2. You should compare the present values of the two annuities.

PV = C((1 / r) – {1 / [r(1 + r)t]})

a.

73.721,7$

(1.05)0.05

1

0.05

1

$1,000PV

10

73.303,8$

(1.05)0.05

1

0.05

1

$800PV

15

b.

47.192,4$

(1.20)0.20

1

0.20

1

$1,000PV

10

38.740,3$

(1.20)0.20

1

0.20

1

$800PV

15

Calculator computations:

a.

Enter 10 5 –1,000

N I/Y PV PMT FV

N I/Y PV PMT FV

b.

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

N I/Y PV PMT FV

N I/Y PV PMT FV

Est time: 01–05

Annuies

3. The present value of your payments to the bank equals:

PV=

01.736$

)06.1(0.06

1

0.06

1

$100

10

The present value of your receipts is the value of a $100 perpetuity deferred for 10

years:

66.930$

)06.1(

1

06.0

100

10

This is a good deal if you can earn 6% on your other investments.

Calculator computations:

a.

Enter 10 6 –100

N I/Y PV PMT FV

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

b.

N I/Y PV PMT FV

Est time: 06–10

Perpetuies

4. If you live forever, you will receive a $100 perpetuity that has present value equal to

$100/r.

5. PV = C / r

6. Using the perpetuity formula, the 4% perpetuity will sell for £4/0.06 = £66.67.

The 2½% perpetuity will sell for £2.50/0.06 = £41.67.

