Solutions to Chapter 22

International Financial Management

1. a. You can buy 100/1.376 = 72.67 euros for $100.

b. You can buy 100 .888 = 88.80 Swiss francs for $100.

c. If the British pound depreciates, then $1 will buy more British pounds, so the direct

d. One U.S. dollar can buy 1.095 Canadian dollars. Therefore, one U.S. dollar is worth

2. You can buy 1 x 13.231 = 13.23 pesos for one dollar

3. Let’s assume the investment for each person was the equivalent of $1,000.

a. The cost of the bond at year 0 was

PV =1000

(1+.052)2=$903.58

PV =1000

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

c. If Madame Butterfly could forecast her USD cash inflow in one year, then she could

hedge this amount (i.e. $970.87) by selling the dollars forward in exchange for yen.

Assuming the forward rate she locks in is at neither a premium nor a discount (i.e. a

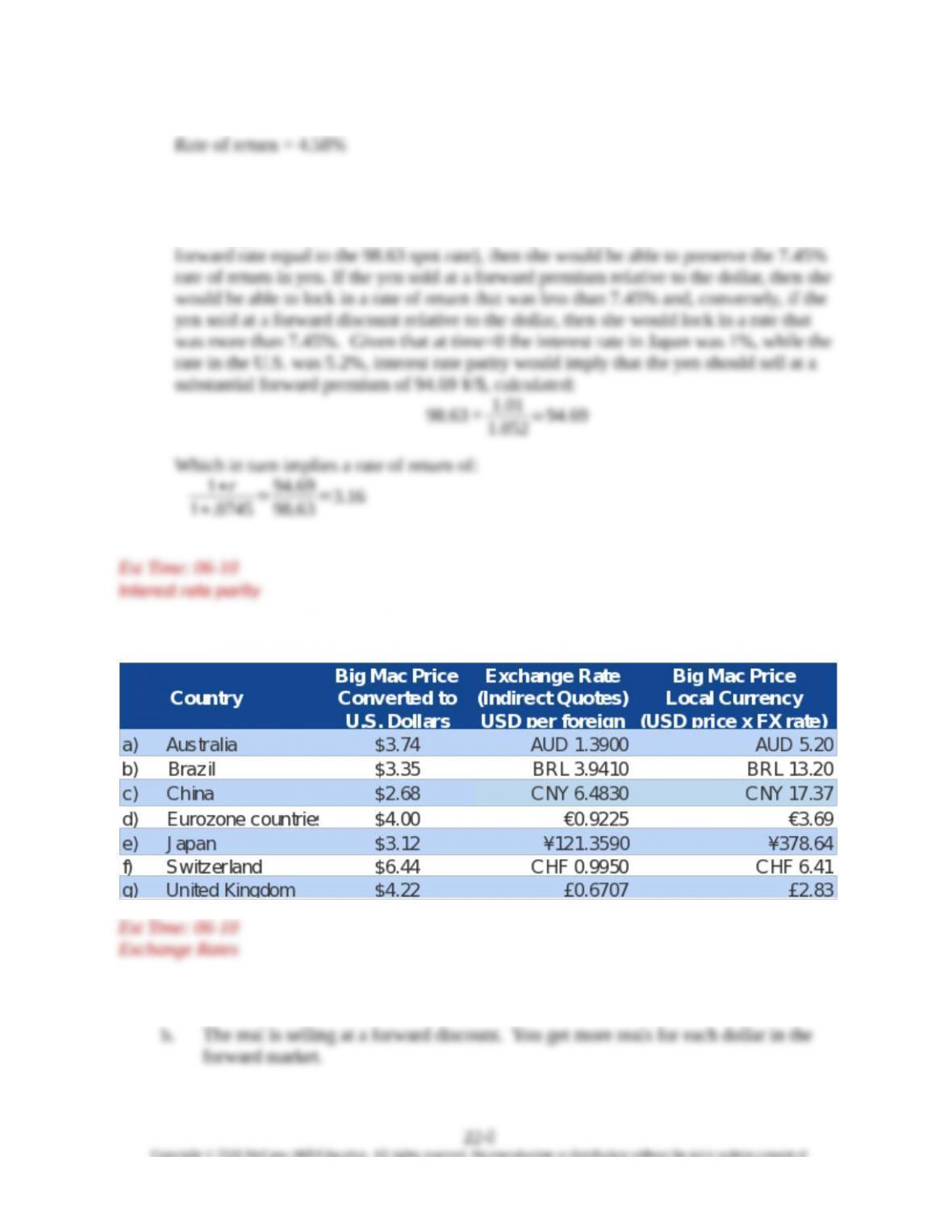

4. The following table calculates the local price of the Big Mac Hamburger:

5. a. 3.941 real/$

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

c.

