Solutions to Chapter 7

Valuing Stocks

1. a. False. The bid price is always lower relative to the ask price, resulting the bid-ask spread

2. – Internet exercise; answers will vary.

3. a. Georgina will receive the bid price of $103 for the 100 shares.

4. P/E ratio = price/earnings

5. The annual dividend is $2 4 = $8.

6. –Internet exercise; answers will vary.

7. –Internet exercise; answers will vary.

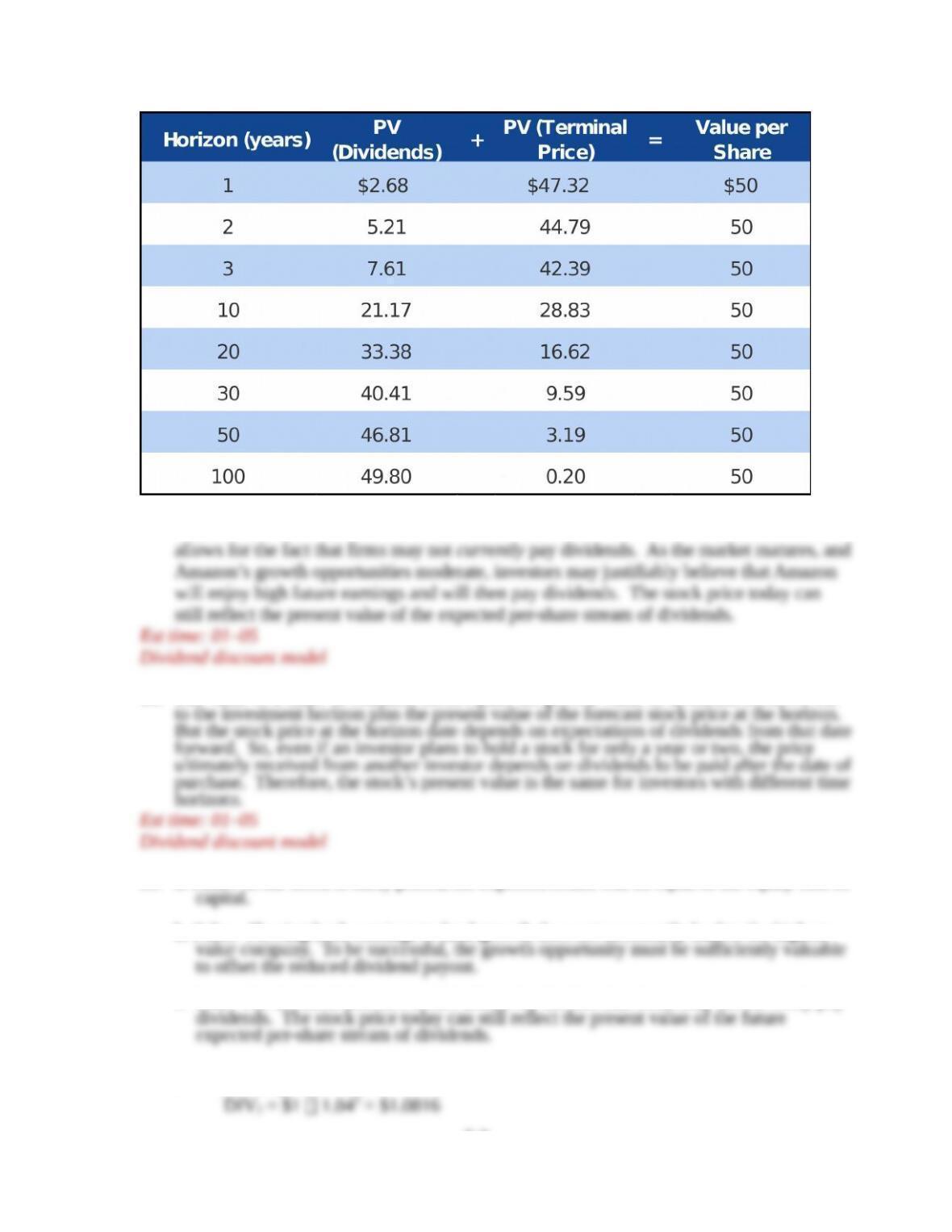

8. The table assuming a growth rate of only 6% per annum is recreated below. The

9. No, this does not invalidate the dividend discount model. The dividend discount model

10. The value of a share of common stock equals the present value of dividends received out

11. a. False. If the stock is fairly priced, the expected return will be equal to the equity cost of

b. False. Plowing back earnings to fund growth does not necessarily lead to the highest

c. True. The dividend discount model allows for the fact that firms may not currently pay

12. a. DIV1 = $1 1.04 = $1.04

7-2

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

b. P0 =

00.13$

04.012.0

04.1$DIV

1

gr

c. P3 =

6237.14$

04.012.0

04.11249.1$DIV

4

gr

d. Your payments will be:

Year 1 Year 2 Year 3

DIV $1.04 $1.0816 $ 1.1249

e.

Year 1 Year 2 Year 3

13. The preferred stock pays a level perpetuity of dividends. The expected dividend next

year is the same as this year’s dividend ($8).

a. $8.00/0.12 = $66.67

14.

g

14.0

5$

50$

%0.404.0

50$

5$

14.0 g

7-3

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

15. . g = return on equity plowback ratio = 0.15 0.40 = 0.06 = 6.0%

%0.1616.006.0

40

4

06.0

4

40

r

r

Est time: 01-05

Constant-growth stock

16.

a.

50.31$

05.015.0

05.13$DIV

1

0

gr

P

b.

45$

05.012.0

05.13$

0

P

The lower discount rate makes the present value of future dividends higher.

Est time: 01–05

Constant-growth stock

17.

a. r = DIV1/P0 + g = [($1.64 1.03)/27] + 0.03 = 0.0926 = 9.26%

19.

a. P0 = DIV1/(r g) = $3/[0.15 – (0.10)] = $3/0.25 = $12

7-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

c. Expected rate of return =

%0.15150.0

12$

)12$80.10($3$gain capitalDIV

0

1

P

20.

00.40$

015.0

6$

0

P

(ii) Reinvest 40%:

43.51$

)40.02.0(15.0

60.3$

0

P

PVGO = $51.43 – $40.00 = $11.43

(iii) Reinvest 60%:

00.80$

)60.02.0(15.0

40.2$

0

P

c. In part (a), the return on reinvested earnings is equal to the discount rate. Therefore,

the NPV of the firm’s new projects is zero, and PVGO is zero in all cases, regardless

7-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

21.

Stock A Stock B

a. Payout ratio $1/$2 = 0.50 $1/$1.50 = 0.67

24. a. P0 = DIV1/(r g)

b. P0 = $3/(0.165 0.04) = $24

25. a. DIV1 = $2.00 PV = $2/1.10 = $1.818

b. This could not continue indefinitely. If it did, the stock would be worth an infinite

26. a. Book value = $200 million

7-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

27. a.

10.18$

)10.1(

20$50.1$

)10.1(

25.1$

10.1

00.1$

32

0

P

7-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.