Est time: 06–10

Perpetuies

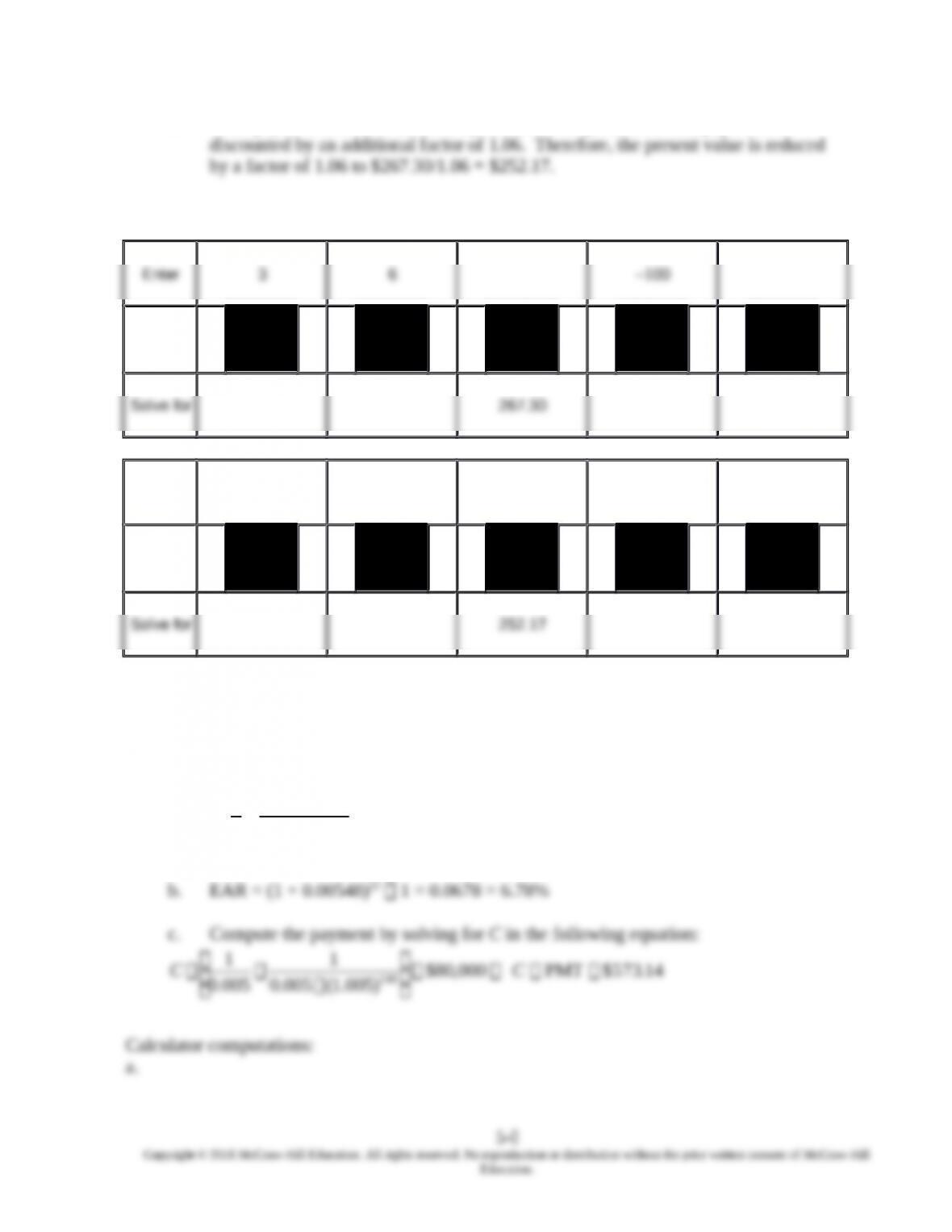

7. a. PV = 100 annuity factor (6%, 3 periods) = 100

30.267$

)06.1(06.0

1

06.0

1

3

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Calculator computations:

a.

N I/Y PV PMT FV

b.

Enter 1 6 –267.30

N I/Y PV PMT FV

Est time: 01–05

Annuies

8. a. This is an annuity problem; use trial and error to solve for r in the following equation:

%548.0000,80$

)1(

11

$600 240

r

rrr

c. Compute the payment by solving for C in the following equation:

14.573$PMT000,80$

)005.1(0.005

1

0.005

1

240

CC

Calculator computations:

a.

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

N I/Y PV PMT FV

Solve for .55

The monthly interest rate is .55%.

c.

