1. a. At a price of $1,200 and remaining maturity of 9 years, find the bond’s yield to

b. Rate of return =

%61.30

980$

)980$200,1($80$

Est time: 01–05

Bond yields and returns

2. a.

000,1$

09.1

000,1$

)09.1(09.0

1

09.0

1

90$Price

99

b. Rate of return =

%91.0

100,1$

)100,1$000,1($90$

c. The rate of return will be slightly higher above −.91%, since the midyear coupon can

be reinvested:

$45+$45×(1.09).5+($1,000−$1,100)

3.

99.907$

045.1

000,1$

)045.1(045.0

1

045.0

1

40$PV

4040

0

83.829$

05.1

000,1$

)05.1(05.0

1

05.0

1

40$PV

3939

1

Rate of return =

%19.40419.0

99.907$

)99.907$83.829($40$

6-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

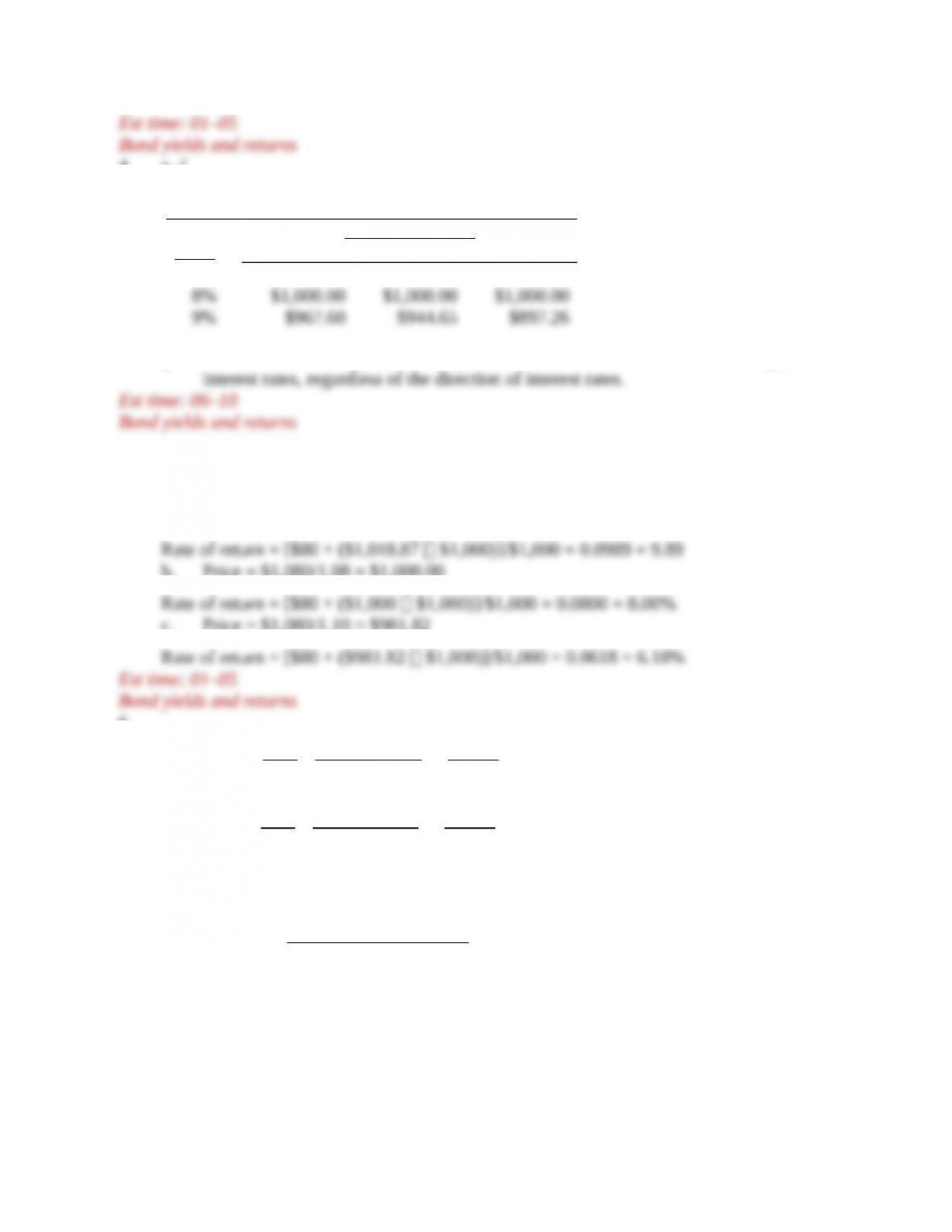

4. a.-f.

