1. Cash flow from operations can be positive even if net income is negative. For

example, if depreciation expenses are large, then negative net income might

2. An increase in accounts receivable reduces cash flow by $10,000. An increase in

3.

Candy Canes, Inc.

Month

Sales

Cost of goods

Δ ↑A/R

Δ↑Inventory

Cash flow*

Net income**

April 0 0 0 100,000 -100,000 0

4. The calculations are presented in the following table. Sales occur in quarters 2 and

3, so this is when the cost of goods sold is recognized. Therefore, net income is

zero in quarters 1 and 4. In quarter 1, the production of the kits is treated as an

investment in inventories. The level of inventories then falls as goods are sold in

quarters 2 and 3. Accounts receivable in quarters 2 and 3 equal the sales in those

quarters since it takes one quarter for receivables to be collected. Notice that cash

flow in quarter 1 equals the cost of producing the kits and that in quarters 3 and 4

cash flow equals cash received for the kits previously sold.

a. Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales $0 $550 $600 $ 0

3-.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

b., c.

5. The table below shows the firm’s net income and investment in net working capital

for each month from January to April. Sales revenue and production costs are

recognized at the time of sale in February. Since the firm neither pays for goods nor

receives cash for sales, cash flow is zero in January and February. Cash flow occurs

in March and April, when cash is actually being exchanged. The sow ears are paid

for in March and cash is received for the purses in April.

Value Added Inc. (in 000s)

January February March April

Sales $0 $2,000 $0 $0

Cost of goods sold 0 $1,000 0 0

Net income $0 $1,000 $0 $0

Est time: 11–15

Operating cash o

6. In section 3.3, the free cash flow is calculated at $7,362 million. Total cash

distributed to shareholders was $9,530 million. Of this, $2,530 was paid as a

3-.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

7.

a. Cash flow from operations = net income + interest + depreciation – additions to

net working capital

Free cash flow = cash flow from operations – capital expenditures

b.

c.

Additions to net working capital = (3,403 − 3,143) − (1,375 − 1,335) − (122 − 117) −

8.

a.

For a married couple, the marginal tax rate on $90,000 of income is 25%.

b.

Taxes = ($18,550 × .10) + (($75,300 – 18,550) × .15) + (($90,000 – 75,300) × .25) =

c.

For a single person, the marginal tax rate on $90,000 of income is also 25%.

d.

Taxes = ($9,275 × .10) + (($37,650 – 9,275) × .15) + (($90,000 – 37,650) × .25) =

9.

a. Taxes = (0.10 $9,275) + 0.15 ($20,000 $9,275) = $2,535.95

b. Taxes = (0.10 $9,275) + 0.15 ($37,650 $9,275) + 0.25 ($50,000

3-.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Marginal tax rate = 25%

c. Taxes = (0.10 $9,275) + 0.15 ($37,650 $9,275) + 0.25 ($91,150

d. Taxes = (0.10 $9,275) + 0.15 ($37,650 $9,275) + 0.25 ($91,150

10. Taxes = (0.10 $18,550) + 0.15 ($75,300 $18,550) + 0.25 ($95,000

11. Taxes = (0.15 $50,000) + 0.25 ($75,000 $50,000) + 0.34 ($100,000

12.

a. Taxes on your salary = (0.10 $9,275) + 0.15 ($37,650 $9,275)

b. If you rearrange income so that your salary and the firm’s profit are both

3-.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

c. Any personal income between $37,650 and $50,000 will create the same

13. a.

