Solutions to Chapter 20

Working Capital Management

1. a.The current assets consist of:

Cash $3.7

Marketable Securities 6.4

Accounts Receivable 8.7

Inventories 7.9

b. The current liabilities consist of:

Accounts Payable 8.4

c. New working capital is equal to Current Assets – Current Liabilities, or 19.1 [39.7-20.6]

2. a.Decrease. The lower inventory levels will mean less cash invested in product on the shelf.

b. Increase. Paying vendors sooner will mean cash is tied up in raw materials sooner.

3. The new inventory management system will (a) decrease working capital and (b) decrease

4.

20-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5.

6. a. Decrease. Customers will be incentivized to pay early.

b. Increase. Less inventory turnover means more product on the shelf.

20-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

c. Decrease. This should decrease the inventory period.

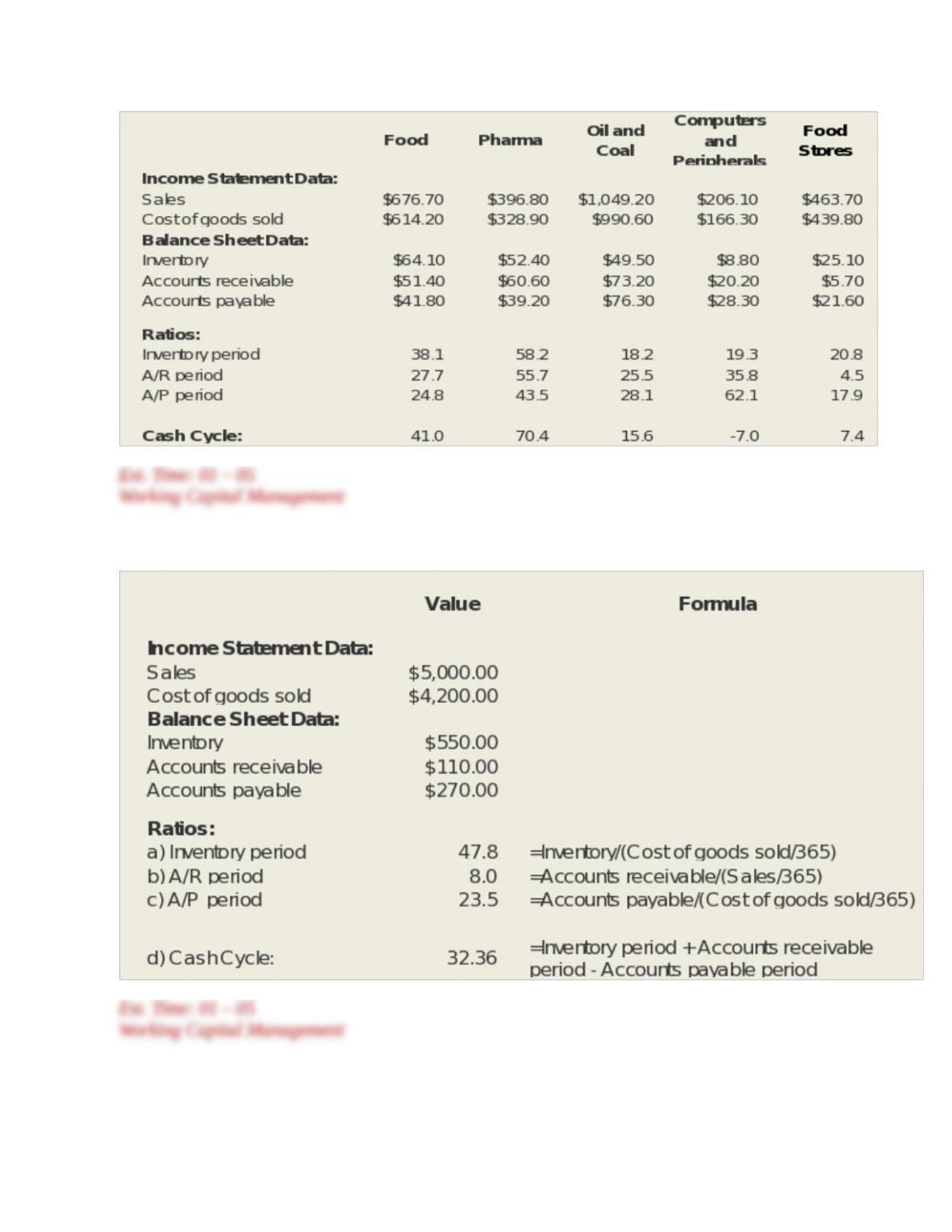

7. Inventory period = $10,000 / [(.80 × $800,000) / 365] = 5.70 days

Receivables period = $65,000 / ($800,000 / 365) = 29.66 days

8. Most goods are sold on open account. In this case the only evidence of the debt is a record

in the seller’s books and a signed receipt. An alternative is for the seller to arrange

9.

a. The service charge discourages late payment. The due lag decreases and, therefore, pay

lag decreases.

b. Companies might be forced to stretch payables. Due lag and, therefore, pay lag

10.

20-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

a. Firm A. Since the item sold can be reclaimed if payment is not made. Bread will be consumed

b. Firm A. Because the inventory turnover is lower (longer days in inventory). Rapid

c. Firm A. The firm selling to customers with the more tangible and salable assets will grant a

11.

a. The discount is 1% of $1,000 = $10.

b. The customer gains an extra 40 days of credit.

c. With the discount, the customer pays $990. Without the discount, the customer pays

12. The current terms allow a 3% discount if the customer gives up an extra 40 – 20 = 20 days

of credit. The effective annual rate is:

a. The implicit rate increases because the discount is higher:

b. The implicit rate increases because the extra days of credit “bought” by forfeiting

c. The implicit rate increases because the extra days of credit “bought” by forfeiting

13.

a. Two-thirds of customers pay within 15 days. The other one-third of customers pay by