Price of Each Bond at Different Yields to Maturity

Maturity of Bond

Yield 4 Years 8 Years 30 Years

7% $1,033.87 $1,059.71 $1,124.09

g., h. The table shows that prices of longer-term bonds are more sensitive to changes in

5. The price of the bond at the end of the year depends on the interest rate at that time. With

1 year until maturity, the bond price will be $1,080/(1 + r).

a. Price = $1,080/1.06 = $1,018.87

b. Price = $1,080/1.08 = $1,000.00

c. Price = $1,080/1.10 = $981.82

6.

73.627$

07.1

000,1$

)07.1(07.0

1

07.0

1

40$PV

3030

0

66.553$

08.1

000,1$

)08.1(08.0

1

08.0

1

40$PV

2929

1

Rate of return =

%63.40

1000$

)1000$66.553($40$

Est time: 01–05

Bond yields and returns

7.

a.

1+.07=

(

1+.04

)

×

(

1+real

)

real = 2.88%

6-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

b.

1+.07=

(

1+.06

)

×

(

1+real

)

real = 0.94%

c.

1+.07=

(

1+.08

)

×

(

1+real

)

real = −0.93%

Est time: 01–05

Nominal and real returns

8.

a. Coupon = $40 × 1.08 = $43.20

9.

a. Cash flow in Year 1 =

40 ×1.08=$43.20

1040×1.08 ×1.08=$1,213.06

10.

a.

66.875$

10.1

000,1$

)10.1(10.0

1

10.0

1

50$PV

33

b.

77.692$

10.1

000,1$

)10.1(10.0

1

10.0

1

50$PV

1010

c. Long -term bonds are more sensitive to interest rate changes. The average cash flow is

received later, thus the present value of those coupons are reduced by more than near

-term cash flows.

Est time: 01–05

Interest rate risk

11. The coupon bond will fall from an initial price of $1,000 (when yield to maturity = 8%)

to a new price of $897.26 when yield to maturity immediately rises to 9%. This is a 10.27%

decline in the bond price.