BRL/$

/$

BRL

$

BRL

1

1

s

f

r

r

941.3

012.4

01.1

1

BRL

r

d. 4.012 real = 1 dollar

6. The New Zealand dollar will appreciate, relative to the U.S. Dollar since one U.S. dollar is

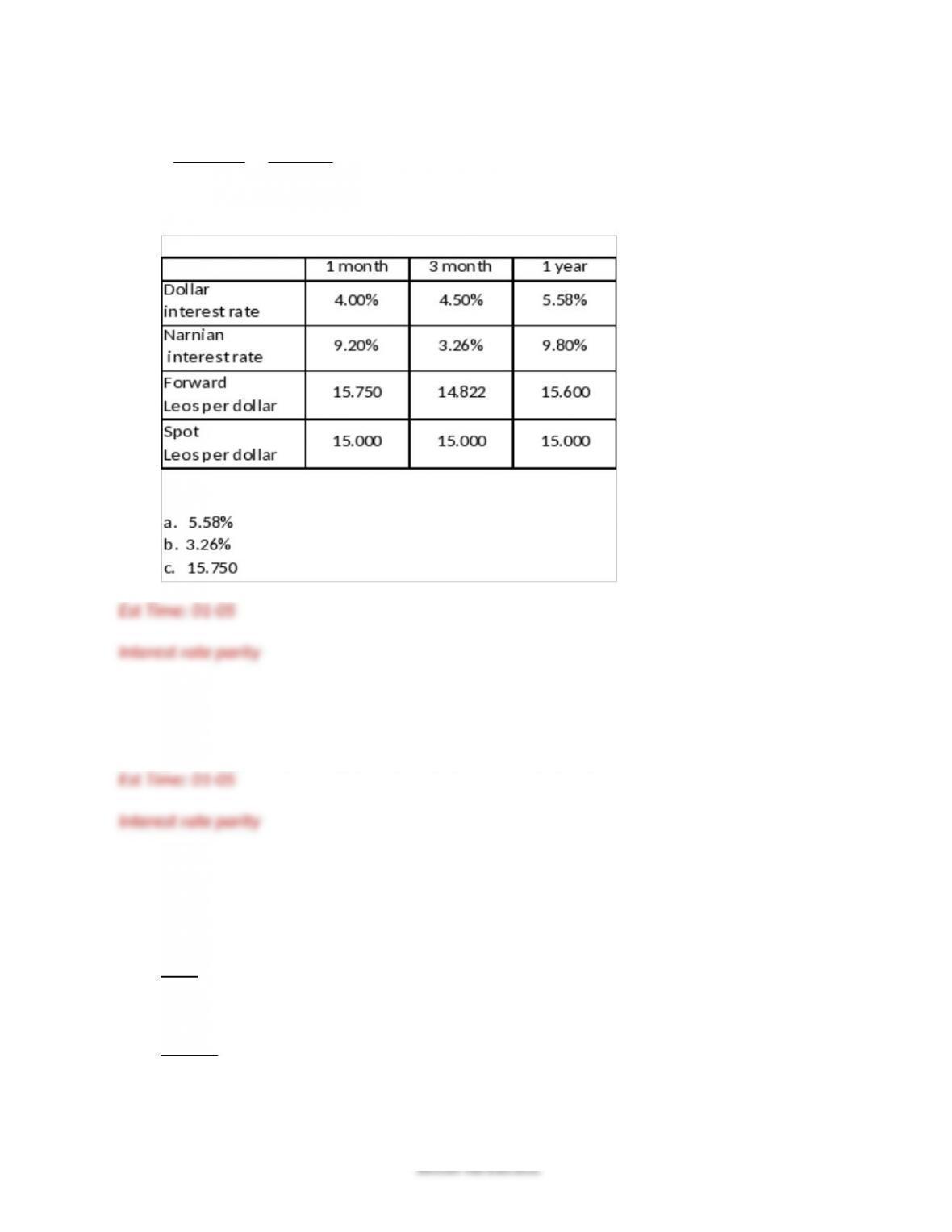

7. The difference in interest rates between Ruritania and the United States equals (a) the

8.

1.10

b.

45

40 =1.15

1+r$

r$=2.22

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

1.12

9.