N I/Y PV PMT FV

Solve for 573.14

Est time: 01–05

Annuies

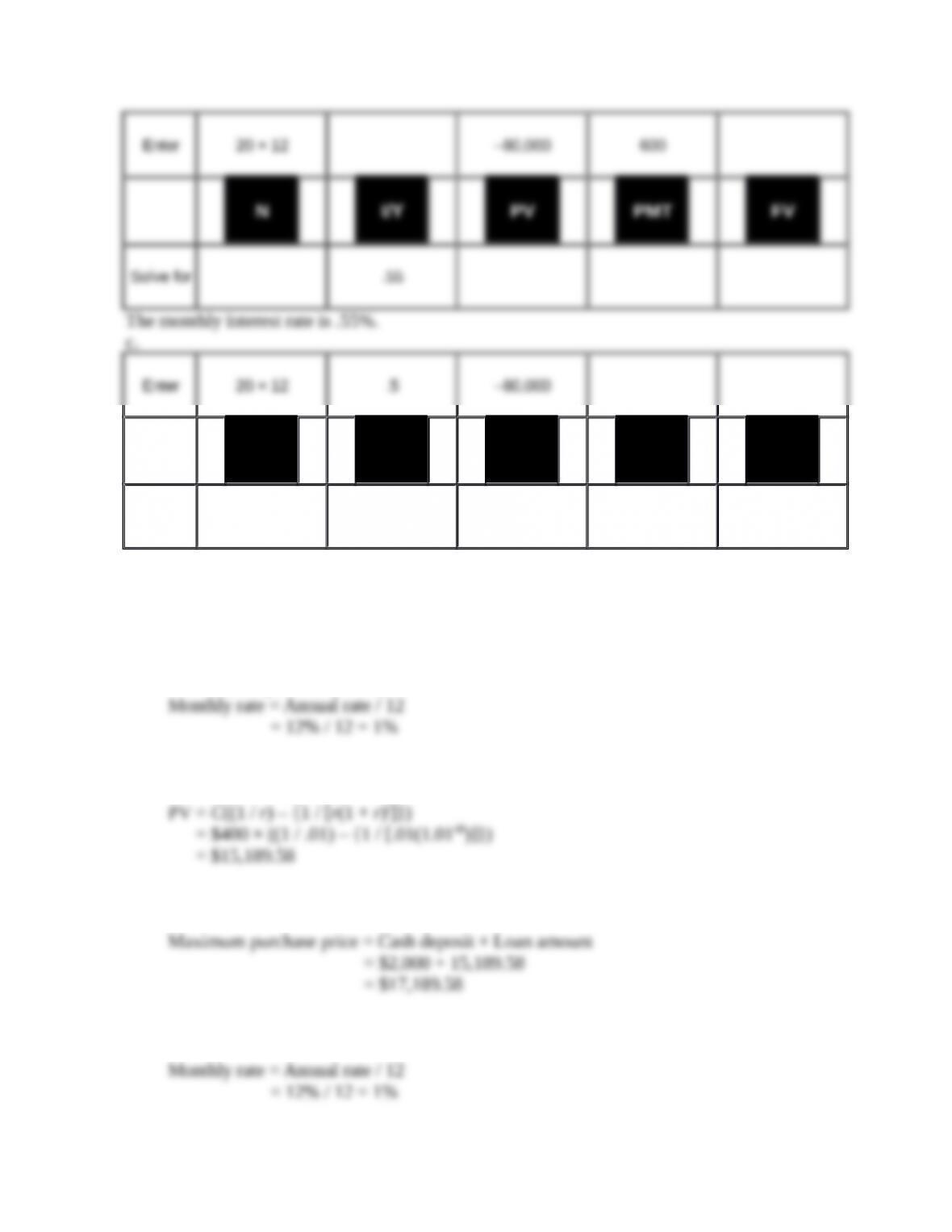

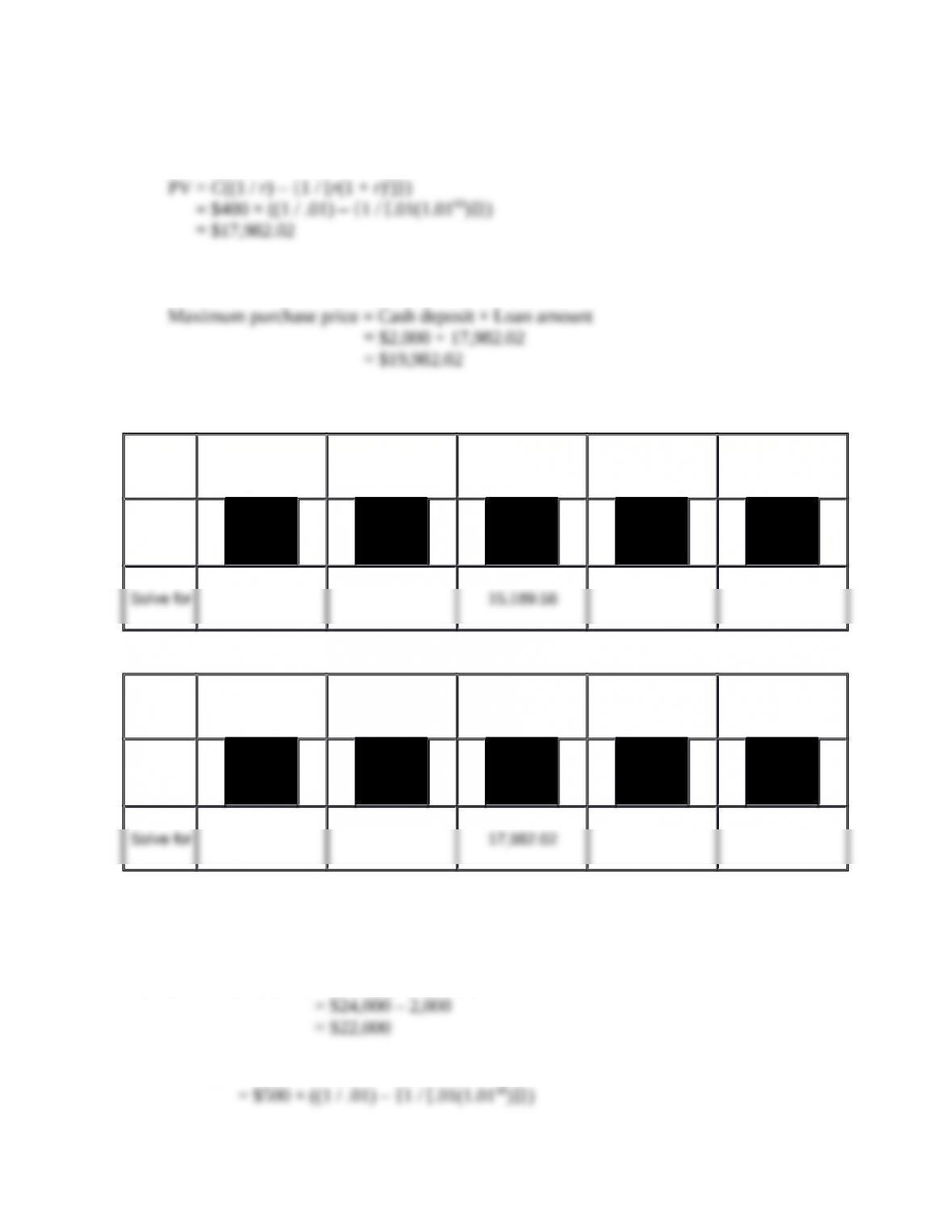

9. a. First, compute the monthly interest rate:

Second, compute the amount you can afford to borrow:

Third, compute the maximum purchase price you can afford:

b. First, compute the monthly interest rate:

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Second, compute the amount you can afford to borrow:

Third, compute the maximum purchase price you can afford:

Calculator computations:

a.

Enter 48 1 –400

N I/Y PV PMT FV

The monthly interest rate is 1%.

c.

Enter 60 1 –400

N I/Y PV PMT FV

Est time: 01–05

Annuies

10. a. Present value = Cash payment – Rebate

b. PV = C((1 / r) – {1 / [r(1 + r)t]})

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

11. a. PV = C((1 / r) – {1 / [r(1 + r)t]})

b. Using the monthly interest rate computed in part a:

c. If lenders only quote one rate, it is most apt to be the APR.

Calculator computations:

N I/Y PV PMT FV

12. Your savings goal is FV = $30,000. You currently have in the bank PV = $20,000.

Solve the following equation for t:

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

74.44000,30$

0.005

1005.1

$100)1.005($20,000

t

t

t

Calculator computations:

Enter .5 –20,000 –100 30,000

N I/Y PV PMT FV

13. Real interest rate = Nominal interest rate – Inflation rate

14. This problem can be approached in two steps. Since the first payment occurs in Year 4,

the present value of the annuity will be as of the prior year, or Year 3.

PV3 = C((1 / r) – {1 / [r(1 + r)t]})

Calculator computations:

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Enter 10 5 –10,000

N I/Y PV PMT FV

Enter 3 5 –77,217.35

N I/Y PV PMT FV

Est time: 01–05

Annuies

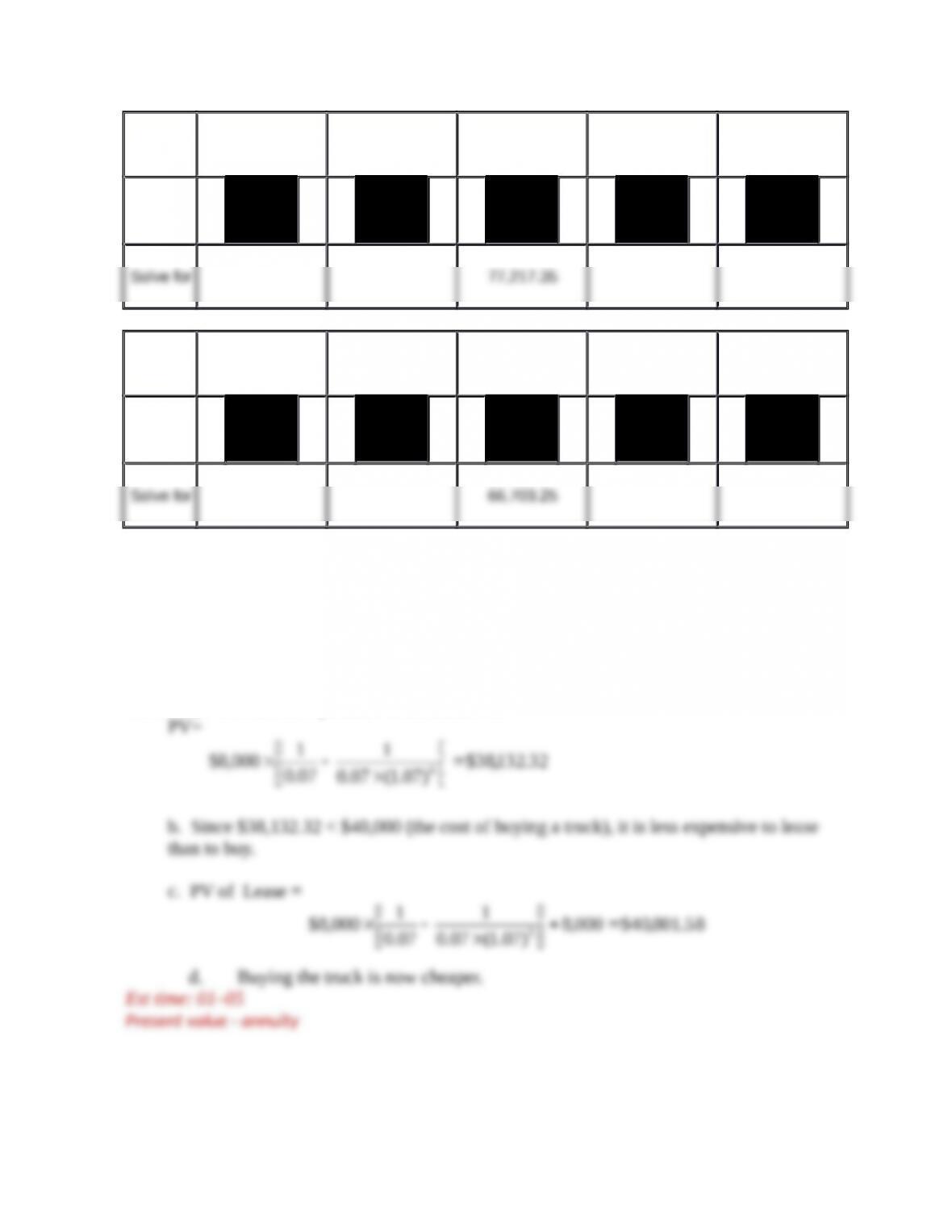

15. a. Leasing the truck means that the firm must make a series of payments in the form of

an annuity. Calculate the present value as follows:

16.

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

a. If we assume cash ows come at the end of each period

(ordinary annuity) when in fact they actually come at the beginning (annuity due),

b. Similarly, the FV of an annuity due equals the FV of an

17. a. Compare the present value of the payments. Assume the product sells for $100.

Installment plan:

b. PV=

65.88$

)05.1(0.05

1

0.05

1

$25 4

The payment plan has a PV of $88.65, so it is a better deal.

Est time: 01–05

Annuies

18.

a. Solve for C in the following equation:

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

b. If the first payment is made immediately instead of in a year, the annuity factor

19. a. The present value of the $2 million, 20-year annuity, discounted at 8%, is:

PV=

64.19$

)08.1(0.08

1

0.08

1

million $2

20

million

b. If the payment comes immediately, the present value increases by a factor of 1.08 to

$21.21 million.