20-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

b. Investment in A/R = accounts receivable period daily sales

million 096.1$

365

million 20$

20

c. With greater incentive to pay early, more customers will pay within 15 days instead of

14.

a. PV of a cash-on-delivery sale = $50 – $40 = $10 per carton

Under the present cash-on-delivery policy, unit sales equal 1,000 cartons per month:

$10 per carton 1,000 cartons = $10,000

b. If the interest rate is 1.5%, PV per carton decreases to:

c. The PV of the old customers remains unaffected. The PV of the new customers is

positive: The additional sales gained by extending credit is 60 cartons. The profit

20-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

15. From the discussion in the text regarding financial ratios (see Chapter 4), important ratios

to consider are:

Cash flow/Total debt

Net income/Total assets

16. PV(REV) = $1,200

PV(COST) = $1,000

Slow payers have a 70% probability of paying their bills. The expected profit from a

sale to a slow payer is therefore:

17. The possibility of collecting a portion of the amount owed to the firm reduces the expected

loss from advancing credit to slow payers and reduces the incentive to pay for a credit

18.

a. For every $100 in current sales, Galenic has $5 profit (ignoring bad debts); this implies

costs of $95. If the bad debt ratio is 1%, then, per $100 sales, the bad debts will be $1

and actual profit will be $4, a net profit margin of 4%.

b. Sales will fall to 91.6% of their previous level ($9,160/$10,000), or to $91.60 per $100

of original sales. With a cost-to-revenue ratio of 95%, total costs (ignoring bad debts)

will be:

20-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

c. There are many reasons why the estimated and actual default rates may differ. For

example, the credit scoring system is based on historical data and does not allow for

d. If one of the variables in the proposed scoring system is whether the customer has

an existing account with Galenic, the credit scoring system is likely to be biased

19. PV(COST) = 96

PV(REV) = 101/1.01 = 100

a. The expected profit from a sale is:

b. At the break-even probability, expected profit equals zero:

c. A paying customer now represents a perpetuity of profits equal to:

20-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

It clearly pays to extend credit.

d. (p $400) – [(1 – p) $96] = 0 p = 0.194 = 19.4%

20-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.