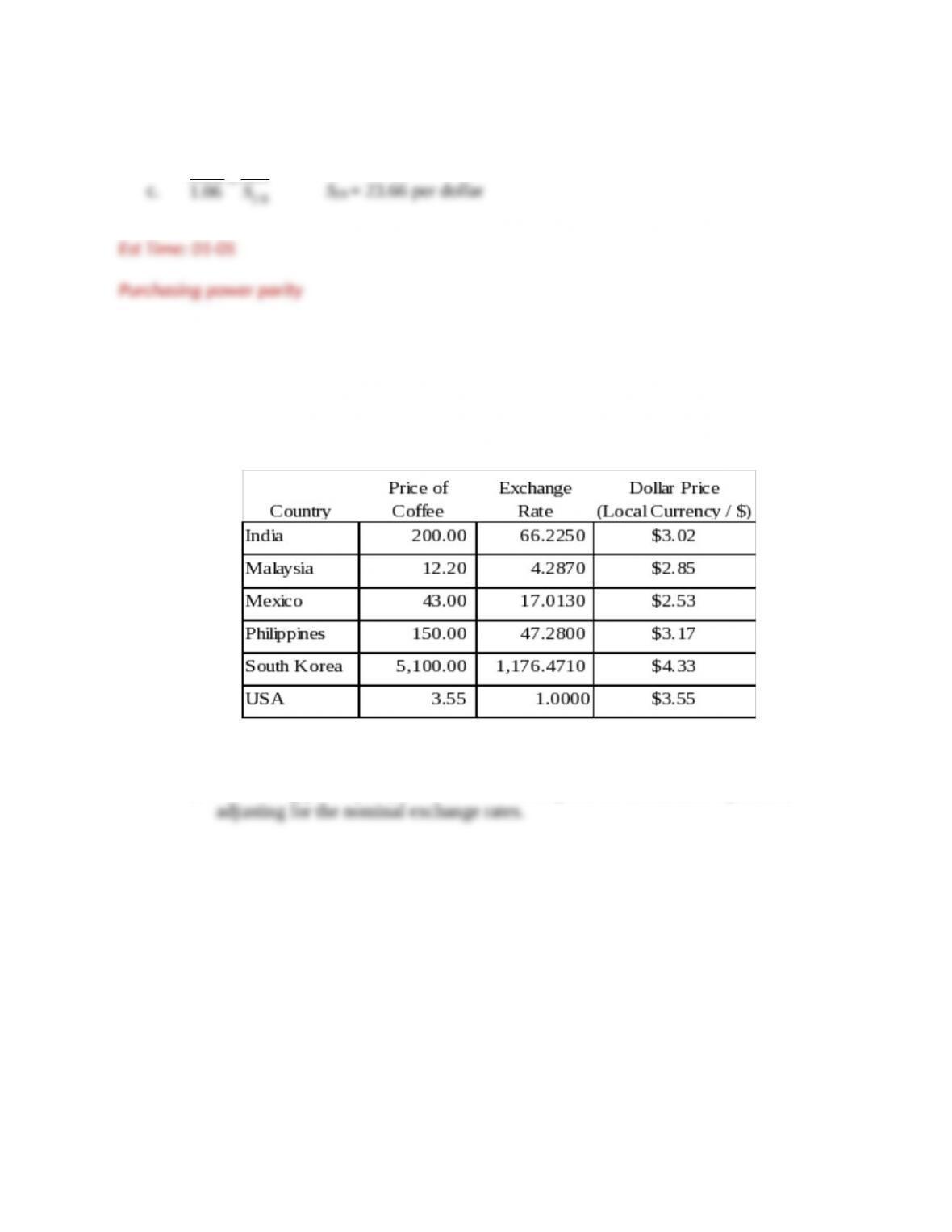

a. The dollar price of the latte in each country is found by dividing the local currency

price by the indirect quote for the exchange rate. See the table below:

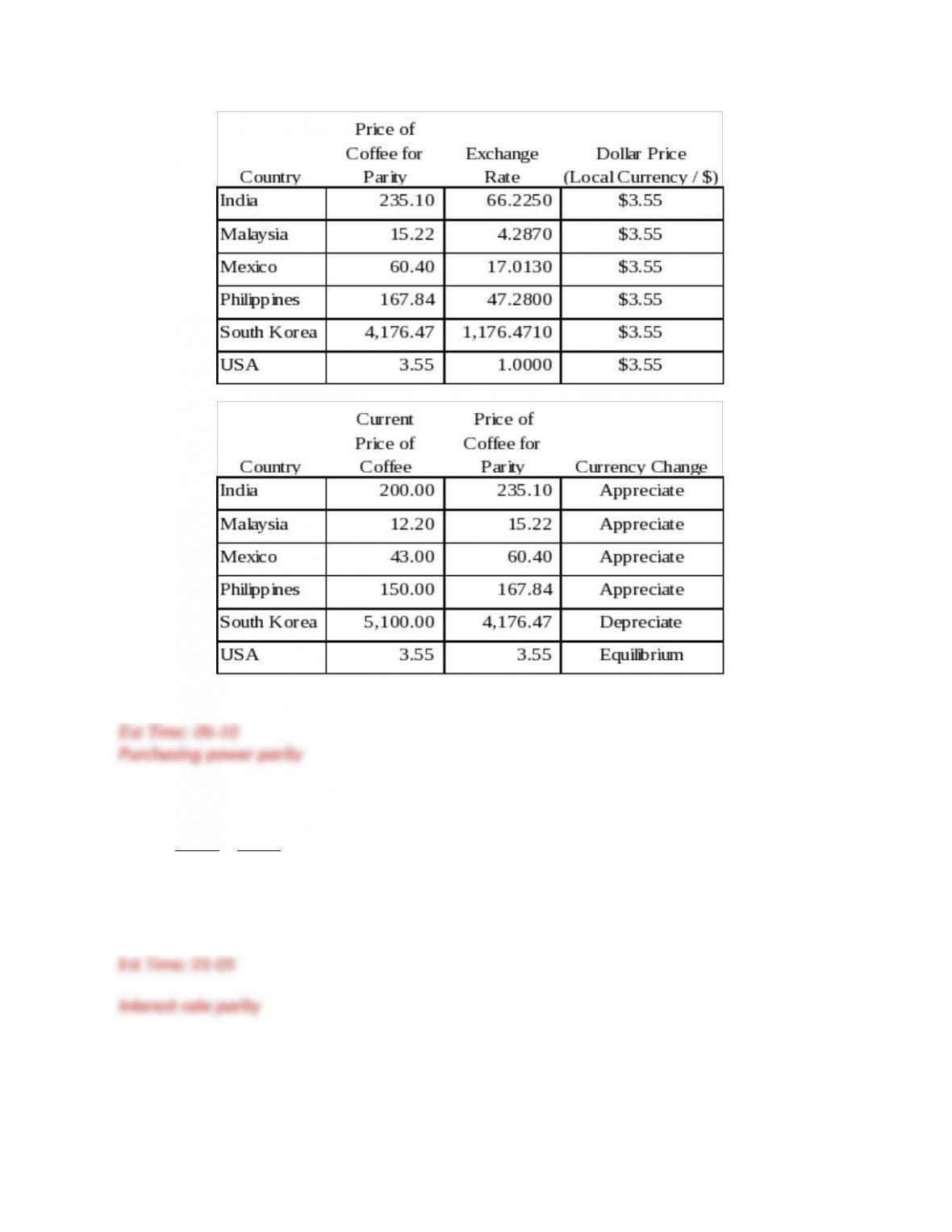

b. Purchasing power parity does not hold as the price for lattes is not equal after

c.

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

10.

4.480

3.941 =1+rf

1.005

rf=14.25

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

11.

foreign foreign/$

$ foreign/$

1+

1+

r f

r s

=

12. No. Forward rates are priced to eliminate carry trade. As such, a forward contract will

guarantee an investor makes the same return in both countries.

13. Suppose a person invests $100,000, note the profit in each country.

a. b.

Example: Borrow USA and Lend Mexico

USA

$100,000×1.03=$103,000

Mexico

$100,000×18=1,800,000 pesos

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

1,800,000 pesos ×1.08=1,944,000 pesos

1,944,000

24 =$81,000

Change in investment in pesos = 1,944,000 – 1,800,000 = 144,000 pesos

Change in investment in US$ = $81,000 – $103,000 = -$22,000

Example: Borrow Mexico and Lend USA

Mexico

1,800,000 pesos ×1.08=$1,944,000

USA

1,800,000 pesos/18=$100,000

$100,000×1.03=$103,000

$103,000×24=2,472,000 pesos

Change in investment in pesos = 2,472,000 – 1,944,000 = 528,000 pesos

Change in investment in US$ = $103,000 – $100,000 = $3,000

By borrowing in Mexico and investing in the USA, you make more money (whether

measured is pesos or US$).

