Solutions to Chapter 8

Net Present Value and Other Investment Criteria

1. NPVA = –$200 + [$80 annuity factor (11%, 4 periods)]

2. Choose Project A, the project with the higher NPV.

3. NPVA = –$200 + [$80 annuity factor (16%, 4 periods)]

4. IRRA = discount rate (r), which is the solution to the following equation:

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

5. No. Even though project B has the higher IRR, its NPV is lower than that of project A

when the discount rate is lower (as in Problem 1) and higher when the discount rate is higher

6. The profitability indexes are as follows:

7. In this case, with equal initial investments, both the profitability index and NPV give

8. Project A has a payback period of $200/$80 = 2.5 years.

9. No. In this case, Project A has the higher NPV and project B has the higher payback

8-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

10. a.

b.

If the discount rate rises above the IRR of 15.34% the project is no longer attractive

11. NPV = $2.2 billion + [$0.3 billion annuity factor (r, 15 years)] [$0.9 billion/(1 +

r)15]

12. NPV9% = –$20,000 + [$4,000 annuity factor (9%, 8 periods)]

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

13. a. r = 0% NPV = –$6,750 + $4,500 + $18,000 = $15,750

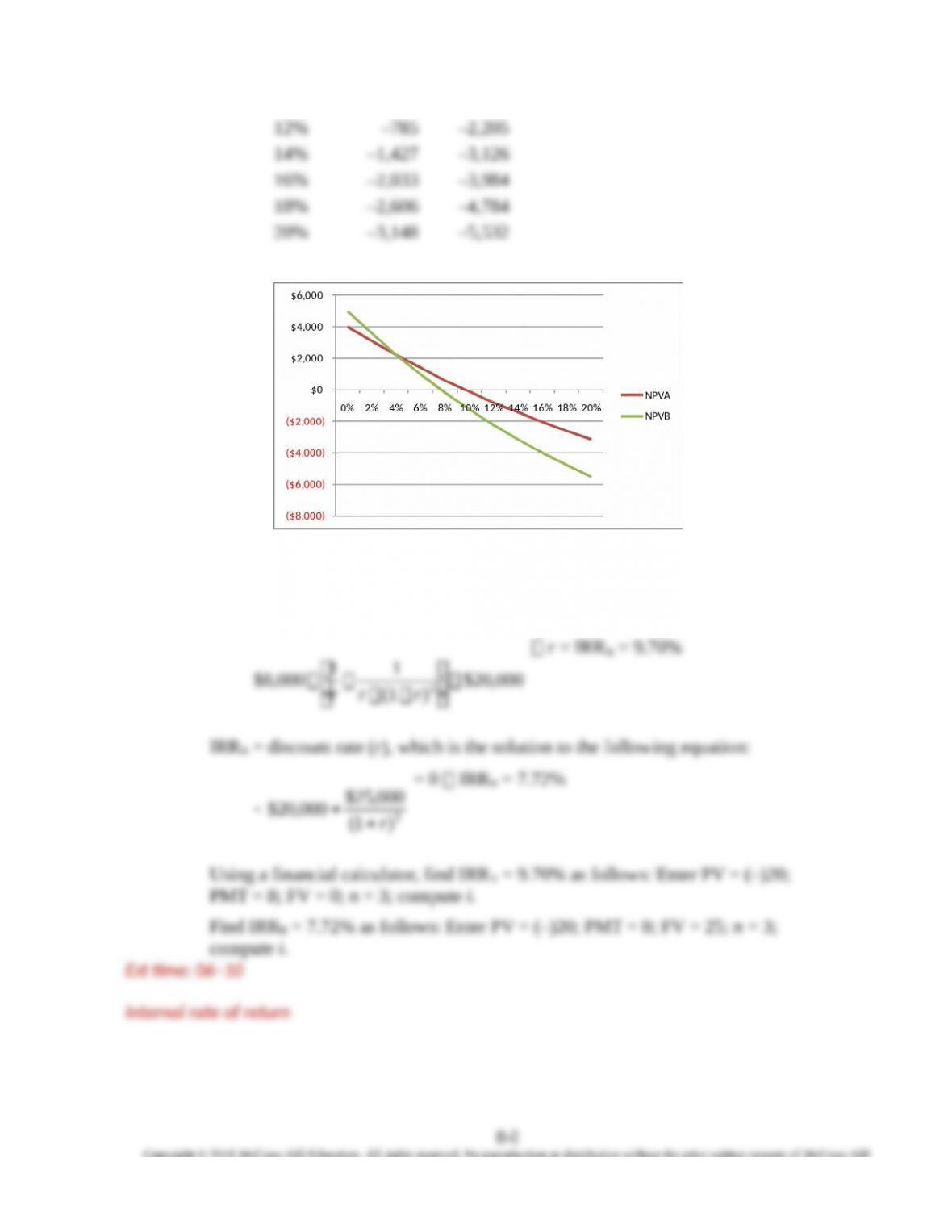

14. a. NPV for each of the two projects, at various discount rates, is tabulated below.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

From the NPV profile, it can be seen that Project A is preferred over Project B if

the discount rate is above 4%. At 4% and below, Project B has the higher NPV.

b. IRRA = discount rate (r), which is the solution to the following equation:

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

15. a. Present value =

Cash flow at end of year $5,000 $100, 000

Discount rate – growth rate 0.10 0.05

= =

–

b. Recall that the IRR is the discount rate that makes NPV equal to zero:

16.

40.1$

)12.1(

60$

12.1

60$

100$NPV 2