6-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

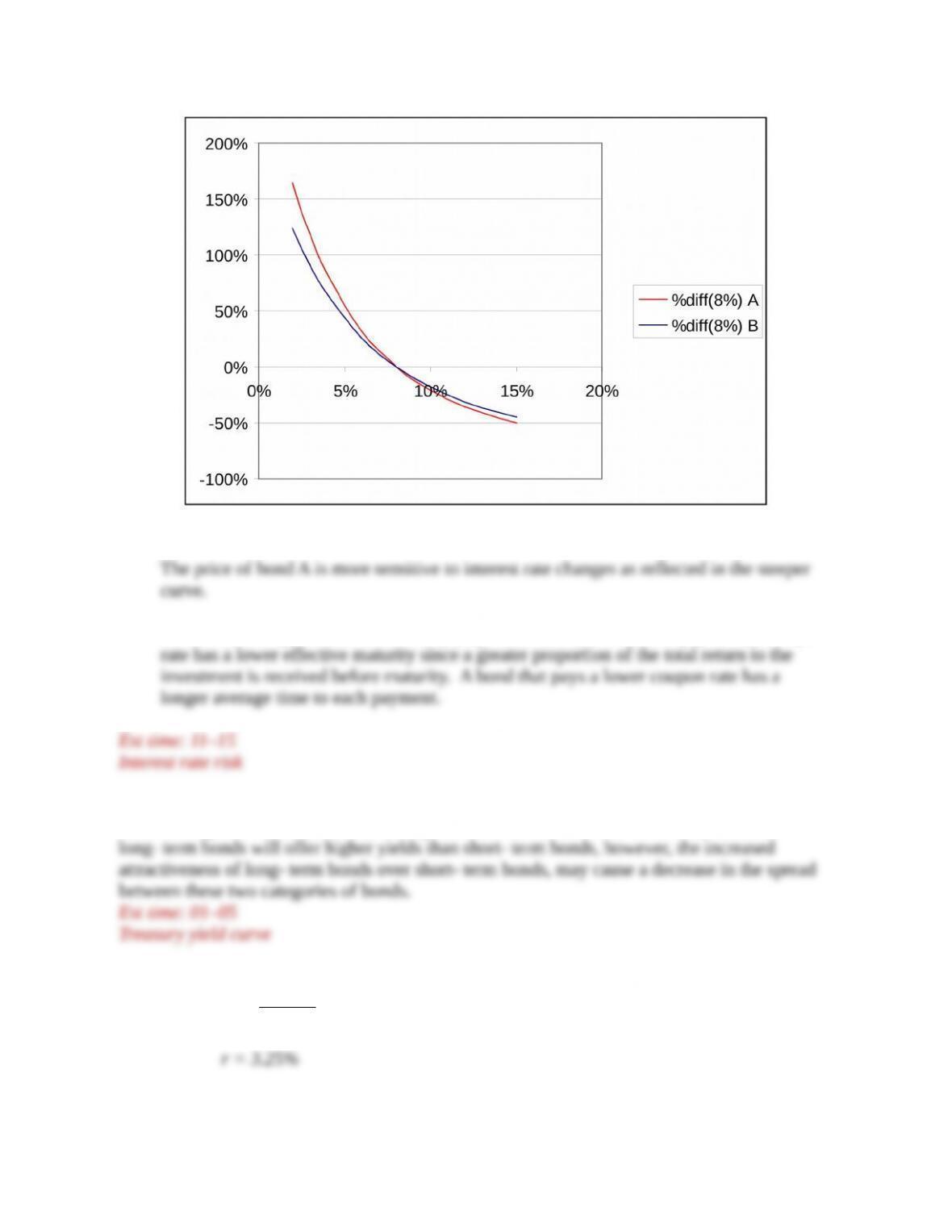

Yield Price A Price B % Di (8%) A % Di (8%) B

2% 144.93

324.67

165% 124%

3% 119.68

277.14

119% 91%

4% 100.00

239.00

83% 65%

12. The price of the coupon bond is much less sensitive to the change in yield. It seems to

act like a shorter maturity bond. This makes sense: There are many coupon payments for

13. a.,b.,c.

6-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

d.

e. Bond A has a higher effective maturity (higher duration). A bond that pays a high coupon

14. Falling interest rates will make long- term bonds more attractive. The expectation is that

15.

a.

968.52=$1,000

(

1+r

)

2

6-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

b.

933.51=$1,000

(1+r)2

c.

895.44=$1,000

(1+r)3

d.