Est Time: 06-10

Interest rate parity

14. Depreciate. The higher interest rate indicates a weakening currency.

15. If the forward rate is such that parity exists, he will not benefit from the lower interest

rates. This assumes he decided not to speculate and instead lock in the forward rate when

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

16. Choice a: Buy euros forward. This locks in the dollar value of the euros that the importer

17. Let s£ represent the spot rate ($/£) in 1 year. The rate of return to a U.S. investor is given

by:

18. If the dollar depreciates, then, to maintain a fixed yen price, Sanyo will need to raise the

dollar price. This action can cause Sanyo to lose business in the United States. It can

Alternatively, Sanyo can fix the dollar price of its products. This means that its U.S. sales are

independent of the exchange rate. But then the yen value of the dollar revenues that it realizes

However, in the scenario posed, the dollar is appreciates against the yen. This implies that

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

19. The firm can borrow the present value of 1 million euro, sell those euros for U.S. dollars

20. a. Revenue is in Trinidadian dollars, whereas the U.S. firm is concerned with the U.S.

b. If the U.S. firm borrows in Trinidad and converts the borrowed funds to dollars, the

c. Now costs as well as revenues are foreign currency-denominated. The firm’s foreign

21. For Alpha, a depreciating euro value would make the goods imported from the US

relatively more expensive and the revenues collected in Germany relatively less valuable

in dollar terms. Alpha could protect from this double edged exposure by selling the euro

For Omega, a depreciating euro value would make the goods procured in Germany

relatively less expensive and the revenues collected in the US relatively more valuable (or

22.

Dollar Value of

Euro Revenue Given

Exchange Rate

Additional Income

from Forward Contract

Given Exchange Rate

Total Profit (or

Loss) Given

Exchange Rate

Revenue in euros

(million) 1.20 1.40 1.20 1.40 1.20 1.40

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Note: Profit on the forward contract = forward rate – ultimate spot exchange rate

Selling the euros forward results in a hedged position only if the export order is received and

the firm receives euro-denominated cash flows. In this case, the profit on the forward sale