17.

a.

Time Cash flow

0

$ 5 million

1 30 million

8-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

2

28 million

The graph below shows a plot of NPV as a function of the discount rate.

NPV = 0 when r equals (approximately) either 15.61% or 384.39%. These are the

two IRRs.

0% 50% 100% 150% 200% 250% 300% 350% 4 00% 4 50% 500%

-4

-3

-2

-1

0

1

2

3

4

Disco unt rat e

NPV

b.

Discount Rate NPV Develop?

10% $0.868 million No

18.

09.029,2$

12.1

500,8$

12.1

500,7$

000,10$NPV 32

8-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

19. IRRA = discount rate (r), which is the solution to the following equation:

20.

70.197$

)12.1(

000,11$

12.1

000,4$

000,5$NPV

2

21. a. The following table shows the NPV profile of the project. NPV is zero at an interest

rate between 7% and 8%, and it is also equal to zero at an interest rate between 33% and 34%.

These are the two IRRs of the project. You can use your calculator to confirm that the two

IRRs are, more precisely, 7.16% and 33.67% (as shown below the table).

Discount

Rate NPV

Discount

Rate NPV

0.00 –2.00 0.21 0.82

8-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

c.

At 20% the NPV is:

840.0$

20.1

40$

20.1

20$

20.1

20$

20.1

20$

22$NPV

432

Since the NPV is positive, the project is attractive.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

22.

38.680,2$

09.1

000,5$

09.1

000,5$

09.1

000,3$

09.1

000,3$

000,10$NPV

432

23. a. The net present values of the project cash flows are:

58.345$

)22.1(

200,1$

22.1

000,2$

100,2$NPV

2

A

31.241$

)22.1(

728,1$

22.1

440,1$

100,2$NPV

2

B

The initial investment for each project is $2,100.

Profitability index (A) = $345.58/$2,100 = 0.1646

Profitability index (B) = $241.31/$2,100 = 0.1149

b. You should undertake both projects, as each has a positive profitability index.

If capital rationing limits your choice, you should undertake project A for its higher

profitability index.