854.80=$1,000

(1+r)4

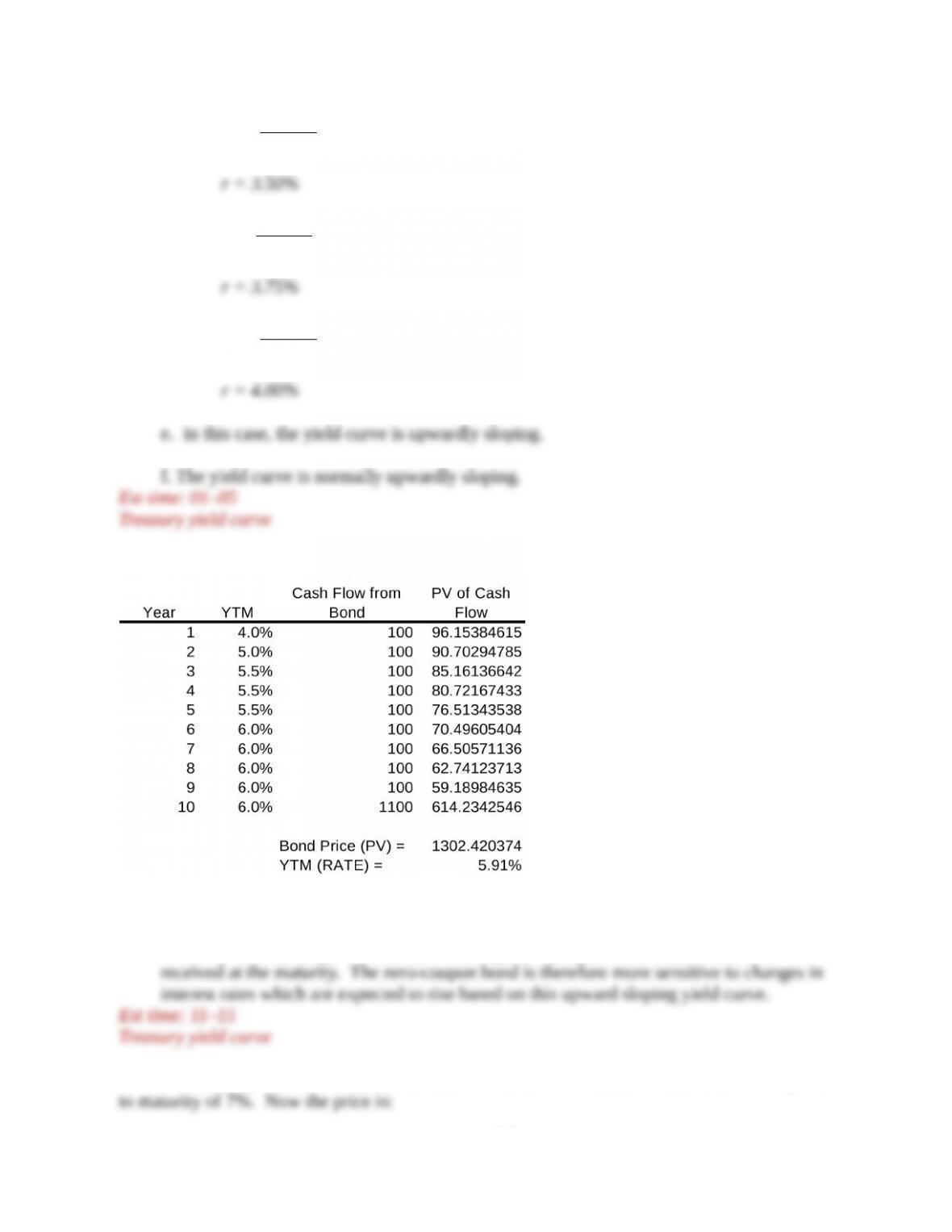

16. a., b.

c. The yield to maturity on the zero-coupon bond is higher. The zero-coupon has a higher

effective maturity (higher duration) in that a greater proportion of the cash flow is

17. a. The coupon rate must be 7% because the bonds were issued at face value with a yield

6-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

34.634$

075.1

000,1$

)075.1(075.0

1

075.0

1

35$PV

816

b. The investors pay $634.34 for the bond. They expect to receive the promised

coupons plus $800 at maturity. We calculate the yield to maturity based on these

expectations by solving the following equation for r:

1616

)1(

800$

)(1

11

$35$634.34 rrr

r

r = 6.49% × 2 = 12.99%

Using a financial calculator, enter n = 16, PV = ()634.34, FV = 800, PMT = 35;

then compute i = 6.49%.

Est time: 06–10

Bond ratings and credit risk

18. A $1,000 par value bond, issued for one year, with an expected yield of 20% will produce

19.

a True. Ignoring reinvestment risk, the promised yield on a treasury will materialize, provided

a. True. Since corporate bonds have default risk, the actual return has the possibility of being

b. True. If interest rates fall, the price of the bonds will rise and the realized return could increase.

20. The bond’s yield to maturity will increase from 7.5% to 7.8% when the perceived

default risk increases. The bond price will fall:

a. Initially, the bond is rated Aa and by that benchmark should yield around 7.5%.

6-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

21. Bonds are repaid in order of seniority. Bond A owners will first receive $2 million. The

remaining $1 million will be paid to Bond B owners.

22. Bond B can expect to receive $1,333,333. Bond A is secured with a building that is

6-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.