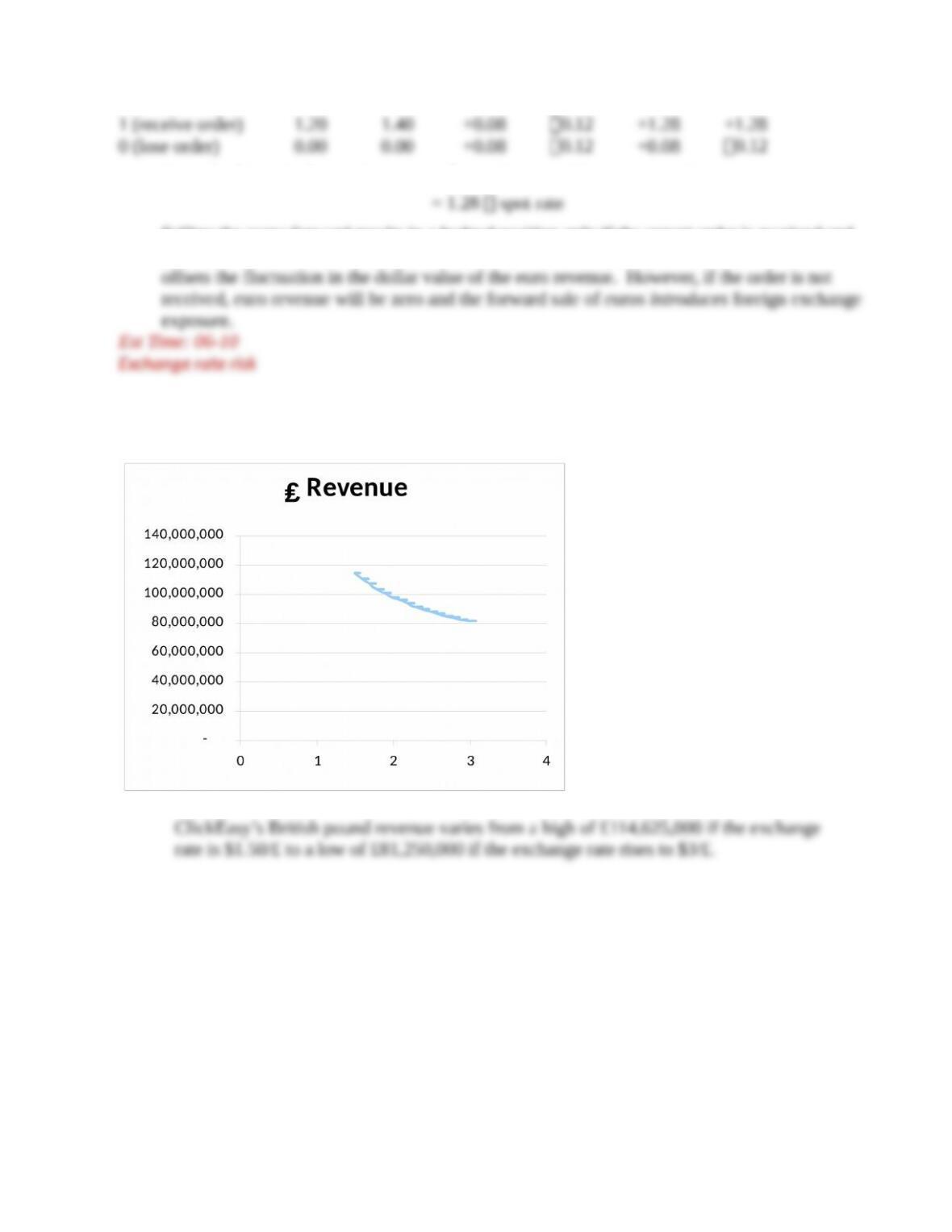

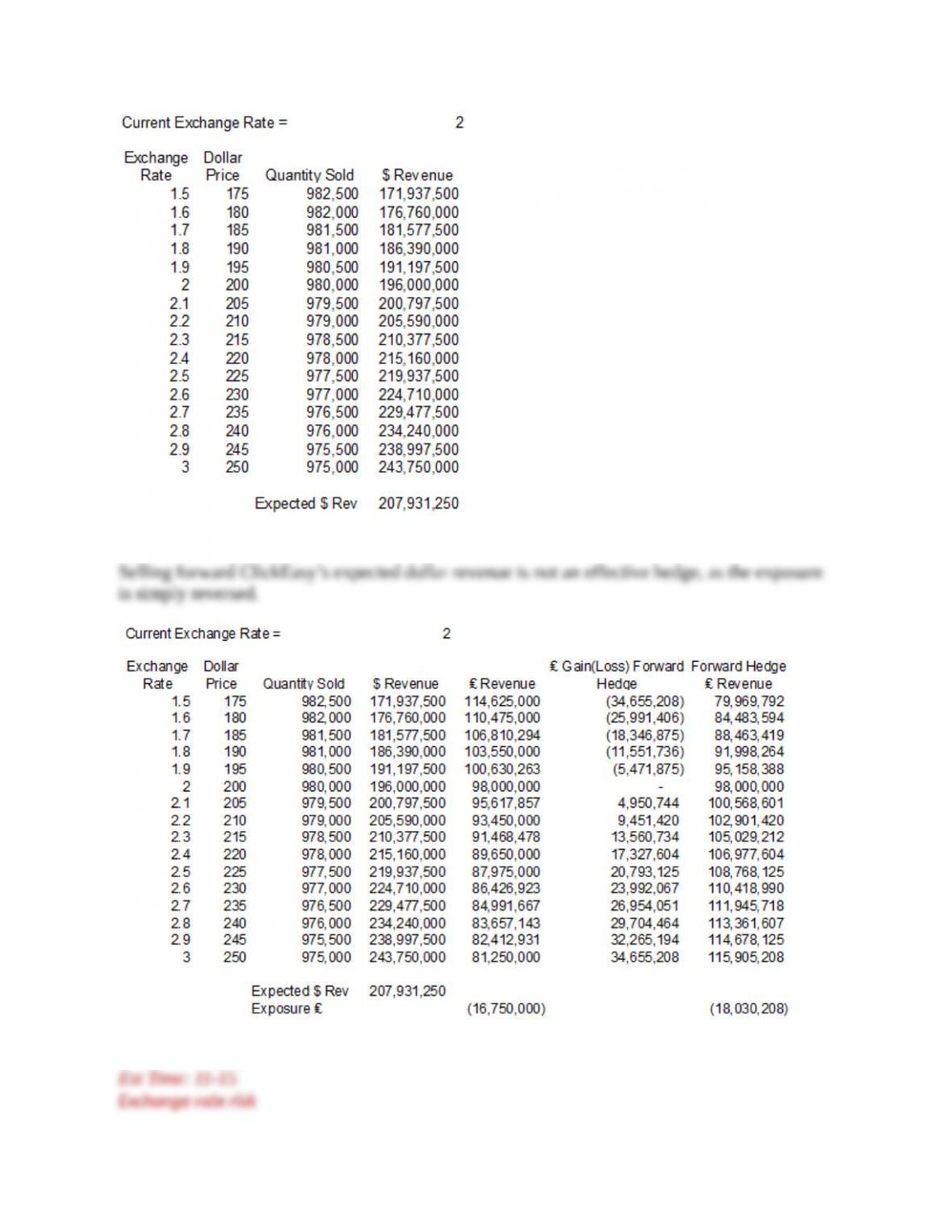

23. a. The exchange rate exposure for ClickEasy is shown in the graph below:

b. Given the demand function (quantity sold = 1,000,000 – 100 × price), ClickEasy’s

expected dollar revenue is $207,931,250, as shown in the Excel table below:

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

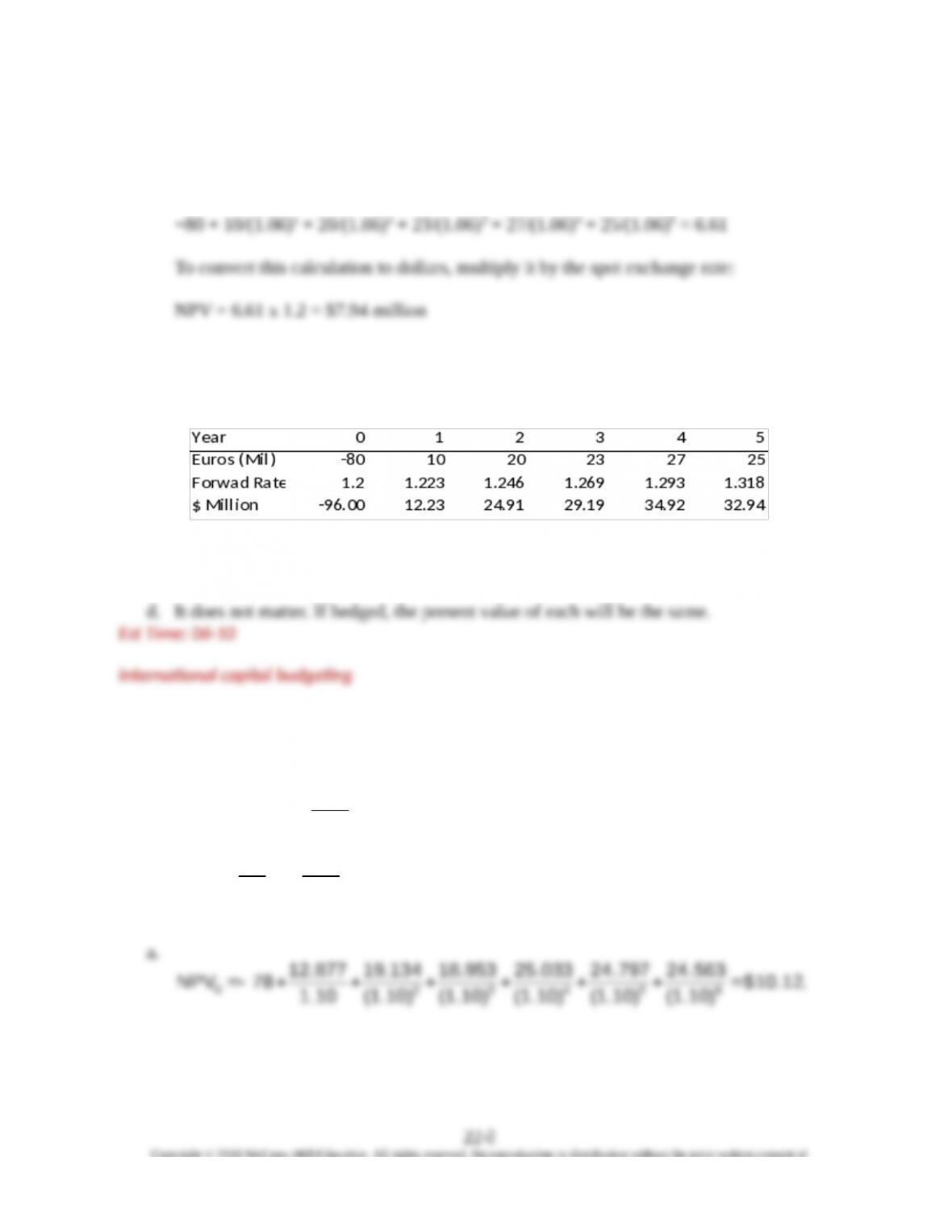

24.

a. First, find the NPV using the euro interest rate of 6%:

b. The forward rate increases by the interest rate differential each year. The following table

shows the forward rates for each of the next five years and adjusts the cash flow in each

year.

c. No. The company can hedge against a drop in the value of the euro.