Est me: 06–10

Profitability index

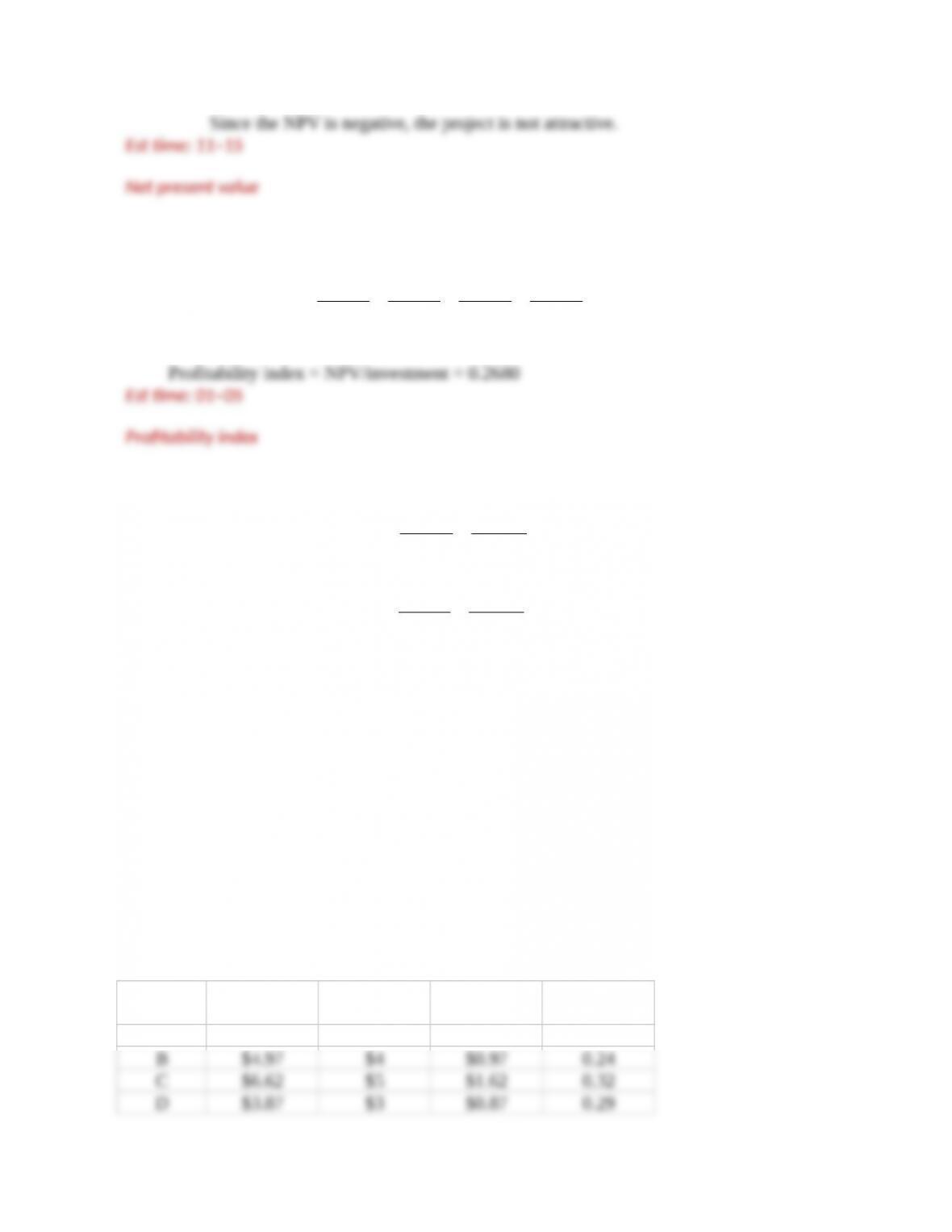

24. a. First, find the profitability index of each project.

Project PV of

Cash flow

Investment NPV Profitability

Index

A

$3.79

$3

$0.79

0.26

8-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

b. All the projects have positive NPV, so all will be chosen if there is no capital

8-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.