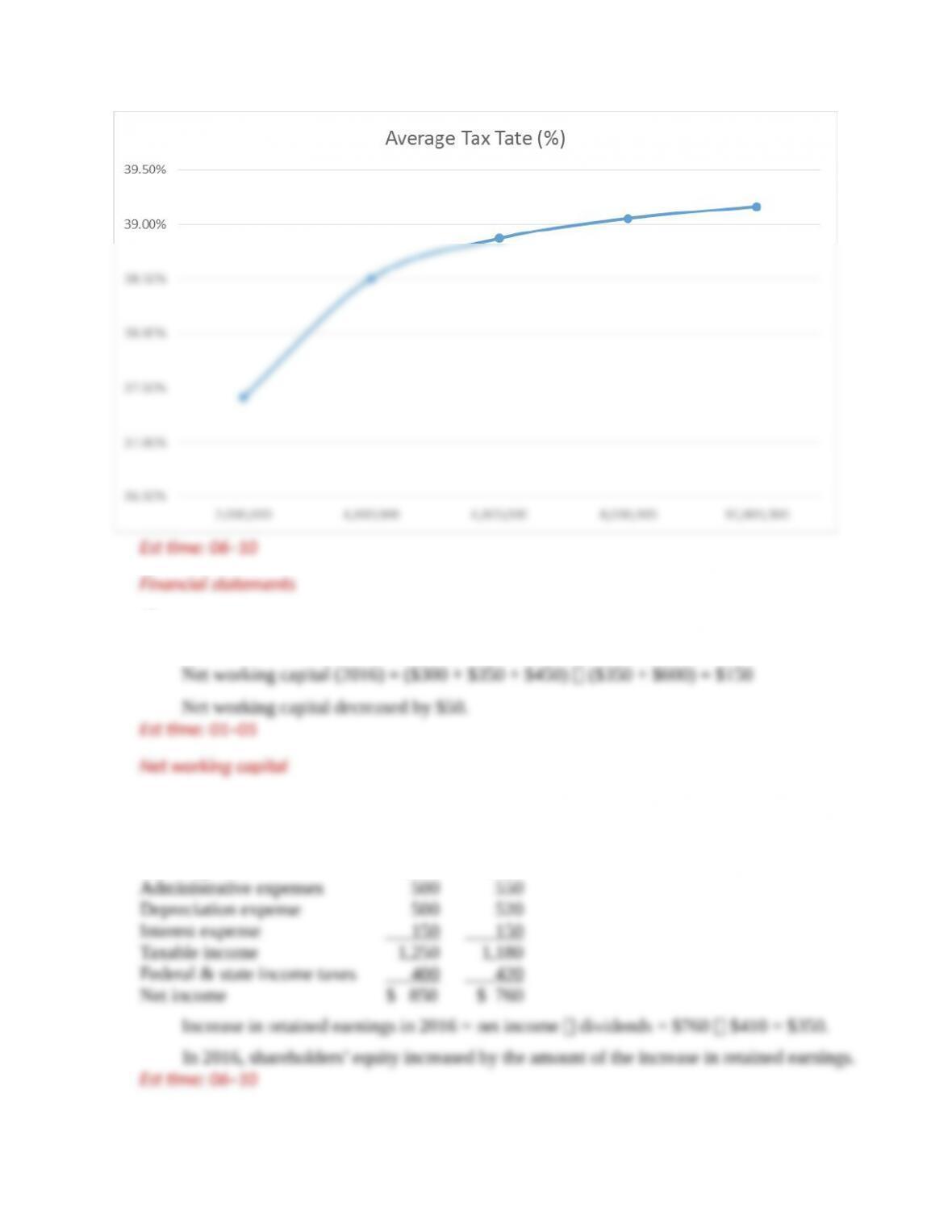

Income Taxes Due Average Tax

Rate (%)

10,000 1,036 10.36%

20,000 2,536 12.68%

40,000 5,771 14.43%

80,000 15,771 19.71%

..

…

b. As shown in the table and graph above, the difference between average tax

14.

3-.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Assets 2015 201

6

Liabilities and

Shareholders’ Equity 2015 2016

Cash & marketable securities $ 800 $ 300 Accounts payable $ 300 $ 350

Inventories 300 350 Notes payable 1,000 600

Accounts receivable 400 450 Long-term debt 2,000 2,400

15.

Net working capital (2015) = ($800 + $300 + $400) ($300 + $1,000) = $200

16.

2015 2016

Revenue $4,000 $4,100

Cost of goods sold 1,600 1,700

3-.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

17. Earnings per share in 2015 = $850,000/500,000 shares = $1.70

18. Net fixed assets increased by $800,000 during 2016, while depreciation expense in

19.

Market Value Balance Sheet, 2016

(figures in thousands of dollars)

Assets

Liabilities &

Shareholders’ Equity

Cash

$ 300

Accounts payable

$ 350

Inventories 350 Notes payable 600

20.

Cash provided by operations

Net income $ 760

Noncash expenses

3-.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Cash flows from investments

Cash provided by (used for) financing activities

21. Average tax bracket in 2015 = taxes/taxable income = $400/$1,250 = 0.320 =

32.0%

3-.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.