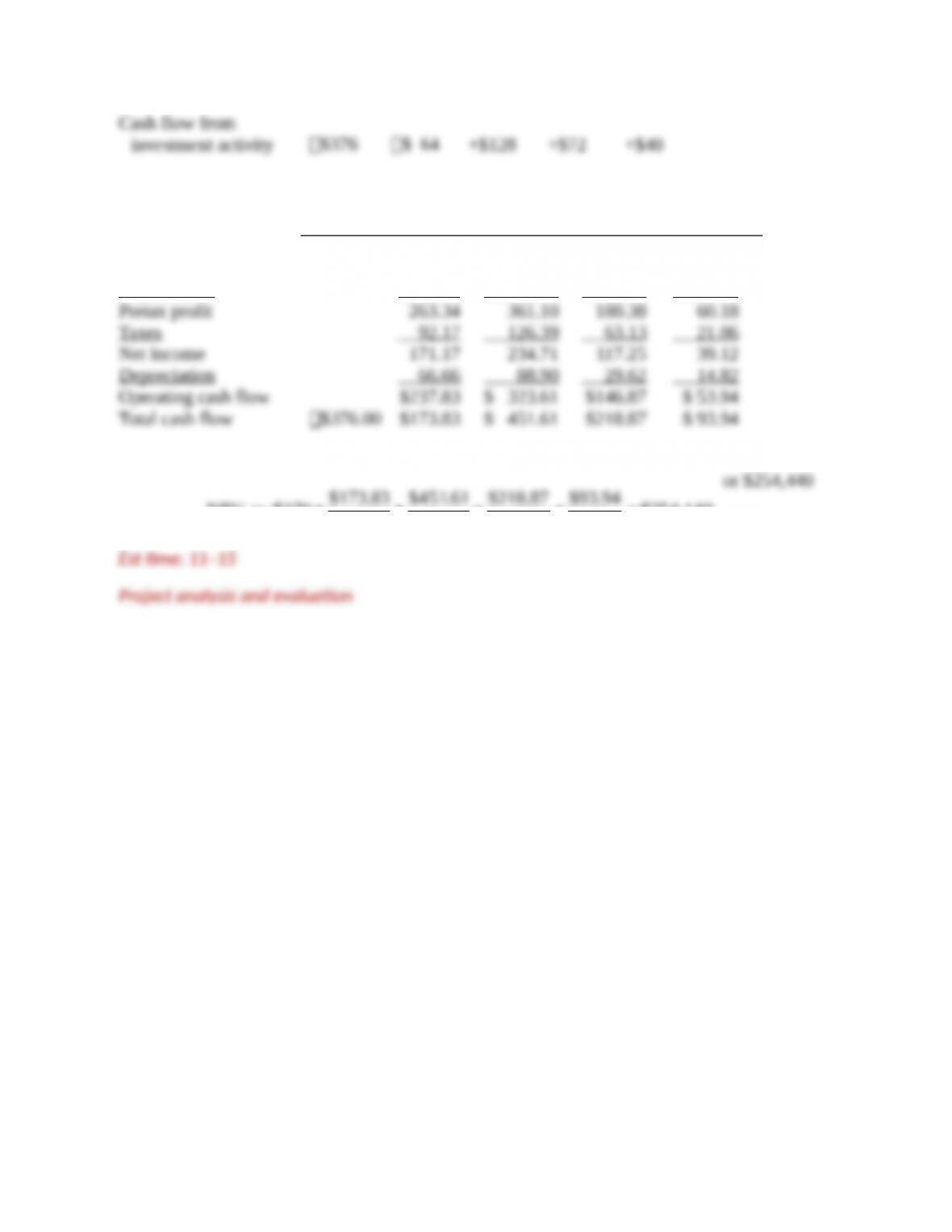

17.

All figures in thousands

01234

Net working capital

$176

$240

$112

$40

$ 0

9–

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

All figures in thousands

0 1 2 3 4

Revenue

$880.00

$1,200.00

$560.00

$200.00

Cost 550.00 750.00 350.00 125.00

Depreciation 66.66 88.90 29.62 14.82