25. First, convert both currencies to US$ as follows (calculation for C1 only):

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

12.877

1.06

1.05

10)(1.3

13.462

1.04

1.05

1.5

20

26. The forecast rur cash flows are converted into dollars at the spot rate that is forecast for

each date. The current spot rate is 100 rur per dollar, but the rur is expected to depreciate

at 2% per year.

Year 0 1 2 3 4 5

rur cash flow (millions)

380

100

125

150

175

200

(Note: As we point out in the text, we think it is poor practice to combine the profits from

the Ruritanian operation with the profits that are expected from guessing the direction of

currency movements. The exchange rate forecasts used in the problem are inconsistent

with the interest rate and inflation rate forecasts. It makes more sense to first consider

whether the project is worthwhile, and then to determine whether the firm should hedge

against, or bet on, exchange rate changes.)

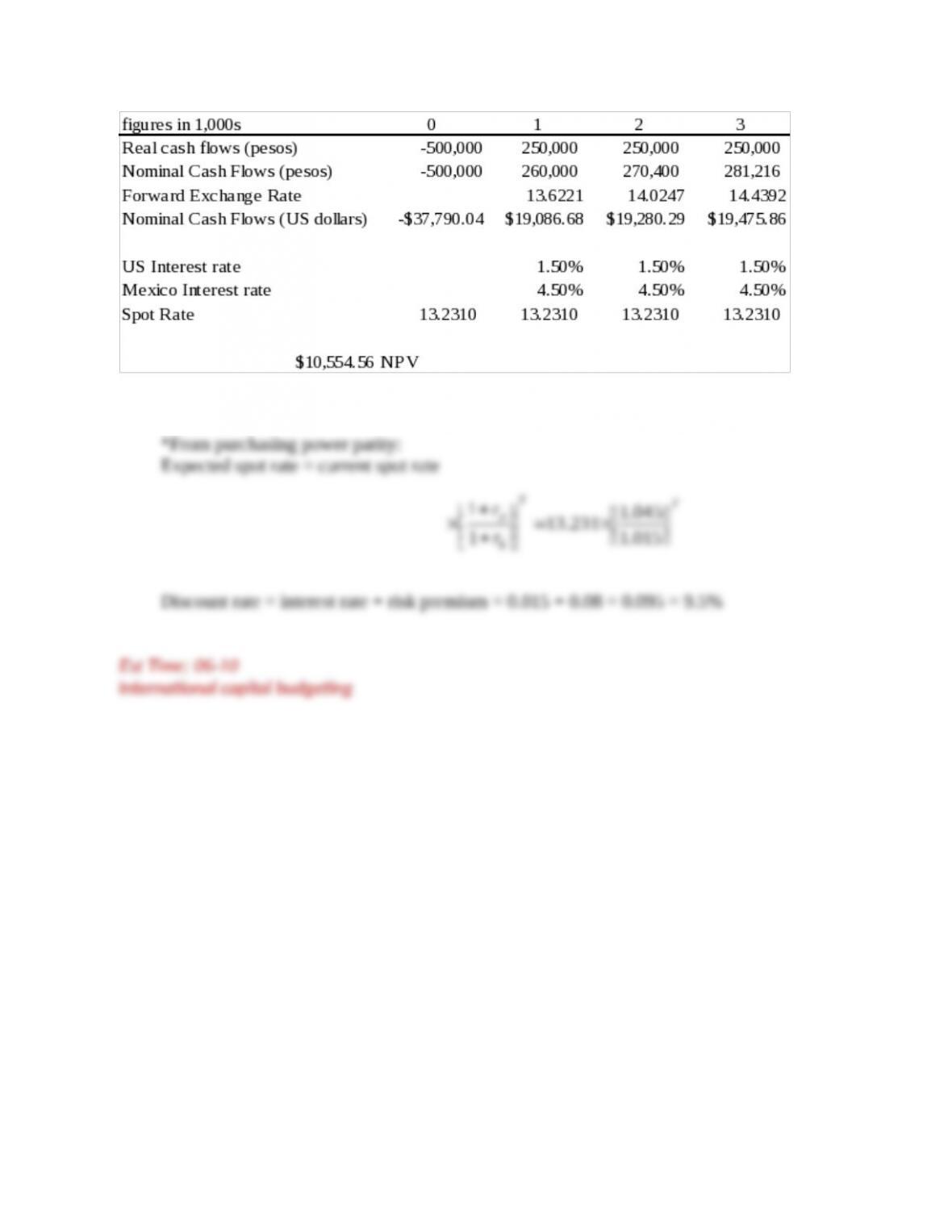

Est Time: 06-10

Interna!onal capital budge!ng

27.

Do calculations in U.S. dollars:

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

22-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.