Est time: 01–05

Annuies

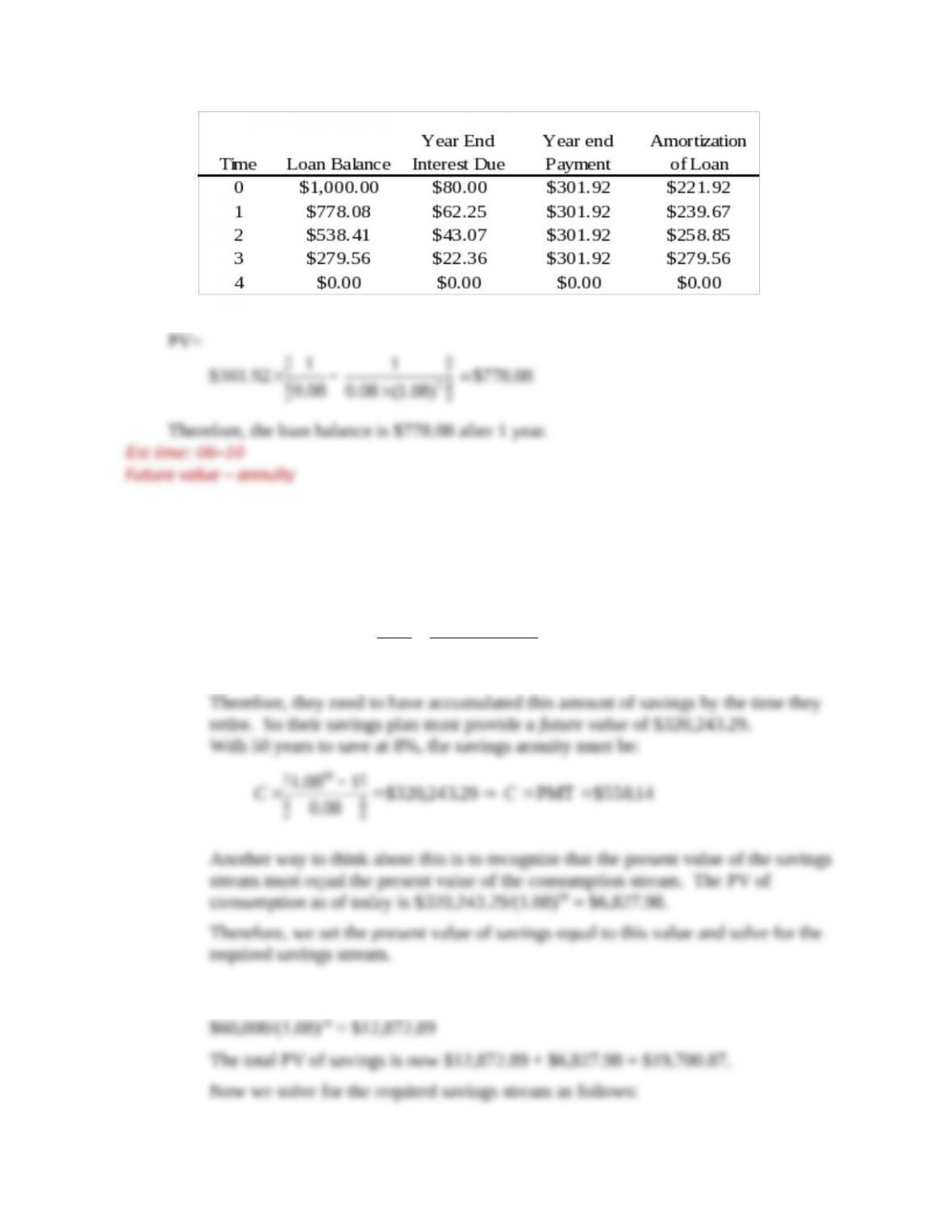

20. The payment on the mortgage is computed as follows:

55.599$PMT000,100$

)]12/06.0(1[)12/06.0(

1

)12/06.0(

1

360

CC

After 12 years, 216 months remain on the loan, so the loan balance is:

37.079,79$

)]12/06.0(1[)12/06.0(

1

)12/06.0(

1

$599.55

216

Est time: 01–05

Future value – annuity

21. a.

92.301$PMT000,1$

)08.1(0.08

1

0.08

1

4

CC

b.

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

22. a. The present value of the planned consumption stream as of the retirement date will

be:

PV=

29.243,320$

)08.1(0.08

1

0.08

1

$30,000

25

b. The couple needs to accumulate additional savings with a present value of:

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

41.610,1$PMT87.700,19$

)08.1(0.08

1

0.08

1

50

CC

23. The future value of the payments into your savings fund must accumulate to $500,000.

We choose the payment (C) so that:

24. Nothing . The future value of your inheritance will be 100,000 x (1+.06)30 = 574,349.12

25. By the time you retire, you will need:

26. a. After 30 years, the couple will have accumulated the future value of a $3,000

b. If they wish to accumulate $800,000 by retirement, they have to save an additional

27. Suppose the purchase price is $1. If you pay today, you get the discount and pay only

5-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.